ECON2: Scarcity & Choice

1/106

Earn XP

Description and Tags

Scarcity & Choice

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

107 Terms

PPC (Production Possibilities Curve)

a model that illustrates scarcity & tradeoffs

Scarcity

When someone or something faces a constraint

Every choice has a cost =

opportunity cost

opportunity cost

What you have to give up to buy/obtain the other thing you want.

Curved PPC means

A curved PPC implies that the opportunity cost of the good on the horizontal axis is rising as more is produced

Productive efficiency means

producing to the maximum efficiency then when you want to produce more you will have to produce less of your other good

Recession

Unemployment above normal & economy not producing at its full potential

Comparative Advantage =

Low Opportunity Cost

Scarcity

High demand for a low availability good

Demand =

Consumers (buying side)

Is the demand curve slope positive or negative?

Negative

Supply =

Producers (selling side)

Is the demand curve slope positive or negative?

Positive

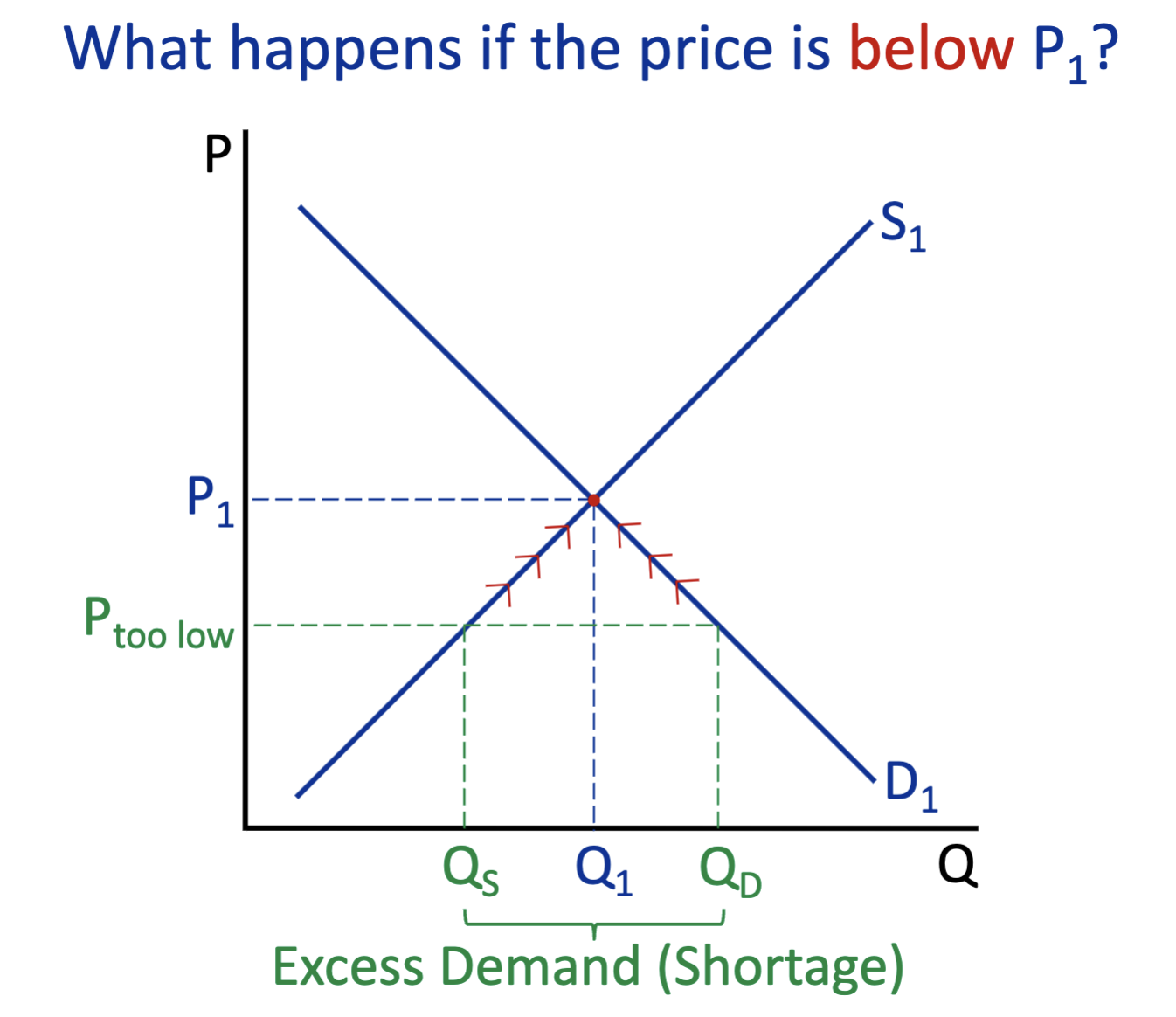

What happens below P1? (demand & supply)

Excess Demand (Shortage)

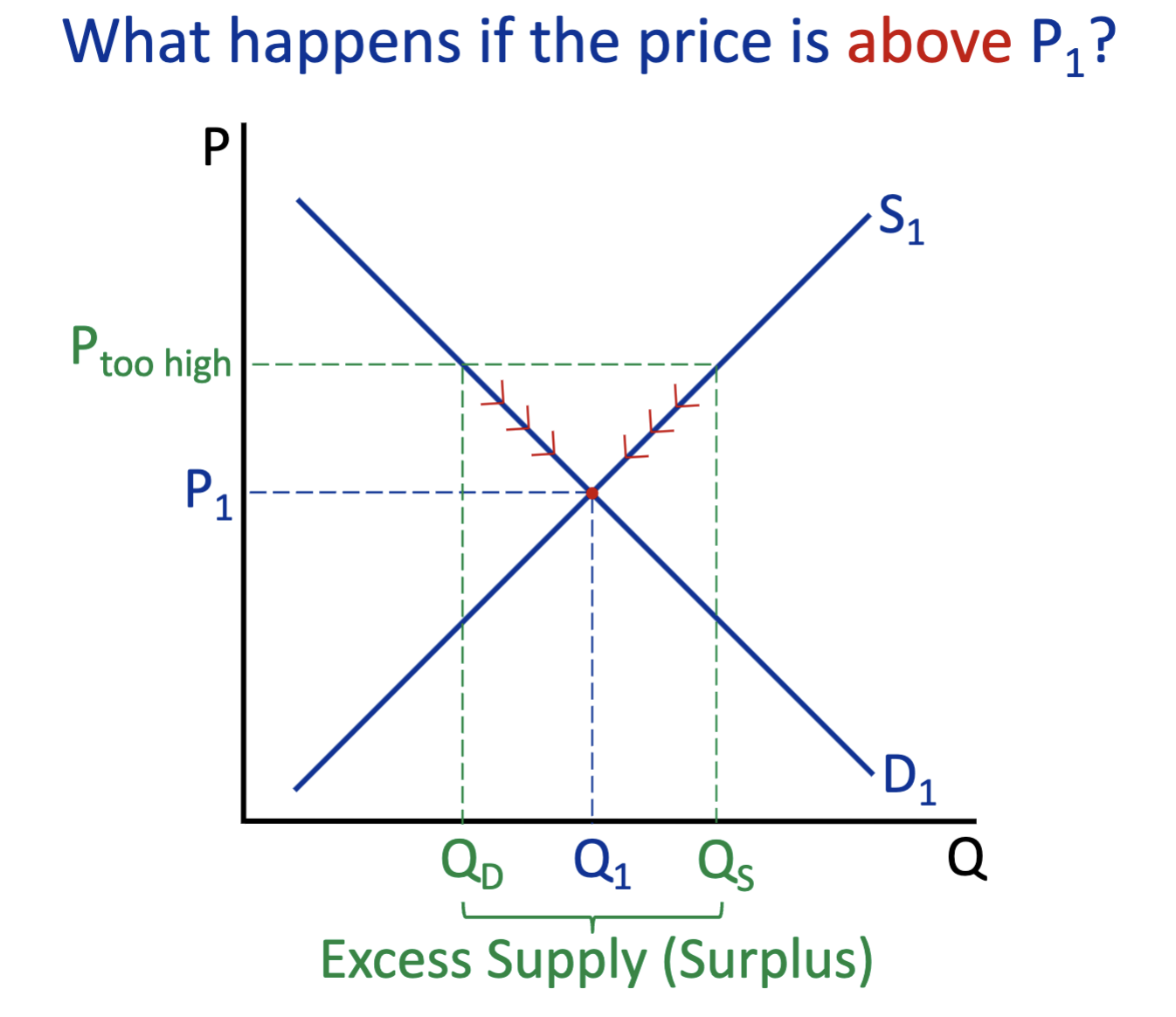

What happens above P1? (demand & supply)

Excess Supply (Surplus)

Ceteris Paribus

Everything equal but the price

Decrease costs of production, the supply curve shifts?

Shifts to the right

Innovation improvement, the supply curve shifts?

Shifts to the right

Increase in the number of producers, the supply curve shifts?

Shifts to the right

Increased cost of production, the supply curve shifts?

Shifts to the left

Natural disasters, the supply curve shifts?

Shifts to the left

Decrease in the number of producers, the supply curve shifts?

Shifts to the left

A tax, the supply curve shifts?

Shifts to the left

Change in taste, the demand curve shifts?

Shifts to the right

Increase in income, the demand curve shifts?

Shifts to the right

Increase in market population, the demand curve shifts?

Shifts to the right

Increase in price of a substitute good, the demand curve shifts?

Shifts to the right

Decrease in price of complementary, the demand curve shifts?

Shifts to the right

Change in taste, the demand curve shifts?

Shifts to the left

Decrease in income, the demand curve shifts?

Shifts to the left

Decrease in market population, the demand curve shifts?

Shifts to the left

Decrease in price of substitute good, the demand curve shifts?

Shifts to the left

Increase in price of complementary good, the demand curve shifts?

