Chapter 6: Client Acceptance, Preliminary Planning, and Materiality Planning for what can go wrong

1/57

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

58 Terms

Purpose for planning

to provide for the effective conduct of an audit

Why planning works

helps to keep audit costs reasonable, avoid misunderstanding with the client, and enable the auditor to obtain sufficient appropriate audit evidence.

Client business risk:

risk that the entity will fail to achieve its objectives or execute its strategies.

How can business risk arise?

from a variety of factors, including significant changes in industry conditions, events such as regulatory changes, or setting inappropriate objectives or strategies.

Engagement risk

is the extent of risk that the audit firm is willing to tolerate (called the firm’s risk tolerance in accepting or continuing with a client).

Risk of Material misstatement

is the risk that the financial statements are materially misstated prior to the audit.

RMM Calculation

= IR x CR x DR

What needs to be done before accepting an engagement?

new client investigation

What does the firm consider when doing a client investigation

Client's standing and financial stability. Consider external sources and technology.

Requirements of successor auditor

communicate with the predecessor auditor to evaluate if there are any reasons not to accept the engagement.

Permission must be obtained from the client to communicate with the predecessor auditor.

When should existing clients be evaluated

annually to determine if there are any reasons to not continue doing the audit.

Obtain an understanding of the terms of engagement

A clear understanding of the terms of the engagement should exist between the client and the public accounting firm.

Engagement letter points

Resources Required for the Engagement

The auditor should develop and document a strategy that sets the scope, timing and direction of the audit.

Staff Selection for engagement

appropriate staff is key to ensuring audit effectiveness and efficiency.

If the Auditor does not have expertise, the engagement should be declined.

Continuity of staff helps the firm maintain familiarity and close interpersonal relationships with the client.

Evaluations of staff selection

Evaluate the need for an outside specialist.

The use of a specialist does not affect the auditor's responsibility for an audit; the report should not refer to the use of a specialist

Evaluate whether internal audit work can contribute.

The auditor may use the internal auditor’s work or

The internal auditor function could provide direct assistance to the external auditor.

Evaluate reliance on other auditors.

If a client has multiple locations or subsidiaries, the audit firm may need to engage other auditors.

Understand the Entity and its environment and the Applicable Accounting Framework

Requires the auditor to obtain knowledge of the entity’s business and environment to assess the risk of material misstatement.

When the auditor gathers information to understand the entity and the environment, the focus is on?

Industry, regulatory and other factors

Organizational structure and ownership

Governance

The entity’s business model

Performance measures.

The process of identifying and assessing the risk of material misstatement

the auditor planning and performing risk assessment procedures to gather evidence and referring to information from other sources, including evidence from

(1) the client acceptance and continuance assessment,

(2) the auditors’ prior experience with the client as well as similar types of audits in the client’s industry and

(3) audit team discussions

Risk assessment procedure

designed for planning the audit so that the auditor can identify risks and develop an appropriate audit plan.

These procedures do not provide audit evidence.

No audit evidence just possible risks

Main risk assessment procedures

Inquires of management and others in the entity

Analytical procedures

Observation and inspection

Preliminary Analytical Review

help the auditor to better understand the client’s business and the client’s business risk.

Also used to identify areas that have high risks of misstatement as well as fraud risk.

What do preliminary tests reveal

unusual changes in ratios compared with those of prior years, or compared to industry averages.

Purpose of Calculate key ratios for the client’s business and

compare them with industry averages

To understand the client’s industry and business.

The purpose of calculating the debt-to-equity ratio and compare it with those of previous years and successful companies in the industry.

To assess going convern

The purpose of comparing the gross margin with those of prior years, looking for large fluctuations

To identify possible misstatements.

To plan nature, timing, and extent of further audit procedures.

Purpose of preparing common-sized financial statements.

To identify high-risk audit areas.

To aid in assessment of fraud risk

Purpose of comparing prepaid expenses and related expense accounts with those of prior years

To identify possible misstatements.

