1.1 What is Economics?

1/26

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

27 Terms

Difference between micro and macro economics?

Microeconomics studies individual markets and choices, households, and firms.

Macroeconomics studies the entire economy, focusing on government policies, economic growth, and interaction with the rest of the world.

Scarcity

unlimited wants but limited resources- suppliers are unable to meet the economies wants due to the scale being too high to fulfil

Efficiency + allowcative effeciency

Efficiency is determined by the ratio of useful output to total input. Allocative efficiency refers to making the best possible use of scarce resources to produce the combinations of goods and services that are optimum for society, thus minimising resource waste.

Intervention

Intervention in economics usually refers to government involvement in the workings of markets.

Change

The economic world is continuously changing, and economists must adapt their thinking accordingly.

Choice

Since resources are scarce, economics is a study of choices. Not all needs and wants can be satisfied; this necessitates choice and gives rise to the idea of opportunity cost.

Sustainability

Sustainability is the ability of the present generation to meet its needs without compromising the ability of future generations to meet their own needs.

Equity

In contrast to equality, equity refers to the idea of fairness, which is a normative concept. The degree to which markets versus governments should, or are able to, create greater equity or equality in an economy is an area of much debate.

Interdependence

Individuals, communities, and nations are not self-sufficient. Consumers, companies, households, workers, and governments—all economic actors—interact with each other within and, increasingly, across nations in order to achieve economic goals.

Economic Well-being

Economic well-being is a multidimensional concept relating to the level of prosperity and quality of living standards enjoyed by members of an economy. It includes present and future financial security, the ability to meet basic needs, the ability to make economic choices permitting achievement of personal satisfaction, and the ability to maintain adequate income levels over the long term.

4 factors of production

CELL stands for Capital, Entrepreneurship, Land, and Labor.

What is the basic economic problem?

People have unlimted wants, but resources are finite, leading to scarcity. This fundamental economic problem requires choices to be made about the allocation of limited resources to meet those wants. Scarcity forces individuals and societies to prioritize their needs.

Economic Agent

Any decisions maker in the economy

Opportunity Costs

The value for next best alternative while making the decision

Enterprise meaning in CELL production

Enterprise refers to the people who organise and co-ordinate the other three factors of production. Some economists regard entrepreneurs as a specialist form of labour input. Others believe that they deserve recognition as a separate factor of production in their own right.

Free Economies

Systems where buying + selling goods → not in control.

Economic goods

Scarce in relation to the demand for them

Free goods

are abundant in supply(water,air)

What is the The Production Possibilities Curve Model (PPC)

The Production Possibility Curve (PPC) is an economic model that considers the maximum possible production (output) that a country can generate if it uses all of its factors of production to produce only two goods/services.

Some assumptions of the PPC model?

1. Only two goods are produced: any two goods can be used to illustrate the underlying principle. In reality, an economy produces many goods/services but focusing on two makes the analysis possible

2. Scarcity of resources exists: the factors of production are limited so choices have to be made about how they are used.

3. Production is efficient: it is assumed that there is no wastage and that all resources are used in such a way that the maximum output is attained from the inputs used. In reality, this is often not the case.

4. The state of technology is fixed: as the model represents a particular moment in time, it is assumed that the technology is not changing. In reality, improvements in technology are continuously occurring and they create the potential to increase the output using the scarce resources.

