Microeconomics-Chapter 3-Supply

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

29 Terms

individual supply

the Quantity firm plans to sell at each price; the amount you plan to sell at a given price is your quantity supplied at that price

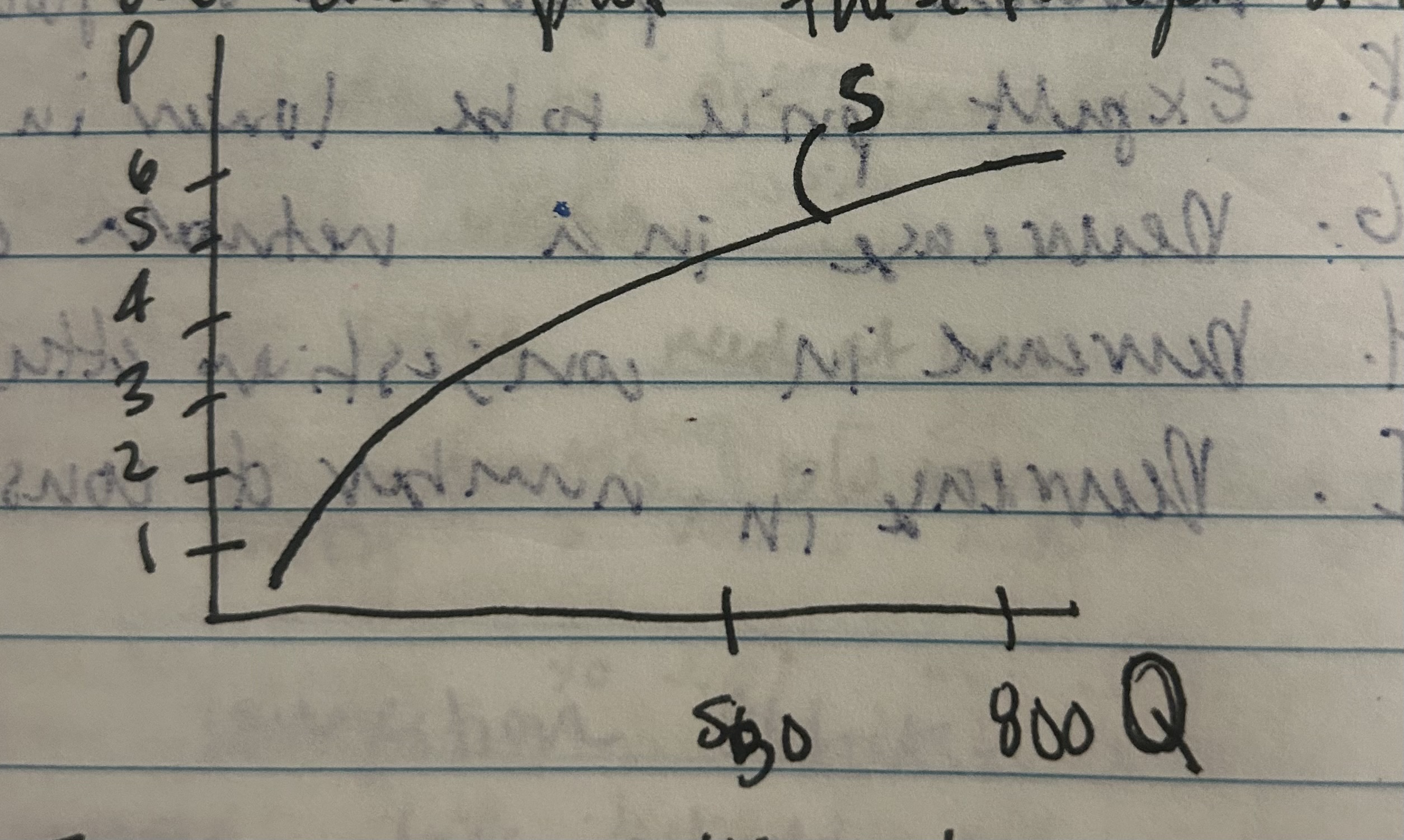

Example of Quantity Supplied

Cups of Hot Chocolate

Price: Quantity:

$6 800

$5 550

$4 350

$3 200

$2 125

$1 50

And can plot a supply curve, this has a positive slope upward => positive relationship between price and quantity.

