Honors Econ Unit 2 Test

1/45

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

46 Terms

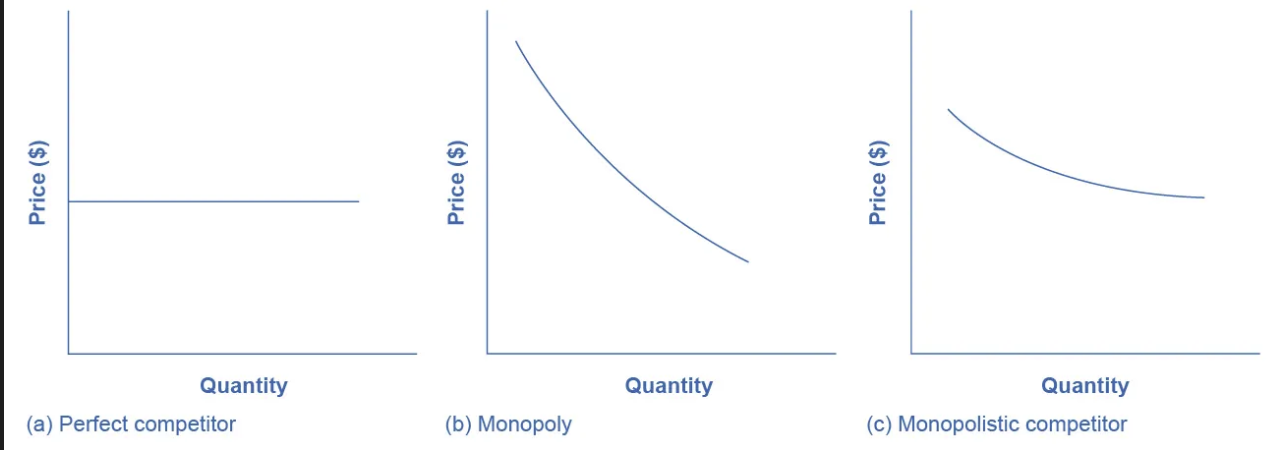

Perfect Competition Pricing (Graphing)

Perfect Competitor (Graphing)

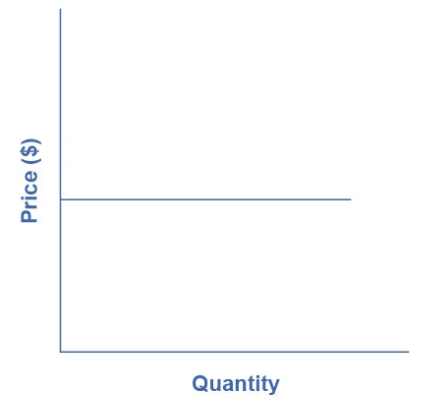

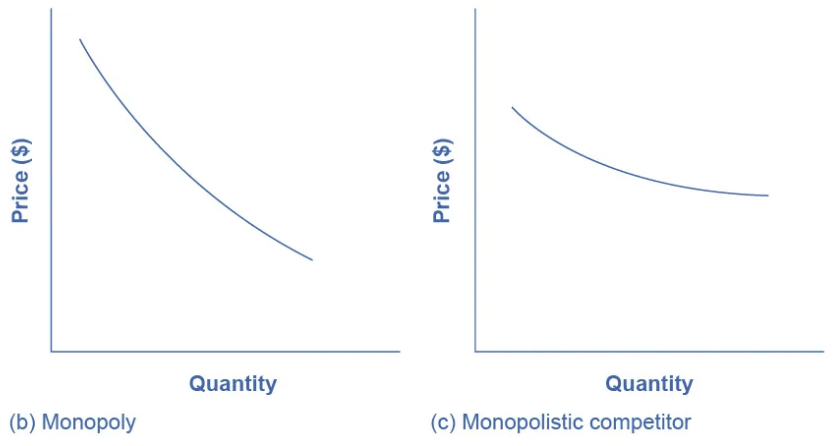

Monopoly Graph (Graphing)

