EC 202- 5,6,7,8

1/71

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

72 Terms

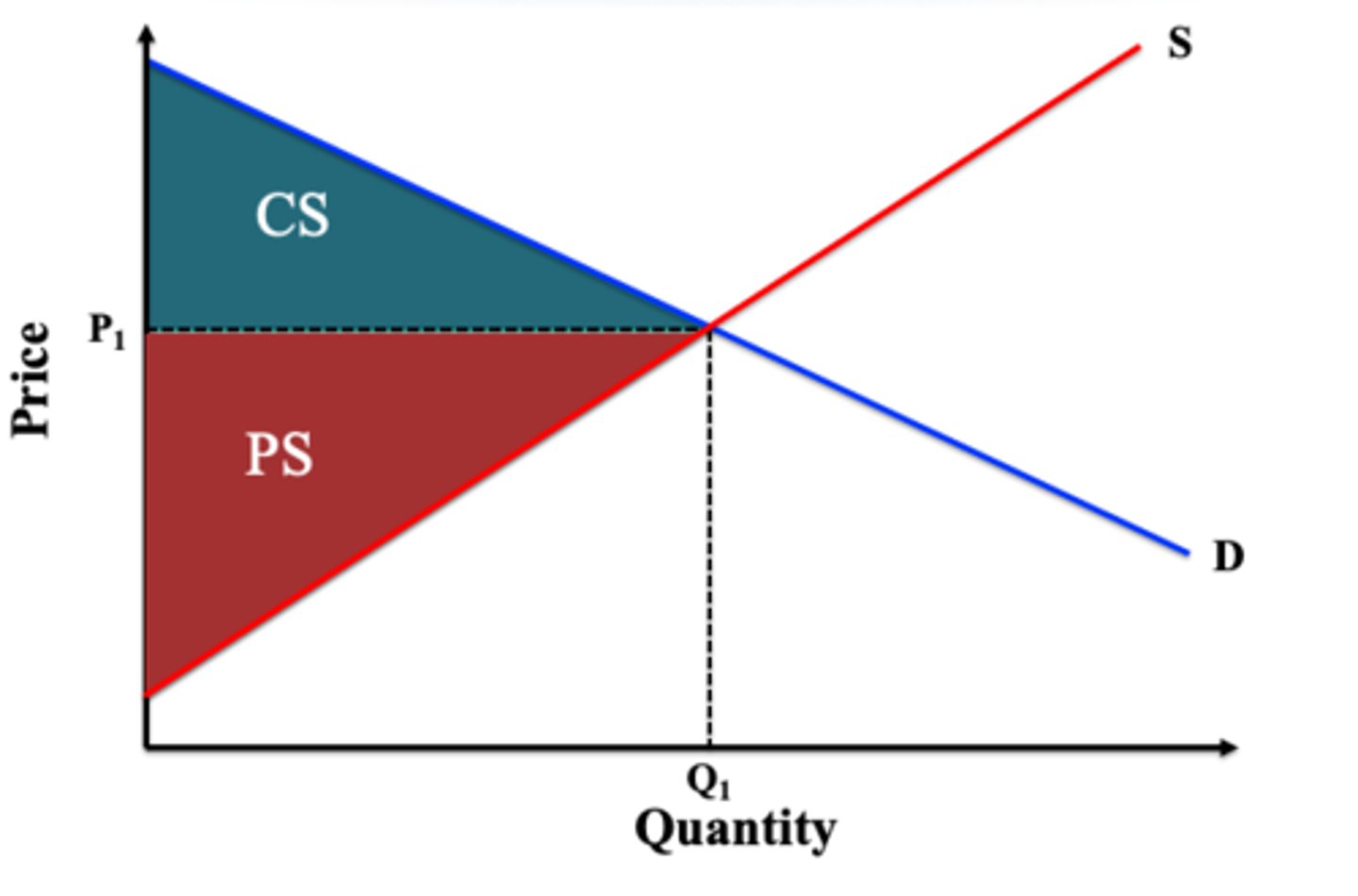

producer surplus

The difference between the price producers receive for a good or service and the minimum price they are willing and able to accept