Shifts to the left

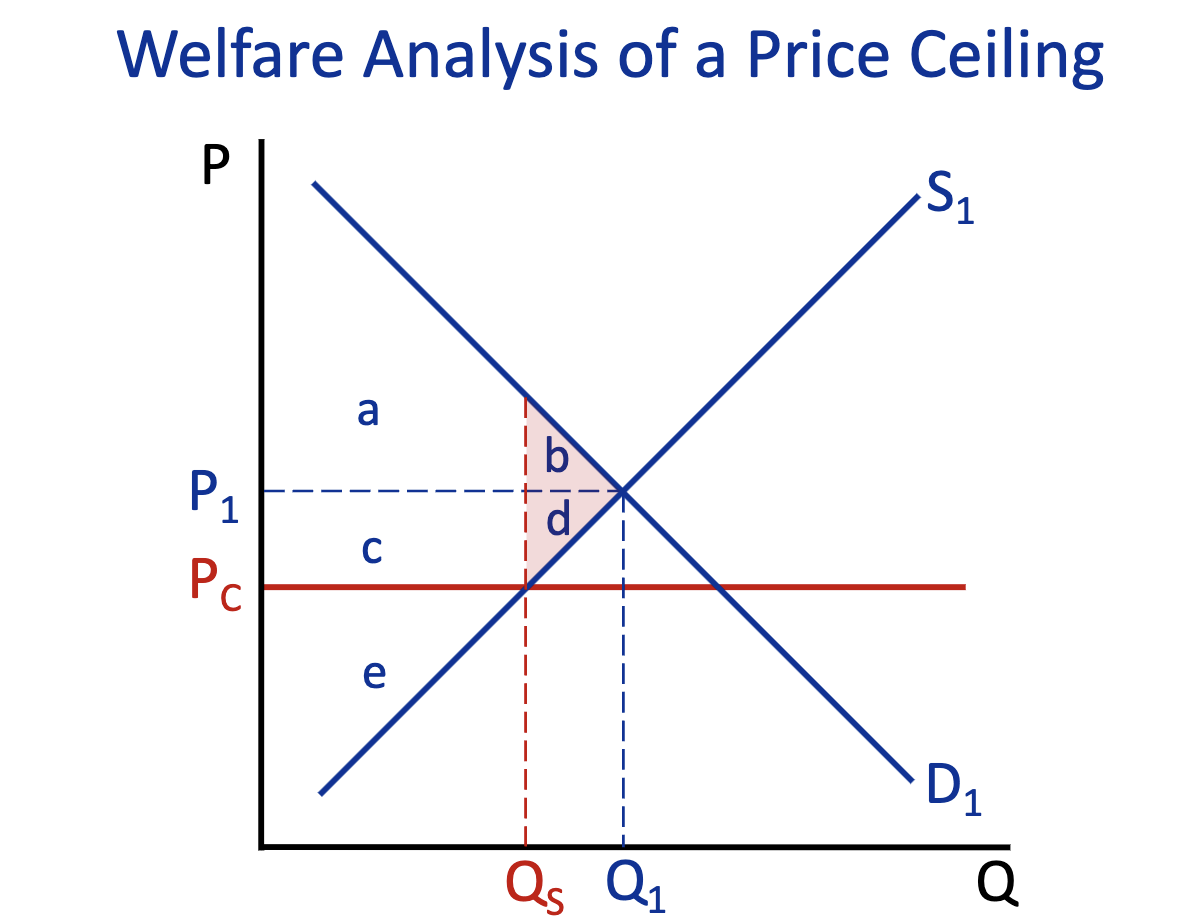

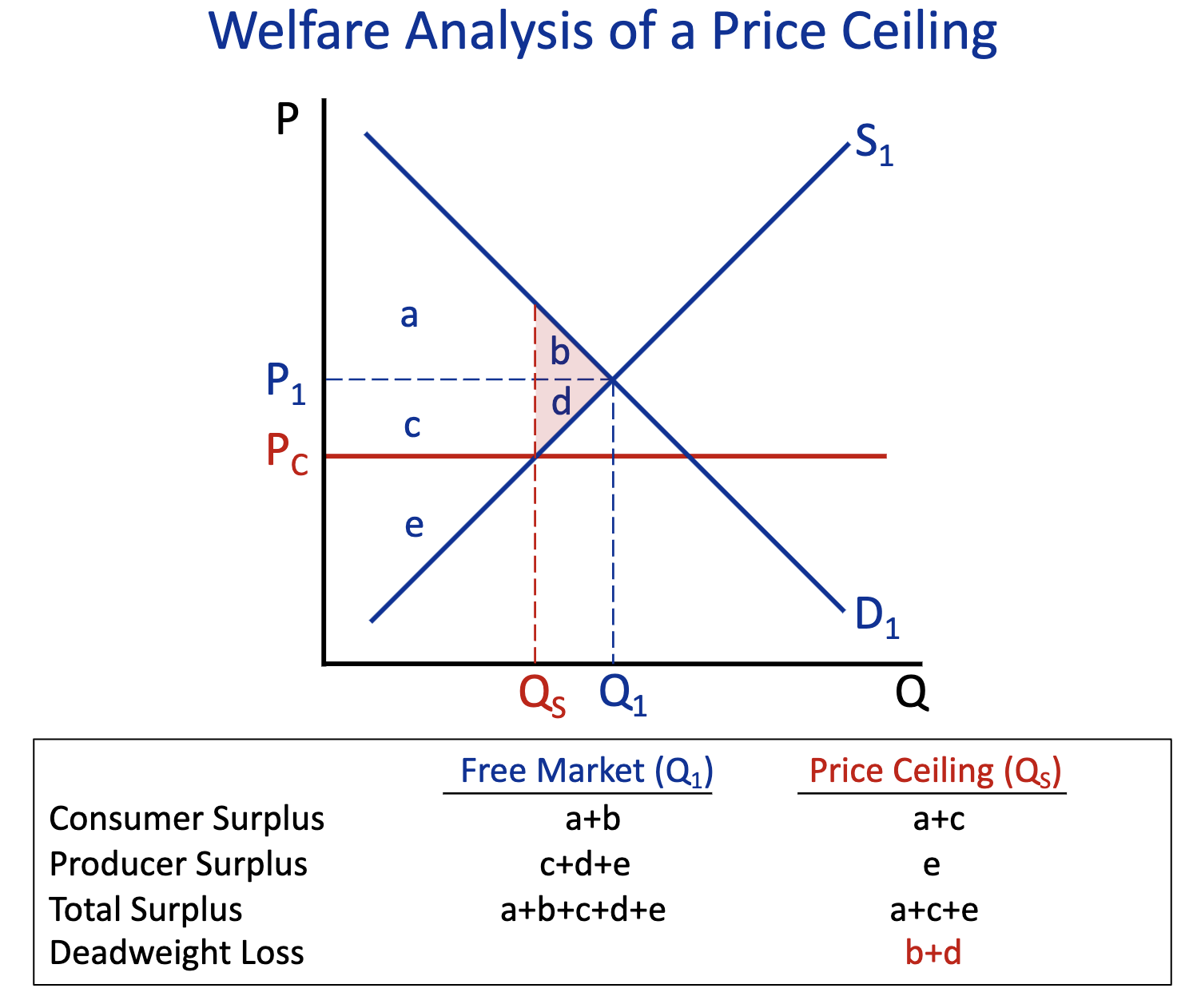

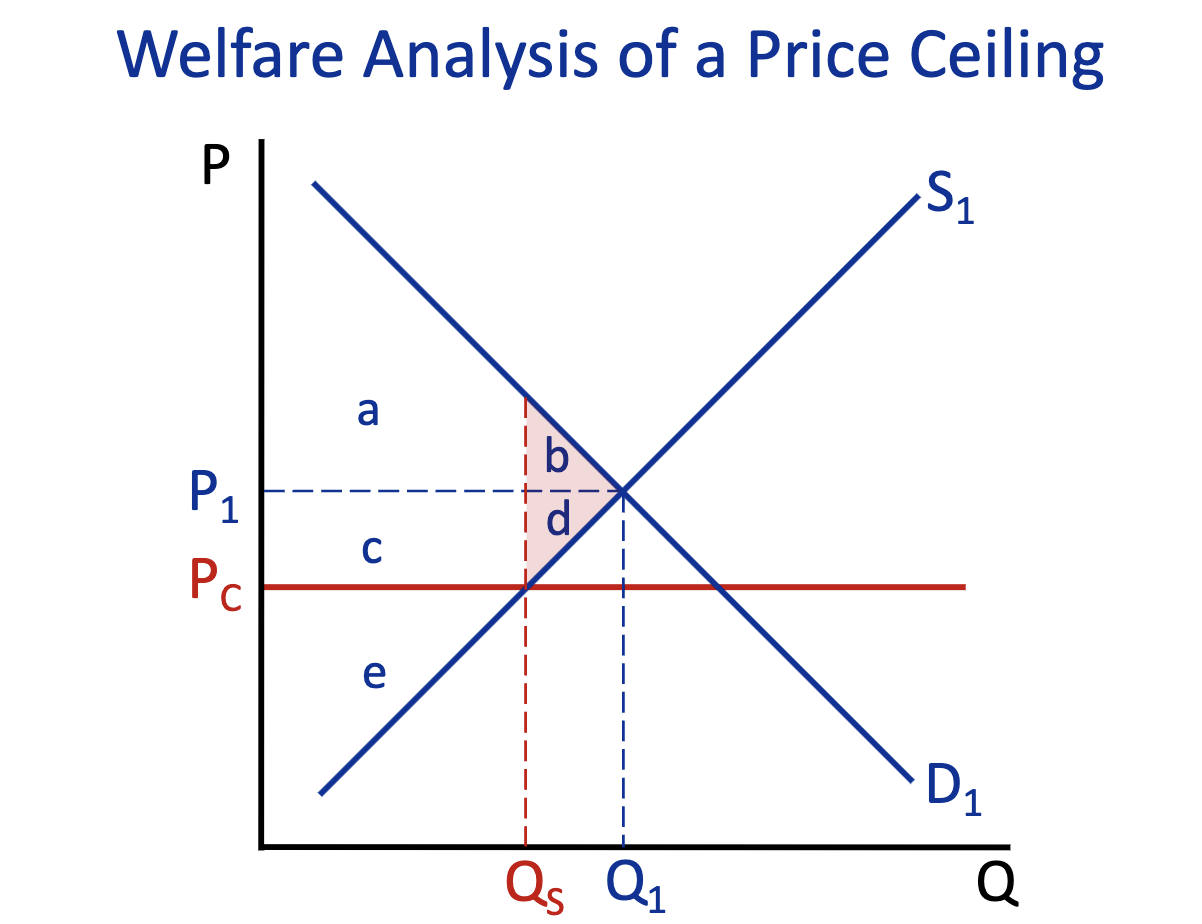

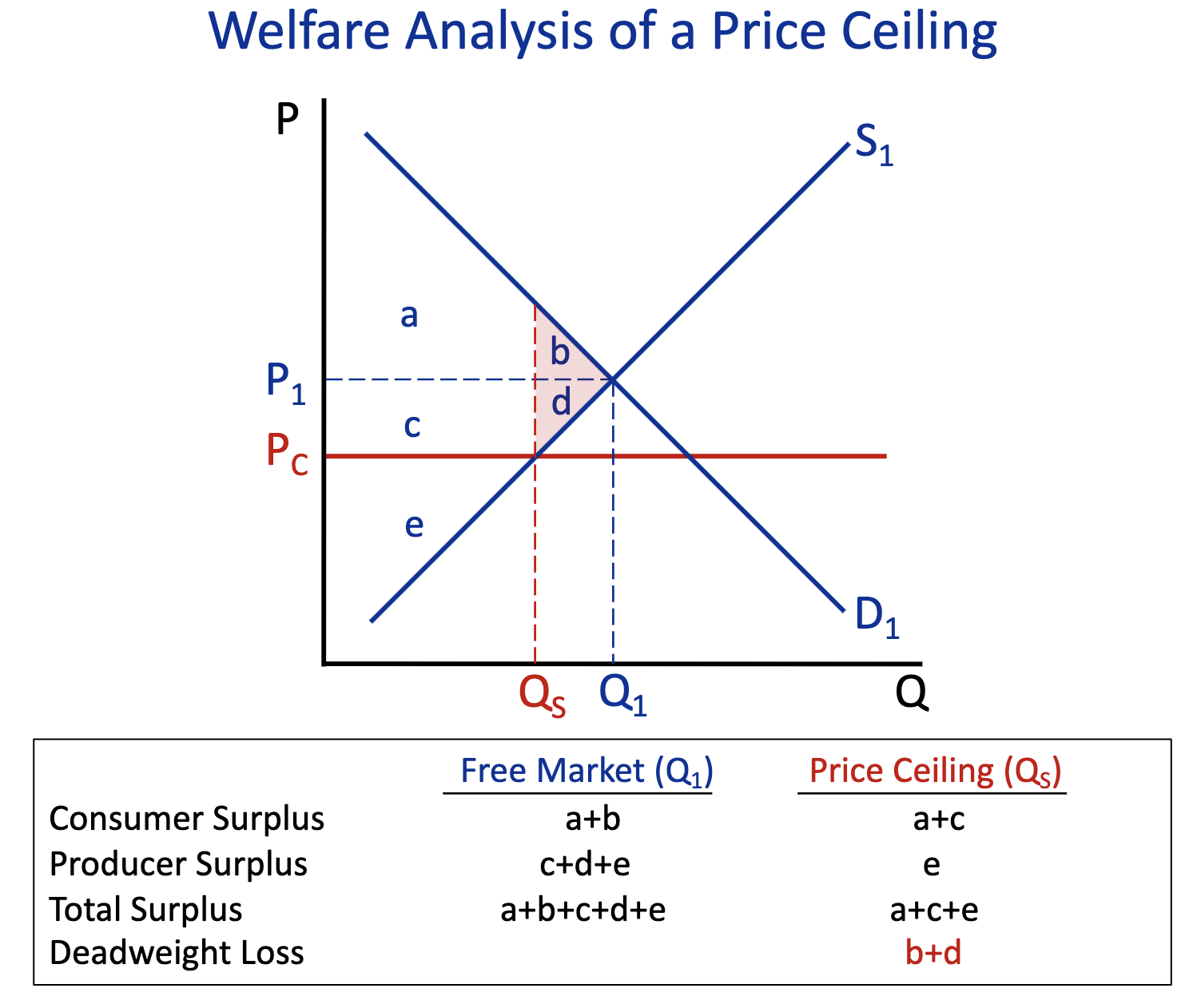

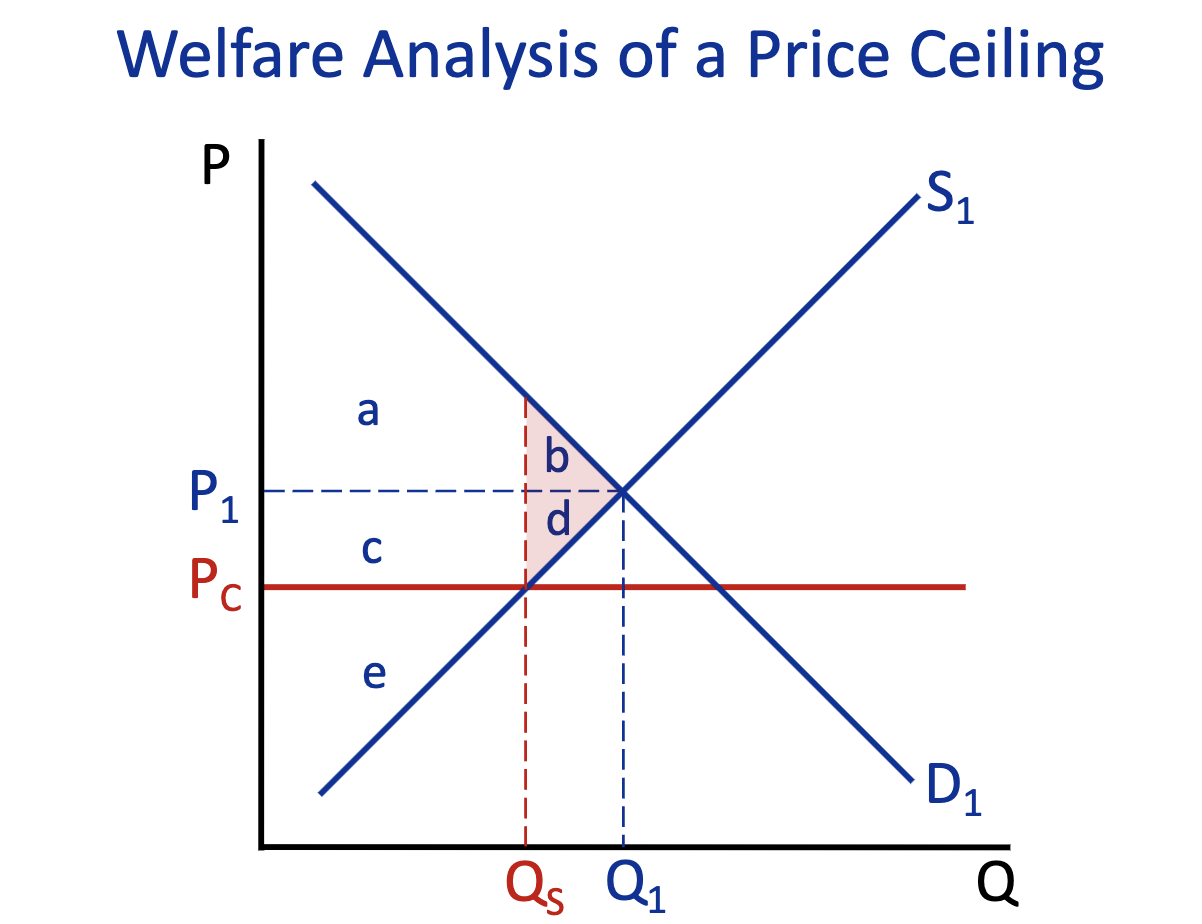

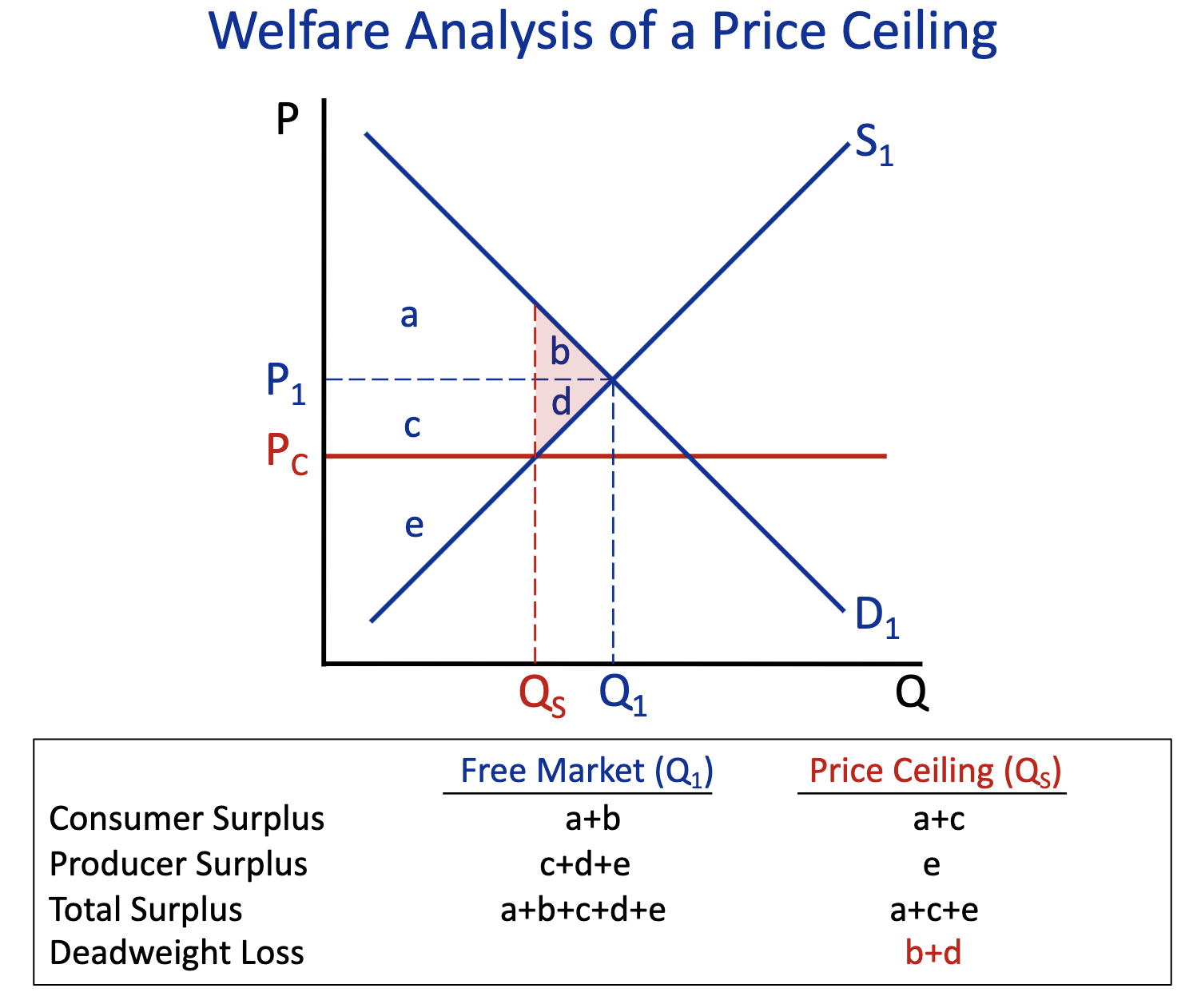

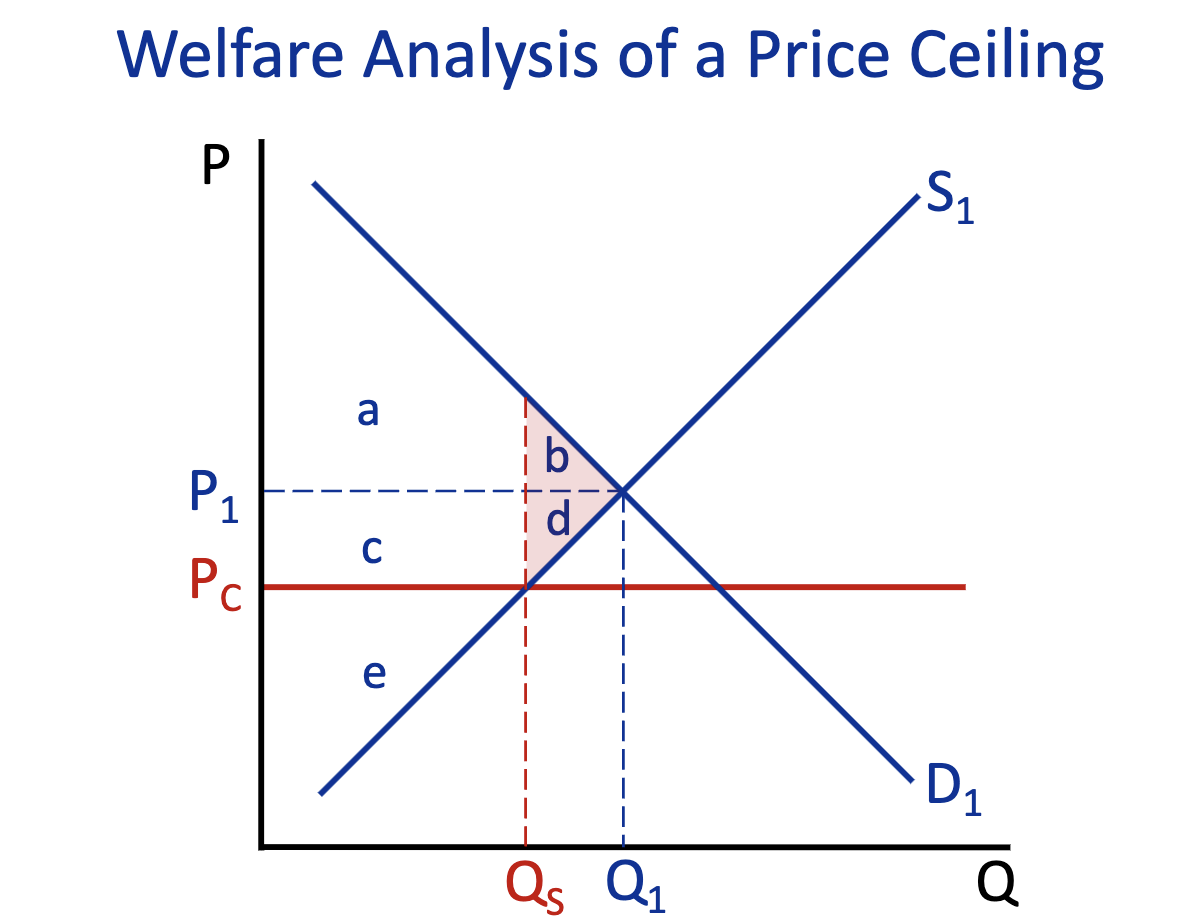

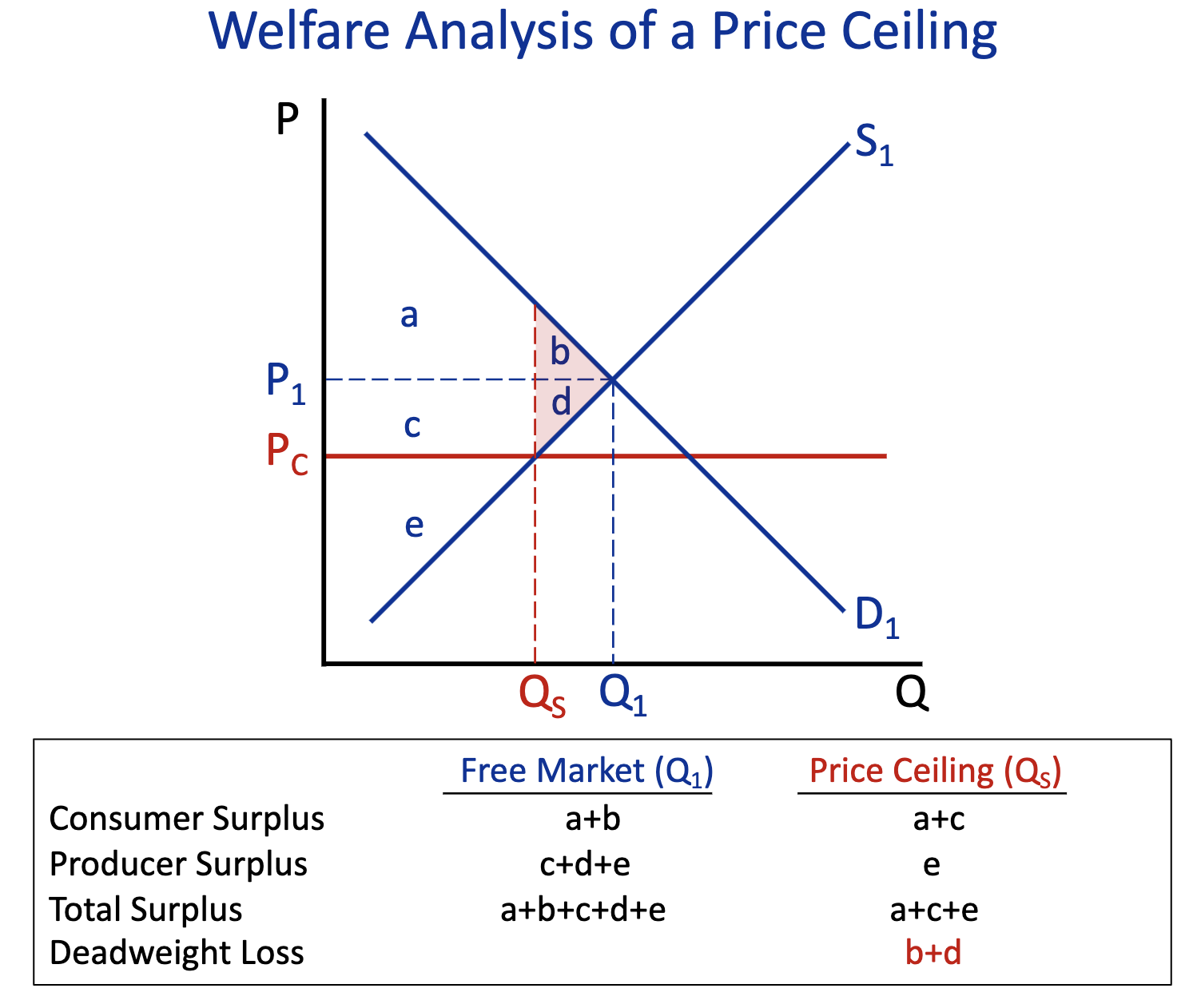

Price Ceiling

Sets the maximum amount a seller can charge for a good or service (normally a govn’t) eg: gas, medicine, and food

Price Floor

lowest legal price that can be paid in a market (min price)

Economic Surplus = the respective gains that a consumer or producer gets within an economic activity

Consumer Surplus + Producer Surplus = Total economic surplus

Marginal Benefit

max amount a consumer is willing to pay for an additional good or service

Marginal Cost

the change in total production cost that comes from making or producing one more unit.

Allocative Efficiency

ensures that resources are used so that their marginal benefit to society is equal to their marginal cost.

Consumer Surplus: Free Market (Q1) & Price Ceiling (Q2)

Free Market (Q1) : a+b

Price Ceiling (Q2) : a+c

Producer Surplus: Free Market (Q1) & Price Ceiling (Q2)

Free Market (Q1) : c+d+e

Price Ceiling (Q2) : e

Total Surplus: Free Market (Q1) & Price Ceiling (Q2)

Free Market (Q1) : a+b+d+c+e

Price Ceiling (Q2) : a+c+e

Deadweight Loss: Free Market (Q1) & Price Ceiling (Q2)

Free Market (Q1) :