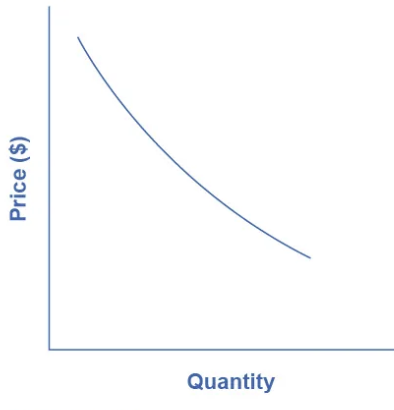

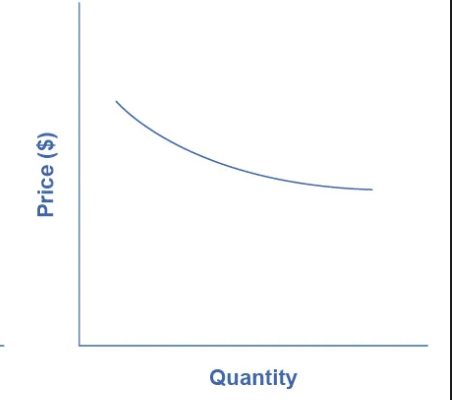

Monopolistic Competitor Graph (Graphing)

Difference between Monopoly and Monopolistic Competitor graphs

A monopoly graph is just a normal demand curve whereas a monopolistic competitor graph shows that businesses can change a price only so far before people see it as too cheap or too expensive and don’t want it.

Example:

Rolex; if their watches are too low, people see it as cheap and don't want it; conversely if it is too high then people switch to competitors

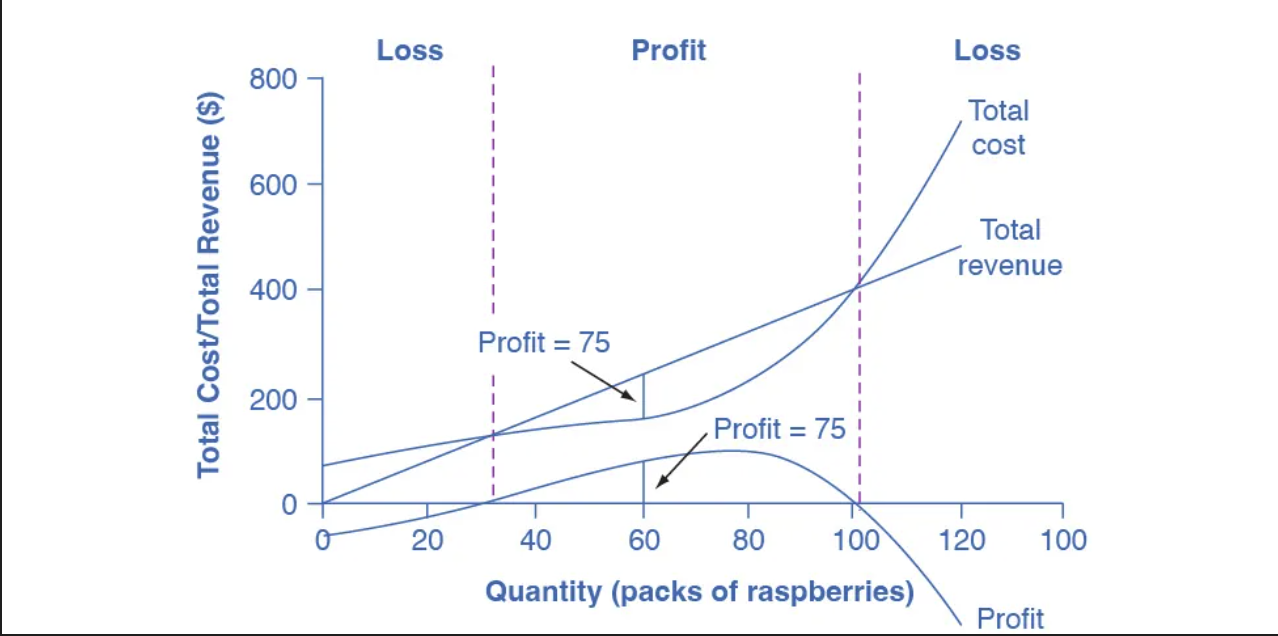

Profit Maximization in Perfect Competition (Graphing)