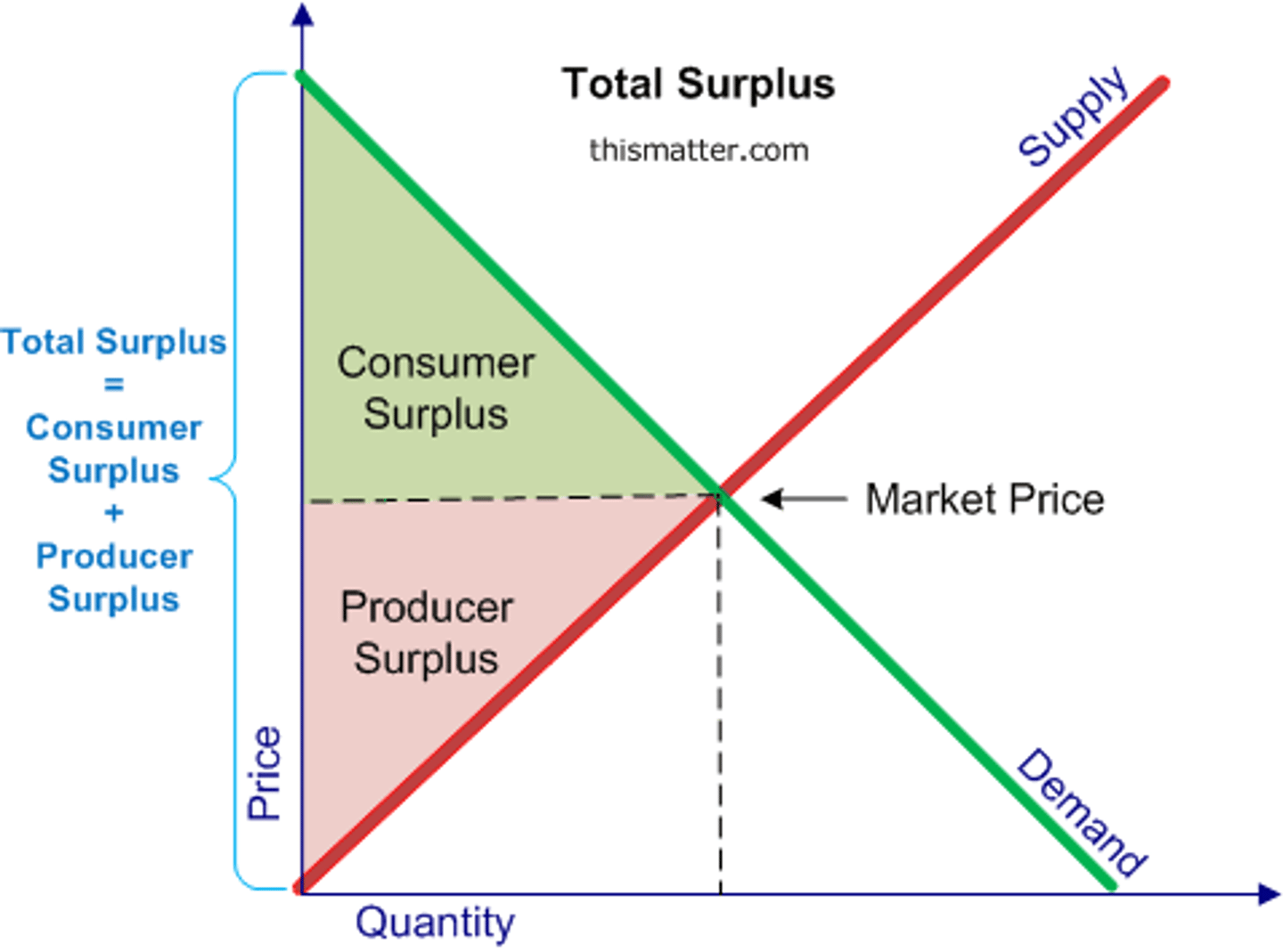

economic surplus

The sum of consumer and producer surplus; total welfare

welfare at equilibrium

welfare at a higher price

welfare at a lower price

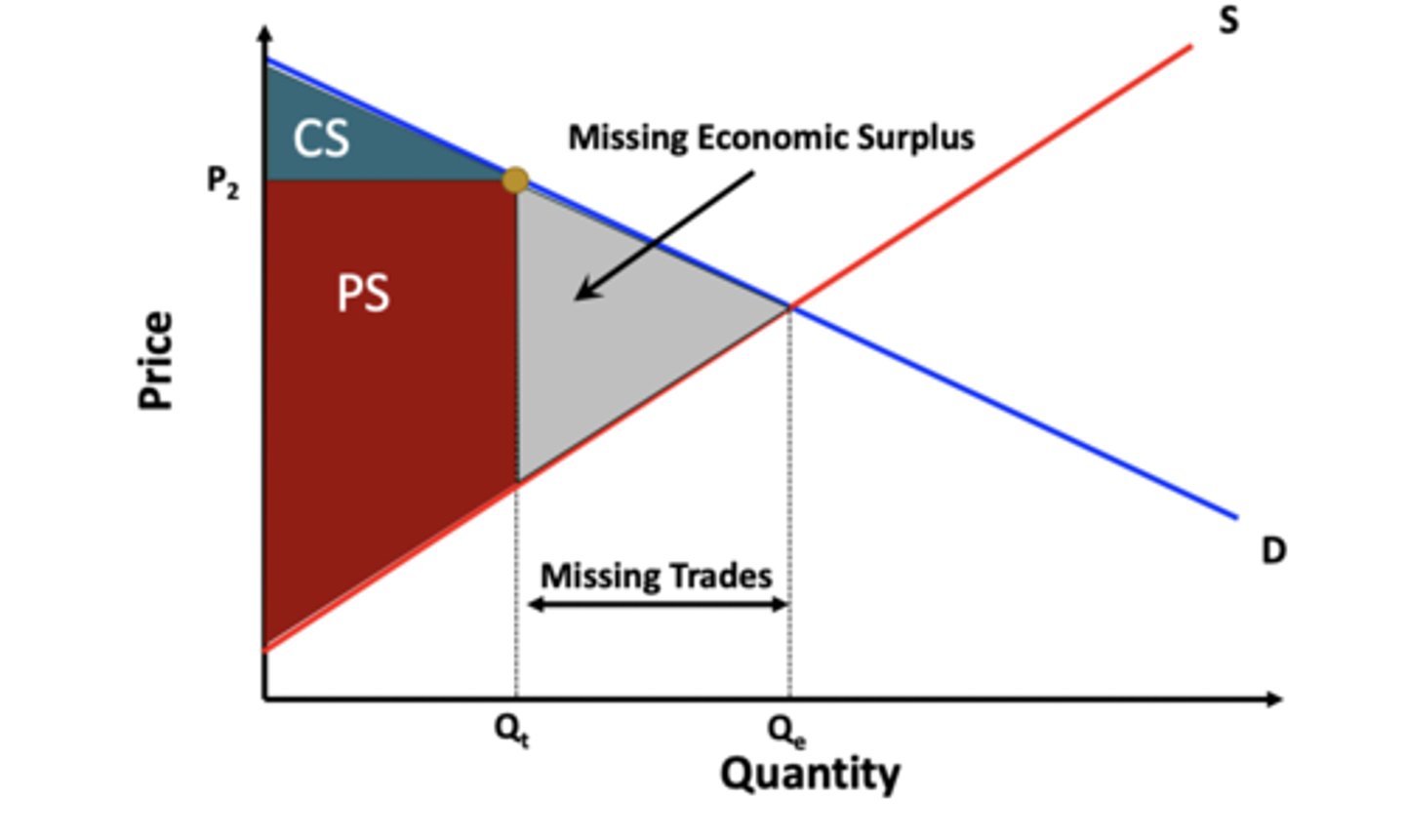

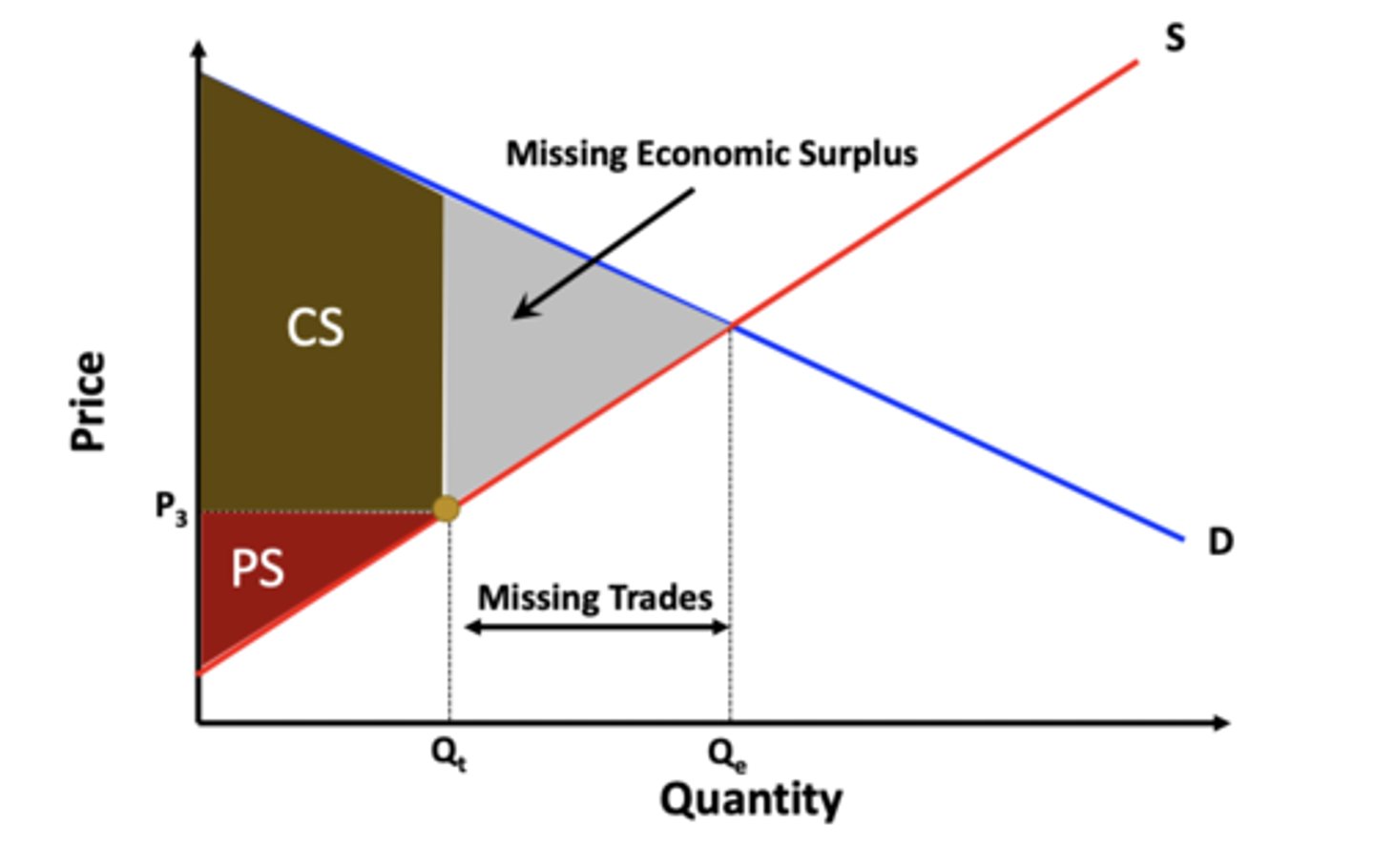

deadweight loss

The value of the economic surplus that is foregone when a market is not allowed to adjust to its competitive equilibrium

A deadweight loss _____________ as tax rates change.

changes

Suppose the equilibrium price is $50. If the actual price paid by the buyer is $60 for one item, and the minimum acceptable price to the seller is $40, then

there is a deadweight loss

Productive Efficiency

Producing output at the lowest possible average total cost of production; using the fewest resources possible to produce a good or service

Allocative Efficiency

Producing the goods and services that are most wanted by consumers in such a way that their marginal benefit equals their marginal cost

Which of the following is not correct when describing allocative efficiency?

A) It occurs where marginal benefit equals marginal cost.

B) It occurs when the right amount of goods and services are produced

.C) It occurs when total surplus is maximized.

D) It occurs when firms produce at the lowest possible average total cost.

D) It occurs when firms produce at the lowest possible average total cost

If the market is in equilibrium, which of the following occurs?

A) Gains from trade are maximized, economic surplus is maximized, allocative efficiency is achieved, and productive efficiency is achieved.

B) Gains from trade are maximized, economic surplus is maximized, allocative efficiency is not achieved, and productive efficiency is achieved.

C) Gains from trade are maximized, economic surplus is maximized, allocative efficiency is achieved, and productive efficiency is not achieved.

D) Gains from trade are lowered, economic surplus is reduced, allocative efficiency is achieved, and productive efficiency is achieved

A) Gains from trade are maximized, economic surplus is maximized, allocative efficiency is achieved, and productive efficiency is achieved

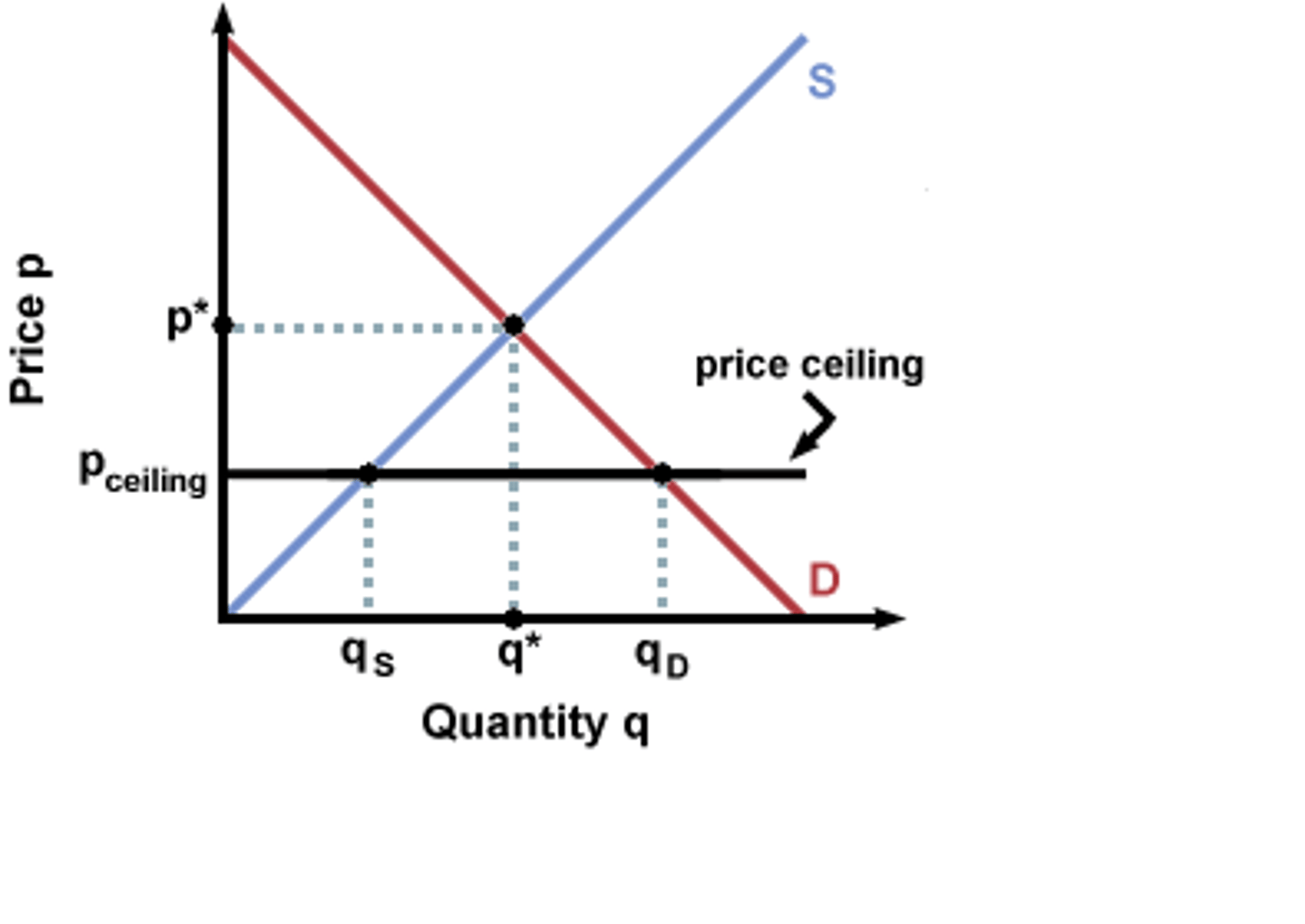

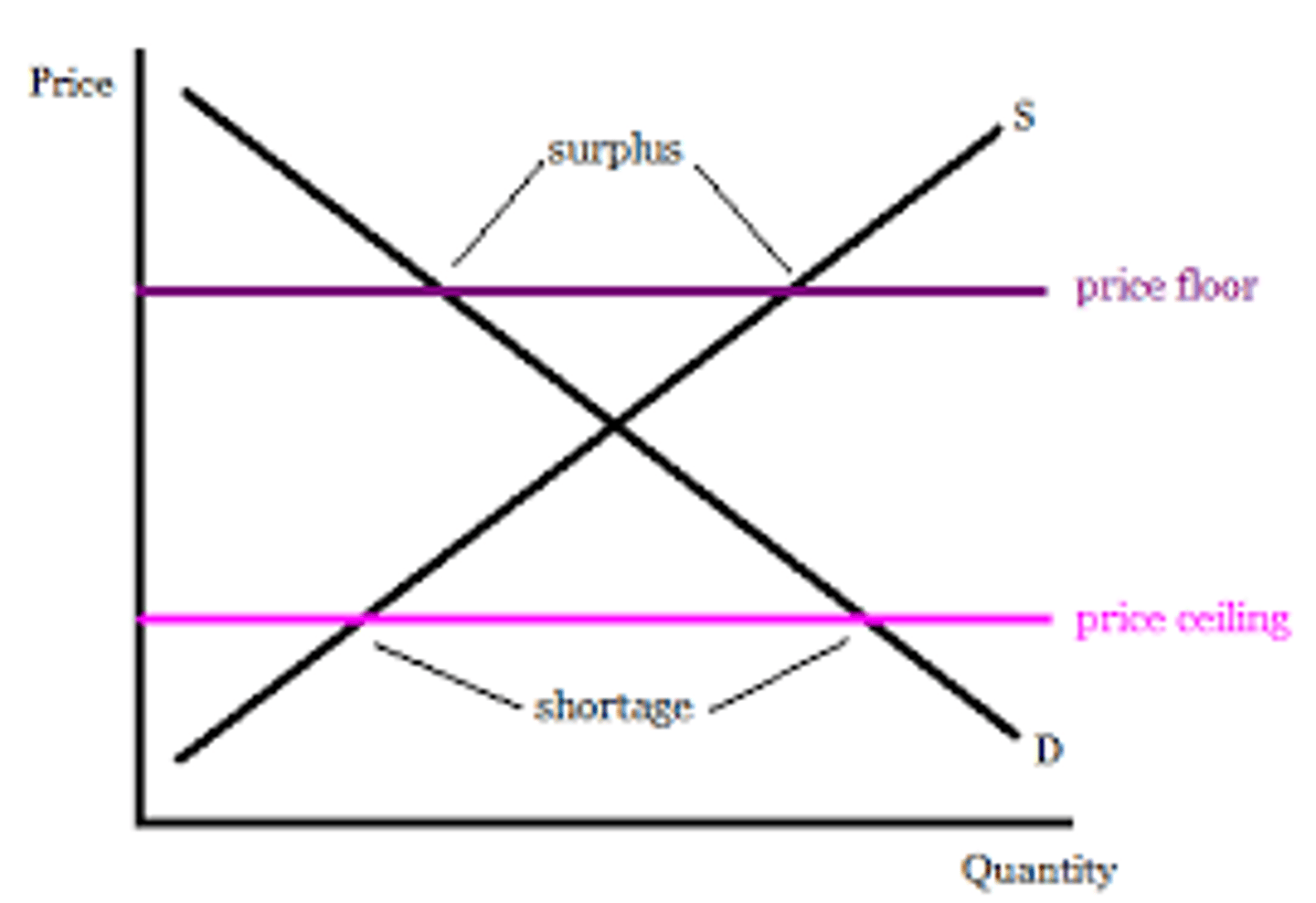

price ceiling

a maximum price that can be legally charged for a good or service

Which of the following correctly describes the social welfare impact of a price ceiling?