Characteristics of a perfect competition:

-many buyers and sellers

-all sellers produce an identical good

-these imply that individual firms are price takers

Example:

-stock in a company

-commodities

Ex:oil, gasoline, gold, aluminum (many agricultural products), many agricultural products

Price takers

Individual firms, this means they should only sell at the market price and they can sell as much as they want at the market price

Market Price

given and based on market demand and market supply, Demand curve is downward slope so why can a firm sell as much as they want at market price because each firm is so small in relative of the size of the market, so if they change, quantity to it does not affect the price.

Why will a firm only decide to sell at price equal to market price?

If a firm sets price higher than the market price, they would not be able to sell any quantity. If a firm sets price lower than the market price, they will unnecessarily lose out on money so firms choose to set price = market price.

Variable Costs

costs that vary with amount of output your produce Ex:Cup, straws, cocoa powder Marginal Costs include variable costs but not fixed costs Ex:How many loaves of bread to produce

Fixed Costs

Costs that do NOT vary with amount of output Ex: Rent

Example of Supply and Marginal Costs

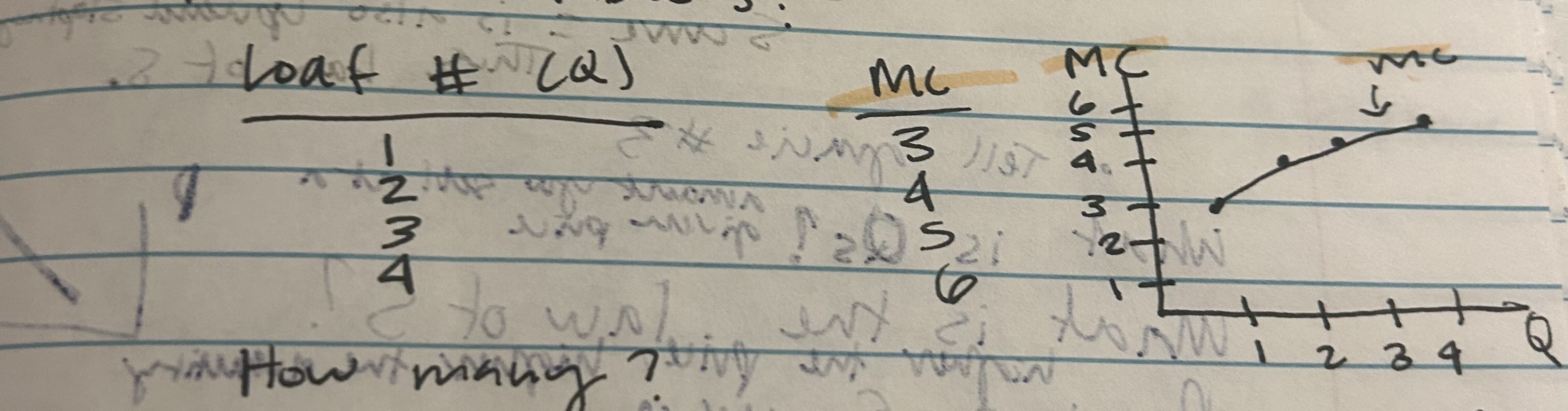

How many loaves of bread to produce?

Firm’s MC table’s:

Loaf #(Q): MC:

1 3

2 4

3 5

4 6

The marginal benefit of an extra loaf to the seller=price

P=MB

For each unit?