Monopolistic Pricing (Graphing)

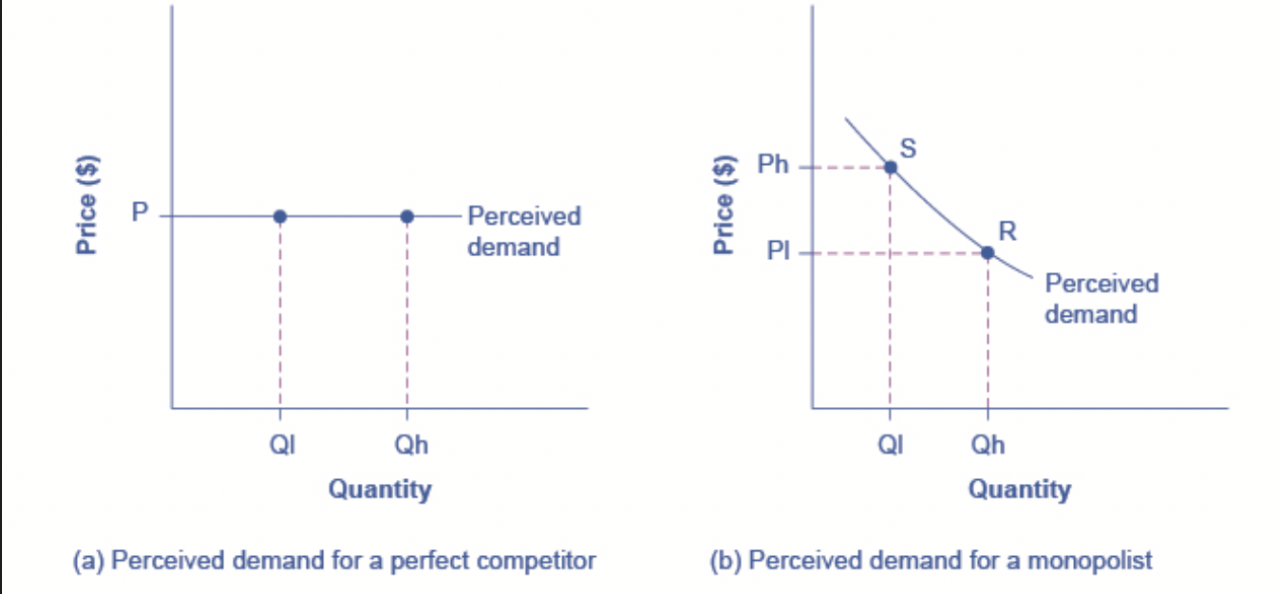

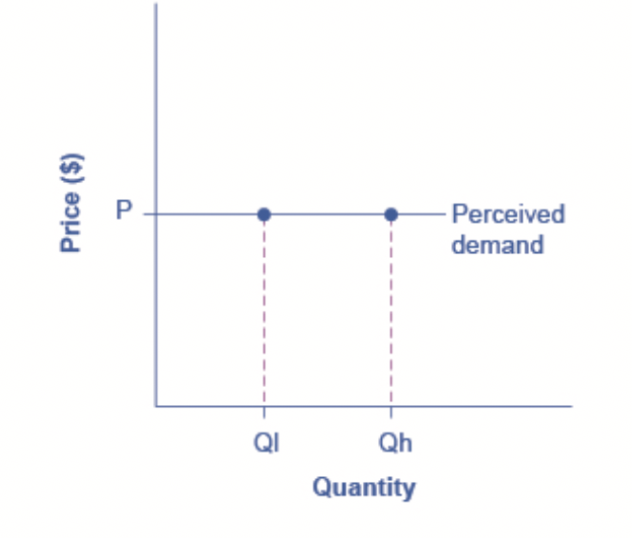

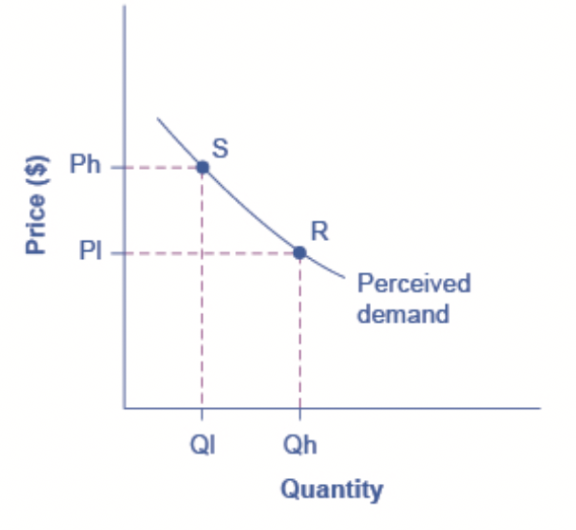

Perceived Demand for a Perfect Competitor (Graphing)

Perceived Demand for a Monopolist (Graphing)