A) All consumers win.

B) A deadweight loss occurs.

C) All producers win.

D) Total surplus is increased.

B) A deadweight loss occurs

price floors

government imposed limits on how low a price can be charged

Which of the following correctly describes the social welfare impact of a price floor?

A) Total surplus is decreased.

B) All producers lose.

C) There is no deadweight loss.

D) All consumers win

A) Total surplus is decreased

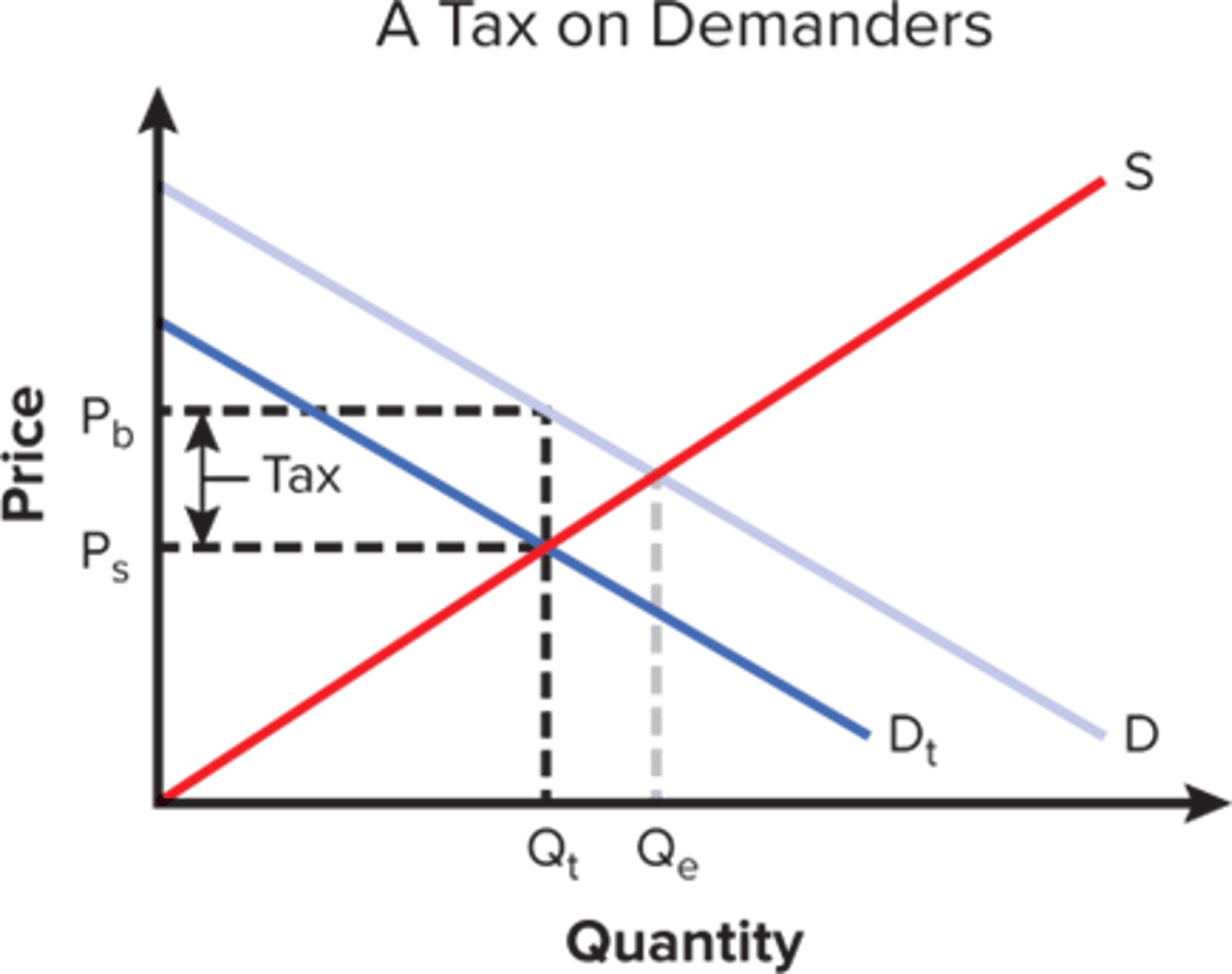

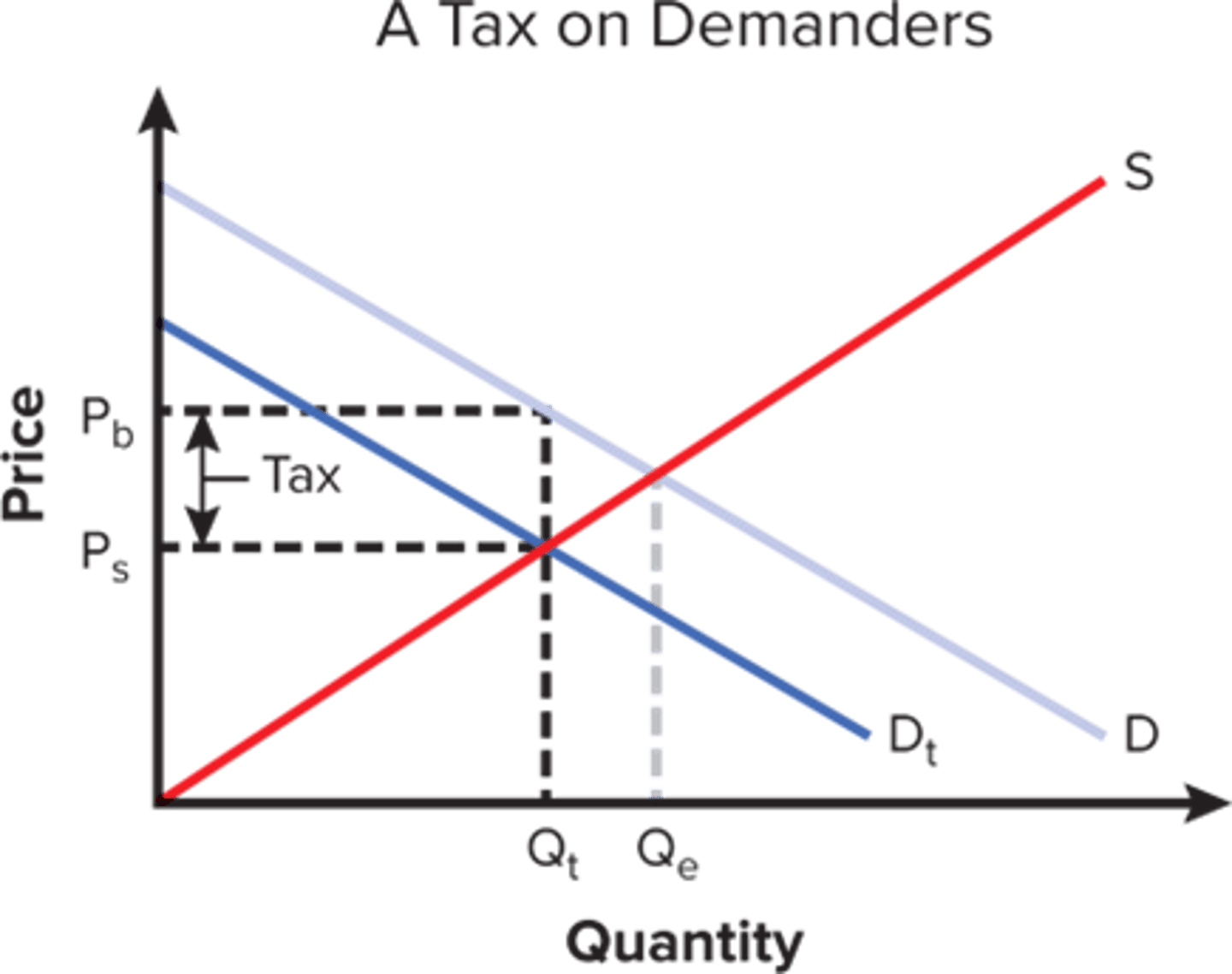

a tax on demanders

shifts the demand curve to the left

Without taxes, a market moves to _______ and _______ surplus is maximized.