1> MB >= MC

P>=MC

Keep producing unit P=MC

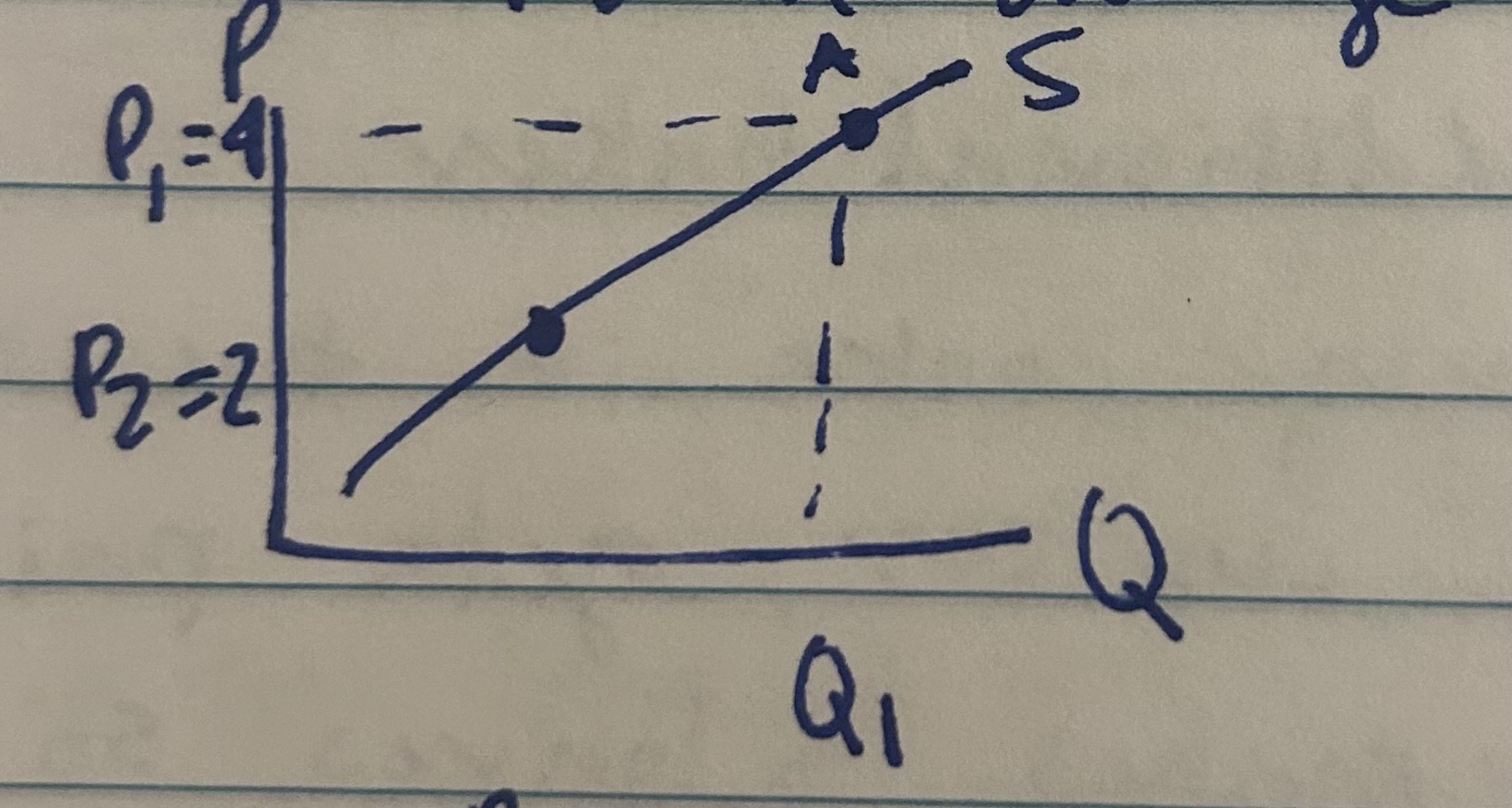

Suppose P=$5 Then Qs= 3

This is one point on the demand curve

Repeat with other prices:

If P=3$, Qs=$1

P=$4, Qs= $2

P=$5, Qs= $3

P=$6, Qs =4

We can plot to get a supply curve and find that marginal cost=supply curve

For a given quantity, the supply curve gives you the least you are willing to accept, the least you are willing to accept is also your marginal costs

Increasing Marginal Costs

MCs rise as we produce more output, so MC is upward sloping, S curve=MC thu, the law of supply

Law of Supply

the higher the price, the higher the quantity

Diminishing marginal product

additional units of an input will add less and less to the output

Input

an input into a production process that produces outputs Ex: Flour is an input into making bread

Example of input and output in Supply

Bread

Output- bread input

First Baker: makes 3 loaves

Second: 2 additional loaves of bread

Third: 1 additional baker

We see to many cooks in the kitchen

Assume each worker, gets paid $30/hour.

