Econ 101

1/309

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

310 Terms

marginal product of labor

the extra output you produce from hiring an extra worker

marginal revenue product

marginal product of labor * price

marginal revenue product

the extra revenue produced by hiring an additional worked

rational rule for employers

hire an additional worker if the marginal revenue product is greater than or = wage, this maximizes the business profit

labor demand curve

shows the relationship between the quantity of labor demanded by firms and the wage rate, illustrating how many workers firms are willing to hire at different wage levels. It is the same as marginal revenue product of labor, downwards sloping because of diminishing marginal product

labor demand shifters

changes in demand for your product

changes in the price of capital

scale effect

substitution effect

better management and productivity gains

Nonwage benefit, subsidies, and taxes

scale effect

when the price of capital goods declines so you can produce output at a lower cost so you will sell a larger quantity or produce at a larger scale. Leads to increases labor demand

substitution effect

when the price of capital goods declines so the demand for workers to do tasks that can be done by machines decreases

scale effect

when it dominates labor and capital are complements and demand curve shifts right

substitution effect

when it dominates labor and capital are substitutes and demand curve shifts left

rational rule for workers

work one more hour as long as the wage is at least as large as the marginal benefit of another hour of leisure.

substitution effect (workers)

says higher wages make work relatively more attractive

income effect

higher income makes leisure more attractive

price elasticity of labor supply

measures worker’s responsiveness to wages

why the market labor supply curve is upwards sloping

new people induced to enter workforce

existing workers may put in more hours

some people may switch occupations

labor supply curve shifters

changing wages in other occupations

changing the number of potential workers

changing benefits of not working

nonwage benefits, subsidies, and taxes

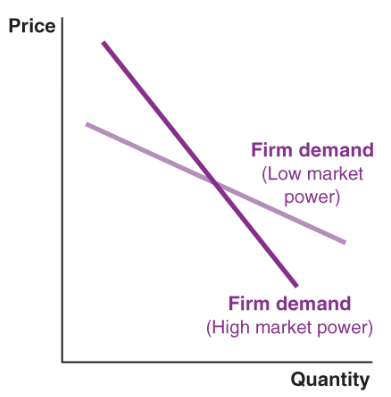

market power

the ability to raise your price without losing many sales to competing businesses

monopoly

only one seller in the market, lots of market power

oligopoly

a market dominated by a handful of large sellers , a strategic battle for market share

Monopolistic competition

product differentiation, having more competitors leads to less market power

product differentiation

making products differ from those offered by their competitors, sellers hope to make each the varieties attractive to a specific group of customers. Can be the product, shipping, or brand image. Ex: Jeans

imperfect competition facts

having more competitors leads to less market power

market power allows you to pursue independent pricing strategies

successful product differentiation gives you market power

imperfect competition among buyers gives them bargaining power

best choice depends on the actions that other businesses take

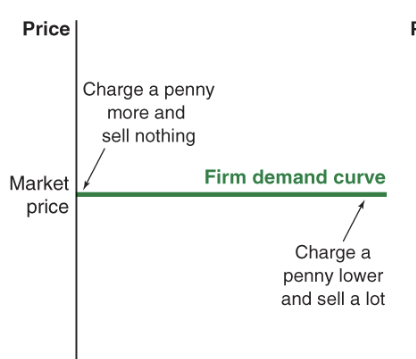

firm demand curve

how the quantity that buyers demand from your individual firm varies as you change your price

perfect competition demand curve

.

monopolistic competition and oligopoly demand curves

.

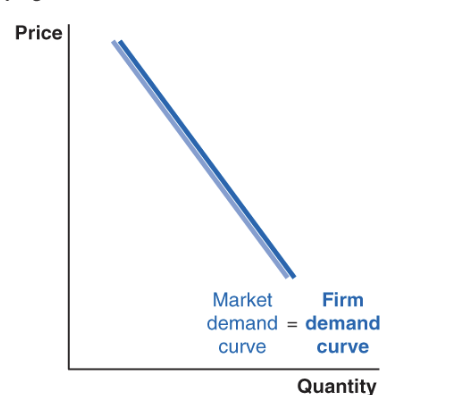

monopoly demand curve

also market demand curve

marginal revenue

change in total revenue from selling one more unit, reflect output effect -discount effect