equilibrium; economic

welfare types

tax revenue + consumer surplus+ producer surplus + DWL

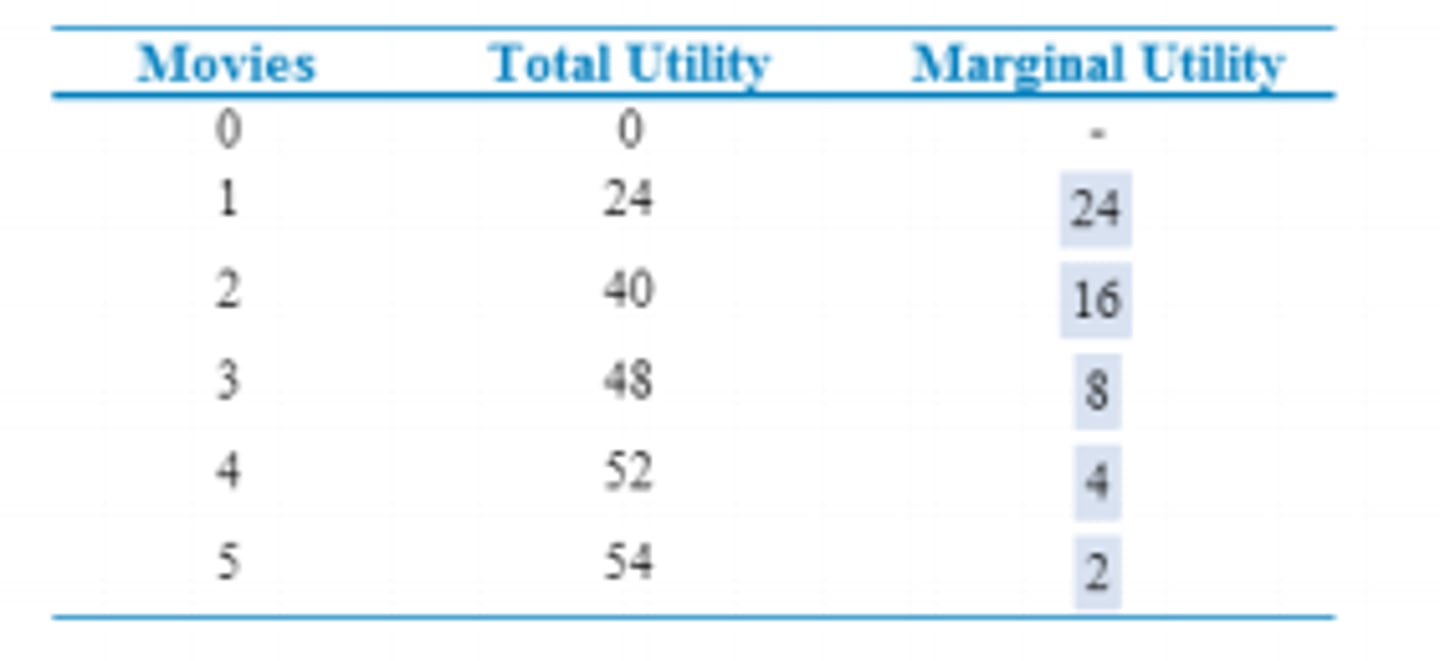

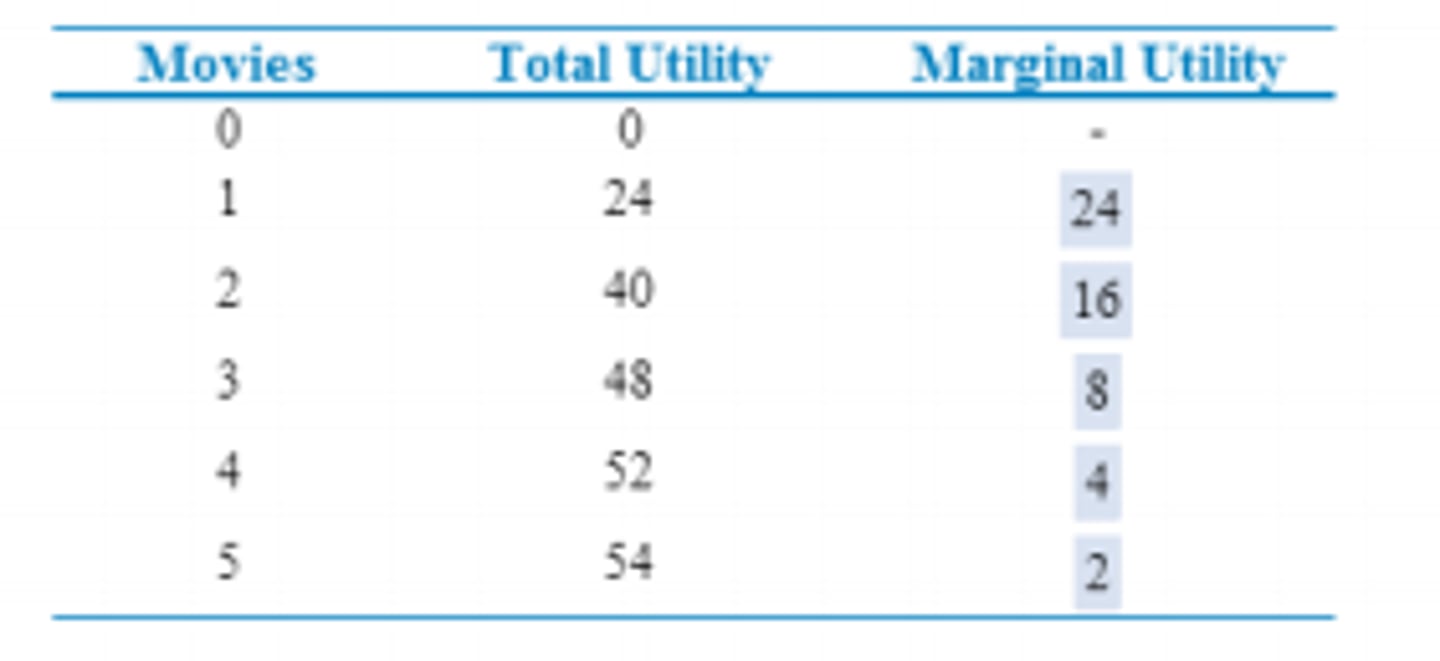

marginal utility

The additional satisfaction or happiness received from the consumption of an additional unit of a good or service; dividing the change in total utility by the change in the total number of units consumed

total utility

The total satisfaction or happiness received from the consumption of a good, service, or combination of goods and services; calculated by adding up the marginal utility (MU) of each unit consumed

Marginal utility is

A) negative, but never positive.

B) positive or negative, but never zero.

C) positive, negative, or zero.

D) increasingly negative

C) positive, negative, or zero.

The demand curve is downward sloping because

marginal utility decreases as more of a product is

consumed

If total utility is decreasing, marginal utility

is negative.

Utility Maximization

The process of obtaining the greatest level of overall satisfaction or happiness from consuming goods and services, subject to consumers' preferences, incomes, and prices

The theory of consumer behavior assumes that

consumers behave rationally, maximizing their

satisfactions

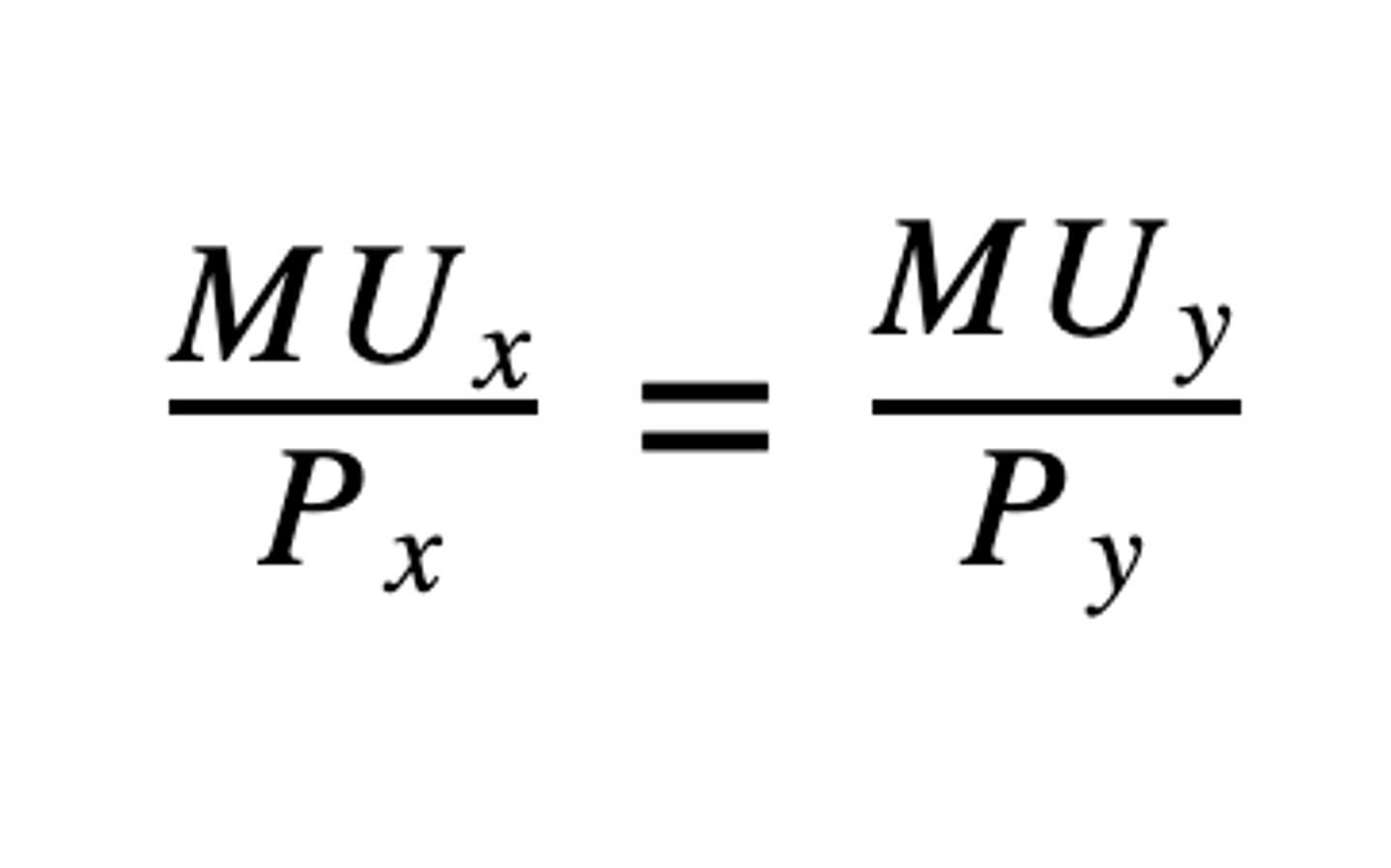

Equal Marginal Principle

Consumers utility is maximized utility when they allocate their limited incomes so that the marginal utility per dollar spent on each of their final choices in a bundle is equal

equal marginal principle formula

MU_x/P_x = MU_y/P_y:

MU_x: Marginal utility derived from good X

MU_y: Marginal utility derived from good Y

P_x: Price of good X

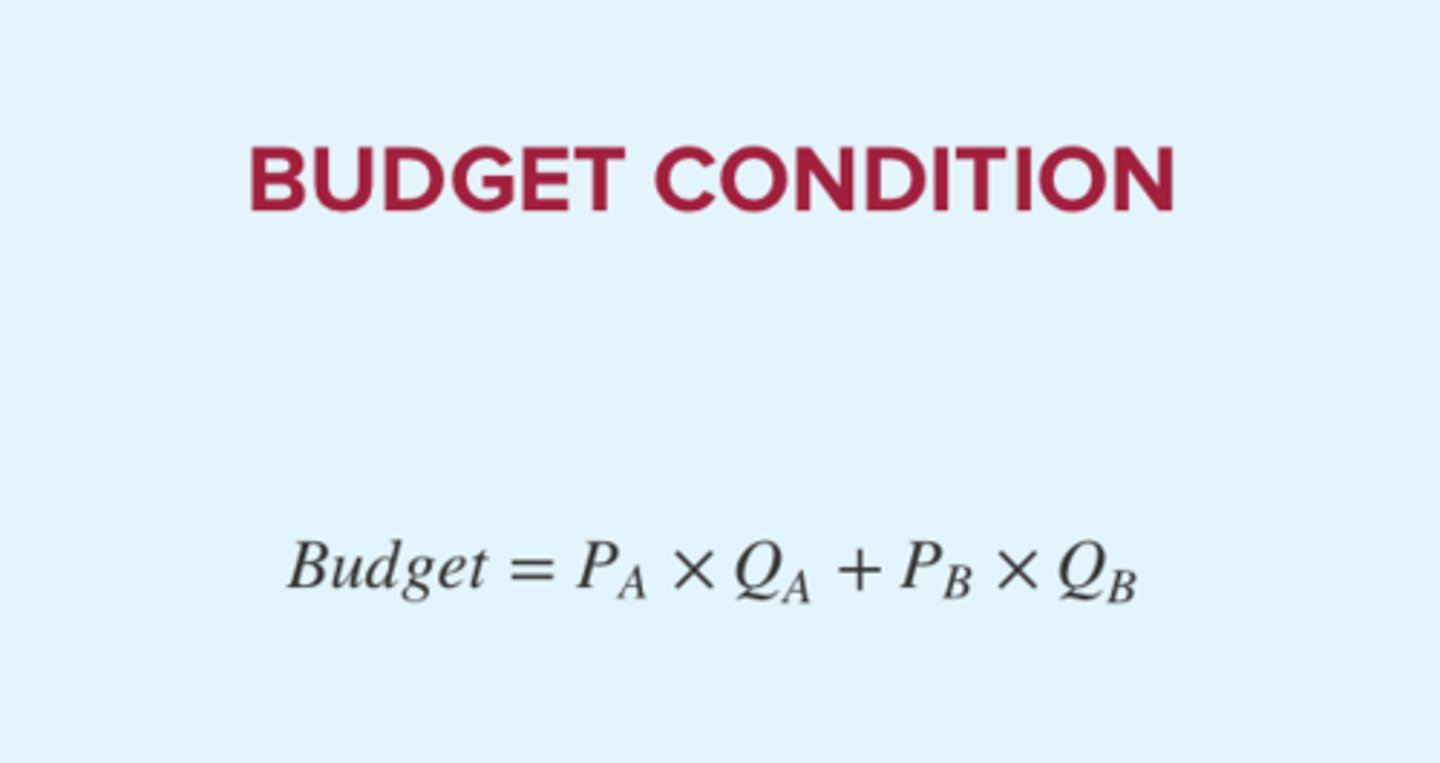

Budget Line

A line showing the different combinations of two products that can be purchased with a given budget and at a known set of prices

