5.5 Break-even analysis BM

1/26

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

27 Terms

Break-even

when a firm’s sales revenues cover all of its production costs.

Break-even quantity

the level of output where a business does

not make either a profit or a loss. The formula for calculating the BEQ is:

Contribution per unit / unit contribution

the amount of money earned from each unit of the product sold to customers.

Selling Price - AVC

Total contribution

(P-AVC)Q

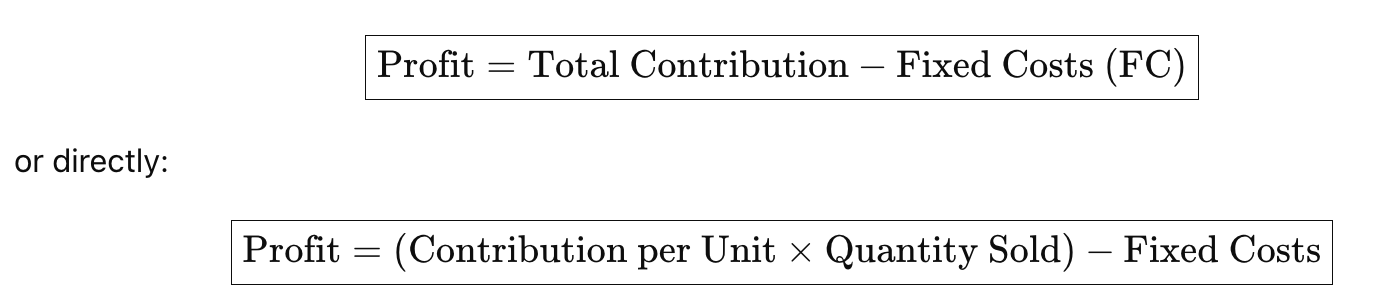

Profit

positive difference between a firm's total revenue

and its total costs. Profit is shown in a break-even chart at all

levels of output beyond the break-even quantity.

[(P-AVC)Q]-TFC

Value added per unit

P - ATC

Margin of Safety

numerical difference between how much the business sells and its BEQ

Quantity sold - BEQ

Target profit output (or target profit quantity)

quantity of sales required to reach the firm’s target profit. It is calculated using the formula:

Target profit quantity = (Fixed cost + Target profit) / (Price – Average Variable Cost)

Target profit

the amount (value) of profit that a firm aims to earn within a given time period. The target profit for each level of output can been seen in a break-even chart by comparing the total cost and total revenue lines.

Target price

the amount customers need to pay per unit in order for the firm to break-even or to reach

a particular target profit. The formula used to calculate the target price for break-even is:

Contribution

the difference between the sales revenue earned from

selling a product (its price) and the variable costs of producing the product.

• Unit contribution = P – AVC

Break even analysis

a decision-making tool used to calculate the level of sales needed to cover all costs of production. Any sales beyond the break-even point generate a positive safety margin and hence profit for the business.

Break-even chart

a diagrammatic representation of a firm's

costs, revenues and profits ( or loss) at various levels of output.

Break-even point

the position on a break-even chart

where the total cost line intersects the total revenue line. This is

shown at the point where TC = TR.

Loss

firm's total costs exceed its total revenues

(TC > TR). This occurs at all levels of output or sales below the

break-even quantity.

Total Cost

Total Revenue

Profit

Average Cost

Average Fixed Cost

Average variable cost

Revenue per unit (Price)

Contribution per unit

Total contribution

Break even output

Margin of Safety

Required Sales (Units) to Achieve Target Profit