First baker makes 3 loaves so 10$/loaf

Second:15$ a loaf

Third:$30/Loaf

Another aspect of why there is increasing marginal costs

may have to pay higher transportation costs to input further away inputs

Miscellaneous Point for increasing in marginal costs

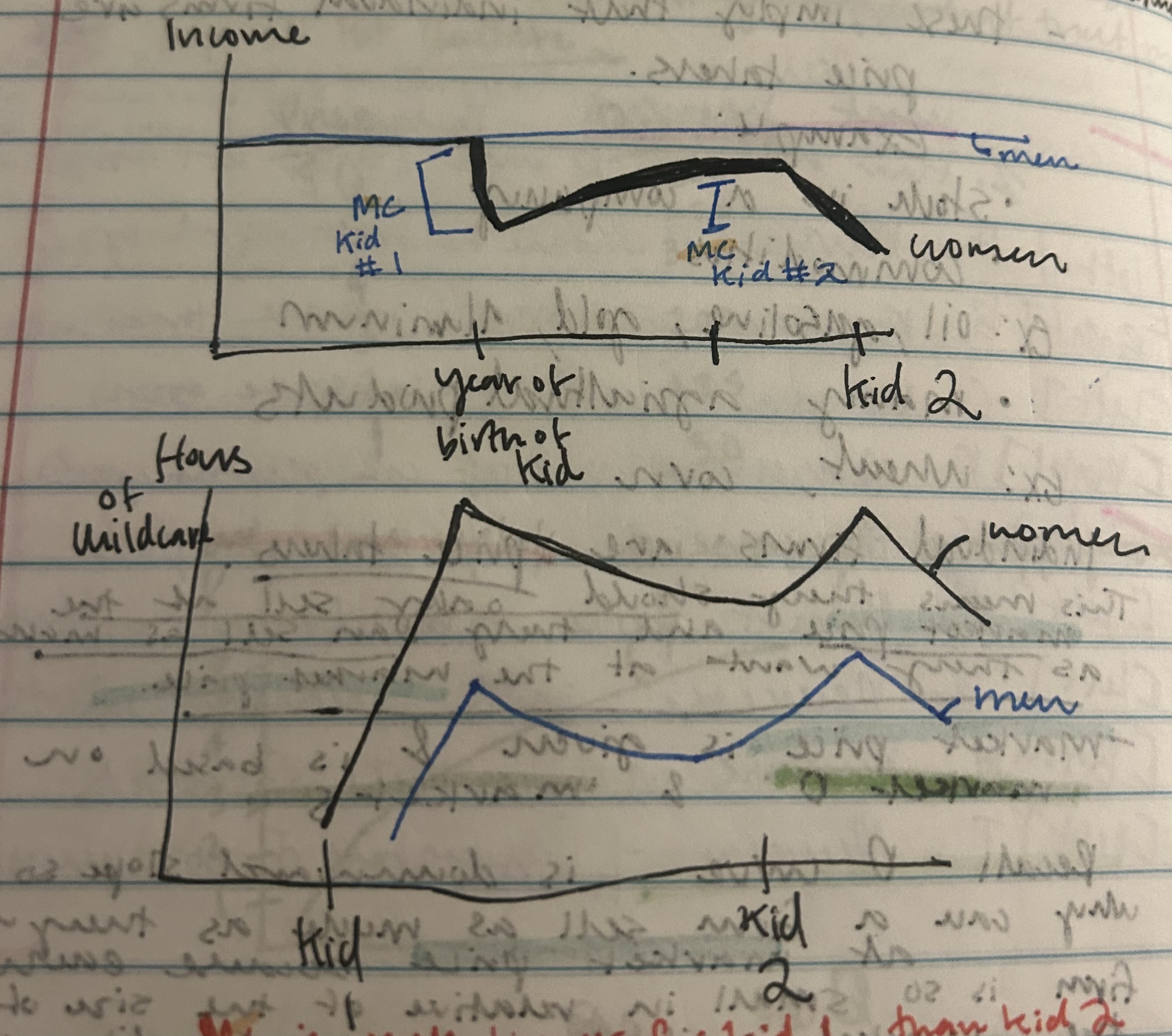

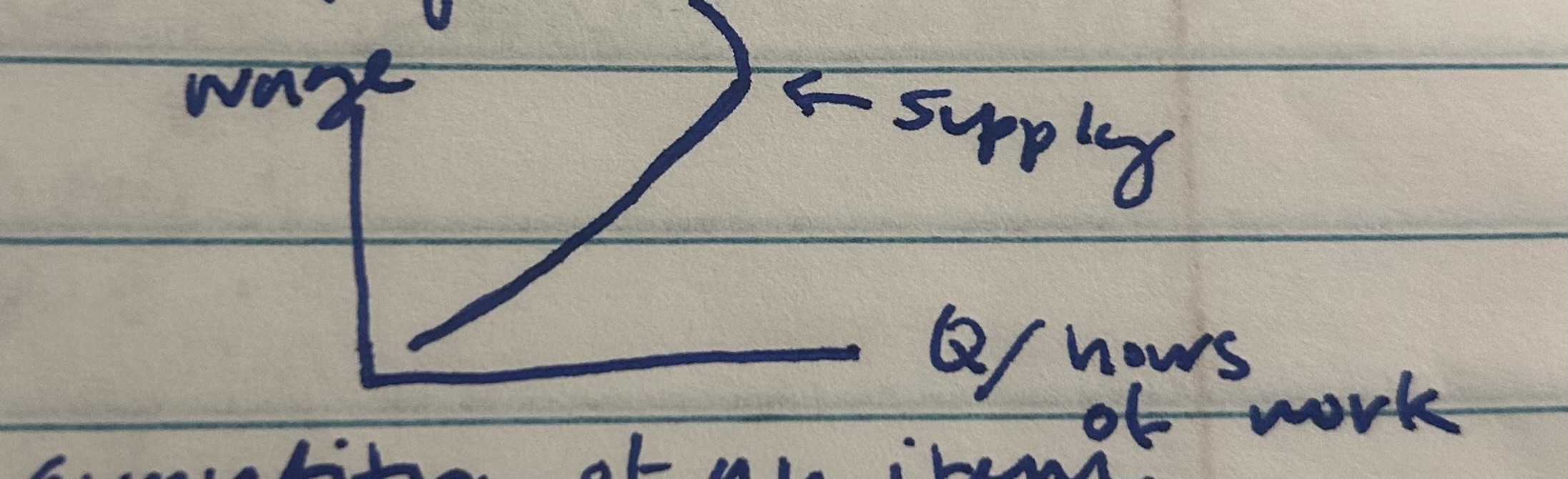

when you work, you supply labor, the labor supply curve bends backwards