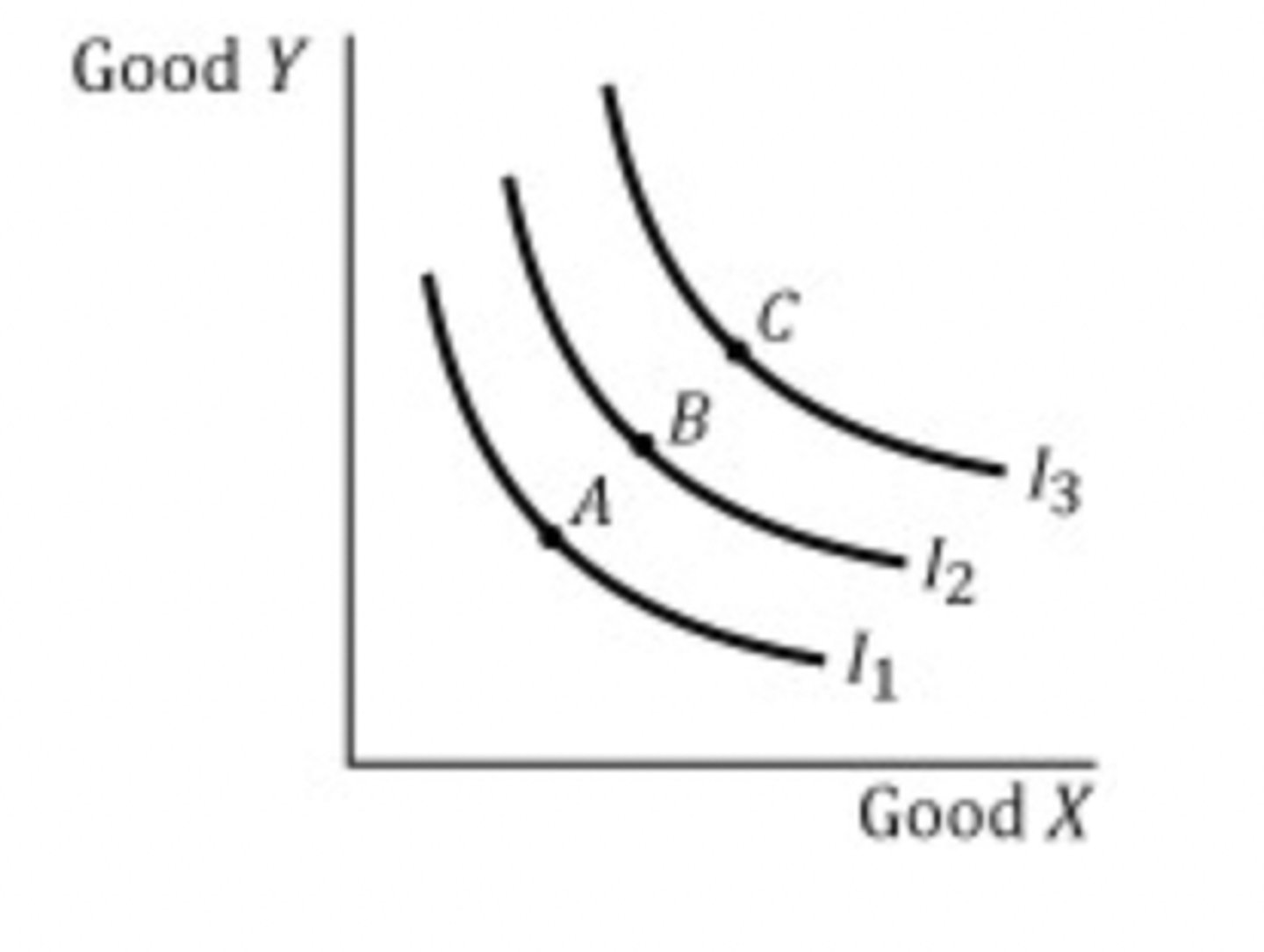

Indifference Curves

A curve that shows the combinations of two products that generate the same amount of total utility or satisfaction

Characteristics of Indifference Curves

• Indifference curves are downward-sloping.

• Indifference curves further from the origin are preferred to

those closer to the origin. (higher utility value)

• Indifference curves cannot cross.

• All combinations on the curve provide the same utility as other

combinations on the curve

Indifference curves show the ________ of combinations of two products

total utility

Explicit Costs

Monetary payments made by individuals, firms, and

governments for the use of land, labor, capital, and

entrepreneurial ability owned by others. Also known as

accounting costs.

Explicit Costs

are there ever zero explicit costs?

no; opportunity cost always

Implicit Cost

The opportunity costs of using owned resources; costs

for which no monetary payment is explicitly made.

Generally, accounting profits are

greater than economic profits, because accounting profits

do not consider implicit costs

Increasing Marginal Returns

A characteristic of production whereby the marginal product of the next unit of a variable resource utilized is greater than that of the previous variable resource

Diminishing Marginal Returns

A characteristic of production whereby the marginal

product of the next unit of a variable resource utilized is less than

that of the previous variable resource

Marginal product

) usually increases then decreases and may become

negative

When total product is rising

marginal product is positive.