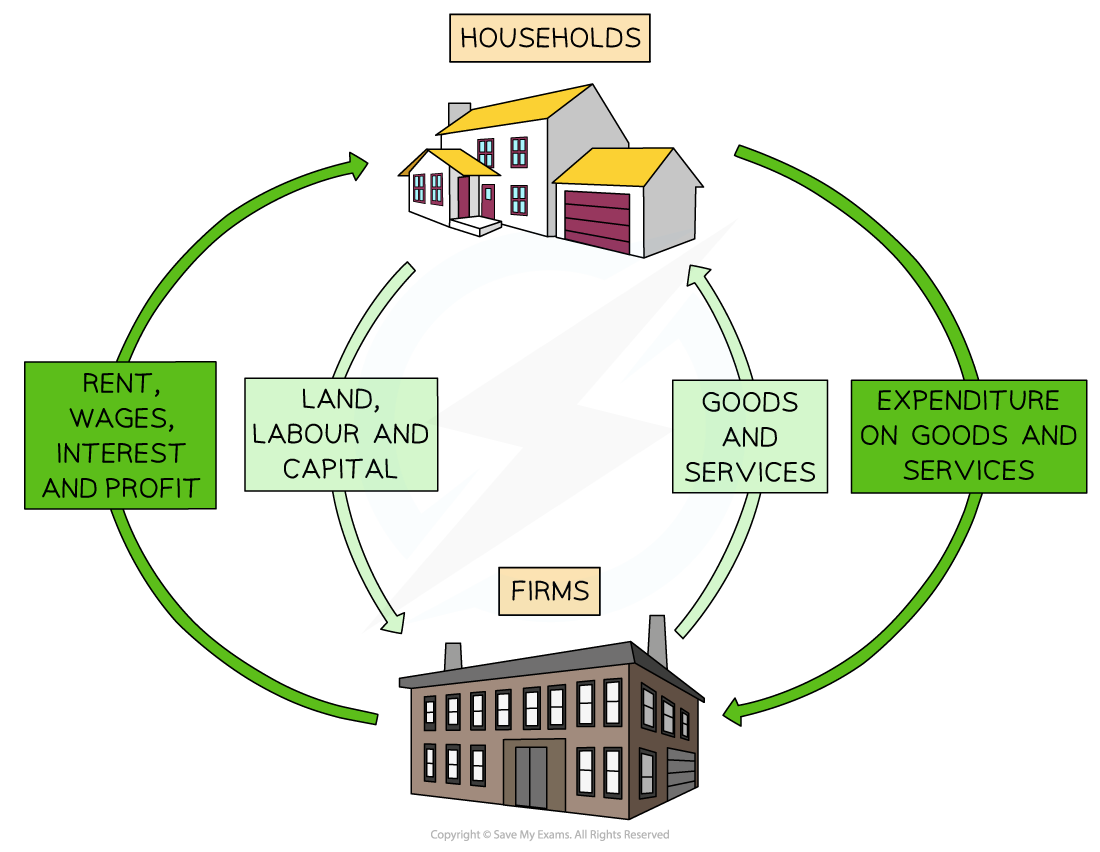

The Circular Flow of Income

Leakages + Injections

Injections add money into the circular flow of income and increase its size eg:

Increased investment (I)

Increased exports (X)

Increased government spending (G)

Leakages (withdrawals) remove money from the circular flow of income and reduce its size

Increased savings by households (S)

Increased taxation by the government (T)

Increased import purchases (M)

Planned vs Free Market

Planned economies: better access to essential resources

Stable employment

Consumers protected from demerit goods

Better access to merit goods

Free: Bigger range of resources available

More innovation

Higher quality goods → competetion betweeen firms

Planned economy?

Complete government interventention on allocation of resources.

Tell businesses what to produce and how much to produce

Government own key industries with large stake

Free economy

System where resources are not allowcated by governments but only firms

→ ‘market forces’ of demand and supply control allocation of goods and services.

→ adam smith → inviisble hand

Mixed economy

Combination of public and private sector = planned + free

Most economies this run way.

What does the PPC curve diagram show us? (3)

The use of the PPC depicts the maximum production of an economy, → shows possible cominations of the maximum output using all of its resources?

Use of PPC to depit oppurtunity costs → producing more of one good requires sacrifice of the other

The use of PPC to depict efficiency, inefficiency, attainable and unattainable production, any point inside the curve represents inefficiency on the line shows efficiency, while points outside are unattainable.