Mid term for Microeconomics

1/195

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

196 Terms

Scarcity

A condition that arises from the conflict between unlimited human wants and limited resources available to fulfill those wants

Economics

A social science that studies how individuals, businesses, governments, and societies allocate scarce resources to satisfy unlimited wants and needs.

Microeconomics

the study of the economic behavior in individual markets, industries, or sectors, such as that for computers or unskilled labor.

Macroeconomics

the study of economic behavior of entire economies, as measured, for example, by total production and employment

economic theory

a simplification of reality used to make conjectures about cause and effect in the real world

Economic model

A simplification of reality used to make conjectures about cause and effect in the real world.

Scientific method

systematic approach scientists use to study and understand the world through observation, hypothesis formulation, experimentation, data analysis, and conclusion drawing.

Other-things-constant assumption

The assumption, when focusing on the relation among key economic variables, that other variables remain unchanged

Behavioral assumptions

an assumption that describes the expected behavior of economic decision makers- what motivates them

Hypothesis

A theory about how key variables relate

Positive economic statement

a statement that can be proved or disproved by reference to facts

Normative economic statement

a statement that reflects an opinion, which cannot be proved or disproved by reference to the facts

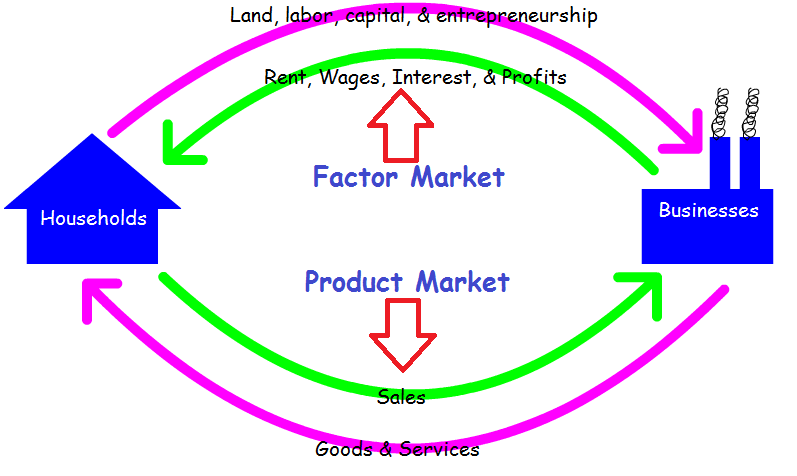

Circular-flow model

A diagram that traces the flow of resources, products, income, and revenue among economic decision makers

resources

the inputs, or factors of production, used to produce the goods and services that people want; consist of labor, capital, natural resources, and entrepreneurial ability

Labor

The physical and mental effort used to produce goods and services

Capital

the buildings, equipment, tools, utensils, appliances, and machinery used to produce goods and services

Human capital

The knowledge, skills, abilities, and other attributes that individuals possess, which can be used to produce goods and services and generate economic value.

entrepreneurial ability

the imagination required to develop a new product or process, the skill needed to organize production, and the willingness to take the risk of profit or loss

entrepreneur

A profit-seeking decision maker who starts with an idea, organizes an enterprise to bring that idea to life, and assumes the risk of the operation

Natural resources

All gifts of nature used to produce goods and services; includes renewable and exhaustible resources

good

a tangible product used to satisfy human wants

service

an activity, or intangible product, used to satisfy human wants

wages

payment to resource owners for the use of their capital

interest

payment to resource owners for the use of their capital

rent

payment to resource owners for the use of their natural resources

Profit

reward for entrepreneurial ability; sales revenue minus resource cost

markets

a set of arrangements by which buyers and sellers carry out exchange at mutually agreeable terms

Product markets

a market in which a good or service is bought and sold

resource markets

a market in which a resource is bought and sold

rational self-interest

each individual tries to maximize the expected benefit achieved with a given cost or to minimize the expected cost of achieving a given benefit

marginal

incremental, additional, or extra; used to describe a change in an economic variable

association-is-causation fallacy

the incorrect idea that if two variables are associated or correlated in time, one must necessarily cause the other

fallacy of composition

the incorrect belief that what is true for the individual, or part, must necessarily be true for the group, or the whole

secondary effects

unintended consequences of economic actions that may develop slowly over time as people react to events

economic theory or economic model

a simplification of reality used to make conjectures about cause and effect in the real world

positive/direct/relation

it occurs when two variables increase or decrease together; the two variables move in the same direction

negative/inverse

It occurs when two variables move in opposite directions; when one increases, the other decreases

slope of a line

a measure of how much the vertical variable changes for a give change in the horizontal variable

tangent

a straight line that touches a curve at a point but does not cut or cross the curve; used to measure the slope of a curve at a point

positive relation/direct relation

it occurs when two variables increase or decrease together

negative relation/inverse relation

it occurs when two variables move in opposite directions; when one increases, the other decreases

opportunity cost

the value of the best alternative forgone when an item or activity is chosen

sunk cost

a cost that has already been incurred, cannot be recovered, and thus is irrelevant for present and future economic decisions.