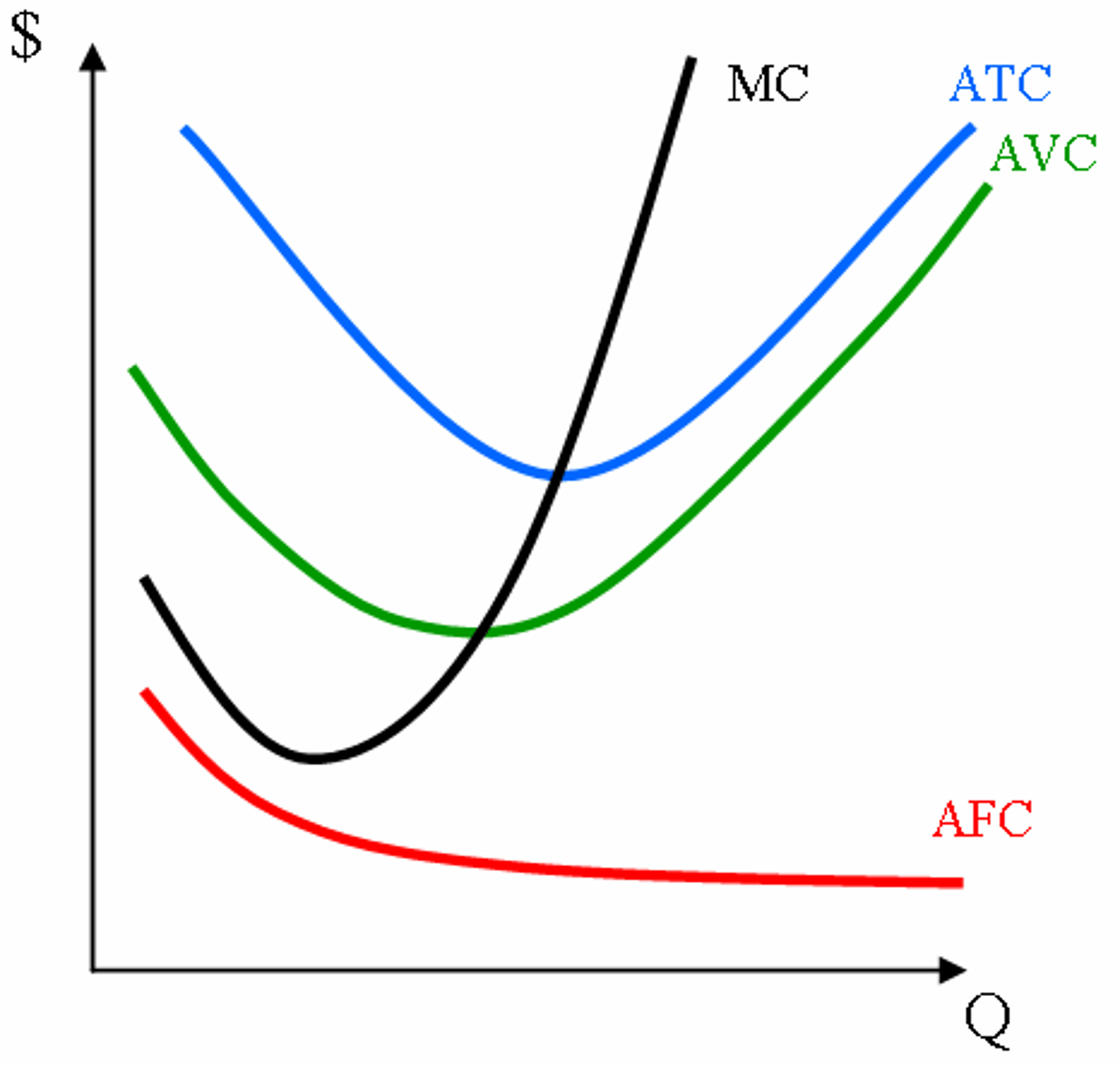

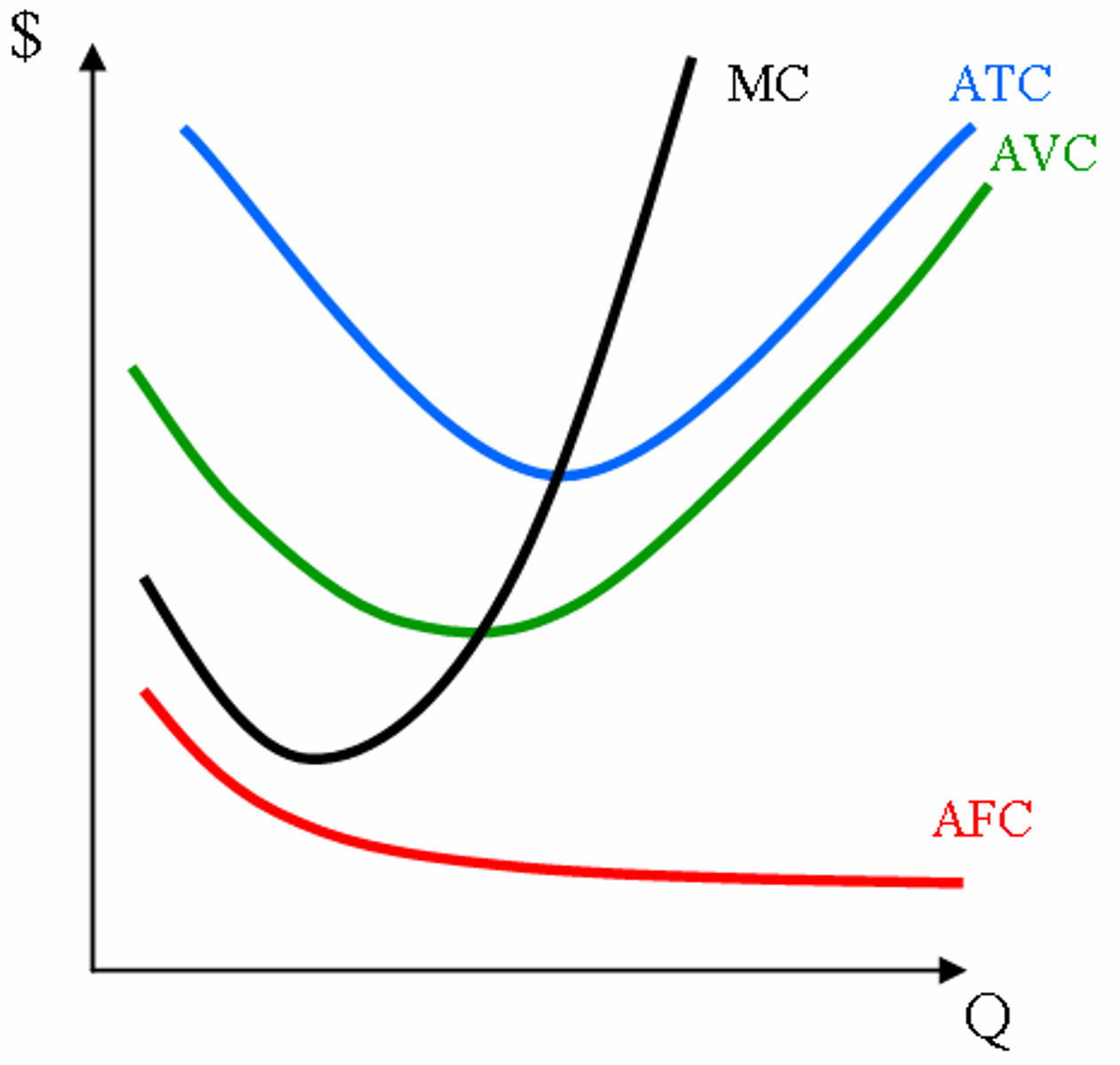

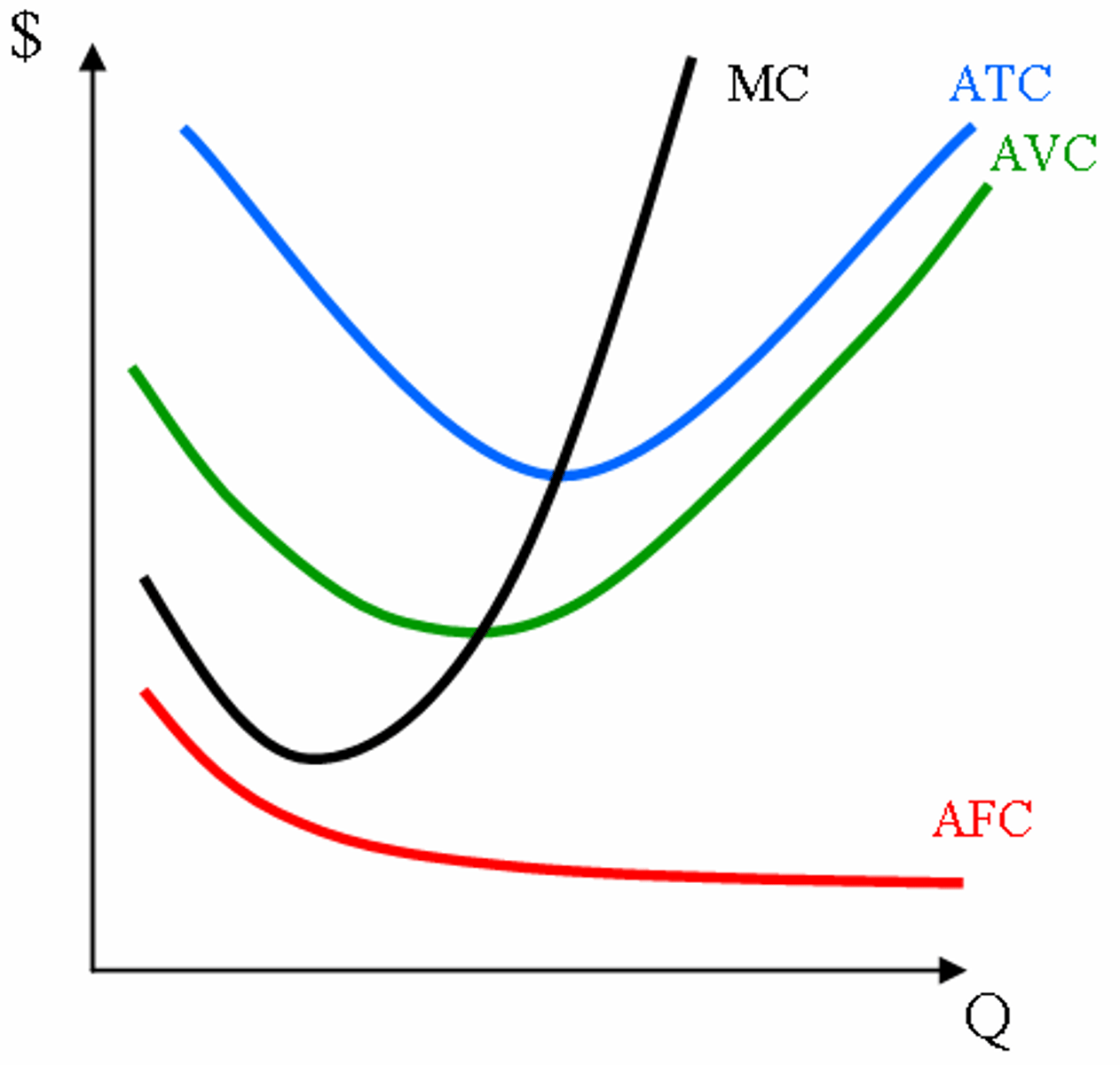

Average fixed cost

A) equals marginal cost when average variable cost is at its

minimum value.

B) is total variable cost divided by the number of units of

output.

C) declines and then rises in a U-shape as output expands.

D) declines continually as output expands

declines continually as output expands.

average total cost

total cost divided by the quantity of output

average variable cost

total variable cost divided by the quantity of output

average fixed cost

total fixed cost divided by the quantity of output

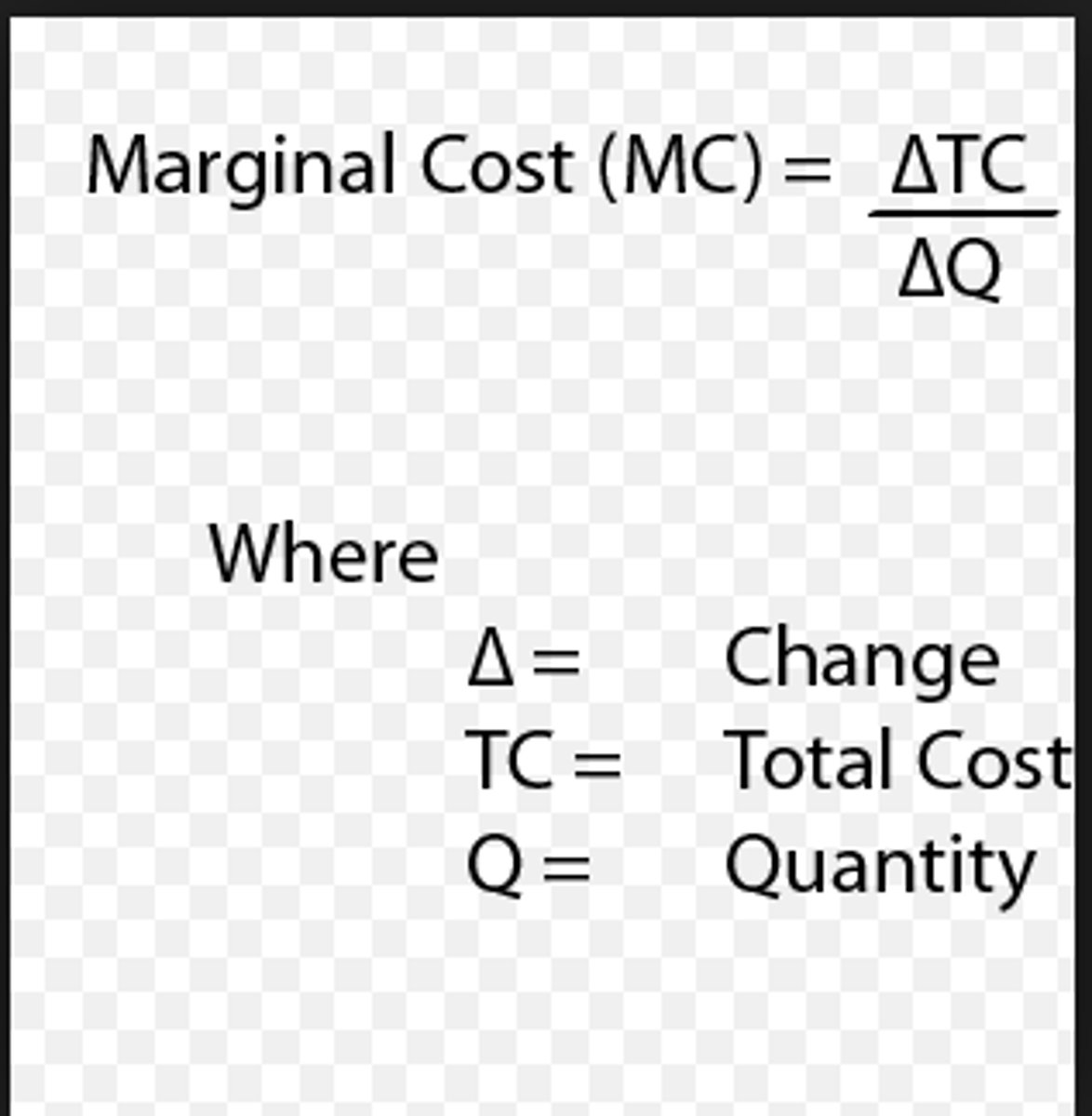

Marginal Cost

The additional cost associated with one more unit of

an activity. For production, it is the change in total cost due to the

production of one more unit of output

Situation: You currently have a 68% free throw completion

average (68/100) for the season. Your completion rate for the

next two games will impact your new average.

• Game 1: You complete 8/10 free throws for an 80% completion

rate. Will your seasonal average increase, decrease, or stay the

same?

Answer: Increase. Your game rate was 80% which is higher than

your season average.

- New season average: (68 + 8)/(100 + 10) = 69.1%

LRATC Curve

A curve showing the lowest average total cost possible

for any given level of output when all inputs of production are

variable

Which of the following statements describes a difference

between the short run and the long run?

A) The law of diminishing returns is an issue in the long run

but not in the short run.

B) All resources are fixed in the short run, and all resources

are variable in the long run.

C) Some resources are fixed in the short run, and all

resources are variable in the long run.

D) Variable costs are more important for decision making in

the short run than in the long run

All resources are fixed in the short run, and all resources are variable in the long run.

