Intro to Economics (non micro/macro specific)

1/83

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

84 Terms

economics

Social Science concerned with the efficient usage of scare resources to achieve economics wants

Categories of Economic resources

Land, Labor, Capital, Entrepreneurial

Land

natural resource involved in production

Labor

Human effort involved in production

Capital

Man made object involved in production

entrepreneurial ability

innovative process of creation and risk taking

Scarcity & Choice

Resources are limited forcing individuals and firms to make choices

Utility

humans act in order to maximize satisfaction

self interest

assumption that individuals act to maximize their personal benefit

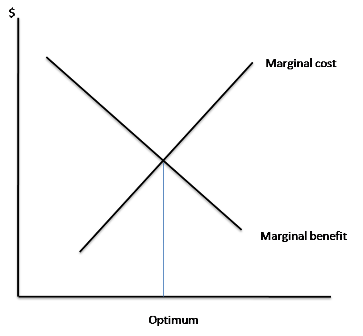

Marginal analysis

Marginal cost vs marginal benefit

Other things equal assumption (Ceteris paribus)

assumption that non focus factors remain constant

Microecnomics

Concerned with decision making of individuals, households, and firms

Macroecnomics

Examines the economy as a whole and aggregate variables.

Positive economics

Focused on facts and cause and effect relationships, establishes scientific statements

Normative economics

Incorporates value judgements about what economy should be like

Economizing Problem

The need to make choices, as wants exceed economics means

Budget Line

Graphical display of goods a consumer is able to purchase with a specific income

Production possibility curve

Combination of goods and services that can be produced with a given set of resources

Optimal allocation

MB=MC

opportunity cost

the cost of forgoing a choice

Law of increasing opportunity cost

as more of one good is produced less of another can be produced.

Laissez-Fare capitalism

very limited government role

Command system

Government owns most resources. economic decision making set by central planning

The market system

Used by vast majority of world’s economy. Private ownership of resources. mixture of centralized and decentralized action.

Private property

ownership of private property plays a large role in market system. includes the right to negotiate contracts and use resources as seen fit.

Freedom of enterprise

Firms are free to use resources to produce their choice of goods in their chosen market.

Competition

2 or more buyers or sellers acting in a market with freedom to enter and exit market.

specialization

devoting resources to produce one or few goods to increase efficiency

division of labor

divide labor force to specialize and maximize outputs

Geographic specialization

production that optimally aligns with local geographic factors

5 fundamental questions

-What will be produces

-how will it be produced

-who will receive the output

-how will the system change

-how will the system promote technological advancement

The invisible hand

firms seeking to further their self interest in a competitive market will be guided in favor of public interest

Demise of command system

coordinating and incentive problem

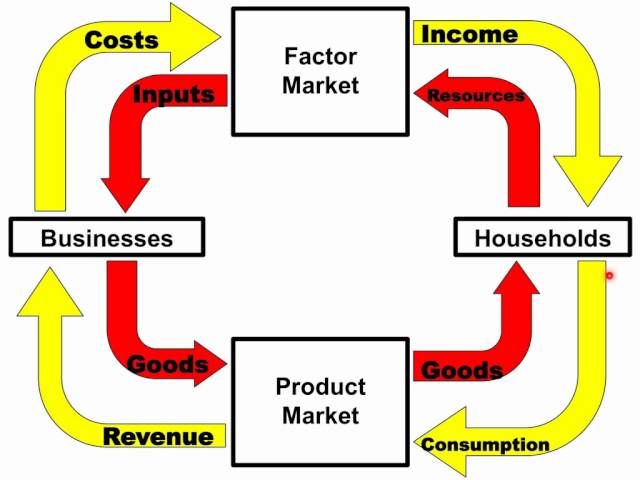

circular flow model

the dynamic market creates a continuous and repetitive flow of goods, resources, and currency.

circular flow model (image)

households

buy goods and obtain income by selling resources

businesses

sell goods and services to obtain revenue. Purchase resources to produce goods.

Product market

households purchase goods and money spent goes to businesses.

Resource market

households sell resources to businesses in order to produce goods.

Risk

the market system creates risk. owners subject to risk and are residuals claimant.

Benefits of limiting risk

-attracting inputs

-focusing attention

creative destruction

new advanced products outcompete an outdated product

Optimal output graph

Future consideration

investing in future goods allows for the PPC to shift outwards

Absolute advantage

one group is better at producing a good (faster and more)

Comparative advantage

One group is relatively better at producing a good through lower opportunity cost

Benefit of trade

Through specialization there is net increase in total goods produced by all groups.

PPF shifted outwards

technology advancements, trade, capital formation

Demand

The amount of a product consumers are willing to purchase at a given price

Law of demand

other things equal, as price falls the quantity demanded rises, and as price rises demand falls.

Demand curve

represents the inverse relation between demand and price. Negative slope.

Determinants of demand

consumer preference, number of buyers, consumer income, price of related goods, consumer expectation

Movements along demand curve

change in product price

Demand curve shifts right

more demanded at every price

Demand curve shifts left

less demanded at every price

Supply

Amount of good producers are willing to make available at a series of prices

Law of supply

Positive relation as price rises, the quantity supplied increases.

Determinants of Supply

Resource prices, technology, taxes & subsidies, price of other goods, and number of sellers in market.

Equilibrium Price/quantity

the intentions of buyers and sellers align

Characteristics of a competitive market

many buyers and sellers and standard product

Network effect

Value increases with more users

Congestion effect

values decreases with greater use

Complimentary goods

goods used together, demand increases in tandem

Inferior Goods

demand decreases and income increases

Normal goods

demand increases as income increases

Substitute goods

goods that can replace eachother

Independent goods

vast majority of goods that are unrelated

Greatest effect on quantity supplies

price of good

Market clearing price

equilibrium price where the quantity demanded equals the quantity supplied.

Productive efficiency

producing goods at the lowest possible cost

allocative efficiency

producing the right mix of goods that the market demands

rationing function

buying and selling decisions are consistent

price ceiling

maximum legal price a seller may charge for a good

law of diminishing marginal utility

as a person consumes more of a good the satisfaction (utility) decreases with each additional good

Demand Increase, Supply constant

P increase + Q increase

Demand decrease, supply constant

P decrease + Q decrease

supply increase, demand constant

P decrease + Q increase

supply decrease, demand constant

P increase + Q decrease

Demand increase + supply increase

P ? + Q increase

Demand decrease + supply decrease

P ? + Q decrease

Demand increase + supply decrease

P increase + Q ?

Demand decrease + supply increase

P decrease + Q ?

determinants of demand

(1) Price of the product, (2) Income of the buyers, (3) Prices of related goods (substitutes/complements), (4) Tastes and preferences, and (5) Consumer expectations regarding future prices.

determinants of supply

1) Input costs (resource prices), 2) Technology advancements, 3) Government actions (taxes/subsidies), 4) Number of sellers, 5) Producer expectations of future prices, and 6) Prices of related goods.