output effect

an extra unit of output will boost revenue by an amount equal to the price of an extra item sold

discount effect

equal to the discount they need to give to sell one more item multiplied by the quantity sold that gets that price count

rational rule for sellers

sell one more unit if the marginal revenue is at least as large as the marginal cost

problems with high market power

sellers exploit mp

higher prices

inefficient smaller quantity

larger economic profits

businesses surviving inefficiently high costs

policies that ensure competition

anticollusion laws

merger laws

monopolizing is illegal

encouraging international trade

human capital

what employers look for. determines wages, accumulated knowledge and skills, education makes you more productive

education as a signal

of ability, the cost of completing a degree for those who are not hardworking is too high, degree is a signal

asymmetric information

workers signal, employers screen

an effective signal is one that is easier for the skilled worker

efficiency wage

employers pay workers more to make them more productive

compensating differential

the difference in wages required to offset the desirable or undesirable aspects of a job.

encourages people to take unpleasant jobs

depends of preferences of other workers

ex: makeup on real people vs dead people

firm

a web of contracts between input suppliers and the owners/managers of the firm

production

the process by which inputs are combined, transformed, and turned into outputs

accounting profit

total revenue - explicit financial costs

economic profit

total revenue - explicit financial costs -implicit opportunity costs

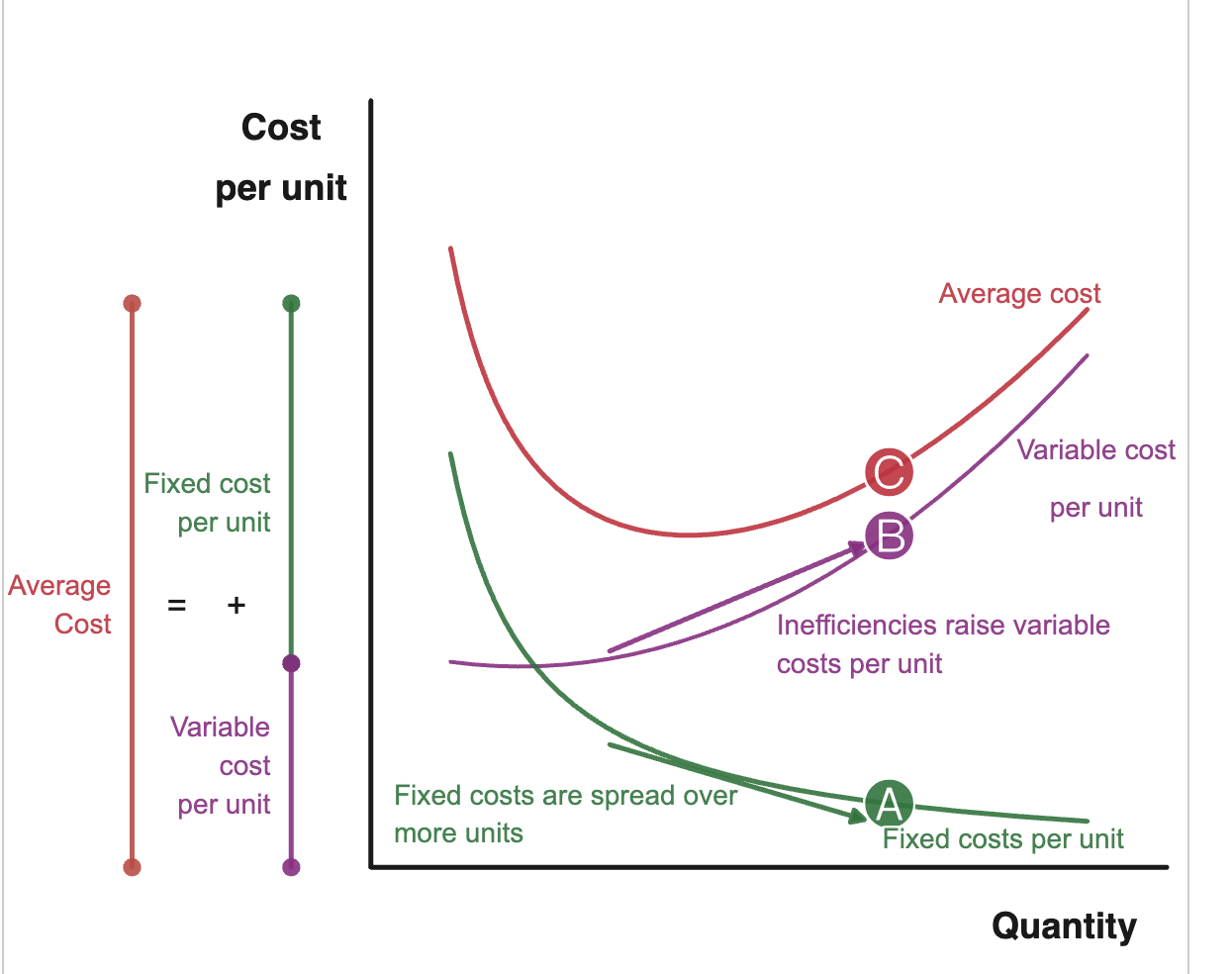

average revenue

price or revenue per unit, with more quantity fixed costs decrease but variable costs increase