To plan nature, timing, and extent of further audit procedures

Misstatements

including omissions, are considered to be material if they, individually or in the aggregate, could reasonably be expected to influence the economic decisions of users taken based on the financial statements

What does materiality require

considerable professional judgment, and it is a relative rather than an absolute concept.

Determining overall materiality

Judgments are made in light of surrounding circumstances and are affected by the size or nature of a misstatement or a combination of both and

Judgments about what is material to users of the financial statements are based on the common financial statements are based on the common financial information needs of users as a group, not on each user individually.

Materiality and planning the audit

Decisions during the planning phase provide benchmarks for decisions throughout the audit about:

Overall FS or planning Mateality (M)

Performance materiality (PM)

Specific Materiality (SM)

Specific performance materiality (SPM)

Determine Overall Materiality

Overall materiality refers to determining materiality for the financial statements as a whole.

Steps in determining overall materiality (MUST USE)

Identify the Key users of the FS (Stick to case facts)

Identify users objectives

Selecting an appropriate benchmark

Determining the percentage to be applied to the selected benchmark

Calculate materiality

Determine and calculate performance materiality

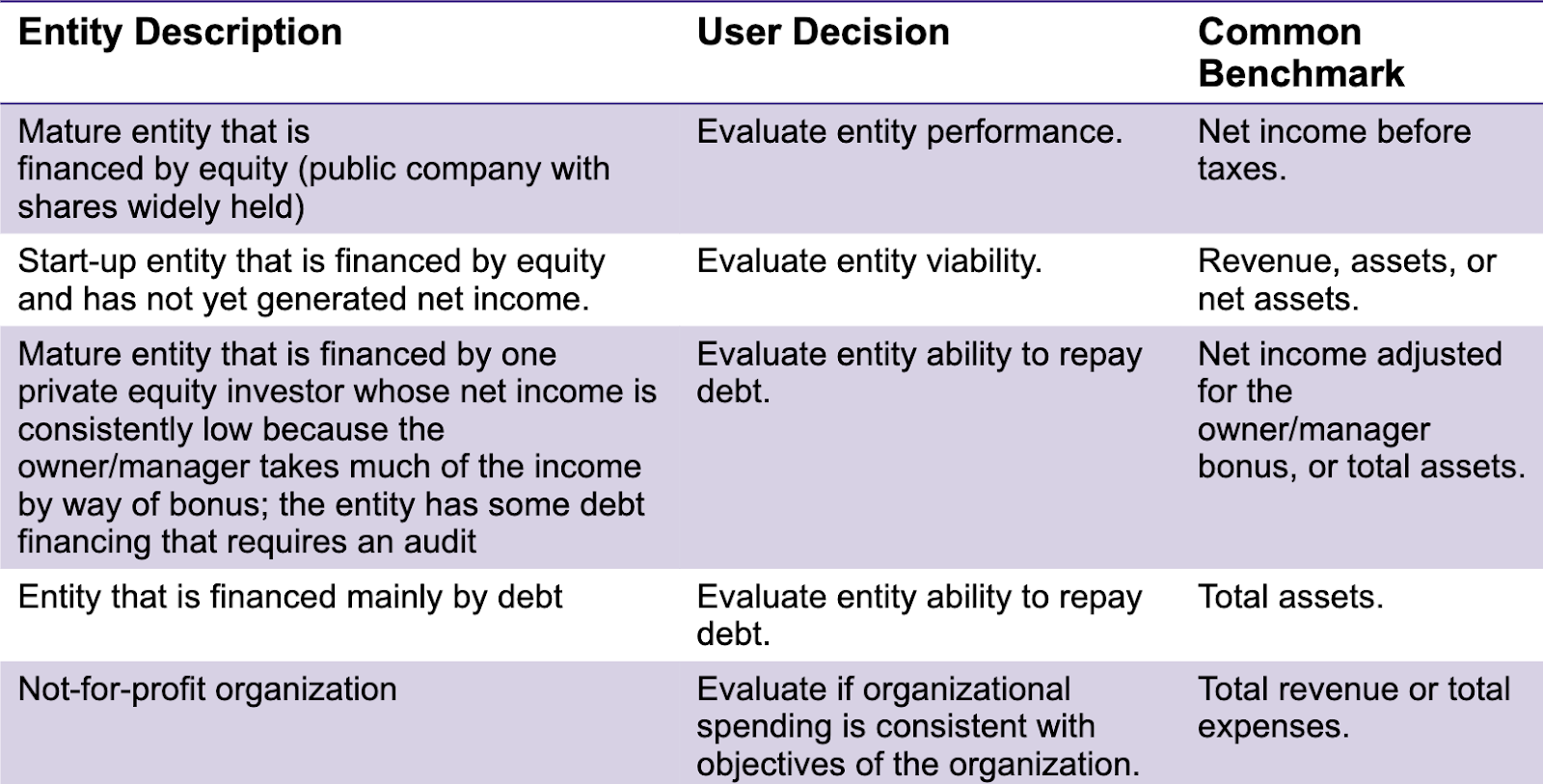

Types of Benchmark

revenue, normalized profit before taxes ( adjust for non-recurring items), total assets, and expenses.

Judgment around selecting benchmarks

understanding what the users are most likely concerned about.

Common materiality Benchmarks

For-profit entities Rules of thumbs for calculating materiality

3% to 7% of income from continuing operations before taxes (this may need to be normalized)

1% - 3% of Total Assets

3% to 5% of shareholders’ equity

1% to 3% of revenue

non-for-profit entities Rules of thumbs for calculating materiality

1% to 3% of revenue

1% to 3% of expenses

1% to 3% of total assets

When to use NIBT

entity is at net loss & users look at profitability

Determining the Bench Mark Percentage

The % chosen is a function of the organization and the users’ needs (i.e. how sensitive are the users to errors in the FS?)

Performance Materiality (PM)

is an amount less than the overall materiality, that, Reduces aggregation risks and Provides a safety buffer against risk of undetected misstatements

How is the performance materiality set

as a percentage of over-materiality, The more errors uncovered the more questions that ended up being asked and usually 50% (high RMM) and 75% (Low RMM)

