Chapter 6: Internal Control in a Financial Statement Audit

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

28 Terms

what is the purpose of internal control (2)

midigate risk

prevent or detective

auditor or management

________has the responsibility to maintain controls that provide

reasonable assurance that adequate control exists over the entityʼs assets and records.

management

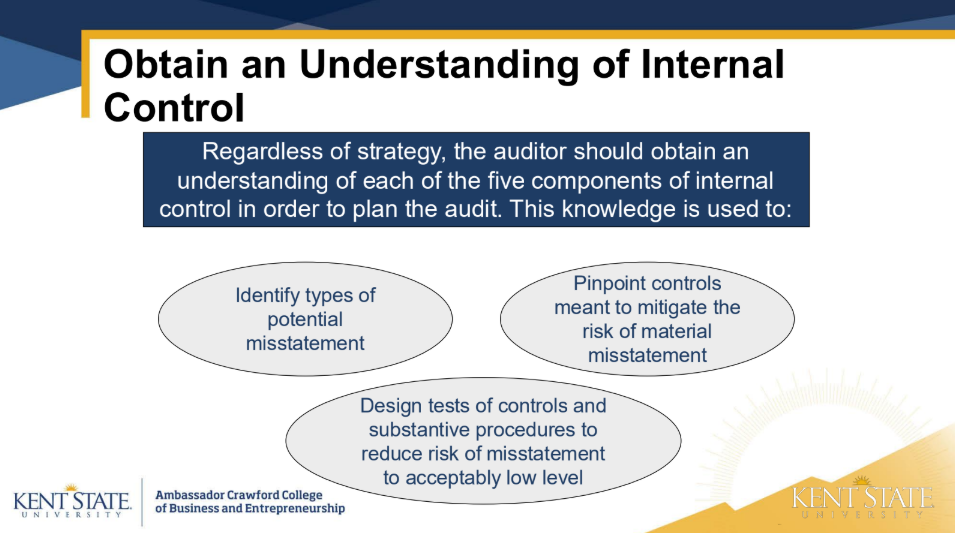

The auditor uses risk assessment procedures to: (4)

• understanding internal control

• Identify key controls

• types of potential misstatements

• Design tests of controls and substantive procedures

The auditor’s understanding of the internal control is a major factor in determining the overall audit strategy.