Production possibility frontier (PPF)

a curve showing alternative combinations of goods that can be produced when available resources are used efficiently; a boundary line between inefficient and unattainable combinations

law of comparative advantage

the individual, firm, region, or country with the lowest opportunity cost of producing a particular good should specialize in that good

Absolute advantage

the ability to make something using fewer resources than other producers use

Comparative advantage

The ability to make something at a lower opportunity cost than other producers face

Barter

The direct exchange of one product for another without using money

division of labor

breaking down the production of a good into separate tasks

specialization of labor

focusing work effort on a particular product or a single task

efficiency

the condition that exists when there is no way resources can be reallocated to increase the production of one good without decreasing the production of another; getting the most from available resources

constant opportunity costs

where the trade-off between producing different goods or services remains constant, meaning that the resources sacrificed to produce one unit of a particular good or service are the same for each additional unit produced

law of increasing opportunity cost

to produce more of one good, a successively larger amount of the other good must be sacrificed

economic growth

an increase in the economy’s ability to produce goods and services; reflected by an outward shift of the economy’s production possibilities frontier

rules of the game

the formal and informal institutions that support the economy- the laws, customs, manners, conventions, and other institutional underpinnings that encourage people to pursue productive activity

economic system

the set of mechanisms and institutions that resolve the what, how, and for whom questions

pure capitalism

An economic system characterized by the private ownership of resources and the use of prices to coordinate economic activity in unregulated markets

Private property rights

an owner’s right to use, rent, or sell resources or property

pure command system

pure command system, an economic system characterized by the public ownership of resources and centralized planning

mixed system

An economic system characterized by the private ownership of some resources and public ownership of other resources; some markets are regulated by the government

production possibilities frontier (PPF)

A curve showing alternative combinations of goods that can be produced when available resources are used efficiently; a boundary line between inefficient and unattainable combinations

utility

the satisfaction received from consumption; sense of well-being

transfer payments

cash or in-kind benefits given to individuals by the government

industrial revolution

development of large-scale factory production that began in Great Britain around 1750 and spread to the rest of Europe, North America, and Australia

firms

economic units formed by profit-seeking entrepreneurs who employ resources to produce goods and services for sale

sole proprietorship

a firm with a single owner who has the right to all profits but who also bears unlimited liability for the firm’s losses and debts

partnership

a firm with multiple owners who share the profits and bear unlimited liability for the firm’s losses and debts

corporation

a legal entity owned by stockholders whose liability is limited to the value of their stock ownership

cooperative

An organization consisting of people who pool their resources to buy and sell more efficiently than they could individually

nonprofit organizations

groups that do not pursue profit as a goal; they engage in charitable. educational, humanitarian, cultural, professional, or other activities, often with a social purpose

information revolution

technological change spawned by the microchip and the internet that enhanced the acquisition, analysis, and transmission of information

market failure

A condition that arises when the unregulated operation of markets yields socially undesirable results

antitrust laws

prohibition against price fixing and other anticompetitive practices

monopoly

a sole supplier of the product with no close substitutes

natural monopoly

One firm that can supply the entire market at a lower per-unit cost than could two or more firms

private goods

a good, such as pizza, that is both rival in consumption and exclusive

public goods

a good that, once produced, is available for all to consume, regardless of who pays and who doesn’t; such a good is nonrival and nonexclusive, such as a safer community

externality

a cost or a benefit that affects neither the buyer nor seller, but instead affects people not involved in the market transaction

fiscal policy

The use of government purchases, transfer payments, taxes, subsidies, and borrowing to influence economy-wide variables such as inflation, employment, and economic growth

Monetary policy

regulation of the money supply and interest rates to influence economy-wide variables such as inflation, employment, and economic growth

mandatory spending

Federal mandatory spending refers to government spending that is mandated by laws and does not require annual congressional approval through the appropriations process. This spending includes entitlement programs like Social Security, Medicare, and Medicaid.

discretionary spending

Federal discretionary spending refers to government spending that is determined through the annual appropriations process and is subject to limits set by Congress. This spending includes funding for various federal agencies, programs, and initiatives such as national defense, education, infrastructure, and research and development.

ability-to-pay tax principle

Those with a greater ability to pay, such as those earning higher incomes or those owning more property, should pay more taxes

benefits-received tax principle

Those who get more benefits from government programs should pay more taxes.

tax incidence

The incidence of a tax refers to the distribution of the tax burden between buyers and sellers in a market

proportional taxation

the tax as a percentage of income remains constant as income increases; as called a flat tax

progressive taxation

The tax as a percentage of income increases as income increases

marginal tax rate

the percentage of each additional dollar of income that goes to the tax

regressive taxation

The tax as a percentage of income decreases as income increases

trade balance

The value during a given period of a country’s exported goods minus the value of its imported goods

ne exports

The value during a given period of a country’s exported goods minus the value of its imported goods

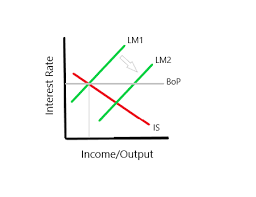

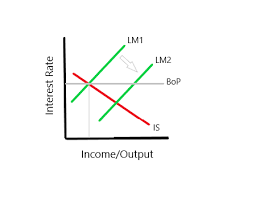

balance of payments

a record of all economic transactions during a given period between residents of one country and residents of the rest of the world

foreign exchange

foreign money needed to carry out international transactions

tariffs

a tax on imported goods

quota(s)

a legal limit on the quantity of a particular product that can be imported or exported

demand

a relation between the price of a good and the quantity that consumers are willing and able to buy per period, other things constant

law of demand

The quantity of a good that consumers are willing and able to buy per period relates inversely, or negatively, to the price, other things constant

demand curve

a curve showing the relationship between the price of a good and the quantity consumers are willing and able to buy per period, other things constant

quantity demanded

The amount of goods that consumers are willing and able to buy per period at a particular price, as reflected by a point on a demand curve