W20- Investment appraisal (IRR)

1/20

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

21 Terms

What is internal rate of return (IRR)?

the 4th investment appraisal method

it applies NPV calculations to calculate the discount rate (cost of capital) for a project that would deliver an NPV of zero

it shows sensitivity of a project to changes in cost of capital

When should you accept an investment project given an IRR?

when IRR > cost of capital

When should you reject an investment project given an IRR?

when IRR < cost of capital (the project doesn’t generate a large enough return to cover the cost of capital required for investment)

What is the formula for IRR?

ra = lower discount rate (cost of capital) chosen

rb = higher discount rate chosen

NPVa = NPV at discount rate a

NPVb = NPV at discount rate b

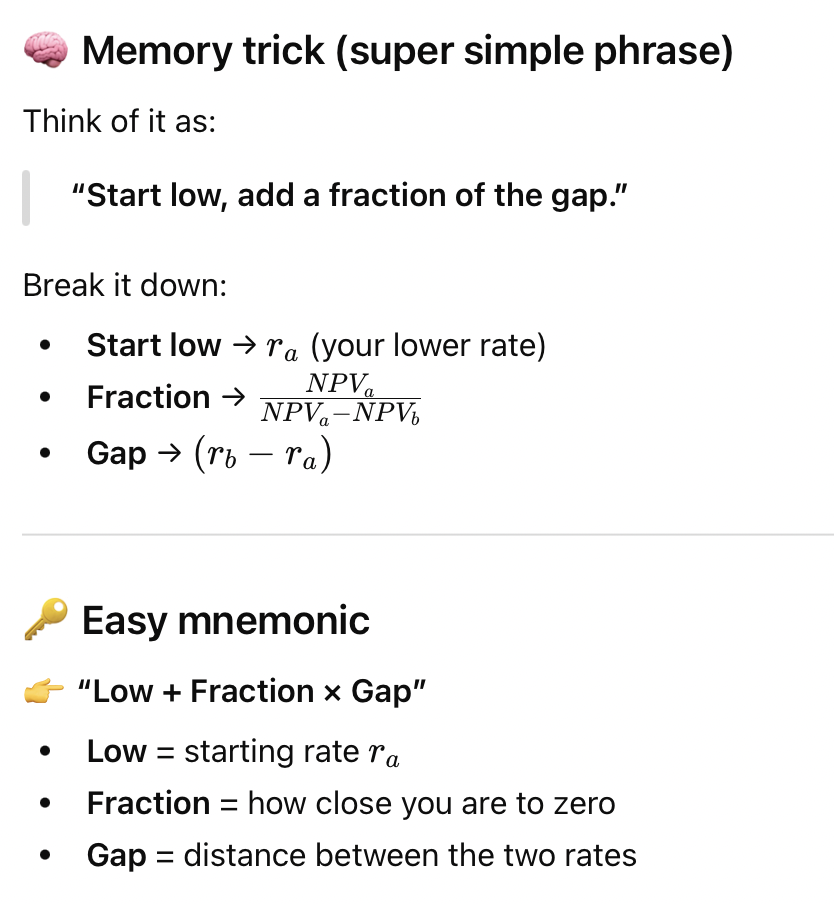

How can I remember the IRR formula?

start low, add a fraction of the gap

Under what condition must the formula be in for it to generate a more accurate IRR?

when NPVa is positive and NPVb is negative

What is the interpretation of the IRR formula?

the formula estimates the discount rate where NPV = 0 by using the linear relationship between 2 known points (discount rate ra yields NPVa and discount rate rb yields NPVb)

Why might using IRR not always be as reliable as using NPV when comparing projects?

it can favour small projects with high proportional returns rather than selecting projects that can create the greatest shareholder wealth

What is meant by non-conventional cash flows?

when some projects have 2 more more IRR (eg. NPV could be 0 at a number of discount rates)

this occurs when cashflows fluctuate from positive to negative (such as a project requiring cash outflows at the end of a project for decommissioning costs

there will be as many IRR as sign changes making IRR a less reliable measure

What are advantages and disadvantages of IRR?

advantages:

considers time value of money

expresses return in a % format easily interpreted

disadvantages:

doesn’t always result in maximised shareholder wealth

uses discount rates- could lead to misleading results

What are the 2 ways in which inflation can impact NPV?

estimates of cash flows (future value) will rise

inflation will make the cost of capital (discount rate) increase

When can we ignore inflation effects when doing NPV calculations?

when all prices related to cash flows are rising at the same rate

increases in the cash flow estimates are offset by the impact of the cost of capital rising

In the real world, prices often change at diff rates so when there are diff rates of inflation how can we adjust our NPV?

by adjusting cash flows by rate of inflation for that cash flow (make sure from year 2 onwards to compound inflation)

by adjusting cost of capital for the general rate of inflation- called the money (nominal) cost of capital

What is the difference between money (nominal) cost of capital and real cost of capital?

money cost of capital - cost of capital adjusted for the general rate of inflation

real cost of capital- cost of capital based on today’s year 0 price levels

What equation can we use to calculate the money cost of capital?

the fisher equation:

1 + money cost of capital = (1 + real cost of capital) x (1 + general inflation rate)

What is meant by general inflation and specific inflation?

general inflation - the overall rise in price levels across the economy (eg. indicated by CPI)

specific inflation0 the price change affecting a particular cost or revenue item relevant to the project which is diff to general inflation rate

Going ahead with a project will result in incremental tax cash flows, which 2 do we need to consider?

corporation tax on taxable profits generated by project

tax relief given due to ‘capital allowances’ on capital assets (depreciation expense that tax authorities allow on things like machinery)

What cashflow will occur due to corporation tax on taxable profits?

incremental future cash outflow which may occur the year after the profit is generated

what does capital allowances result in?

tax-allowable depreciation (capital allowances) reduces taxable profit and results in a cash saving

when calculating taxable profit, we need to make adjustments for capital allowances so what is the the formula assumed?

taxable profits = project cash flows for year - capital allowances

(ignore year 0 cash flows)

What are the calculation steps for working out taxable profit?

work out cash flows for each year before tax (using NPV method)

calculate capital allowance for each year on any capital expenditure

deduct capital allowance from that year’s cash inflow

multiply result by the tax rate given in the question

check scenario to determine when the tax is paid (usually this year or next year) and include the tax paid as a cash outflow