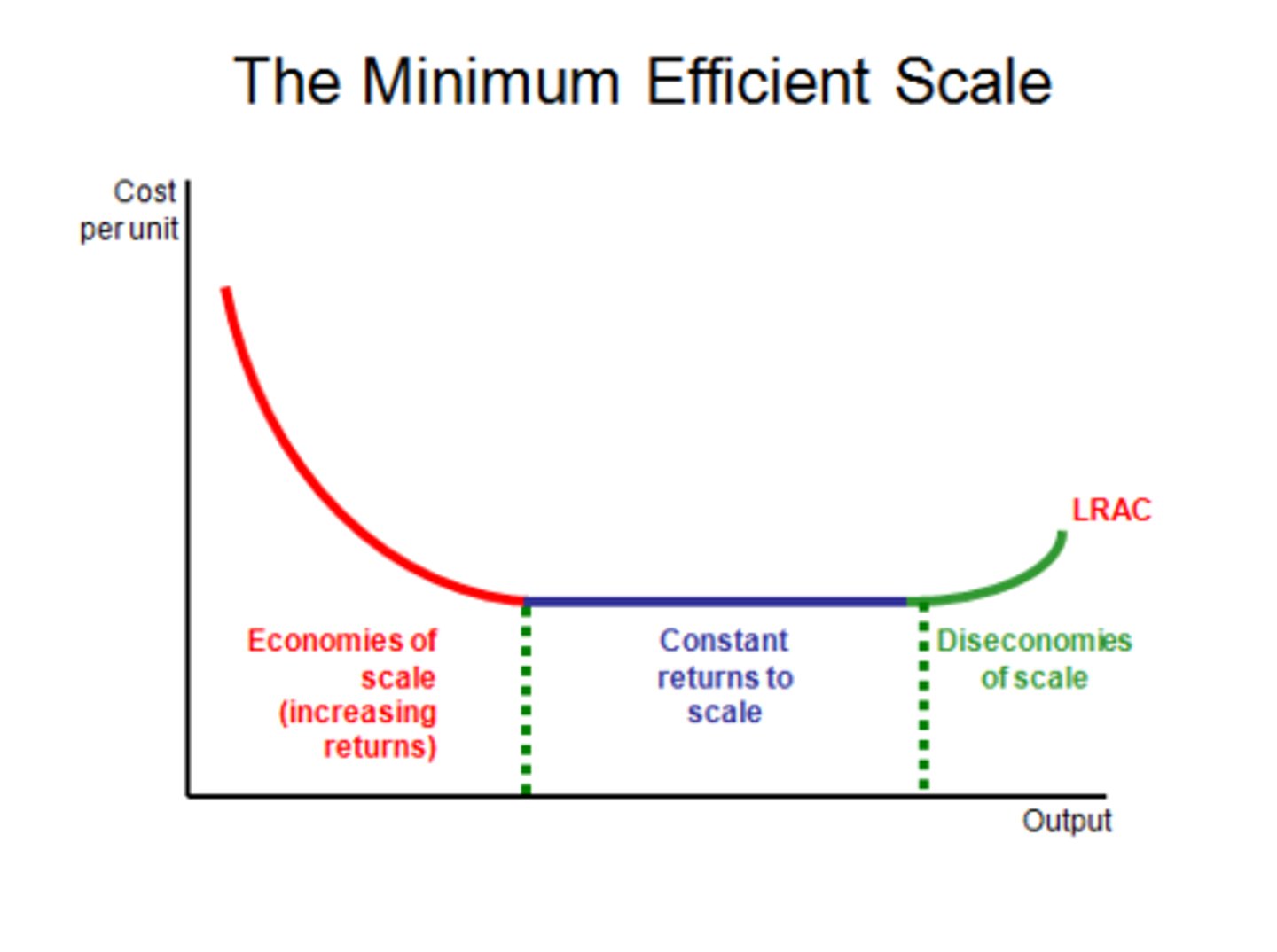

Economies of Scale

A condition in which the long-run average total cost of

production decreases as production increases

Constant Returns to Scale

A condition in which the long-run average total cost of

production remains constant as production increases

Diseconomies of Scale

A condition in which the long-run average total cost of

production increases as production increases

LRATC Curve (scale)

One reason a firm may experience economies of scale is

the firm experienced specialization in labor and management

A firm is experiencing diseconomies of scale if

costs increase as output expands.

Perfect Competition Characteristics:

- Large number of buyers and sellers

- Standardized/homogeneous product

- Price takers / No price control

- Easy entry and exit

- Perfect information on the market

Marginal Revenue

The change in a firm's total revenue that results from a one-unit change in output produced and sold

Average Revenue

Revenue per unit sold, equal to total revenue divided

by the quantity of output produced and sold

How Does a Perfectly Competitive Firm Respond to Changes in Market Prices?