Perfomance materiality factors

First year audit

Fraud risks

weak control environment,

history of identified misstatements in prior year audits

history of significant misstatements in prior audits

increased number of accounting issues that require significant judgment or estimates with high uncertainty

Management under significant pressure

First year audit

Auditors typically set performance materiality lower for new clients since they have no prior experience.

Fraud risks

These factors all increase the risk of intenational material misstatements

weak control environment

Errors are more likely in this type of environment

history of identified misstatements in prior year audits

Unless changes have been made, there is a risk that misstatements will continue to occur.

history of significant misstatements in prior audits

Poor controls over processing transactions increases the risk of errors occurring

increased number of accounting issues that require significant judgment or estimantes with high uncertainty

A high degree of complexity and subjectivity increases the potential for misstatements

Management under significant pressure

Pressure can lead to management being bias in application of accounting policies

Specific materiality (SM)

is a materiality level based upon a specific group of users’ needs and determined for a particular class of transactions, account balance, or disclosure

Requirements of threshold for specific materiality

it must be equal to or less than performance materiality

Specific performance materiality (SPM)

is less than overall performance materiality and is calculated based on specific materiality.

Accumulating Misstatements During the Audit

requires the auditors to request uncorrected misstatements be corrected.

Misstatements can be categorized as

Factual misstatements

Jugmental misstatemetns

Project misstatements

Factual misstatements

those about which there is no doubt

Jugmental misstatemetns

differences in management’s judgment concerning recognition, measurement, presentation and disclosure in the FS and the auditor’s judgment

projected misstatements

the auditor’s best estimate based upon a sample

Forming an Overall Opinion and Reporting

The auditor concludes with the overall reasonableness of the financial statements using the bench mark of overall materiality.

If a misstatement is not corrected, the auditor’s report will be affected by whether the misstatement is materially pervasive or can be isolated to specific accounts or disclosures.

Requires that the auditor communicates with those in charge of government with respect to incorrect misstatements and their impact on the auditors’s report.