auditor or managerment responabilities

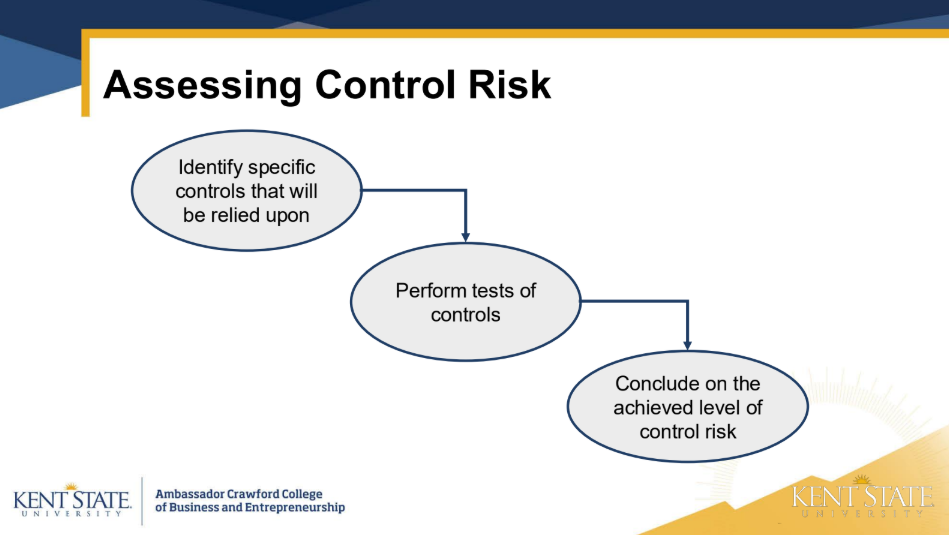

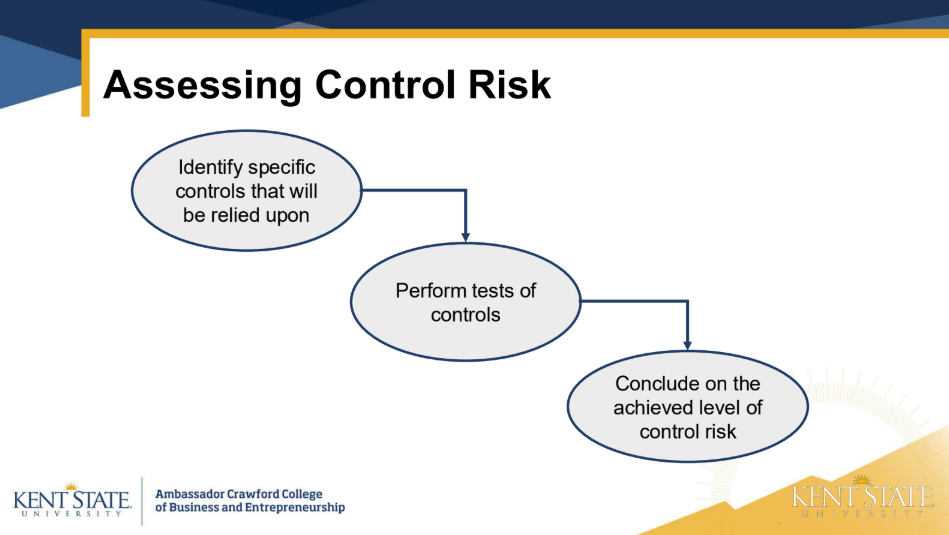

1) Obtain an understanding of internal controls

2) Assess control risk

auditor

An auditor’s primary consideration regarding an entity’s

internal controls is whether they

A.Prevent management override

B.Relate to the control environment

C.Reflect management’s philosophy and operating style

D.Affect the financial statement assertions

D.Affect the financial statement assertions

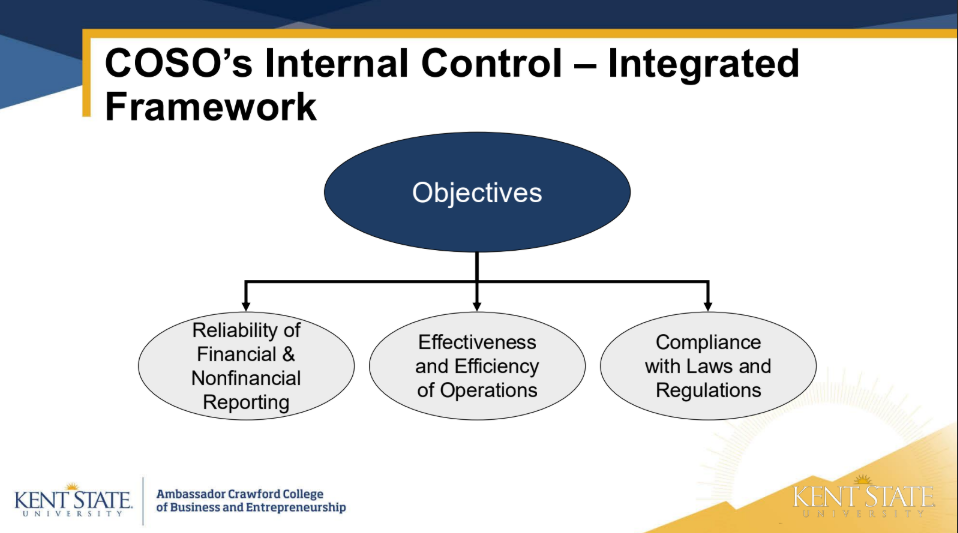

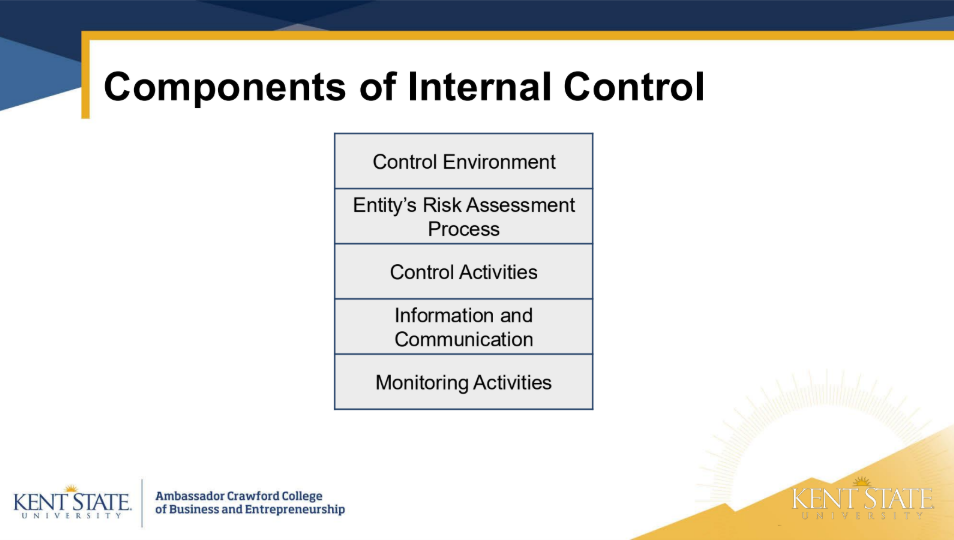

what is control environment

The control environment consists stuff form the foundation for internal control, set by the board and senior management

what is risk assessment

a dynamic process of identifying and analyzing risks to achieving objectives

what is control activities

actions taken by management's to reduce risks and help achieve objectives

what is information and communcation

what’s needed to run internal controls and meet objectives. Clear communication helps staff understand their roles and keeps management informed.

what is monitoring activities

Internal controls are monitored through ongoing or separate evaluations to ensure all components are working. Issues are reviewed and serious problems are reported to senior management and the board.

reason why control will be set at high

controls do not pertain to an assertion

controls are assessed as ineffective

testing the effectiveness of controls is inefficient

what is a reliance strategy

• Plan to rely on internal control and assess control risk at a

lower level

the level of control risk is set in terms of assertion about classes of transactions and event, and related disclosures, for the period under audit

