Economics Test 1

1/44

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

45 Terms

Macroeconomics

study of whole part of economy and how each economy (country’s, city, etc) interact with others

Minimum wage, unemployment rate, inflation, GDP

Who is considered the founder of modern macroeconomics?

John Maynard Kaynes

Believe government do big things (policy, funding, etc) and change country state

Microeconomics

study of individuals, households, firms in decision making and allocation of resources

Business making decisions, how narrow policies affect single entities, individual markets

Opportunity cost

most desirable alternative that was given up as result of final decision being made/chosen

Can only be one

Most important option picked, next important option given up (opportunity cost)

Trade-offs

other things you give up beside most desirable outcome/alternative

Individual trade-offs

personal choices made

ex: personal spending or time allocation

Business trade-offs

how to use land, labor, capital

Society trade-offs (relate to gov)

chose where to what to spend money on -> ex: fund social security or reduce payments and use government money for something else

“guns or butter”

Factors of production

land, labor, capital -> all resources sacre, must make decision on how to use/allocate them

Land

all natural resources

clean air and water, renewable and nonrenewable

Labor

the work you do

Capital

physical and human capital

Physical Capital:

tools used to do work/labor

Human Capital

your skills, ability, knowledge (soft and hard skills) -> you’re in control of the things you bring to table

Entrepreneurship is human capital (“skill”)

What is money?

Money serves as transaction

Use money to buy resource, physical capital, human capital, labor, natural resources

not a resource or factor of production

Scarcity

refers to state when resource is available in finite quantities at particular point of time (limited)

Usually created by nature and involve nature resources

Shortage

situation in which quantity of a good or service demand by consumers exceeds the quantity supplied at the current price

Usually created by ppl/market

What results from scarcity or shortages? (what is outcome?)

Both usually lead to limited availability of products and higher prices

Who is Adam Smith?

father of modern economics who outlined capitalism

What is Adam Smith’s theory of markets?

Invisible hand theory

What is the Invisible hand theory?

ppl are rational, make rational decisions for their best interests, leave them alone and economy sort itself out (reach equilibrium)

Gov don’t need to intervene in economy

Market sort itself out but take a long time

What book did Adam Smith write and when?

He wrote the Wealth of Nations in 1776

Free (capitalistic) economy

the government is less involved in the economy, doesn’t own factors of production, doesn’t plan the economy out (ex: doesn’t plan how much goods produced, production, etc), lets businesses/individuals run freely

Command economy (planned)

the government is heavily involved in economy, owns factors of production, plan the economy out (ex: how much wheat needs to produced, etc) in best interests of the people

How are economies mixed? (Mixed economy)

Economies combine elements of capitalism and command/planned economies together, usually get socialism

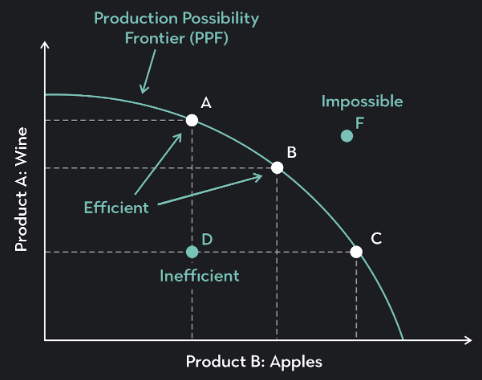

Explain the points on the Production Possibility Curve

points on the curve indicate production is at full capacity (efficient)

Points A, B, C

production is inefficient and not running at full capacity when point inside the curve → point D

economy cannot produce that amount of goods given current factors of production when point above/beyond the curve → point F

Efficient (PPF)

economy is running at full capacity

Inefficient (PPF)

economy is not running at full capacity

Have resources but not using them effectively

No demand for products

Layoffs, slowed production

Indicate recession

Impossible (PPF)

given current factors of production economy cannot product that amount of goods unless if factor of production are expanded

What can move a PPC to the impossible?

Increase of land, labor, capital, and technology to expand production

What does increasing and decreasing opportunity costs have in common?

a person/company must give up something when producing more of one good or another

Increasing Opportunity costs

production of a good increases, the opportunity cost of producing another good rises because resources cannot efficiently produce all goods equally

What is an example of increasing opportunity costs?

Ex: Starbucks only make coffee, and begin making sandwiches, overtime to maximize production, produce more sandwiches and less coffee

Decreasing Opportunity costs

cost of sacrificing production of main good diminishes as more resources are allocated to another good, often resulting from specialization or efficiency gains

What is an example of decreasing opportunity costs?

Ex: Apple initially face high cost for producing laptops and give up producing iphones, but overtime workers more specialized and give up less to produce iphone and laptops

Constant Opportunity costs

trade-offs between producing 2 goods remain unchanged/constant as production shifts

What is an example of constant opportunity costs?

Give up 5 tacos to produce 5 burgers

Comparative advantage

have comparative advantage in producing good or service if opportunity cost of producing good is lower for that individual than others

China make 10 cars a day and 5 shoes while America make 5 cars a day and 10 shoes—who has the comparative advantage in cars?

China have comparative advantage in cars

Absolute advantage

in an activity if individual do it better than others -> use less input and get more output, etc

China make 20 cars a day, while America make 10 cars a day—who has the absolute advantage?

China has the absolute advantage

What do countries do in trade? (involve comparative and absolute advantages)

In trade, 2 countries specialize in good where they have comparative advantage and trade for other product leading to better production and economic advantage

Productivity

amount of output per hour

Produce more output with less input or produce more output with same input

How does labor productivity increase?

increase when get more output with same input or same output with less input

How does productivity (overall) increase?

Increase through tech advance, improve worker skills, improve management practices