FINA 469 Midterm Exam 2

1/121

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

122 Terms

Closed-end funds are typically traded at a premium to NAV

False

Open-end funds cannot be shorted

True

Closed-end funds allow investors to trade index portfolios

False

Index EFTs typically follow passive strategies

True

Open-end funds offer a fixed number of shares

False

Everything else equal, which portfolio has a higher turnover rate?

1. An actively managed portfolio with interim transactions

2. A passive portfolio that needs no rebalancing

1. An actively managed portfolio with interim transactions

Closed-end fund

a fund with a fixed number of shares, shares cannot be redeemed

Shares outstanding do not change unless new shares are offered

closed-end fund

Fund share price trades at a discount to NAV

closed-end fund

Traded on the stock exchange and can be shorted

closed-end fund

Open-end fund

A fund that issues or redeems its shares at net asset value

Mutual fund is the common name for

an open-end investment company

Shares outstanding change when new shares are sold or old shares are redeemed

open-end fund

Fund share price = Net Asset Value (NAV)

open-end fund

Buy directly from the fund, traded once a day -- at close, cannot be shorted

open-end fund

May be forced to liquidate (sell) "good" stocks if facing an unexpected redemption wave

open-end fund

Exchange-traded funds (EFTS)

offshoots of mutual funds that allow investors to trade entire index portfolios

EFTs can trade like

shares of stock, unlike mutual funds, which can be bought or redeemed only at the end of the day or when the NAV is calculated

EFTs trade

continuously throughout the day

EFTS can be sold or purchased

on margin, can be sold short

EFTs typically trade at

NAV

EFTs typically track

indexes and follow passive strategies (low turnover)

EFTs potentially lower

tax rates

EFTs have lower

costs (no marketing, lower fund expenses)

EFT examples

SPY: Spiders (S&P 500 index)

DIA: Diamonds (Dow Jones Industrial Average)

VTI: Vangaourd Total Stock Market EFT

Who are EFT investors?

About 13% of US households (16.9 million) held EFTs in 2024

Fixed Income Securities

Security that obligates issuer to make payments to holder over time

Face Value, Par Value

Payment to bondholder at maturity of bond

Coupon Rate

Bond’s annual interest payment per dollar of par value

Bond Characteristics

Face Value, Par Value

Coupon Rate

Maturity

Default-free Fixed Income Securities

Debt issued by the government of developed countries

Coupon Bonds

A fixed income security that promises to pay fixed coupon payments at prespecified dates and a fixed principal amount at maturity

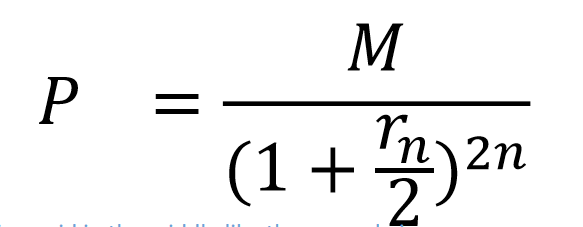

Zero Coupon Bond (ZCB)

When there is no promised coupon and the fixed income security only pays a fixed principal amount at maturity, the security is called a pure discount bond

Bond Value (Bond Pricing) =

Present par value + Present value of coupons

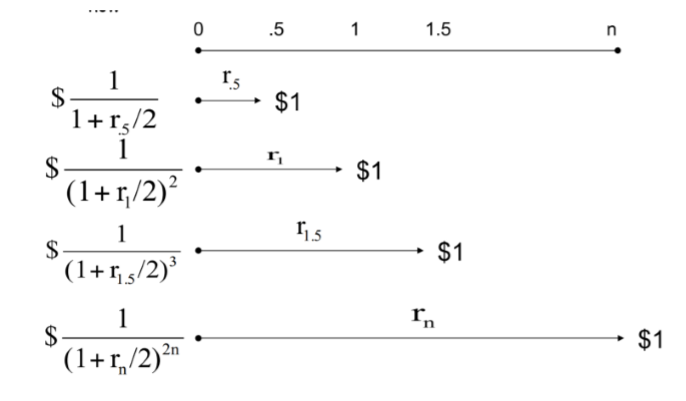

Spot Rates

Current interest rates for investments of various maturities

“n”

number of years/maturity

“rs”

annualized spot rate for s years

n-year spot rate applies only for

cash flows that occur exactly n years from now

Carries no coupons, provides all return in form of price appreciation

Zero-Coupon Bonds

For Treasuries, coupons and compounding are always

semi-annual

Present value formula for ZCB paying $M at maturity (after n years):

Nothing paid in the middle like the example in the previous slide. One price at end.