Price Ceiling (Q2) : b+d

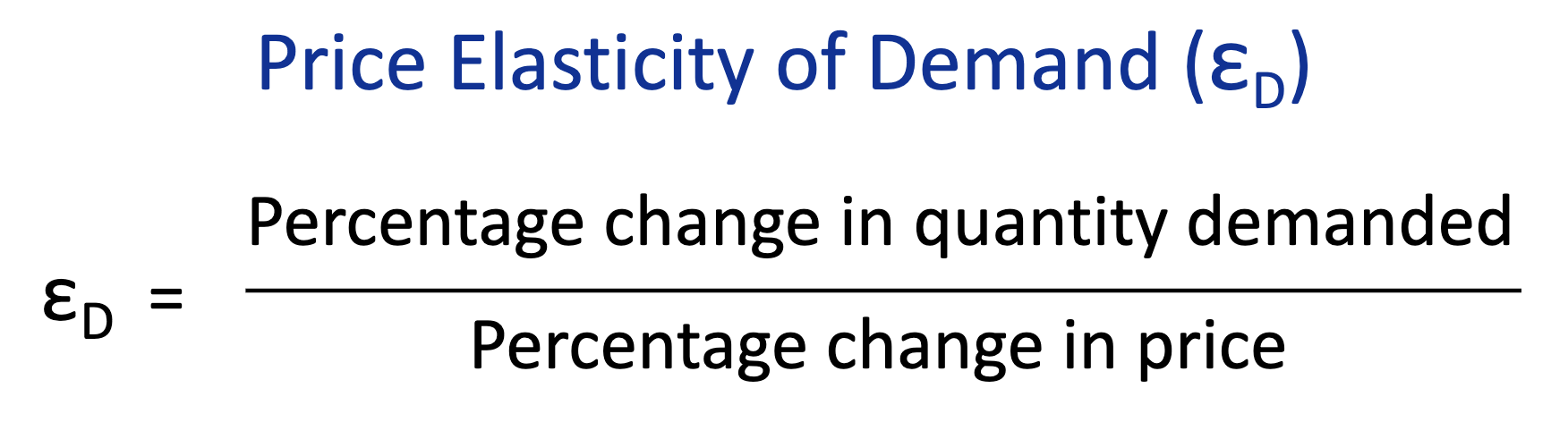

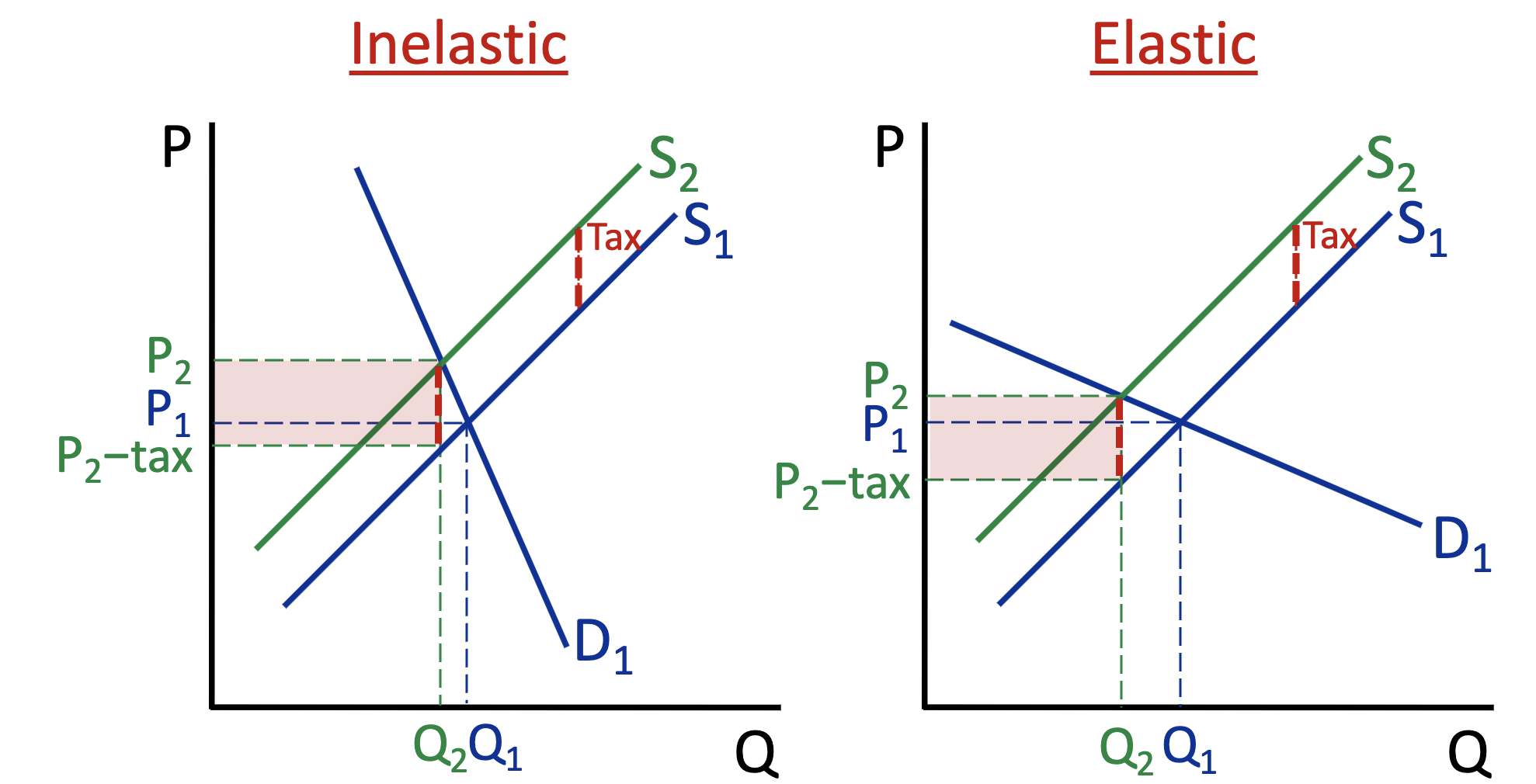

What is the equation for elasticity? (Demand & Supply)

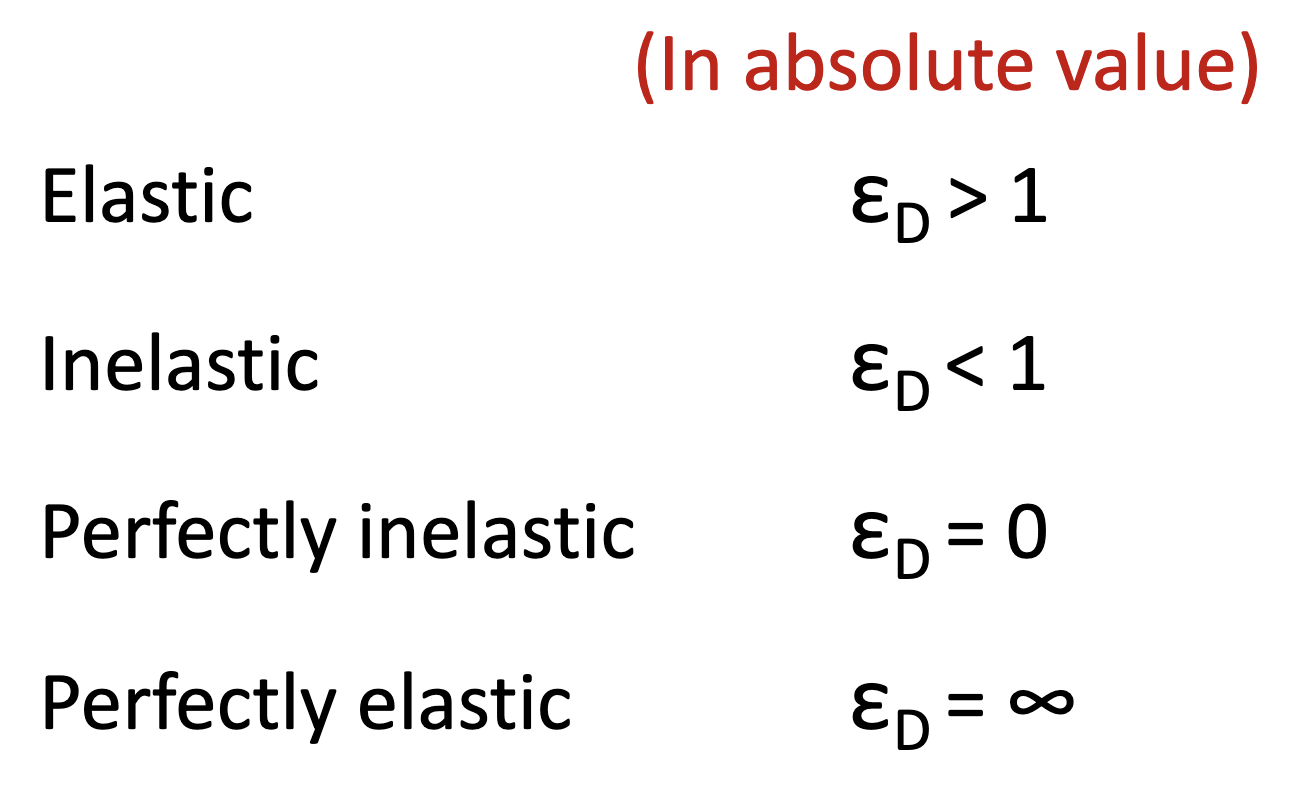

Elasticity? Inelasticity? Perfectly Elasticity? Perfectly Inelasticity? (Demand & Supply)

When demand is inelastic?

When there is no close substitute good & consumers need this good.

When supply is inelastic?

When there is a resource constraint (short-run)

When demand is elastic?

When there is a close substitute or when consumers do not need this good

When supply is elastic?

When there are no hard resource constraint (long-run)

Total Expenditure means

what consumers spend on a product at a given price.

What is the total expenditure equation?

Price * Quantity = Total Expenditure

Inelastic or elastic if the total expenditure rises when the supply curve shifts back?

Inelastic

Inelastic or elastic if the total expenditure falls when the supply curve shifts back?