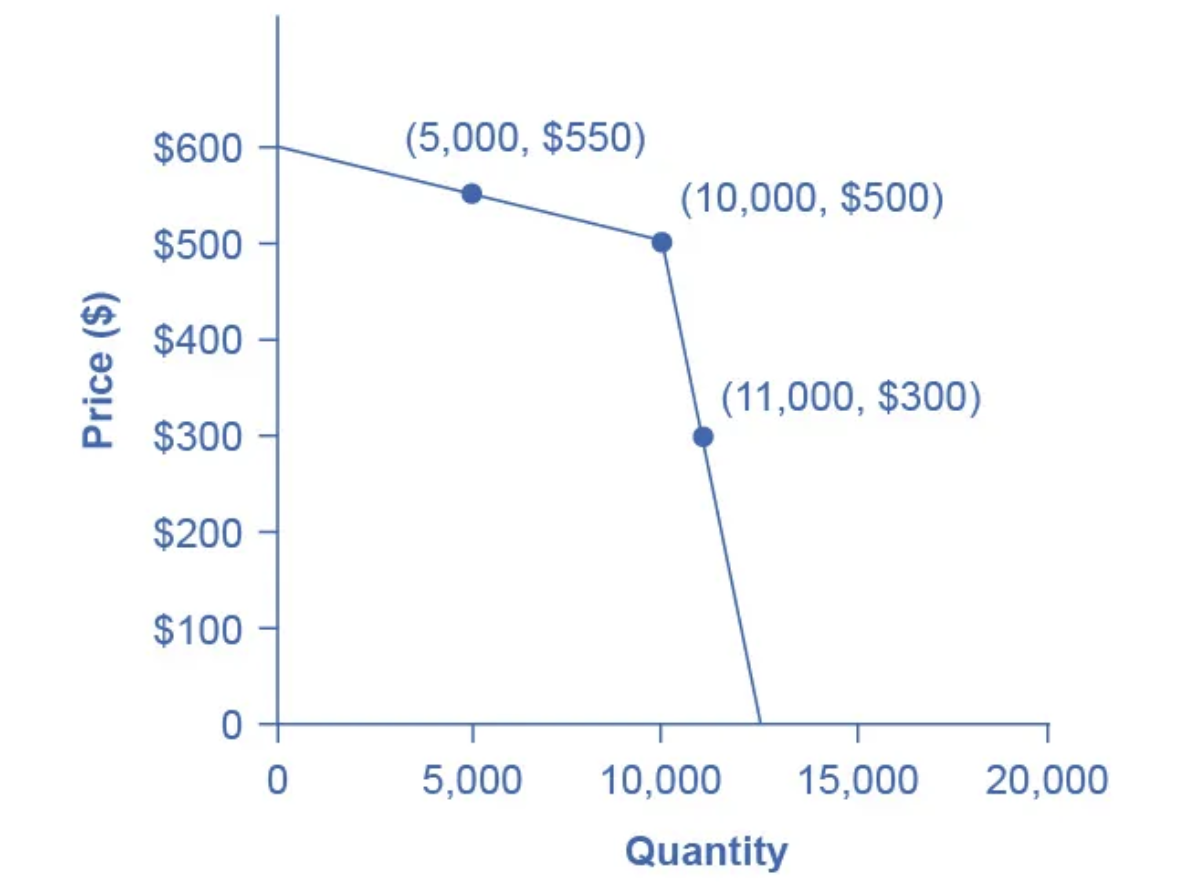

The “Kinked” Demand Curve (Graphing)

A firm finds that when it charges $600, no units are sold, but as the price falls to $550, quantity demanded increases to 5,000 units and to 10,000 units at $500; however, if the price drops further to $300, quantity jumps to 11,000 units, and at a price of $0, quantity demanded reaches about 12,000 units.

For what type of imperfect competition is a kinked demand curve used to graph?

Oligopolies

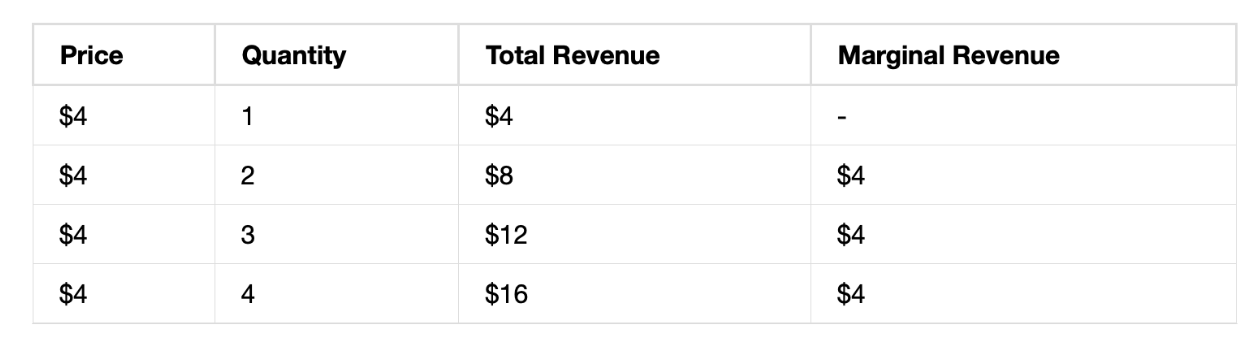

Scheduling Marginal Revenue in Perfect Competition (Graphing)

Formula for Marginal Revenue (Graphing)

marginal revenue = (change in total revenue/change in quantity)

Perfect Competition (FIB)

A theoretical model that shows competition that is completely perfect.

What is the purpose of the perfect competition model?

To find imperfections within our markets

Price Taker

A perfectly competitive firm that must accept the market price for its products because if it raises its price, customers leave, and if it lowers its price, competitors follow, so it cannot benefit from changing its price.

Hallmarks of perfect competition (List)

Many firms produce identical products.

Many buyers are available to buy the product.

Sellers and buyers have all relevant information to make rational decisions about the product.

Firms can enter or leave the market without any restrictions.

Perfect knowledge by all buyers and all sellers of all conditions in the market.

Perfect mobility of resources.

Types of Monopolies (List)

Natural Monopoly

Geographical Monopoly

Technological Monopoly

Government Monopoly

Resource Monopoly

Why is a natural monopoly allowed?

If we had competing utility companies we would have a sink faucet or light switch for each company out there, which is inefficient because it looks terrible.