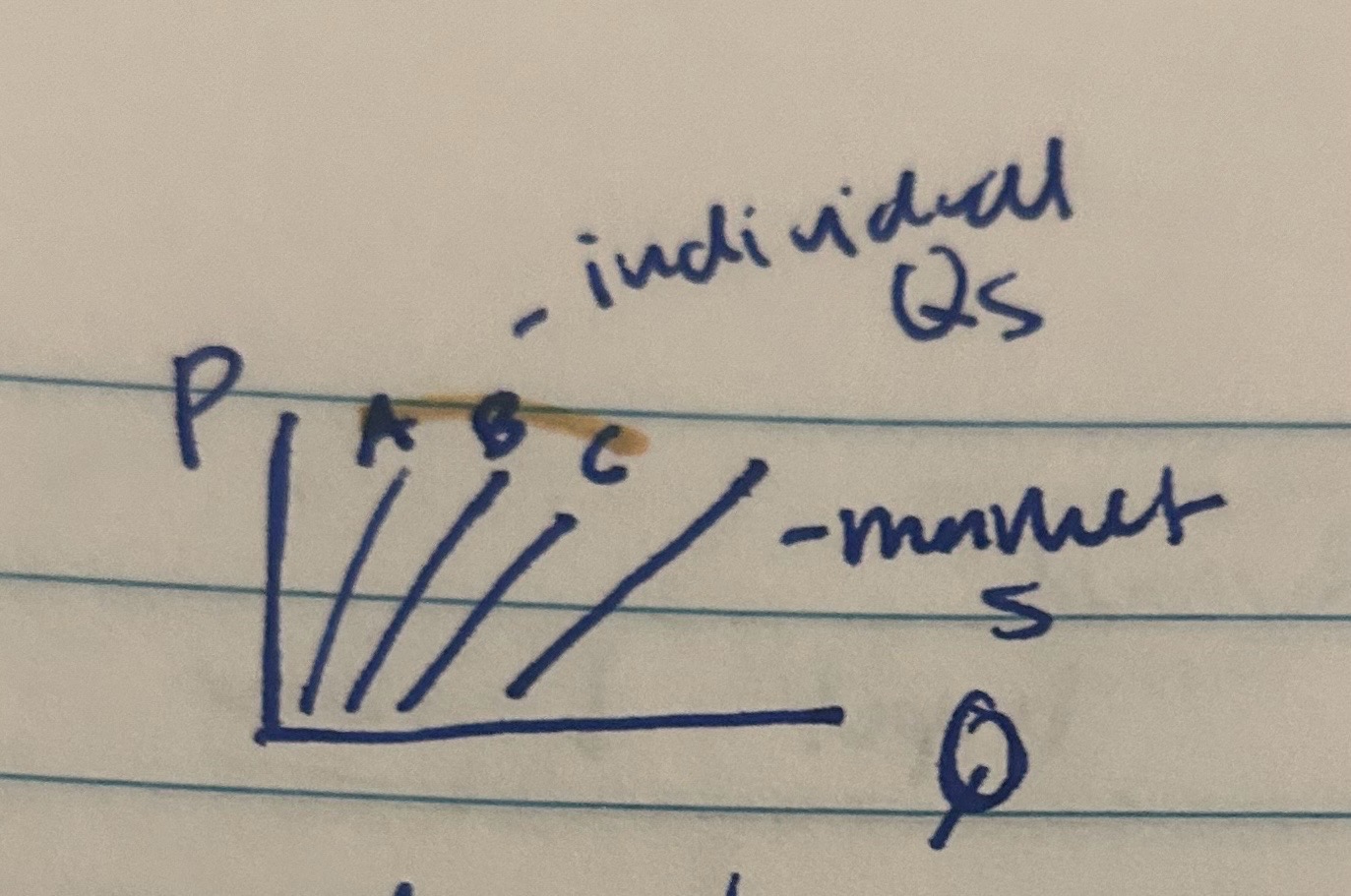

Market Supply

the total quantity if an item that produces in a market plan to sell at each price, for each price, sum up the Quantity supplied

