supply&demand + elasticity (quiz 3)

1/60

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

61 Terms

market economy

resources are allocated among households and firms with little or no government interference

market

a collection of buyers and sellers of a particular product or service

competitive market

exists when there are so many buyers and sellers that each has only a SMALL IMPACT on the market price and output

goods sold by each vendor are similar

imperfect markets

either the buyer or the seller can influence the market price

more UNIQUE goods

market power

a firms ability to influence the price of a good or service by exercising control over its demand, supply, or both

monopoly

when a single company supplies the entire market for a particular good or service

quantity demanded

the AMOUNT of a good or service that a consumer is willing and able to purchase at a given price

law of demand

when price goes up, quantity demanded goes down

when price goes down, quantity demanded goes up

inverse relationship

demand schedule

table showing the relationship between price and good

demand curve

a graph of the relationship between the prices in the demand schedule and the quantity demanded at those prices

market demand

sum of all the individual quantities demanded by each buyer in the market at each price

quantity demanded shifts demand curve. how does it shift with an increase or decrease?

Increase: shifts right

Decrease: shifts left

factors that shift a demand curve:

income

price of related goods

changes in taste and preferences

expectations of future prices

number of buyers

taxes and subsidies

purchasing power

the value of your income expressed in terms of how much you can afford

normal good

consumers buy more as income rises

ex: meals at a restaurant

inferior good

demand declines as income rises

(they can afford something better)

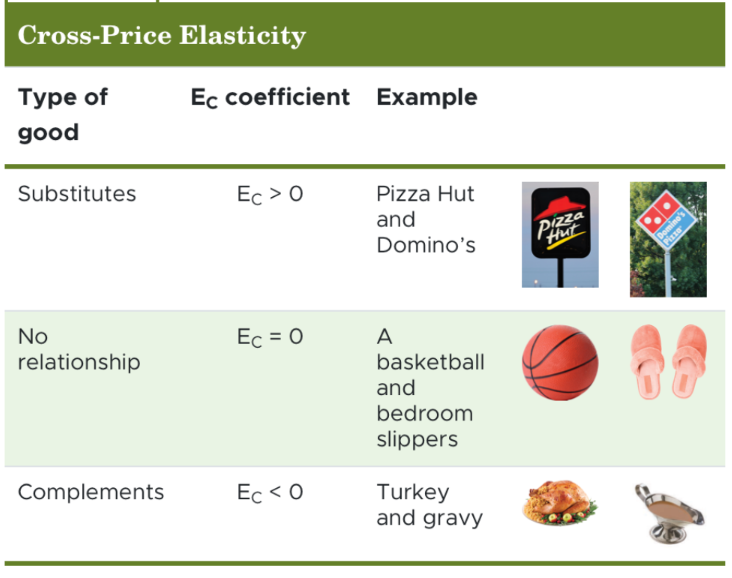

complements

two goods that are bought and used together

when price goes up, quantity demanded of that good AND of related good goes down

substitutes

two goods that are used in place of each other

when price increases for this good, quantity demanded this good DECREASES while for the other good increases

subsidy

a payment made by the government to encourage the consumption or production of a good or service

quantity supplied

amount of a good or service producers are willing and able to sell at the current price ^price, ^quantity supplied ... v prices, v quantity supplied

law of supply

quantity supplied of a good rises when the price of a good rises, and falls when the price of a good falls

direct relationship

supply schedule

a table showing the direct relationship between the price of a good and the quantity supplied

supply curve

a graph of the relationship between the prices in the supply schedule and the quantity supplied at those prices

positive curve: direct (positive) relationship between the price and the quantity offered for sale

factors that shift a supply curve:

cost of inputs

changes in technology or the production process

taxes and subsidies

number of firms in the industry

price expectations

when would a supply curve shift left?

if the change would reduce the amount of a good or service a business is willing and able to supply at every given price

when would a supply curve shift right?

if the change would increase the amount of a good or service a business is willing and able to supply at every given price

inputs

resources used in the production process

an increase in technology would shift supply curve to the...

right

^production process, ^supply, shifts to the right

how do taxes impact supply curve?

taxes make firms less profitable -> lower profits make firms less willing to supply product -> supply curve shifts left -> overall supply declines

REVERSE FOR SUBSIDIES

how do the number of firms in the industry affect the supply curve?

shifts left

equilibrium

the point where the demand curve and supply curve intersect

equilibrium price

the price at which the quantity supplied is equal to the quantity demanded

equilibrium quantity

amount where quantity supplied = quantity demanded

law of supply and demanded

the market price of any good will adjust to bring the quantity supplied and supply demanded into balance