Natural Monopoly

A monopoly that is allowed so that a single firm can produce the product more cheaply than any number of competing firms due to convenience.

Example is public utility like Florida Power and Light.

Geographical Monopoly

A monopoly based on the absence of other sellers in a certain geographic area.

Example, the only gas station at an interstate.

Technological Monopoly

A monopoly based on ownership or control of a manufacturing method, process, or scientific method.

Example is something under a patent.

Government Monopoly

A monopoly owned and operated by the government.

Example is when a state controls the sale of alcoholic beverages.

Resource Monopoly

A monopoly that occurs when a single firm controls a single resource needed to produce a good, preventing other firms from competing.

Example: De Beers is almost a monopoly because it controls most of the world’s diamond mining and distribution. Diamonds themselves are not rare, they are just expensive because of a manufactured scarcity produced by DeBeers.

Regulation

Used to control market behaviors to protect consumers and producers.

Ex: Food labels

Deregulation

When a government limits its restrictions on who can and cannot enter a market to encourage competition.

Ex: airlines

Examples for “Regulation and Deregulation” ***

Ex: AT&T controlled almost all phone services, so there was little need for improvement or innovation.

Later, the government broke up AT&T into smaller companies to allow competition in phone services.

Prices decreased, more services became available, and new features like caller ID, voicemail, and cell phones were introduced.

Ex: Pan Am, who was the only airline company allowed to make transatlantic flights, was regulated.

Later, it was deregulated to allow other airline companies to compete with Pan Am by allowing them to make transatlantic flights.

Pan Am collapsed because the other companies could only make regional flights and Pan Am only made transatlantic flights, so the regional companies who started making transatlantic flights surpassed and dominated Pan Am.

Trademarks

An identifying name, symbol, or logo that distinguishes a particular good and is owned by a firm.

Patent

Allows a inventor to be given exclusive legal rights to make, use, or sell a specific product, creating a temporary monopoly on the idea.

Copyright

A form of protection for original works of authorship including literary, dramatic, musical, architectural, cartographic, pictorial, sculptural, etc.

Innovation

Putting advances in knowledge to use in a new product or service

IPs and Innovation

Because of patents and trademarks creating temporary monopolies, people have to make something new, and make it better if they want to make money, leading to innovation. People need to make something better to compete and in order to make something better they need to spend resources and money, which leads to economic activity because people are always trying to innovate.

Allocative Efficiency

An economic concept regarding efficiency at the social or societal level. In other words, producing the optimal quantity of some output.

Why are monopolies not allocatively efficient? (AE & Inefficiency)

Monopolies generally get criticized for charging too high a price, which is fair. However, economists object to the fact that monopolies do not supply enough output to be allocatively efficient, meaning all monopolies are inefficient. Consumers will suffer from a monopoly because it will sell a lower quantity at a higher price than would have been the case in a competitive market.

Monopolistic Competition

A form of imperfect competition, where many firms are competing to sell similar but differentiated products. Products like these include designer clothes, gourmet, foods, cosmetics, and shoes.

Monopolistic Competitor

Someone who is doing well in a market or a geographic location will inspire and draw competition. This has all the features of perfect competition except for identical products.

Firm Differentiation

In order to stand out, firms will associate with a certain lifestyle or way of life: rich or for the poor, outdoor or modern.

Firms will advertise, do giveaways or other things to make their product seem unique.

Ex: Apple makes its products seem different by focusing on design, simplicity, and status, even though other phones have similar features.

Lifestyle

Big companies advertise a desired lifestyle and connect their product to it so people want to be part of that life.

This is a method used to make their product seem like the best option.

Ex: Nike connects its products to an athletic and successful lifestyle.

Advertising

Explaining how the products of one firm are differentiated from that of another firm.

If the advertising works, this results in either higher demand for the product or causes demand for the product to become more inelastic (not very responsive to price changes)

Oligopoly

An oligopoly arises when a small number of large firms have all or most of the sales in an industry. Oligopolistic firms can either ruin other firms and compete very heavily, or combine together by colluding.