Example of Market Supplied

Price Qs Firm A Qs Firm B Qs Firm C = Market S

6 800 1200 4000 6000

5 550 1000 3500 5050

Movement along the S curve

The only thing that causes movement along the curve is a change in price

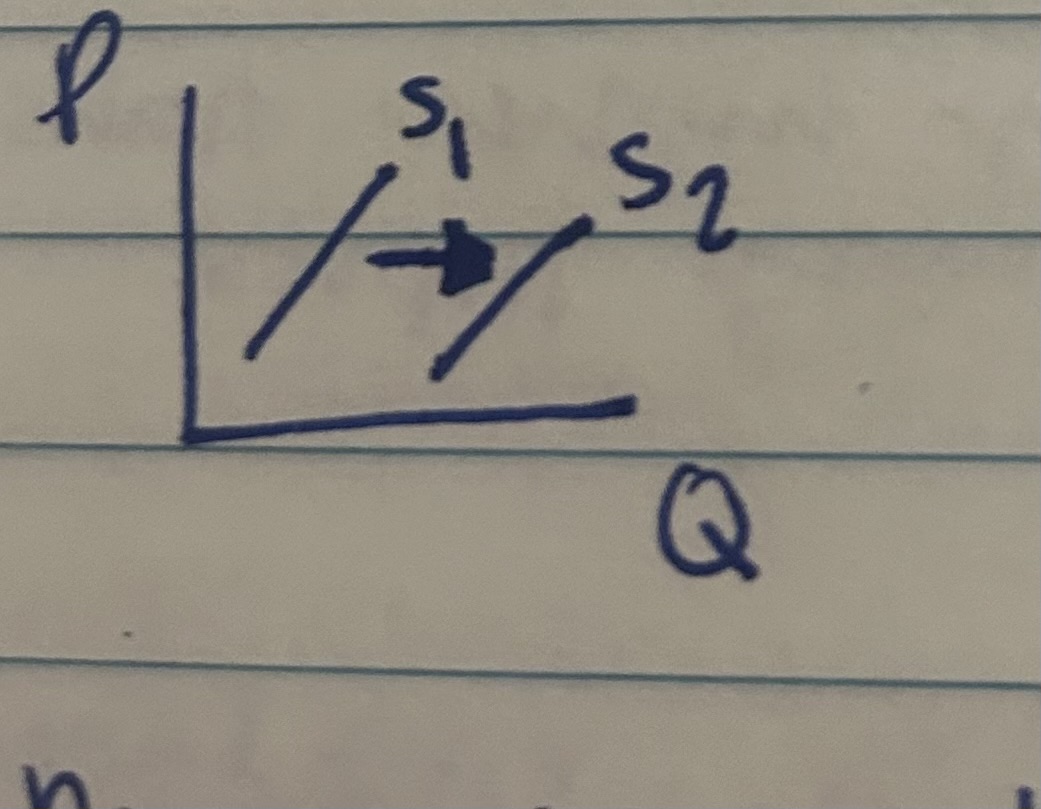

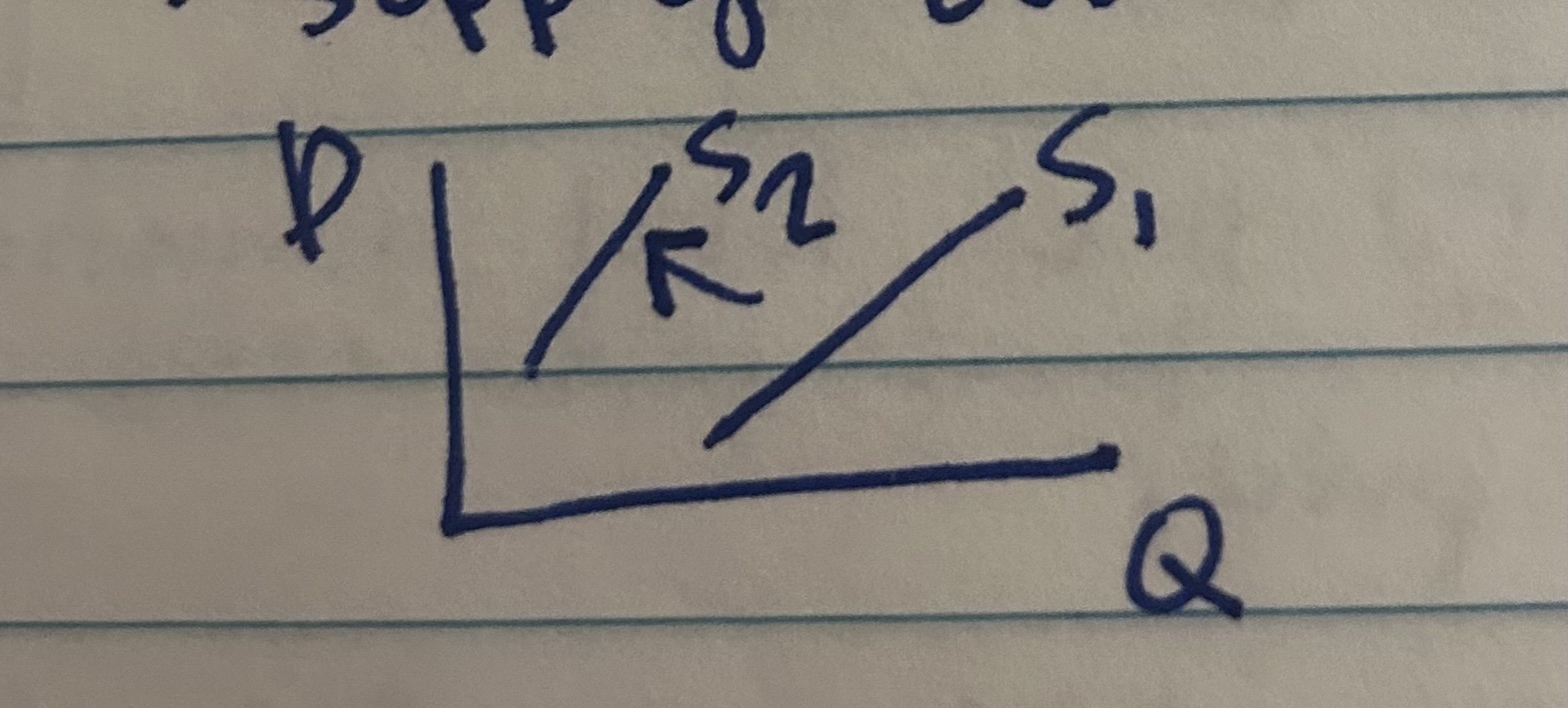

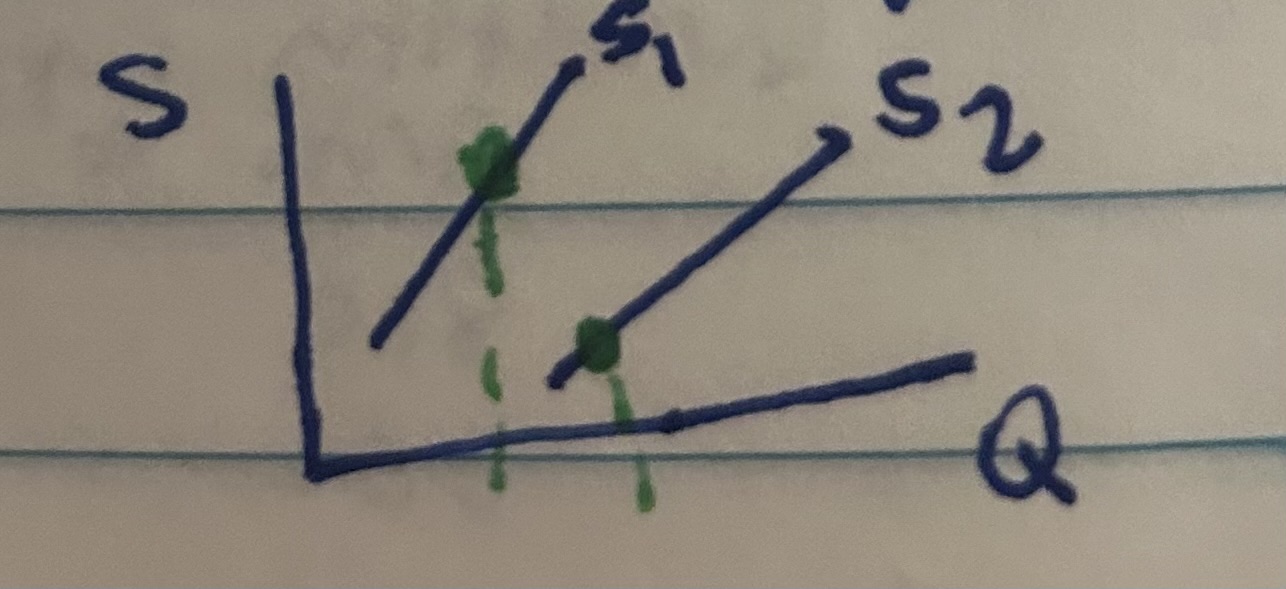

Increase in Supply

S(up arrow), produce more at every price, S curve shifts to the right

Decrease in Supply

S(down arrow), produce less at every price, supply curve shifts left. When S curve shifts right, it technically shifts downward

What happens when a demand curve shift to the right?

It technically shifts upward because of the slope of the lines

Things that cause Shifts in Supply

Input prices, technology and productivity, prices of related outputs, producer expectations about future prices, type and number of sellers

Input prices

lower input prices lead to lower marginal cost, this means the supply curve shifts to the right and vice versa Ex:oil price falls, supply curve shifts to the right

Technology and Productivity

Better technology and higher productivity, allows films to produce some output with fewer inputs(or more output with some inputs), this lowers the MC of production so supply curve shifts to the right Productivity- if bad weather or pest infestation farmers crop production is less productive so curve shifts to the left

prices of related outputs

A. Substitutes in Production B. Compliments in Production

producer expectation about future prices

If producer expects the price they can sell goof to increase in the future, they will decrease in the supply today, Supply curve shifts to the left.

Type and number of Sellers

(market supply) more sellers in the market→ Supply curve shifts to the right

Miscellaneous shifts in the supply curve

war, natural disasters, government (something is banned, supply goes to zero)