Unit 1-B

1/24

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

Competitive Market

Many buyers, none of whom can control the price, or prevent others from entering/ exiting the market.

Quantity Demand

Quantity of goods or services consumers are willingly able to purchase at a specific price.

Demand

Quantity of goods/services consumers are willingly able to purchase at various prices.

Demand Schedule

A way to see demand in a table.

Demand Curve

A way to see demand in a graph format.

Law of Demand

When price goes up, quantity demand goes down. When price goes up, QD goes down.

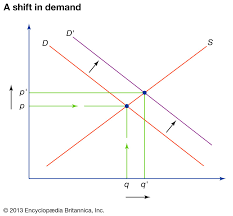

Does this show increase or decrease in demand

Increase in Demand

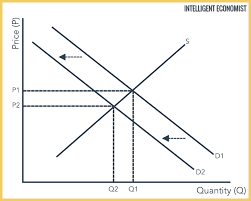

Does this show increase or decrease in demand?

Decrease in demand.

What is the M in Merit?

Market Size

If the number of consumers goes up: The Market demand goes up.

What is the E in Merit stand for?

Expectations by Consumers

If the expectations are up to par in the future: Demand goes up.

What does the R stand for in MERIT?

Related Prices (Substitutes & Complements)

If A and B are substitutes: and the price goes up, Demand Quantity goes up.

If A and B are compliments: and the price goes up, Demand goes down.

What does the I stand for in MERIT

Income of Consumers (Normal and Inferior)

If good A is a normal good, and income goes up: Demand goes up

If good A is a normal good and

What does the T stand for in MERIT

Tastes and Preferences.

Substitute in Consumption

Consumers will typically either buy one or the other.

Complements in Consumption

Two goods that are jointly produced given the same resources.

Quantity Supplied

The amount of a good or service people are willing to sell at some specific price.

Supply Schedule

Shows how much a good or service producers would supply at different prices.

Supply Curve

Shows the relationship between the quantity supplied and the price.

Law of Supply

Other things being equal, the price and quantity supplied of a good are positively related.

Change in Supply

Shift of the supply curve, in which indicates a change in the quantity supplied at any given price.

Movement along the supply curve

A change in the quantity supplied of a good arising from a change in the good’s price.

Input

A good or service that is used to produce another good or service.

Substitutes in Production

Two goods that producers can use the same inputs to make either one good or the other.

Complements in Production

Two goods are __________ if increased production of either good creates more of the other.

Equilibrium

Quantity where buyers are willing to purchase and sellers will want to provide.