Coupon Bond Pricing

No-Arbitrage Bond Pricing, Present Value

No-Arbitrage Bond Pricing

The coupon bond cash flows are replicated by positions in ZCBs

If the coupon bond price is not the same as the cost of the equivalent portfolios of ZCBs, then there will be an arbitrage opportunities

Present Value

Using ZCB spot rates in the Present Value formula

Present Value Steps

Write down cash flows: semi-annual coupons (CF=C/2) and par payment (face value M)

Add up the present value of all coupon payments and par payment

“T”

maturity years, t = 0.5, 1, 1.5, 2, ……, T

Yield to Maturity (YTM)

Discount rate y that makes present value of bond’s payments equal to price. y is semi-annual

“C”

coupon payment

“M”

face value

YTM: annualized discount rate

twice the y

What is the YTM of a zero coupon bond?

the annualized rate of return earned by holding the bond until it matures

Price and YTM (for short, just call yield) move in

opposite directions

Price and coupons move in

same directions

Price and yields are

inversely related

Prices are convex

When yields increase, prices decline by less than prices increase when yields decrease

Current yield

bond’s annual coupon payment divided by the bond price

premium bonds

bonds selling above par value

coupon rate > current yield > YTM

discount bonds

bonds selling below par value

coupon rate < current yield < YTM

par bonds

bonds selling at par value

fixed-income instruments are risky even if ______ and _________ are guaranteed for Treasuries

coupon; principal

______ fall as market interest rate _____

prices; rises

interest rate fluctuations are a primary source of

bond market risk

bonds with ______ maturities are more sensitive to fluctuations in interest rate

longer

two types of interest rate risk

reinvestment risk

price risk

reinvestment risk

uncertainty surrounding cumulative future value of reinvested coupon payments

price risk

when interest rates move, bond prices change, affect price if you sell the bond

the two risks offset

decrease (increases) in interest rates cause capital gain (losses) but at the same time decrease (increase) the rate at which reinvested income will grow

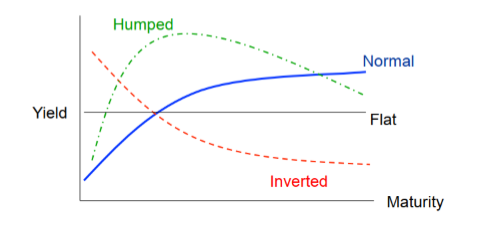

yield curve

graph of yield to maturity as function of term to maturity

PROBABLY SHORT ANSWER! term structure of interest rates

relationship between yields to maturity and terms to maturity across bonds

PROBABLY SHORT ANSWER! normal

short-term debt instruments have a lower yield, compensate investors for the risks of holding longer-term debt securities

PROBABLY SHORT ANSWER! inverted (also called negative yield curve)

a situation in which long-term debt instruments have lower yields. a predictor of economic recession

PROBABLY SHORT ANSWER! humped

a transition between normal and inverted

who determines short interest rates?

the federal reserve board control short interest rates (spot rates at short maturities) by setting the Federal Fund Rate

Extremely close relationship between short interest rates and _______

fed funds target rates

what is the fed supposed to do?

promote “maximum” output and employment

promote “stable” prices

long interest rates depend on

investors’ expectations of future policy and the economy

long rates are related to expected future _____ rates, expected inflation, and _____

short; risk premiums

short and long rates do not

always move together

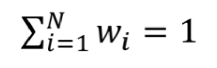

portfolio weights (w)

fraction of wealth invested in different assets

the weight of a security in a portfolio at a particular point in time is equal to

the security’s market value divided by the total value of the portfolio

N assets in a portfolio

can portfolio weights be negative (w<0)?

yes, borrowing/short selling

if you borrow money to purchase securities for your portfolio

the securities’ values add in as positive amounts to the market value of the portfolio, but the borrowed money comes in as a negative amount for the market value of the portfolio

a short sale occurs when

you sell something you do not have

when a short sale exists within a portfolio

the market value of the short security comes into the portfolio as a negative amount

capital allocation

between the risky portfolio and risk-free assets

asset allocation

in the risky portfolio across broad asset classes (e.g., U.S. stocks, international stocks, and long-term bonds)

security selection

of individual assets within each asset class

complete portfolio

entire portfolio, including risky and risk-free assets

capital allocation

choice between risky and risk-free assets

E(rc)

expected return of the complete portfolio

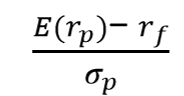

E(rp)

expected return of the risky portfolio

rf

return of the risk free asset

y

percentage assets in the risky portfolio

σc

standard deviation of the complete portfolio

σp

standard deviation of the risky portfolio

Capital Allocation Line (CAL)

set of portfolios that can be chosen by allocating different proportions of an investor’s wealth to the risky assets and the risk-free asset

what’s the slope of the CAL?

sharp ratio of the risky assets

weighted average of returns on components with investment proportions as weights

weighted average of expected returns on components, with portfolio proportions as weights