Substantive vs. Reliance Strategy - How are they different?

• Substantive Strategy: Set CR at the max

• Reliance Strategy: Set preliminary CR below the max, test controls, then

adjust CR based on results of tests of controls

After obtaining an understanding of an entity’s internal control system, an auditor may set control risk at high for some assertions because the auditor

A.Believes the internal controls are unlikely to be effective

B.Determines that the pertinent internal control components are not well documented

C.Performs tests of controls to restrict detection risk to an acceptable level

D.Identifies internal controls that are likely to prevent material misstatements

A.Believes the internal controls are unlikely to be effective

how does entity size effect on internal control

All companies should have the five components of internal control, but in small or midsize businesses, they’re usually less formal than in large companies.

what are the 3 limitation of an entity’s internal control

management override of internal control

human errors of mistakes

collusion

Which of the following audit techniques would likely provide an auditor with the least assurance about the effectiveness of the operation of a control?

A.Inquiry of entity personnel

B.Reperformance of the control by the auditor

C.Observation of entity personnel

D.Walkthrough

A.Inquiry of entity personnel

what is control deficiency

A control deficiency exists when a control’s design or operation doesn’t let staff prevent or catch mistakes in time

what is significant

A control deficiency that's not severe but still important enough to report to those in charge.

what is material weakness

A control deficiency that could likely cause a material misstatement to go unnoticed or uncorrected in time.