economics (demand, supply, equilibrium)

5.0(2)

Studied by 16 peopleCard Sorting

1/58

Earn XP

Description and Tags

Last updated 7:30 PM on 5/11/25

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

59 Terms

1

New cards

demand

the willingness and ability to purchase a good or service

2

New cards

law of demand

if prices go up, demand will go down.

if prices go down, demand will go up.

if prices go down, demand will go up.

3

New cards

demand curve

represents the utility one gets when consuming a good or service

4

New cards

individual demand

each of us have our own level of demand for a good or service

5

New cards

market demand

sum of all individual demand for a good or service

6

New cards

change in quantity demanded

a change in price leading to movement along the demand curve

7

New cards

change in demand

a change in demand due to a non price determinant leads to a shift in demand

8

New cards

normal good

a good that consumers prefer to purchase if their income allows it

9

New cards

inferior good

less desirable, cheaper good that consumers may purchase when incomes are low

10

New cards

non price determinants of demand

T- tastes and preferences

I- income

M- market size

E- future price expectations

R- related goods

I- income

M- market size

E- future price expectations

R- related goods

11

New cards

income (demand)

non price determinant of demand

when incomes goes up, demand for normal goods goes up and demand for inferior goods go down

when incomes goes up, demand for normal goods goes up and demand for inferior goods go down

12

New cards

future price expectations (demand)

non price determinant of demand

if consumers think that prices are going to go up in the future they will purchase now.

if consumers think that prices are going to go down in the future they will purchase later

if consumers think that prices are going to go up in the future they will purchase now.

if consumers think that prices are going to go down in the future they will purchase later

13

New cards

related goods (demand)

non price determinant of demand

if price of a complement goes down, demand for your good will go up.

if price of a substitute goes down, demand for your good will go down

if price of a complement goes down, demand for your good will go up.

if price of a substitute goes down, demand for your good will go down

14

New cards

complement

goods that are purchased and used together

15

New cards

substitutes

goods used in place of another good (not inferior)

16

New cards

market size (demand)

non price determinant of demand

if there is an increase in population or consumers then demand will go up.

if there is a decrease in population or consumers then demand will go down.

if there is an increase in population or consumers then demand will go up.

if there is a decrease in population or consumers then demand will go down.

17

New cards

tastes and preferences (demand)

non price determinant of demand

advertisements and influences can impact demand.

seasonal changes increase demand for some goods.

changes in population's age structure.

government policies can change demand.

advertisements and influences can impact demand.

seasonal changes increase demand for some goods.

changes in population's age structure.

government policies can change demand.

18

New cards

supply

the willingness and ability of producers to produce a good or service

19

New cards

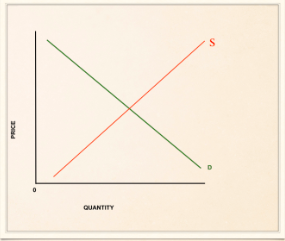

law of supply

as prices go up, supply goes up.

as prices go down, supply goes down.

as prices go down, supply goes down.

20

New cards

supply curve

represents the costs to a firm producing the good or service

21

New cards

individual supply

the willingness and ability for one firm to produce a good or service

22

New cards

market supply

the willingness and ability for all firms within a market to produce a good or service

23

New cards

non price determinants of supply

S- subsidies (changes in costs of factors of production)

T- technology

O- other related goods

R- resource costs

E- expectations

S- size of market

T- technology

O- other related goods

R- resource costs

E- expectations

S- size of market

24

New cards

resource costs (supply)

non price determinant of supply

if costs go down then profits go up

if costs go up then profits go down

if costs go down then profits go up

if costs go up then profits go down

25

New cards

cost

price of the resources that firms use to make a good or service

26

New cards

factors of production

land, labor, capital, and entrepreneurship

27

New cards

price of related goods (supply)

non price determinant of supply

if price of a good with joint supply goes up, then supply will go down

if price of a good with competitive supply goes up, then supply will go down

if price of a good with joint supply goes up, then supply will go down

if price of a good with competitive supply goes up, then supply will go down

28

New cards

joint supply

when two or more goods are made from the same product

29

New cards

competitive supply

when the same producer can produce two or more different products

30

New cards

indirect taxes and subsidies (supply)

non price determinant of supply

indirect taxes raise costs of producer, causes supply to decrease

subsidies lower costs of producer, causes supply to increase

indirect taxes raise costs of producer, causes supply to decrease

subsidies lower costs of producer, causes supply to increase

31

New cards

indirect taxes

tax placed on the production of a good or service by the government

32

New cards

subsidies

payments by the government to a producer

33

New cards

future price expectations (supply)

non price determinant of supply

If suppliers think that prices will go up in the future, then they will reduce supply today

If suppliers think that prices will go down in the future, then they will increase supply today.

If suppliers think that prices will go up in the future, then they will reduce supply today

If suppliers think that prices will go down in the future, then they will increase supply today.