Elastic

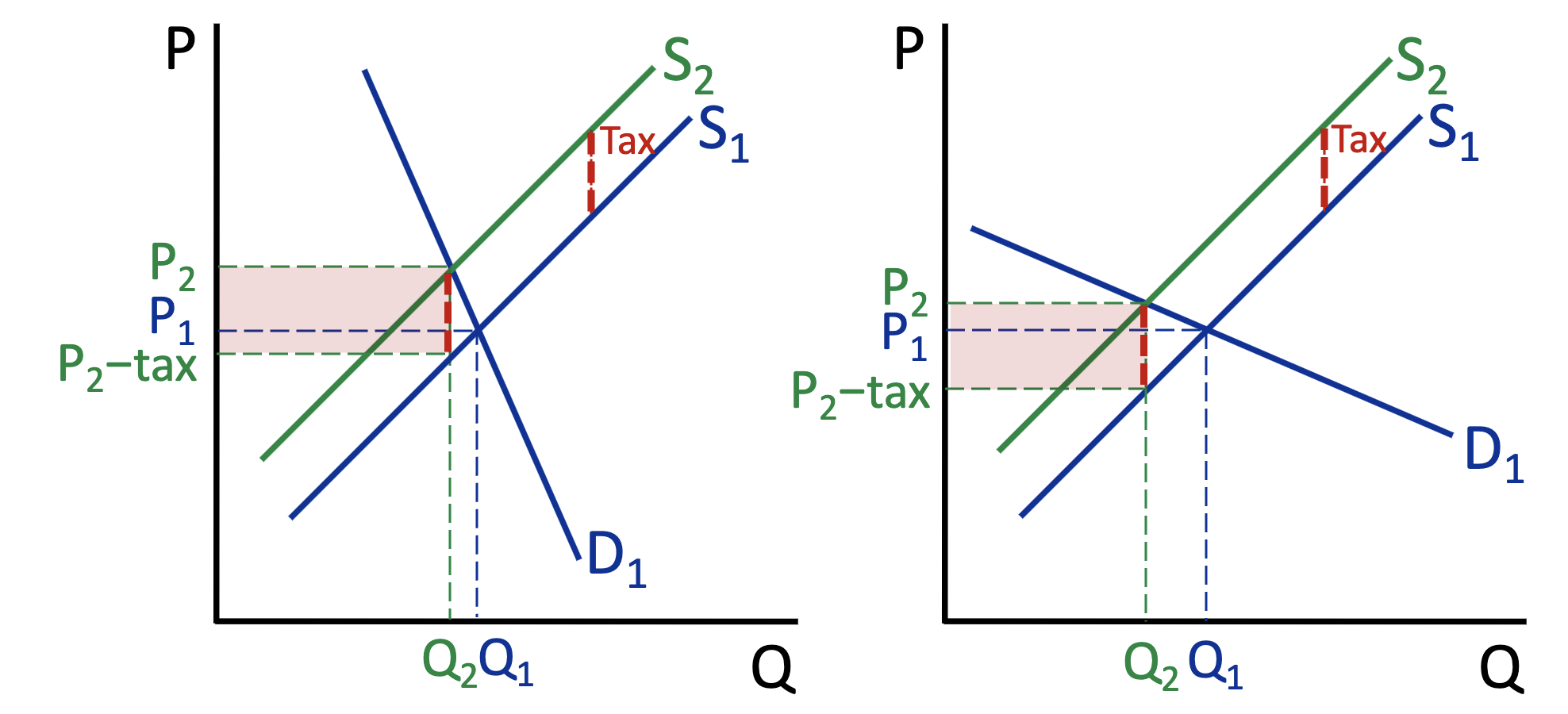

What happens to the supply curve when tax is raised higher?

the supply curve shifts up/left

Which one is inelastic and elastic?

Do inelastic factors bear or avoid the tax?

bear

Do elastic factors bear or avoid the tax?

avoid

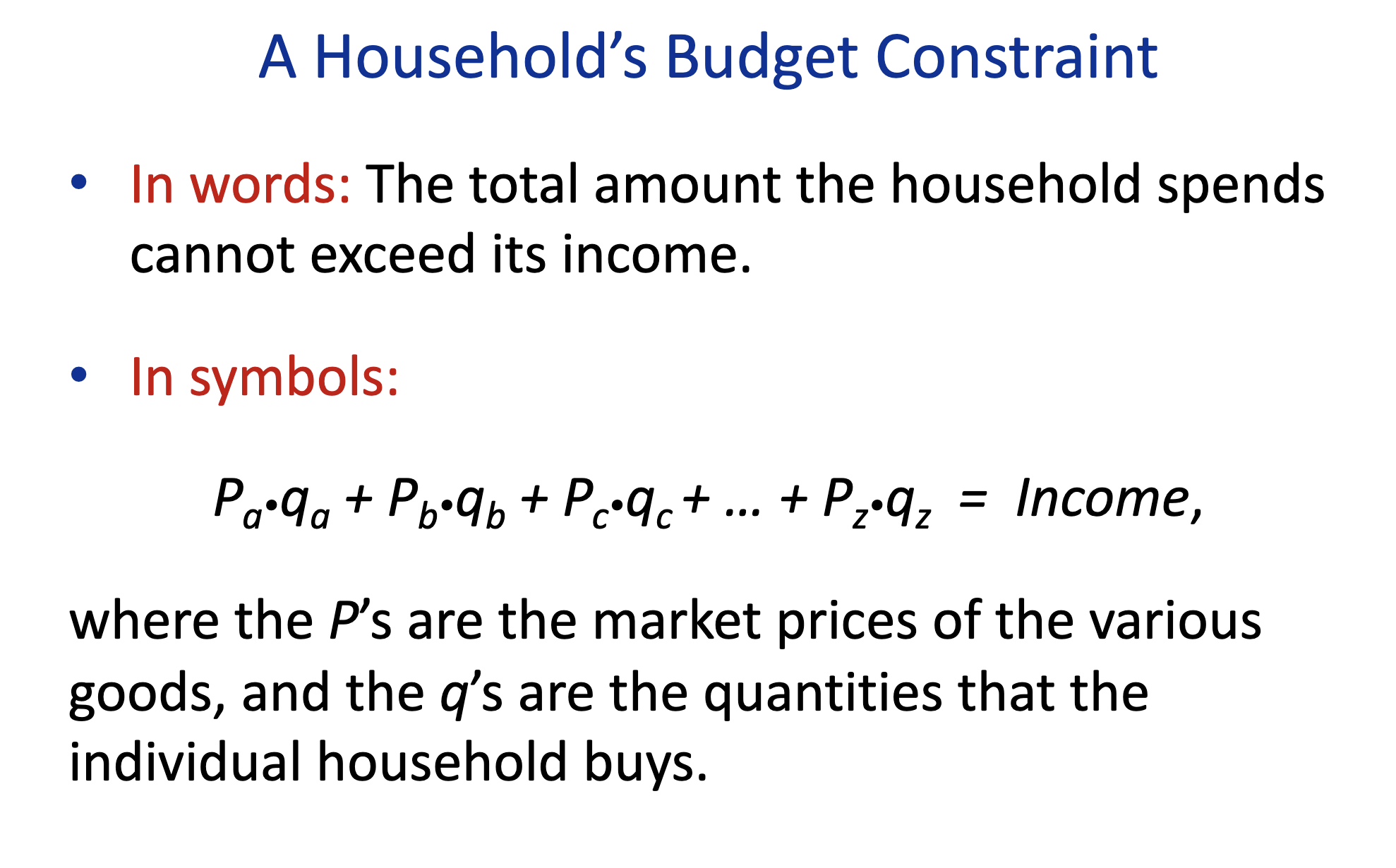

A household budget constraint equation:

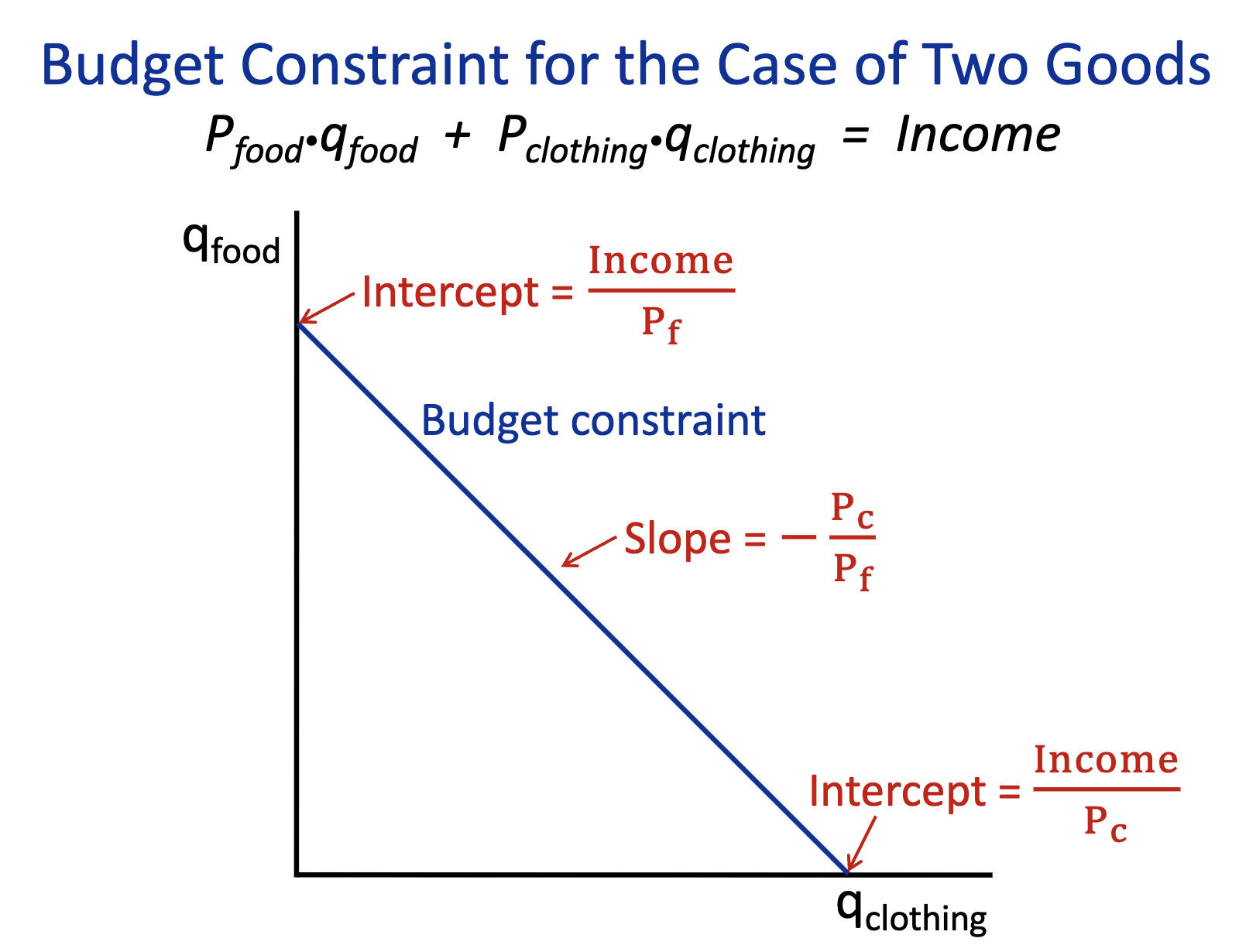

Budget Constraint equation for two goods:

Total Utility

The total happiness one gets from consuming a given amount of a good

Marginal Utility

addition satisfaction a consumer gets from having one more unit of a good or service.