average revenue

total revenue

quantity

average revenue

fixed costs + variable costs

quantity + quantity

profit margin

price - average cost

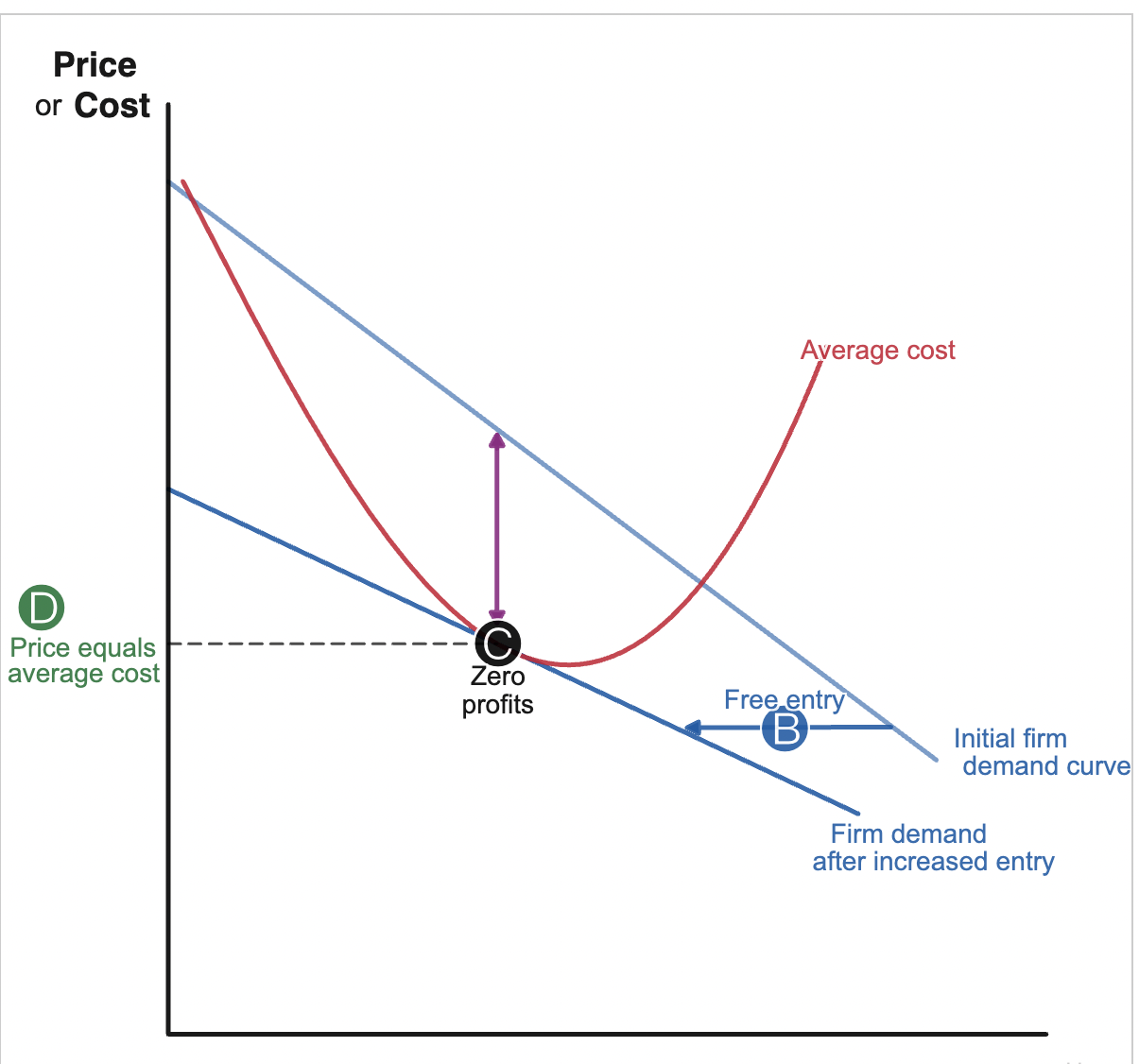

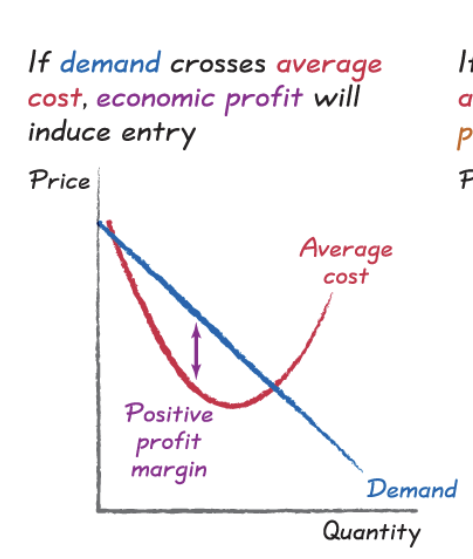

rational rule for entry

enter a new market if you expect to earn a positive economic profit, when price > average cost

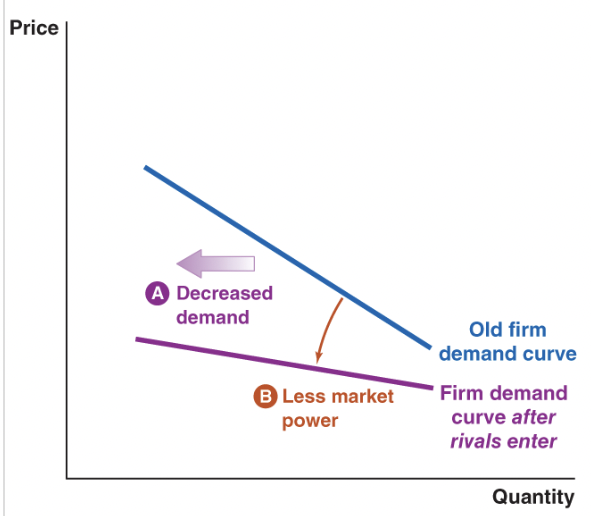

new competition enters market

makes the market less profitable, leads to decreased market power, shifts demand curve for firm left, and demand curve becomes more elastic so flatter curve

competition exits market

makes the market more profitable, increases demand, more inelastic , increased market power

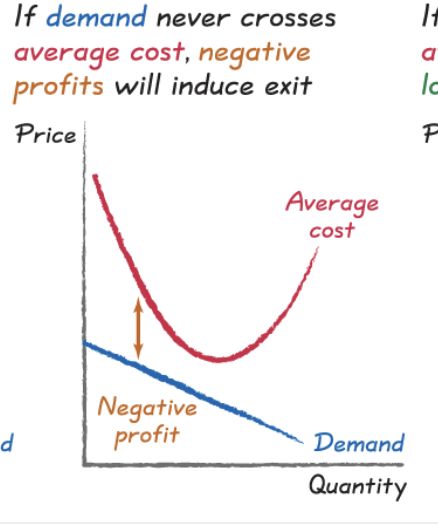

rational rule for exit

exit a market if you expect to earn a negative economic profit, when price < average cost

free entry

no factors making it particularly difficult or costly for a new business to enter the market, pushes economic profits down to zero in the long run, pushes price down toward average cost

free exit

no factors making it particularly difficult or costly for a new business to exit the market, ensure the market won’t remain unprofitable in the long run, pushes price up towards average cost

zero profits

.