34

New cards

changes in technology (supply)

non price determinant of supply

if improved technology reduces the costs of producers, then supply will increase

if improved technology reduces the costs of producers, then supply will increase

35

New cards

number of firms (supply)

non price determinant of supply

if the number of firms producing a good or service decrease then supply will decrease

if the number of firms producing a good or service increase then supply will increase

if the number of firms producing a good or service decrease then supply will decrease

if the number of firms producing a good or service increase then supply will increase

36

New cards

change in quantity supplied

change in price leads to movement along the supply curve

37

New cards

change in supply

change in supply due to a non price determinant leads to a shift in supply

38

New cards

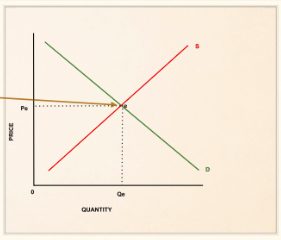

equilibrium

where supply meets demand, determines the quantity and price of a good, answers two of the basic economic questions of who gets the good or service and what is produced

39

New cards

equilibrium price

where quantity supplied is equal to quantity demanded, no surplus and no shortage

40

New cards

price rationing

free markets use prices to decide who gets the good or services

41

New cards

utility

satisfaction gained by consumers when they consume a good or service

42

New cards

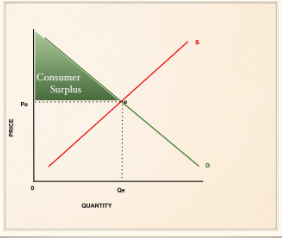

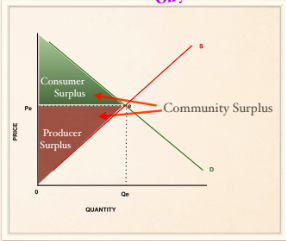

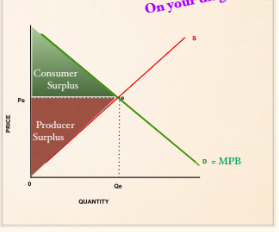

consumer surplus

extra utility gained by consumers when paying a price lower than they were willing to pay

43

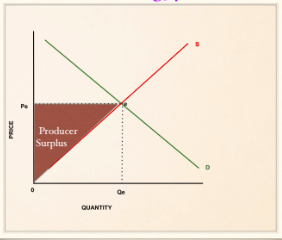

New cards

producer surplus

benefit producers receive when they receive a price above the one which they were willing to supply the good

44

New cards

community surplus

consumer surplus + producer surplus

45

New cards

marginal private benefit (MPB)

the utility consumers get when consuming one more unit of a good

d = mpb always

d = mpb always

46

New cards

marginal social benefit (MSB)

the total benefit to society from consuming one more unit of a good

d = msb IF the good or service doesn't harm or benefit a third party when consumed

d = msb IF the good or service doesn't harm or benefit a third party when consumed

47

New cards

marginal private cost (MPC)

the cost to a firm from producing one more unit of a good

s = mpc always

s = mpc always

48

New cards

marginal social cost

the cost to society of producing one more unit of a good

s = msc IF the production of the good or service doesn't harm or benefit society when produced then there is no further cost to society as a whole

s = msc IF the production of the good or service doesn't harm or benefit society when produced then there is no further cost to society as a whole

49

New cards

allocative efficiency

when the cost to society equals the benefit to society

MSC = MSB

resources are allocated in the most efficient way from societies POV

community surplus is maximized

the argument for a market economy

MSC = MSB

resources are allocated in the most efficient way from societies POV

community surplus is maximized

the argument for a market economy

50

New cards

arguments for a free market

allocative efficiency

freedom of choice

variety of goods

prices and wages are set by supply and demand

innovation

keeps prices low

freedom of choice

variety of goods

prices and wages are set by supply and demand

innovation

keeps prices low

51

New cards

signalling and incentive function

increase in price is the SIGNAL

chance to make greater profits is the INCENTIVE to increase supply

chance to make greater profits is the INCENTIVE to increase supply

52

New cards

reallocation in a free market

disequlibrium which leads to excess demand, leads consumers to pay a higher price for the good or service, suppliers see the increase in price and begin to increase supply which is the signalling and incentive function

movement along the supply curve as suppliers increase prices and supply, as price goes up, demand goes down, movement along a new demand curve until a new equlibrium is reached

movement along the supply curve as suppliers increase prices and supply, as price goes up, demand goes down, movement along a new demand curve until a new equlibrium is reached

53

New cards

assumptions underlying the demand curve

substitution effect

income effect

law of diminishing marginal utility

income effect

law of diminishing marginal utility

54

New cards

substitution effect

if price of a good goes down, consumers will switch from other substitute goods to this good because the price is comparatively lower

55

New cards

income effect

if prices go down, then our real income (income that is adjusted to price changes) has increased because we can buy more goods and services. we feel wealthier and tend to buy more of the same goods or services

56

New cards

law of diminishing marginal utility

as we consume additional units of something, the utility we derive from each unit decreases

57

New cards

assumptions underlying the supply curve

increasing marginal costs

law of diminishing marginal returns

law of diminishing marginal returns

58

New cards

increasing marginal costs

when increasing the output of a good or service marginal costs (the cost of producing one more good or service) will go down at first, and then go up because of the law of diminishing marginal returns

59

New cards

law of diminishing marginal returns

at first when you add labor the output per worker will go up, but if you keep hiring workers the ouput per worker will go down