Ex: Auto industry, cable television, and commercial air travel

Collusion

When firms act together to reduce output and keep prices high.

- when you cooperate with others in an unlawful way

Oligopoly and Collusion Example ****

EX:

- Laundry Detergent in France

- Laurence, Hugues, Christian, and Pierre, just 4 guys meeting in cafes across Paris.

- These men worked for the 4 detergent companies that controlled 90% of the French market and they were colluding to align detergent prices.

- They agreed never to have sales, promotions, or BOGOs.

- They agreed to their respective market shares and essentially became price takers with artificial perfect competition and monopolized the market in France.

- This did not last though as one of the companises (Unilever - makes Persil detergent along with Axe, Dove, etc.) had a D-Day sale (prisoners' dilemma?), the others soon followed with ever more destructive sales.

- Eventually a unilever employee turned state's evidence and the firms (other than Unilever) were fined 361 million euros.

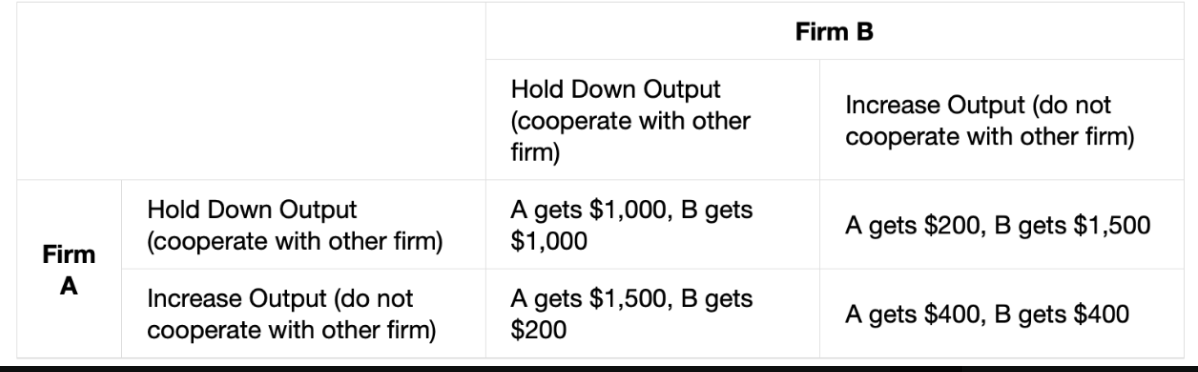

Prisoner’s Dilemma

The prisoner’s dilemma is a physiological game. A game in which the gains from cooperation are larger than the rewards from pursuing self-interest

Oligopoly Version of Prisoner’s Dilemma

In an oligopoly, firms face a problem like the prisoner’s dilemma. If they all cooperate and produce less, they can keep prices high and make more profit.

But each firm has an incentive to cheat by producing more to make even more money.

Because every firm thinks this way, they all end up producing more, prices drop, and they all make less profit than if they had cooperated.

OPEC

Perhaps the easiest approach for colluding oligopolists would be to sign a contract with each other that they will hold output low and keep prices high. If a group of U.S. companies signed such a contract, however, it would be illegal.

Certain international organizations, like the nations that are members of the Organization of Petroleum Exporting Countries (OPEC), have signed international agreements to act like a monopoly, hold down output, and keep prices high so that all of the countries can make high profits from oil exports.

Such agreements fall in a gray area of international law and are not legally enforceable.

If Nigeria, decides to start cutting prices and selling more oil, Saudi Arabia cannot sue Nigeria in court and force it to stop.

Because oligopolists cannot sign a legally enforceable contract to act like a monopoly, the firms may instead keep close tabs on what other firms are producing and charging.

Cartel

A group of firms that collude to produce the monopoly output and sell at the monopoly price. In OPEC’s case, they control the output of oil and in turn keep the prices high.