shortage

quantity supplied < quantity demanded

surplus

quantity supplied > quantity demanded

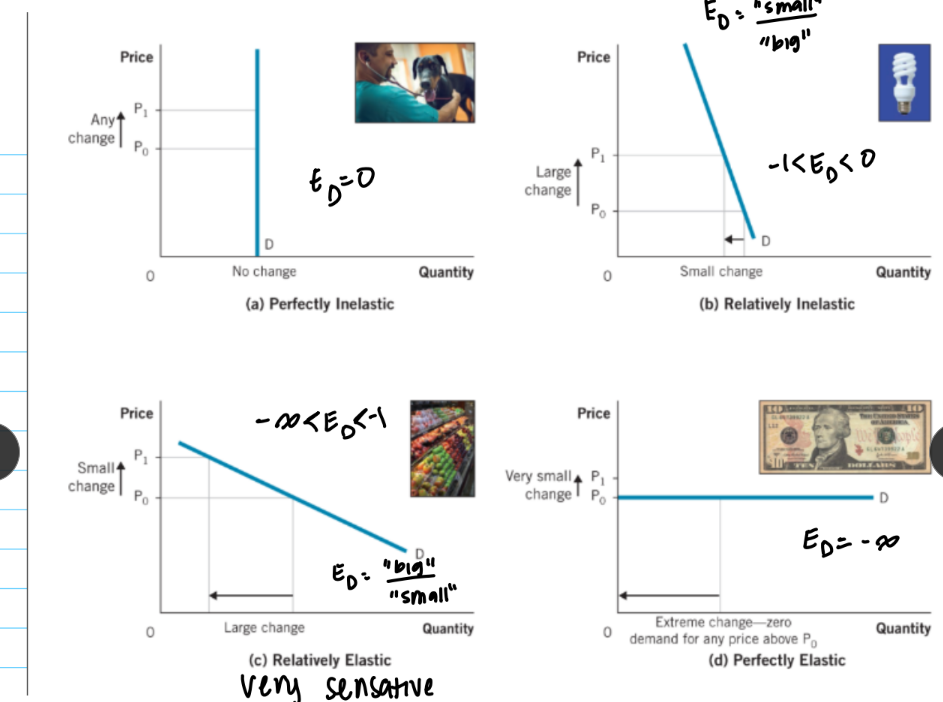

elasticity

a measure of the responsiveness of buyers and sellers to changes in price or income

elastic

if the quantity demanded changes significantly as a result of price change

inelastic

if quantity demanded changes a small amount as a result of a price change

price elasticity of demand

measures the responsiveness of quantity demanded to a change in price

determinants of price elasticity of demand

existence of substitutes

share of the budget spent on the good

demand is more inelastic for inexpensive items on sale

necessities vs luxury goods

necessities = inelastic

whether the market is broadly or narrowly defined

broad (ex: “toothpaste”) = inelastic

narrow (ex: “Crest toothpaste”) = elastic

time + the adjustment process

demand is more elastic in the long run

immediate run

there is no time for consumers to adjust their behavior

ex: demand for gas

short run

a period of time when consumers can partially adjust their behavior

long run

a period of time when consumers have time to fully adjust to market conditions - demand becomes more elastic

price elasticity of demand formula

percent change in quantity demanded / percent change in price

midpoint method formula

(Q2 - Q1) / [(Q2 + Q1) / 2] / (P2 - P1) / [(P2 + P1) / 2]

elasticity coefficient range interpretation

-inf < elastic < -1 < inelastic < 0

total revenue and formula

the amount a firm receives from the sale of goods and services

quantity sold x price of good

graphs of price elasticities of demand

how does total revenue change when lowering price with elasticity of demand?

demand is elastic, lowering price increases total revenue

demand is inelastic, lowering price decreases total revenue

income elasticity of demand

measures how a change in income affects spending

income elasticity formula

percent change in quantity demanded / percent change in income

income elasticity of a necessary normal good

0 < EI < 1

income elasticity of a luxury normal good

EI > 1

EI of inferior goods

have negative income elasticity

as income expands, demand for these goods declines

cross-price elasticity formula

EC = percent change in quantity demanded of one good / percent change in price of related good

cross-price elasticity coefficient interpretation

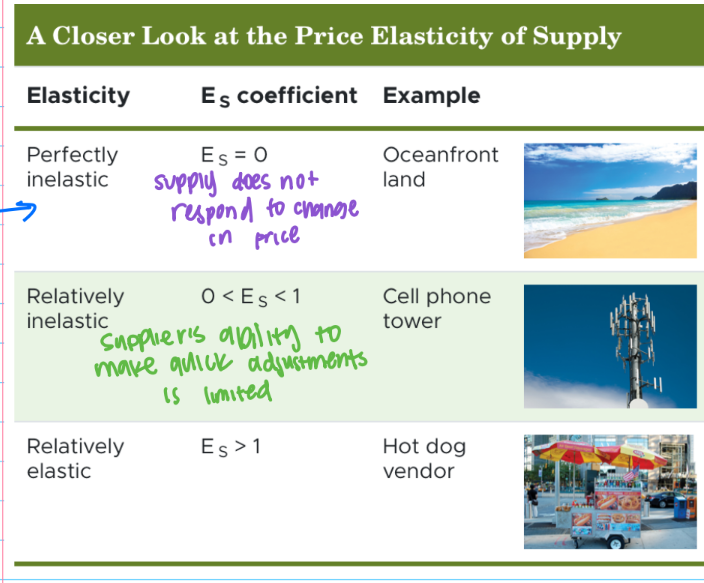

price elasticity of supply

a measure of the responsiveness of the quantity supplied to a change in price

price elasticity of supply coefficient interpretation

ES = percent change in QS / percent change in price

determinants of price elasticity of supply

flexibility of producers

when a producer can quickly ramp up an output, supply tends to be elastic

time and adjustment process

immediate run → short run → long run: supply (like demand) becomes more elastic

rotation of curves as they become more elastic

supply curve → rotates clockwise

demand curve → rotates counterclockwise