positive profits

.

negative profits

.

barriers to entry

obstacles that make it more difficult for new suppliers to enter the market

demand side strategies

supply side strategies

regulatory strategies

entry deterrence strategies

demand side strategies

create customer lock in, use switching costs, earn goodwill from customers to keep customers loyal, develop network effects

switching costs

any immediate thing that makes it difficult or costly for your customers to buy from another business instead.

supply side strategies

develop unique cost advantages through experience, mass production, research and development, relationships with input suppliers, limit key inputs

regulatory strategies

enlist government policies to prevent entry, patents, government licenses,

entry deterrence strategies

to scare off potential rivals, convince rivals that if they enter the markets that you will crush them, need to build excess capacity, have financial resources, brand proliferation, have a reputation for fighting

overcoming barriers for entry

demand side strategies to combat customer lock in, supply side strategies to combat cost disadvantages, use regulatory strategies to secure government help, overcome deterrence strategies to fight bad guys

competitive merger

creates more fearsome competition, bad for rivals, could be good for consumers

noncompetitive merger

reduces competition, good for rivals, bad for consumers

natural monopoly

an industry that realizes such large economies of scale in producing its product that single firm production of that good or service is most efficient. Ex: utilities

natural monopoly solutions

government provides goods: set price = marginal cost, tax revenue pays for losses

let private sector supply: price = average cost

price discrimination

the strategy of selling the same product at different prices

reservation price

the maximum price that a customer will pay

perfect price discrimination

when you charge each customer their reservation price. leads to

charging highest possible price

make every possible sale

redistributes economic surplus from buyers to sellers,

efficiency of price discrimination

increase the quantity sold, helps solve underproduction problem, reduces discount effect the more accurate the discrimination is