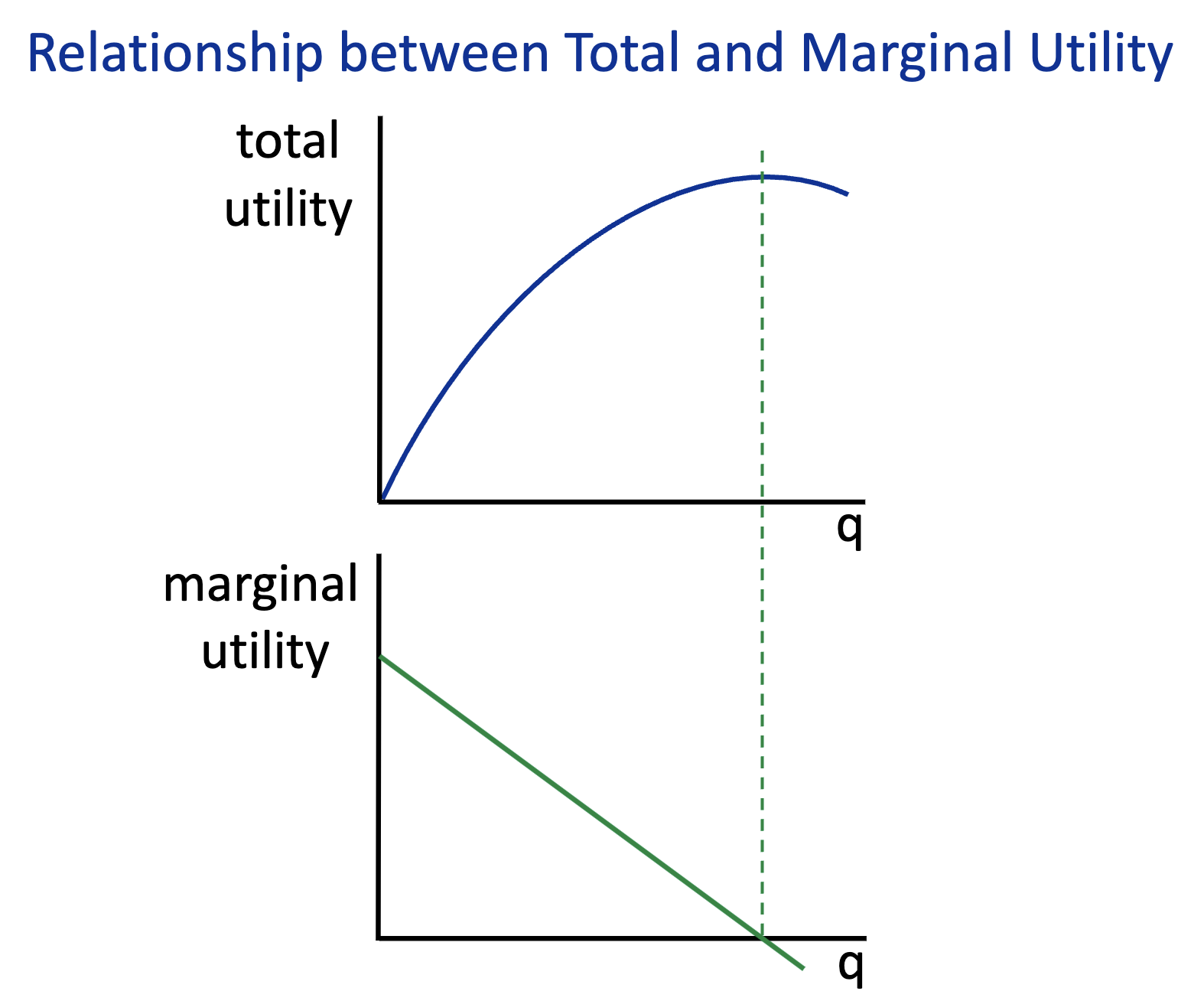

Diminishing Marginal Ulility

The marginal utility of a good or service declines as more of it is consumed by an individual.

What is the equation for the total utility?

What is the equation for the marginal utility?

Draw the graphs of total and marginal utility

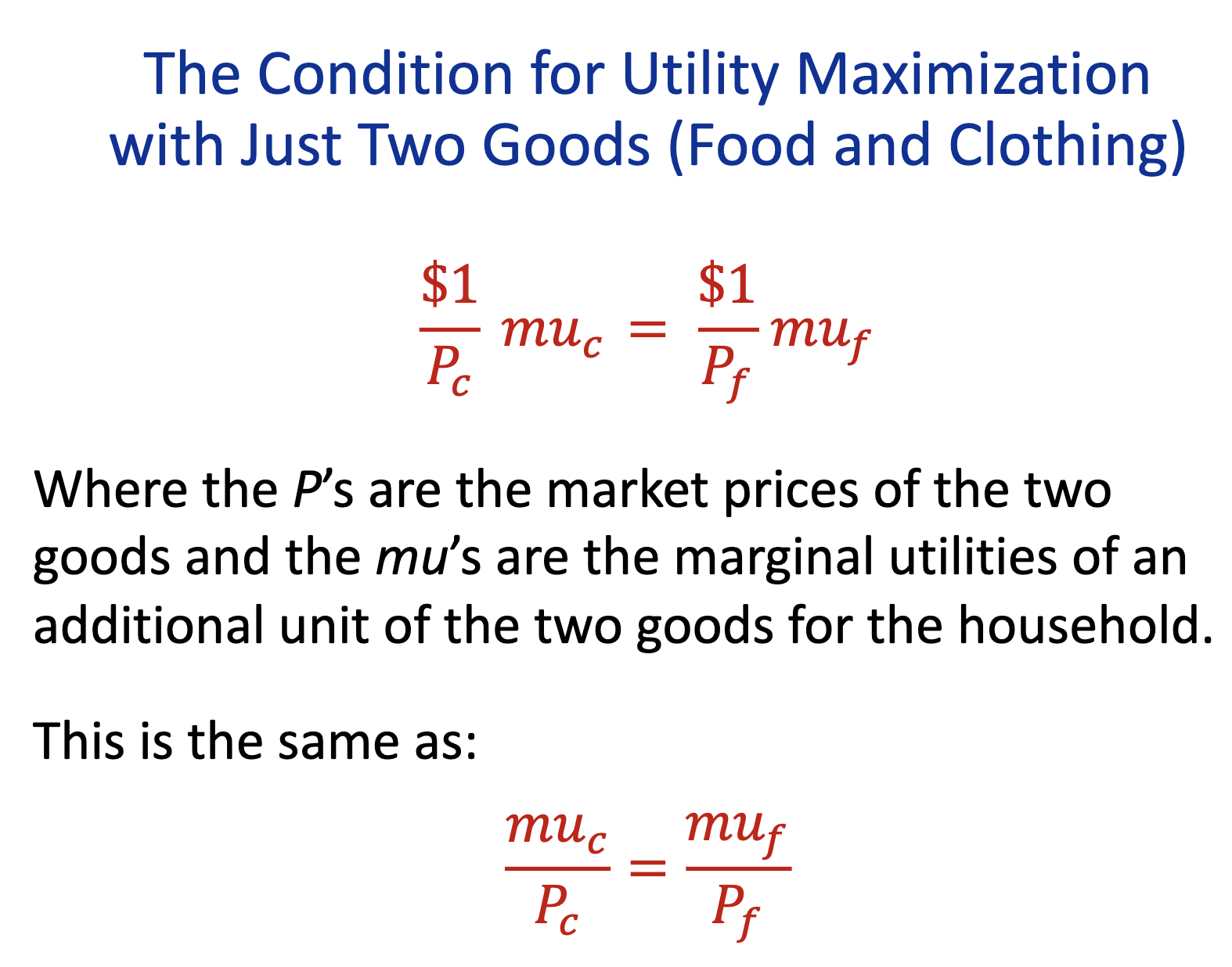

Utility Maximization Condition with just two goods =

Substitution Effect

A decrease in sales for a product bc consumers switch to cheaper alternatives when its price rises.

Income Effect

A decrease in sales when a good’s price rises. If price increases, I won’=Utilitarian

Libertarian

A kind of politics that says the government should have less control over people's lives. I

Utilitarian

For example, if you are choosing ice cream for yourself, the utilitarian view is that you should choose the flavor that will give you the most pleasure

How to find the total revenue (equation)?

Quantity sold * Price

Equation for average total cost:

Total cost/Quantity

How to find the total cost?

Opportunity cost of all inputs

What is the equation for Economic Profit?

