Basic Economics

1/46

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

47 Terms

scarcity

there is a limited amount of resources on the planet to meet the unlimited wants of people

economics

the study of how people use their resources (or make choices) to deal with the problem of scarcity

positive economic statement

based on facts and not opinions

normative economic statement

include opinions

opportunity cost

when we make decisions in life, there are trade-offs or other possible options

factors of production

the resources used to produce goods and perform services (land, labor, capital [physical/human])

entrepreneur

person who puts together the factors of production to create goods and services

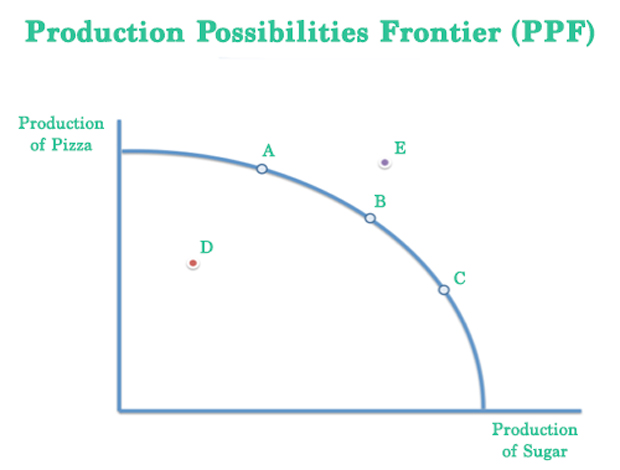

production possibilities curve (ppc)

a graphic representation of how much can be produced by an economy and the opportunity cost of producing that good or service

assumptions of the production possibilities curve

1) represents full employment/productivity

2) only producing 2 different goods

3) resources can be used for both goods

4) resources and technology are fixed (ceteris paribus)

graph of production possibilities curve

points A, B, and C: efficient, max output using resources

point D: underutilization, unemployment, natural resource depletion

point E: impossible to produce, not enough resources

law of increasing costs (ppc)

as production switches from one good to another, the opportunity costs increase

growth (ppc)

when an economy can produce more than it previously could, the ppc shifts outward

reasons an economy can grow

1) acquiring new resources

2) better technology

3) trade with other economies

consumer goods

goods that satisfy our wants/needs directly, produced for personal consumption

capital goods

goods that help create consumer goods more efficiently

decline

when an economy can produce less than it previously could, the ppc shifts inward

reasons an economy can shrink

1) weather or natural disaster destroys natural resources

2) war destroys resources

economic system

how a society allocates its resources

market economy

an economic system where decisions on how to allocate resources are decided by voluntary exchanges of individuals on markets

market

consumers buy the goods and services from products

product market

consumers buy the goods and services from producers

factor market

producers buy the factors of production to make more goods or services for the product market

economic freedom

consumers buy whatever they want at whatever price they want and producers make whatever goods they want at whatever price they want to sell it at

laissez faire

“let them do as they please”

invisible hand (Adam Smith)

the economy guides itself and needs little government intervention, it shifts and adapts

price

direct resource usage by producers and they are determined, how consumers and producers communicate

competition

producers struggling against one another to get consumers to buy their goods and services

what competition gives us

1) choice and variety in goods and services produced

2) innovations

3) efficiency as producers produce a better product or cheaper products

private property

people have the right to control their possessions as they wish; the government does not control the factors of production

downsides to a free market economy

1) wealth is not evenly distributed

2) individual interests are more important than overall public well-being

3) lack of safety net for economic failure

4) competition brings out best and worst in people

socialism

philosophy based on the belief that society as a whole should control the factors of production and evenly distribute goods and services throughout society

communism

government plans and controls entire economy, centrally planned

downsides of a command economy

1) no economic freedom

2) lack of competition

3) lack of efficiency: if doctors and janitors are getting paid the same, why didn’t they have to do the same amount of school or work?

mixed economy

economic system which combines a free market economy and socialism, limited government control over some programs, but individuals make most choices

absolute advantage

the ability to produce more of a given product using a given amount of resources

comparative advantage

the ability to produce a given product more effectively (lowest opportunity cost)

in an input problem…

it shows the amount of resources required to produce 1 unit of the product, we use the lower number

to find the opportunity cost of producing ____, the amount of resources it takes to produce that product goes above the number of resources it takes to produce the product we are comparing it to

in an output problem…

it shows the amount of resources we can produce within a given amount of time, use the higher number

to find the opportunity cost of producing one ____, the number of ____ we can produce in one hour goes under the number of the compared product that can be produced in that same time

optimal allocation

finding how much to produce of a good to make consumers happy

marginal analysis

weighing marginal benefit vs marginal cost

marginal benefit

economic benefit gained from consuming or producing one more unit

marginal cost

economic cost from consuming or producing one more unit

utility

amount of satisfaction a consumer gets from consuming a good or service (unit=UTILS)

total utility

sum of all utility received from consuming a certain quantity of goods and services (add up all UTILS)

marginal utility

additional satisfaction or utility a consumer receives from consuming one more marginal good or service

law of diminishing marginal utility

the amount of utility gained from consuming each additional unit of a good decreases with each additional unit consumed (the more utility a person receives from a good or a service, the more they are willing to pay for that good or service)