price discrimination requirements

market power

ways to prevent resale

need to target the right prices to the right customers

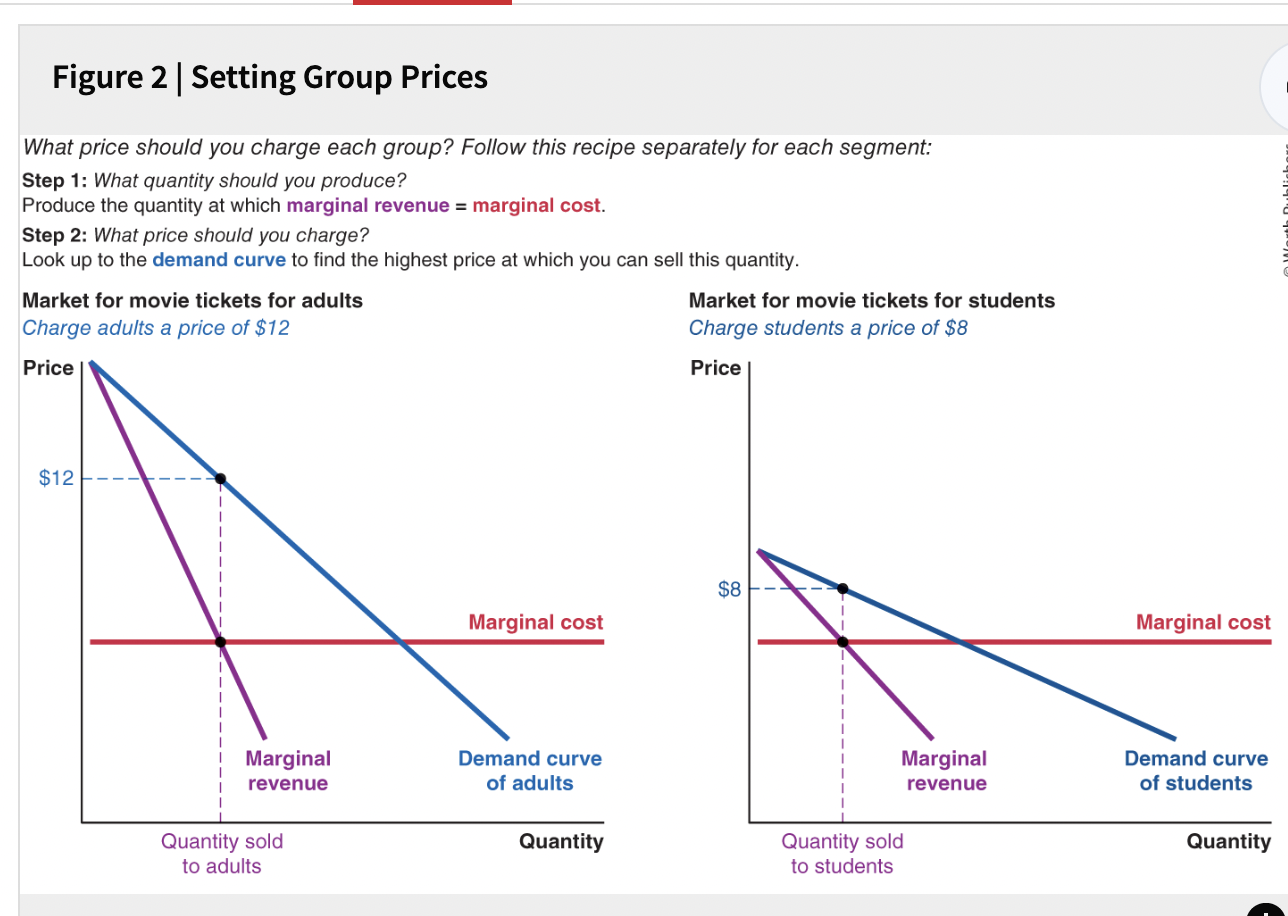

group pricing

charging different prices to different segments of people ex: student discounts

charge a higher price to groups that value your product more

charge a lower price to groups that are price sensitive

segmenting your market

segment your market into groups whose demand differs

target your group discounts based on verifiable characteristics

base group discounts on difficult to change characteristics

hurdle method

offer lower prices only to those buyers who are willing to overcome some obstacle. Induces customers to sort themselves into groups

hurdles

timing, fluctuating prices, haggling and coupons are this

quantity discount

the per unit price is lower when you buy a larger quantity

bundling

selling different goods together as a package also a hurdle

setting group prices

.

types of barriers to entry

government franchising, regulations, licensing

patents

economies of scale or other cost advantages

ownership of a scarce factor of production

network effects and switching costs

game theory

the science of making good decisions in situations involving strategic interactions

strategic interactions

when your best choice may depend on what others choose, and their best choice may depend on what you choose, comes from interdependence principle

thinking strategically

consider all possible outcomes

consider whatifs separately

evaluate your best response

put yourself in someone else’s shoes

best response

the choice that yields the highest payoff given the other players choice

nash equilibrium

occurs when you both choose your best response

correct expectations

each player’ expectation about what the other player chooses is correct

multiple equilibria

when there is more than one equilbrium

coordination game

both of the players are better off if they coordinate their choices

anticoordination game

when your best choice is to take a different action to the other player

solving coordination problems

communication

focal points,culture, and norms

laws and regulations

focal points

a cue from an outside game that helps you coordinate a specific equilibrium

simultaneous games

choosing at same time, you choose without knowing the other persons choice

first mover advantage

the strategic gain from an anticipatory action that can force a rival to respond less aggressively, occurs when you commit to being aggressive

second mover advantage

about the benefits of flexibility, the strategic advantage that can follow from an action that adapts to your rivals choice

collusion

an agreement by rivals to limit competition with each other

one shot game

strategic interaction that occurs only once

repeated game

when you face the same strategic interaction with the same rivals and the same payoffs in successive periods

finitely repeated game

when you face the same strategic interaction a fixed number of times indefinitely

repeated game

when you face the same strategic interaction an unknown number of times

grimm trigger strategy

if the other players have cooperated in all previous rounds, you will also cooperate. If any player has defected in the past you will defect

statutory burden

the burden of being assigned by the government the responsibility of sending a tax payment

economic burden

the burden created by the change in after tax price faced by buyers and sellers as a result of the tax. It doesn’t matter who the tax is levied on it has the same effect.