Total Revenue - Total Cost = Profit

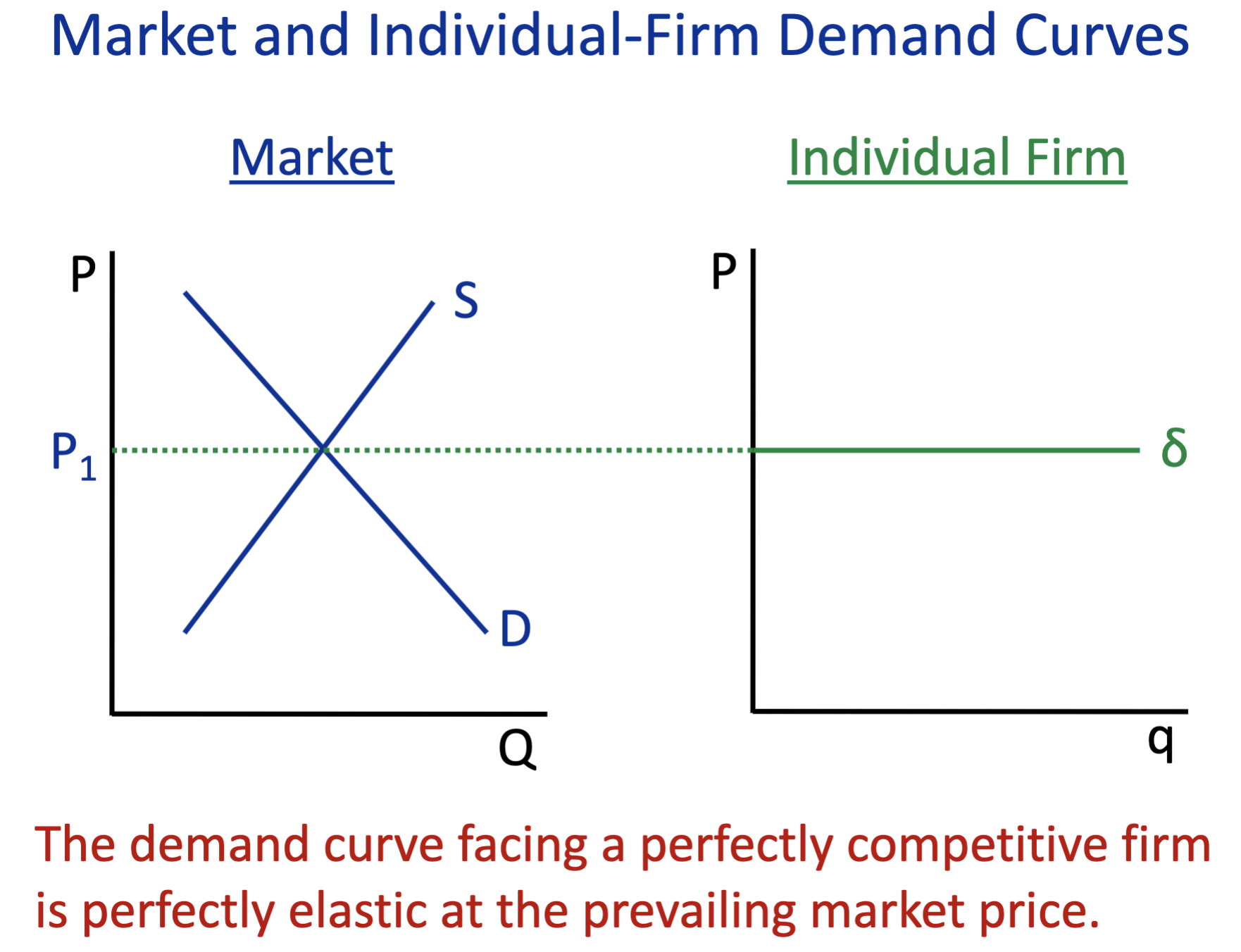

Draw a regular demand market then draw a individual firm demand market

Fixed Cost means

costs that are based on time rather than the quantity produced or sold by your business. ex. rent or bills

Variable Cost means

costs that change as the volume changes. ex. delivery cots, or credit card fees.

Total cost means

The sum of fixed and variable costs

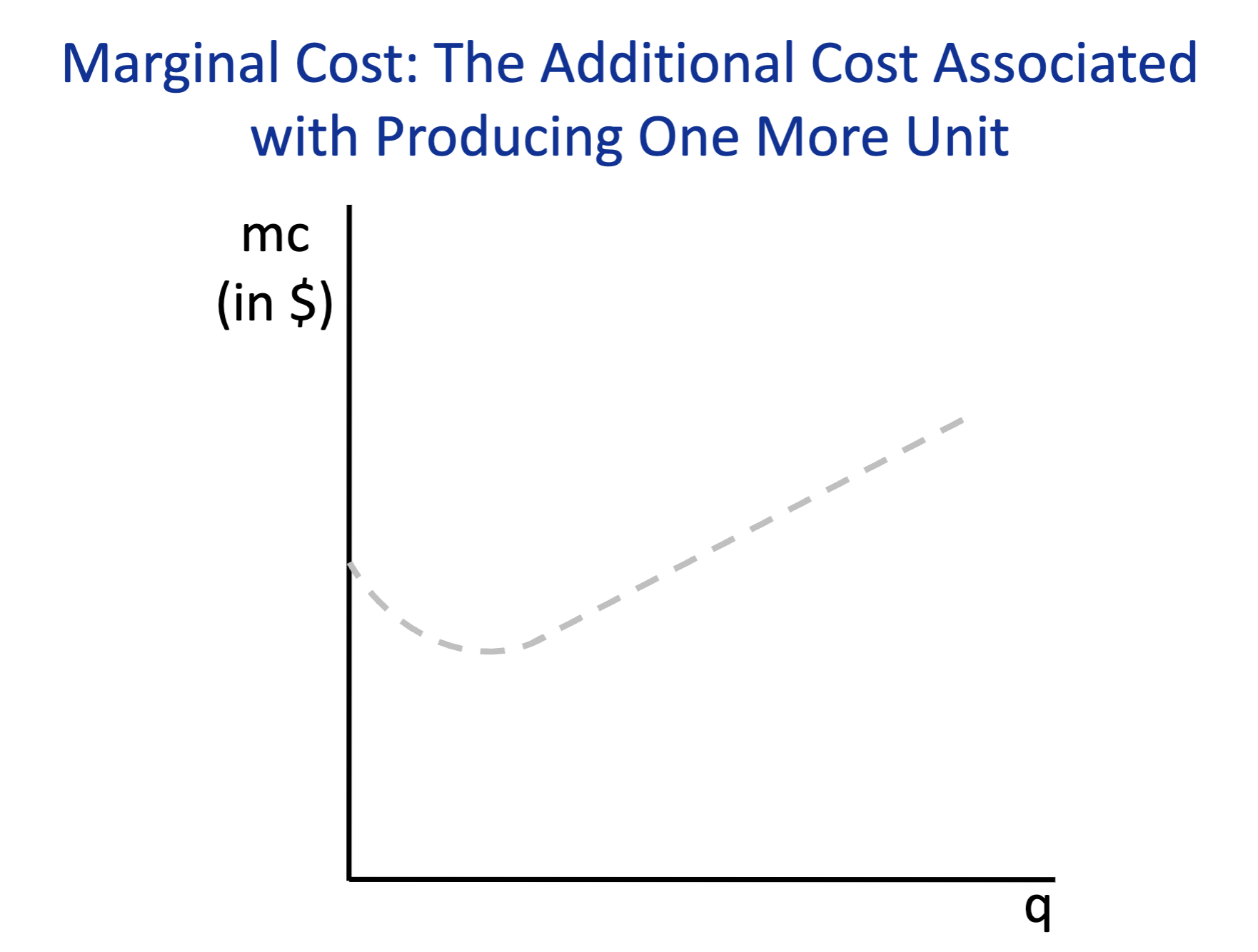

Marginal Cost

The change in total costs from producing one more unit.

Draw a line on how a marginal cost looks like on a graph?

In a perfect competitive firm, Price =

marginal cost/marginal renvenue

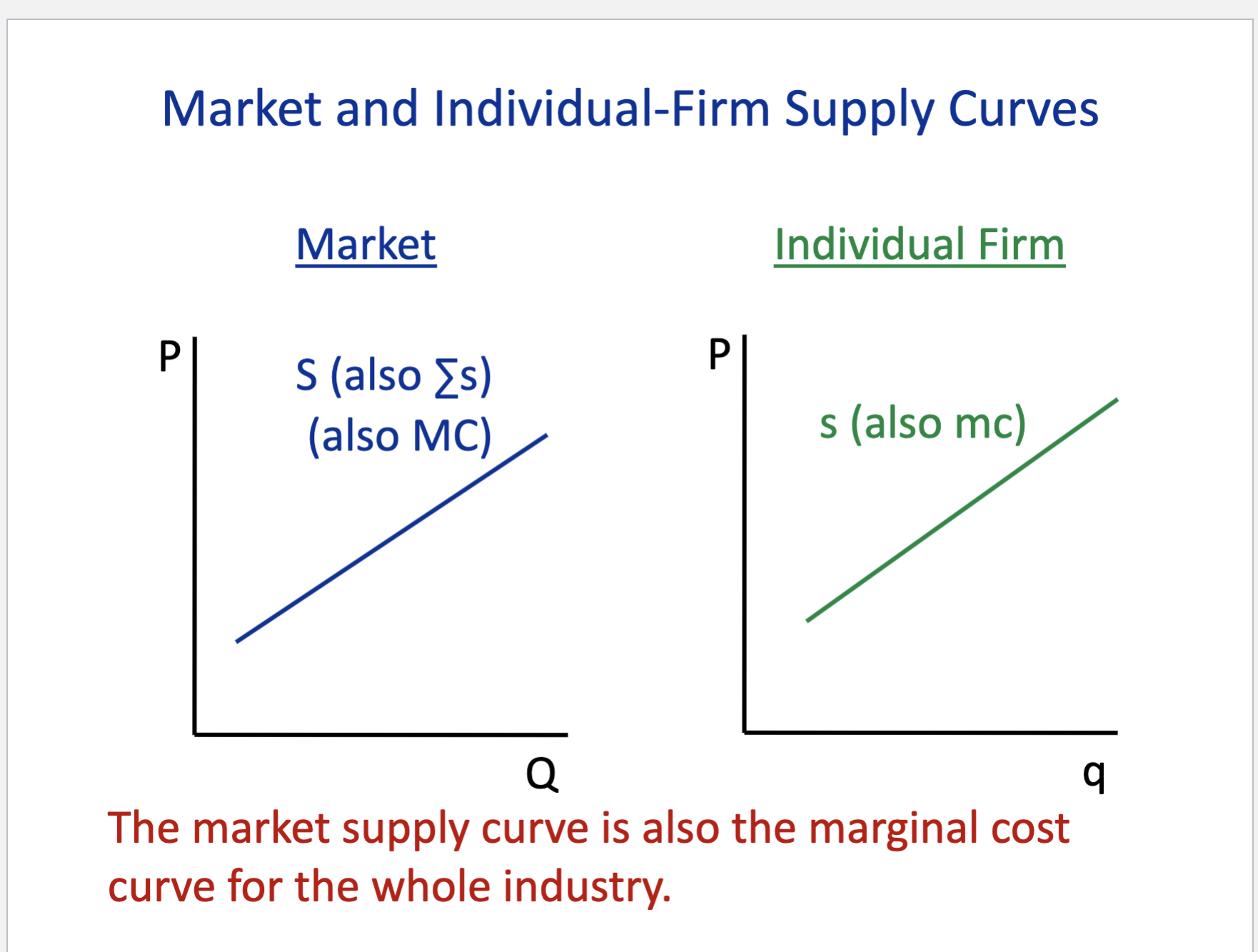

Draw a regular supply market then draw a individual firm supply market

The horizontal sum of individual firms’ supply curves =

Market supply curve

The Industry Supply Curve =

Industry Marginal Cost Curve

Monopoly

when there is only one supplier for a good with no close substitutes → they can set the price and normally yield the largest possible profit. but the demand can fall because of this price point. ex. mircosoft and windows

Natural Monopoly

Only one most effective firm whose supply meets the demand efficiently in the entire market. able to produce at ar (Watch ACDC econ)

Monopoly equation