raises cost and revenues; MR line shifts up

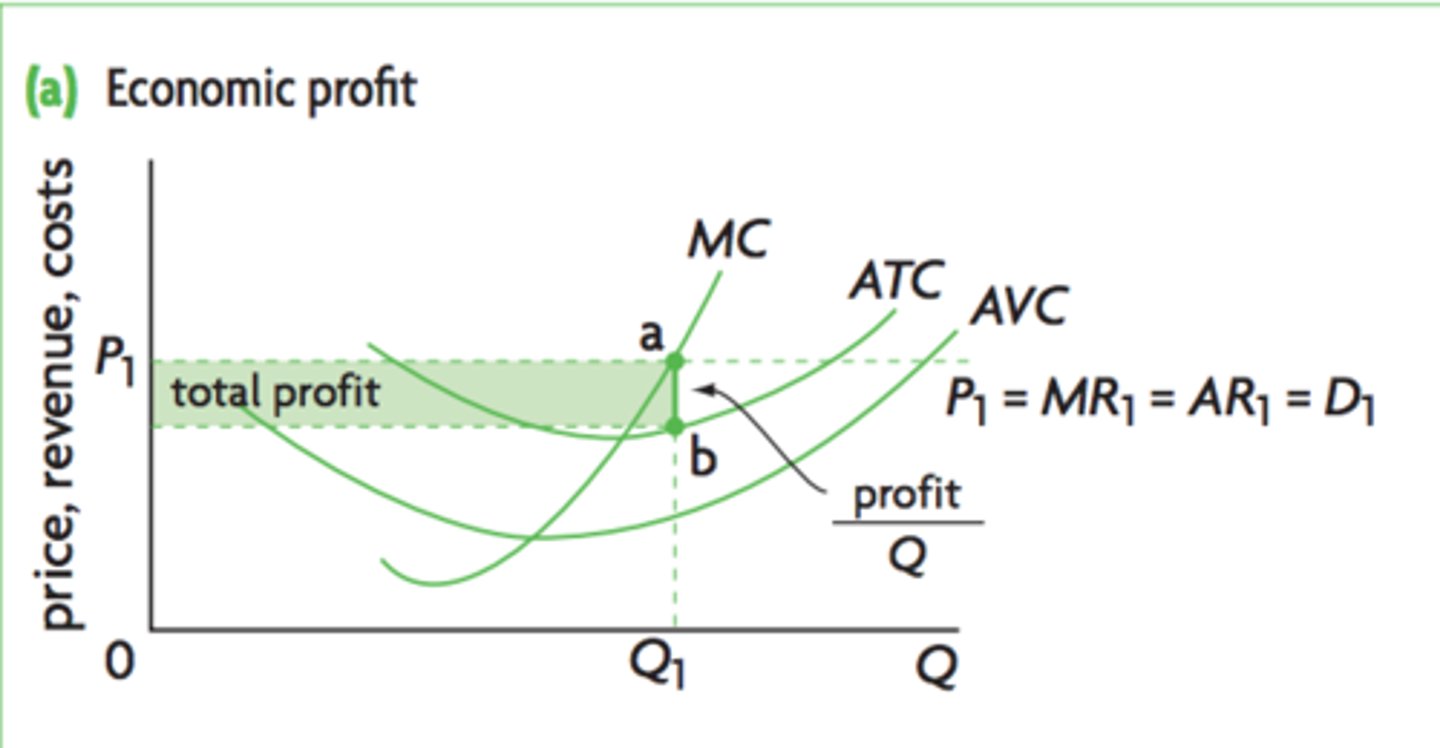

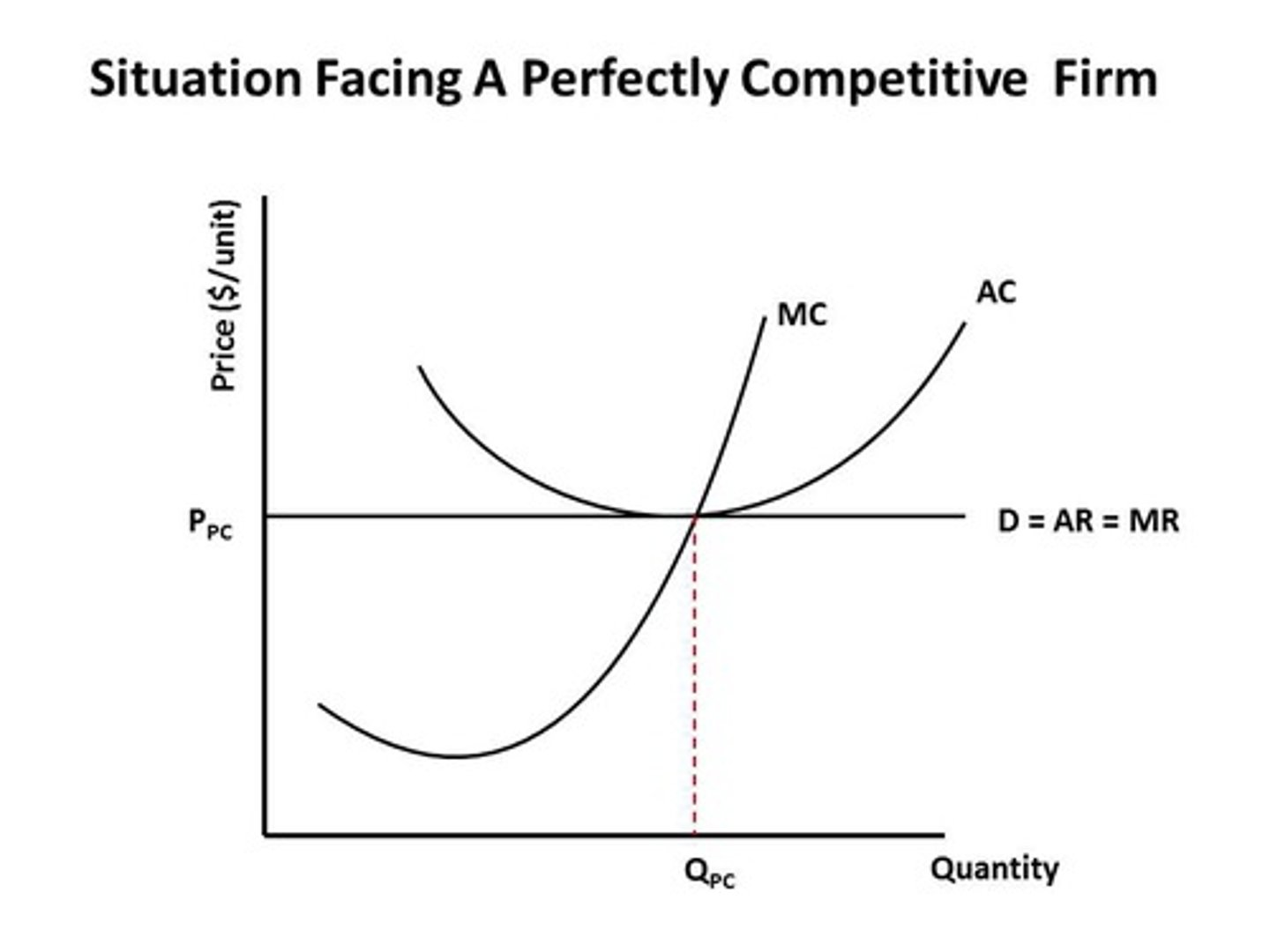

Determining Short-Run Economic Profits for a Perfectly Competitive Firm

Determining Normal Profits for a Perfectly Competitive Firm

In a perfectly competitive industry, firms seek to maximize

total profit

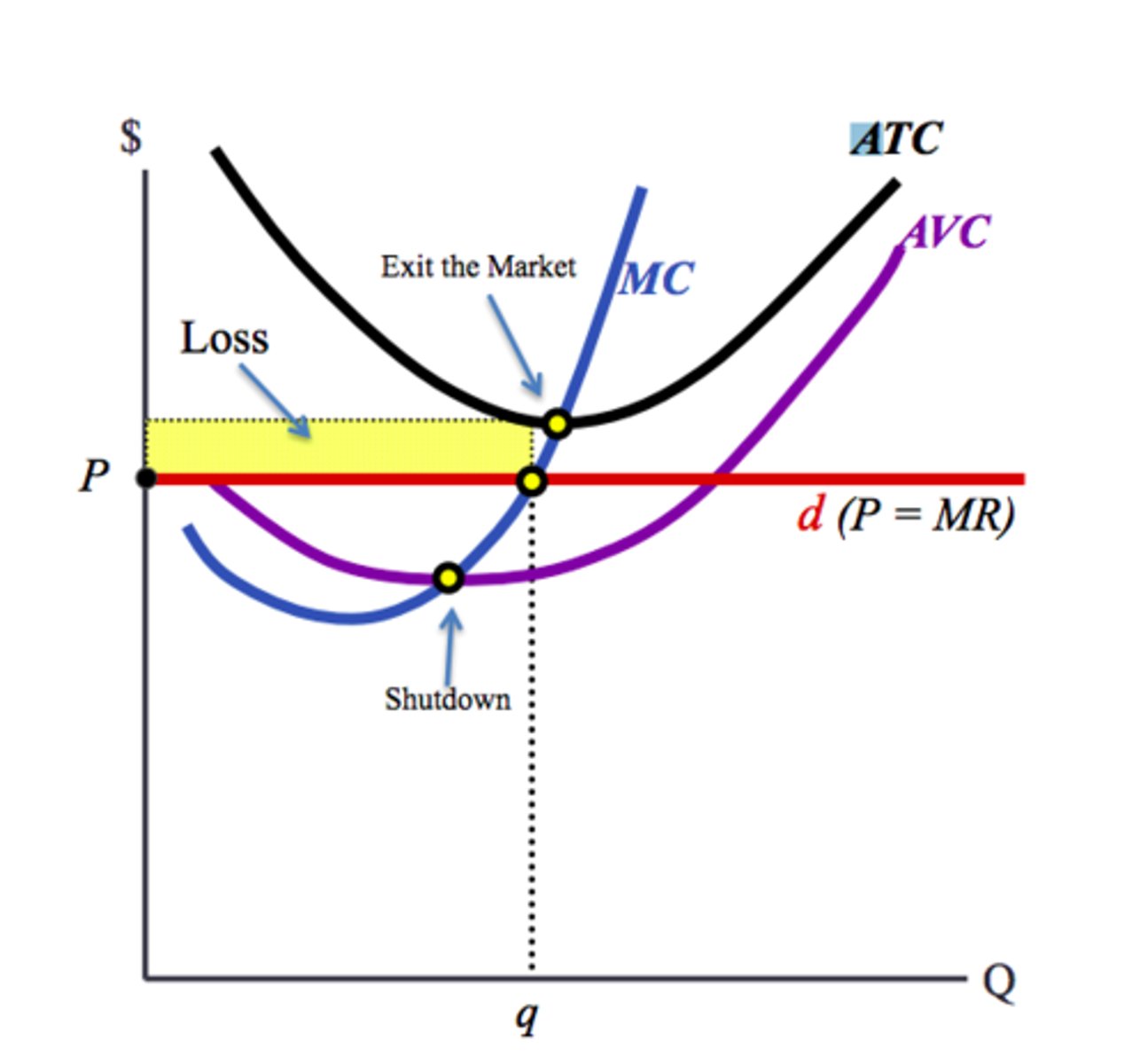

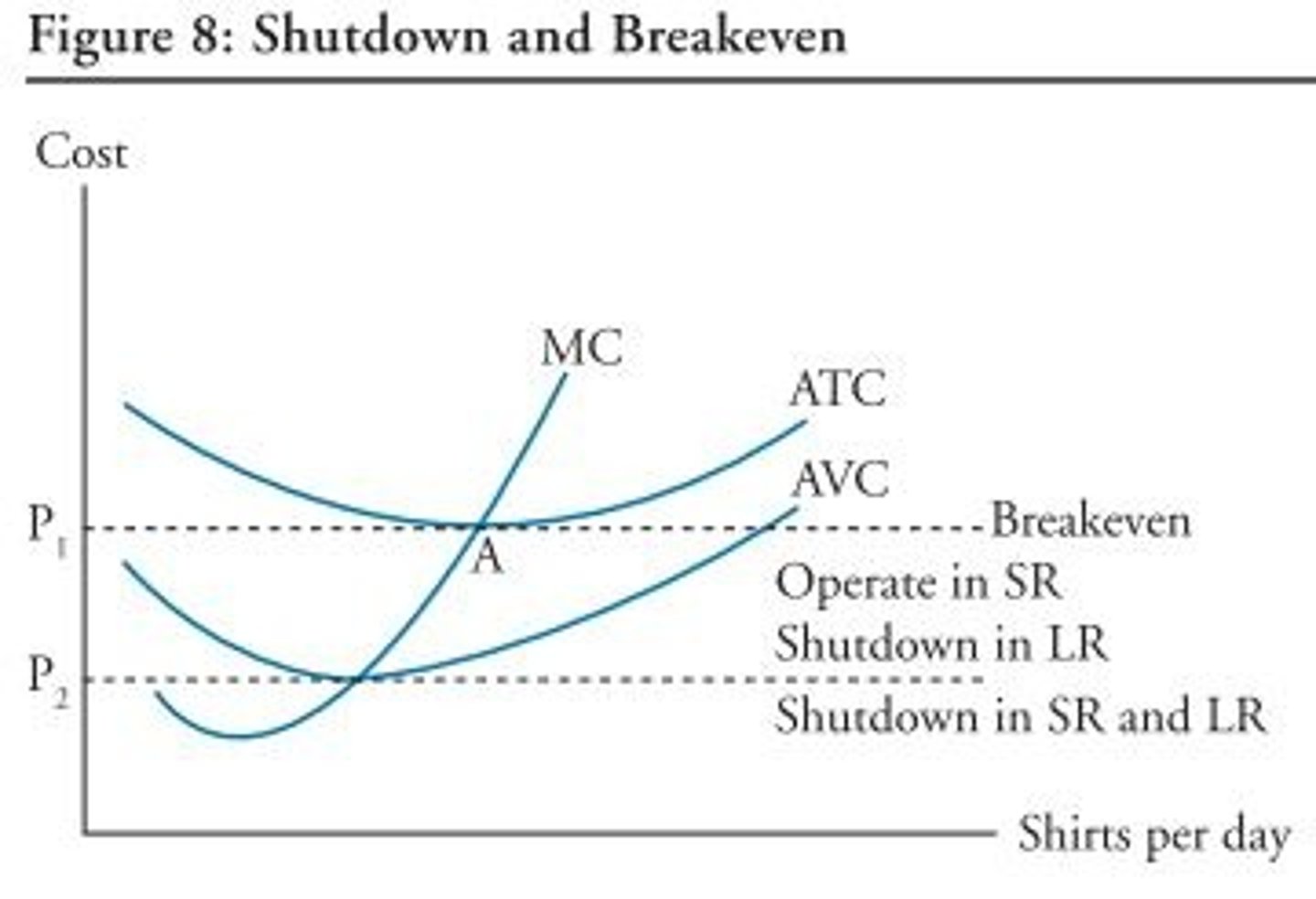

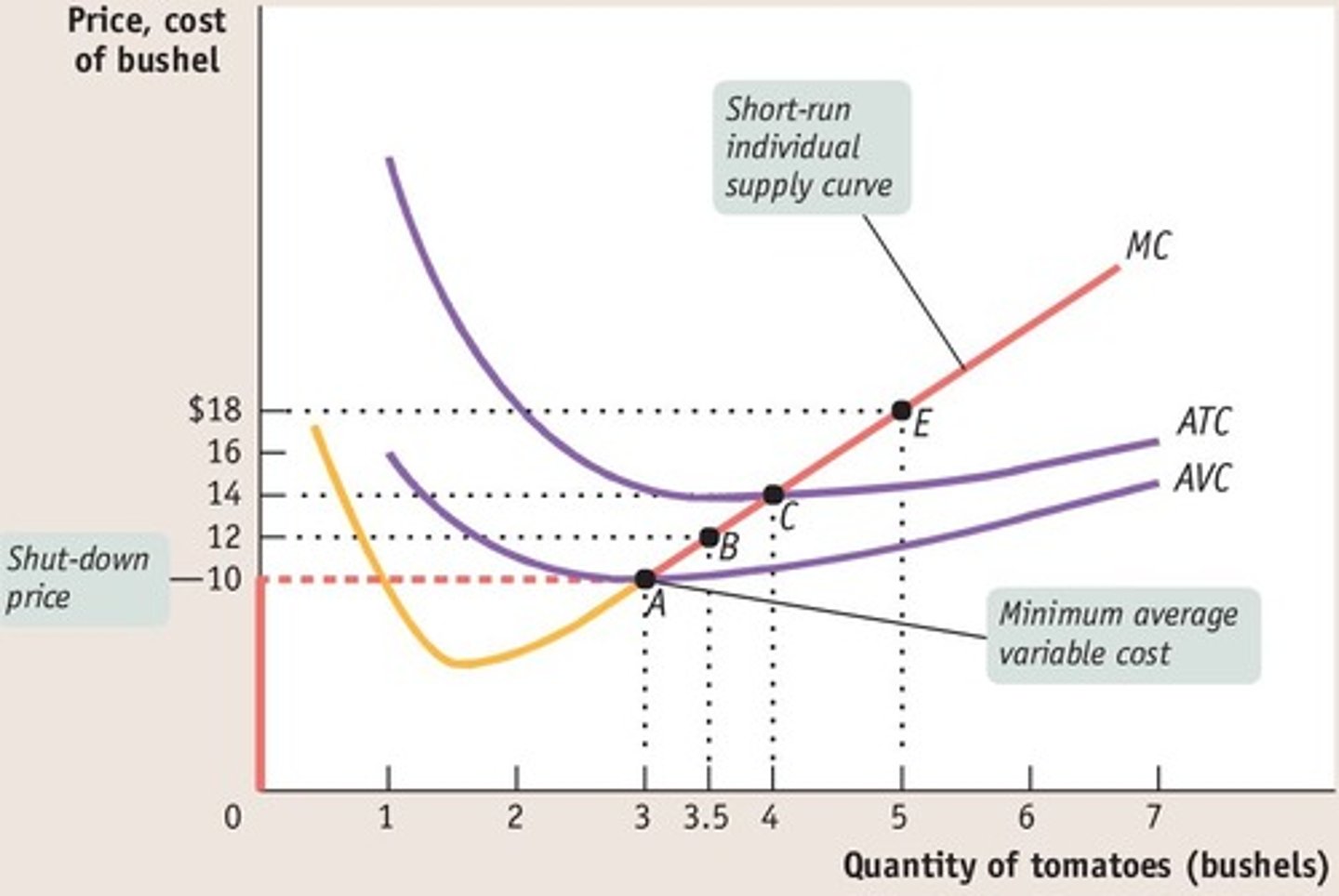

Determining When a Perfectly Competitive Firm Will Shut Down or Operate at a Loss in the Short Run

Shutdown Point

Numerically, this point occurs when

marginal revenue equals marginal cost at the minimum average

variable cost. Graphically, this point occurs where the price, or

marginal revenue curve, intersects the marginal cost curve at the

minimum point of the average variable cost curve (AVC)

In the short run, if ATC is greater than price at the output level

where MC = MR then

A) new firms may be incentivized to enter the industry.

B) the firm may be able to minimize losses.

C) the firm will shut down.

D) the firm will realize an economic profit

B) the firm may be able to minimize losses.

Assume the Unico Corporation is producing 40 units of output

and selling the output in a perfectly competitive market for $5 per

unit. Its total fixed costs are $110, and its average variable cost is

$4 for each of the 40 units of output. Unico

A) earns a profit of $40.

B) maximizes its profits.

C) earns a loss of $70.

D) should shut down

earns a loss of $70.

Determining the Shape of a Perfectly Competitive

Firm's Short-Run Supply Curve

connect dots at these points where they intersect with marginal revenue lines

A perfectly competitive firm's short-run supply curve is at its

lowest point when MC equals the minimum point of

A) the average fixed cost curve.

B) the marginal revenue curve.

C) the average total cost curve.

D) the average variable cost curve

D) the average variable cost curve

in the long run, if ATC equals price at the output level where MC =

MR then

A) new firms may be incentivized to enter the industry.

B) the firm will shut down.

C) the firm will earn a normal profit.

D) the firm may be able to minimize losses

D) the firm may be able to minimize losses

In the long run, perfectly competitive firms achieve

A) allocative and productive efficiency.

B) allocative efficiency, but not productive efficiency.

C) productive efficiency, but not allocative efficiency.

D) neither allocative nor productive efficiency

A) allocative and productive efficiency.

Which of the following statements describes what perfectly

competitive firms experience in the long run?

A) Price equals ATC.

B) Price equals the minimum point on AVC.

C) Price equals the minimum point on ATC.

D) Marginal revenue is greater than marginal cost

C) Price equals the minimum point on ATC.

Constant-Cost Industry

An industry in which the firms' cost structures do not

vary with changes in production

Which of the following statements describes a perfectly

competitive market under conditions of constant cost?

A) The market supply curve becomes perfectly elastic in the

long run.

B) The market rarely experiences changes in the price and

quantity sold in the short run.

C) If 50 units can be produced for $150, then 150 units can

be produced for $350 and 200 units for $450.

D) The market rarely experiences changes in supply in

response to changes in demand.

A) The market supply curve becomes perfectly elastic in the

long run.