ch5: national insurance

1/21

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

22 Terms

class 1 employee NIC

deducted by the employer

paid by employee on earnings

What are the types of National Insurance

Class 1 (Employee) → paid by employee on earnings

Class 1 (Employer) → paid by employer on earnings

Class 1A → paid by employer on benefits (15%)

What is included in earnings for NIC?

Salary / wages (cash earnings)

Most benefits (for employer NIC)

Vouchers (treated as cash)

not included

Reimbursed business expenses

Exempt income (same as income tax rules)

How is employee NIC calculated (2025/26)?

£0 – £12,570 → 0%

£12,571 – £50,270 → 8%

Above £50,270 → 2%

Formula:

(Main band × 8%) + (Excess × 2%)

How is employer NIC calculated?

£0 – £5,000 → 0%

Above £5,000 → 15%

Formula:

(Total earnings – £5,000) × 15%

What is the employment allowance?

Employer can deduct £10,500 from total NIC bill

Applies to employer NIC only

Reduces overall liability (not per employee)

What is Class 1A NIC?

Paid by employer on benefits in kind

Rate = 15%

Employee does NOT pay this

Formula:

Benefits × 15%

vouchers are subject to class ___ employee and employer NIC, as they deemed as cash equivalent

1

Key rules to remember for NIC?

Use cash earnings only for Class 1

Ignore reimbursed expenses

Employee + Employer NIC calculated separately

Class 1A = benefits only

Same income figure used for both employee & employer NIC

What is an earnings period for NIC?

Weekly paid → weekly thresholds

Monthly paid → monthly thresholds

Exam default → usually annual basis unless told otherwise

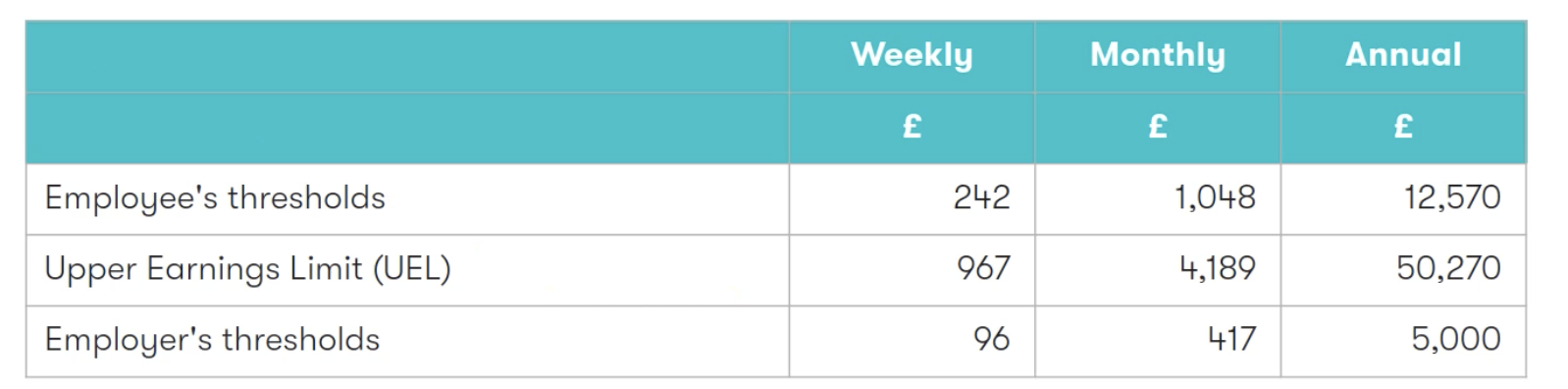

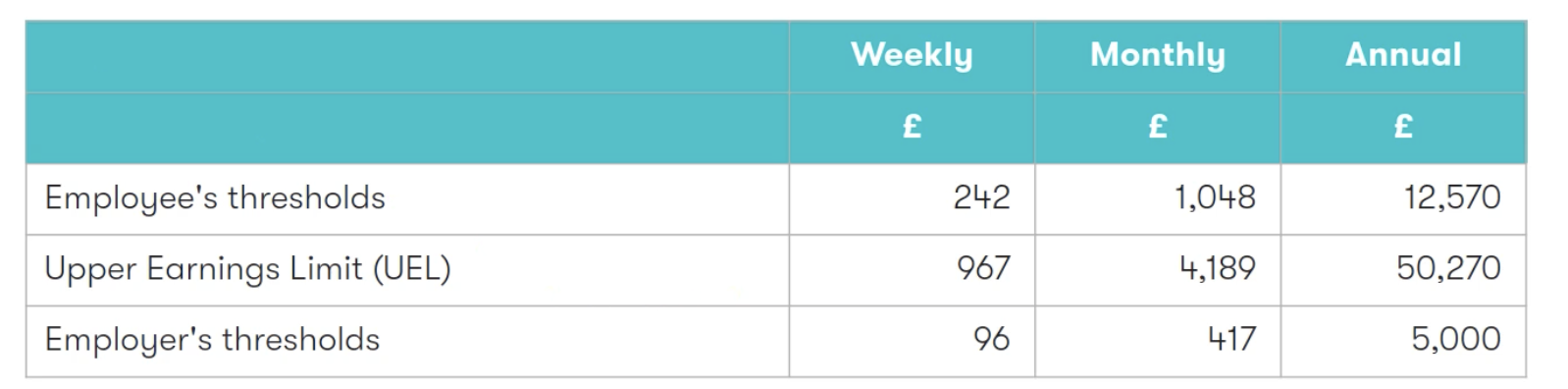

What are the key NIC thresholds (2025/26)?

Employee:

£12,570 (annual threshold)

£50,270 (UEL)

Employer:

£5,000 threshold

👉 Monthly equivalents:

£1,048 (employee threshold)

£4,189 (UEL)

£417 (employer threshold)

When do you use annual vs monthly/weekly NIC?

Normal employees:

→ Use pay period basis (monthly/weekly)Exam shortcut:

→ Use annual unless question says otherwise

How is NIC calculated for directors?

ALWAYS use ANNUAL earnings basis

Combine total income for the year

Apply thresholds once

Prevents manipulation of timing

How are bonuses treated in NIC?

Employees (monthly method):

→ Bonus taxed in that specific month

→ Can push income into higher band (2%)Directors:

→ Bonus included in total annual earnings

Why does earnings period affect NIC?

Monthly spikes (e.g. bonus)

→ Can trigger 2% rate earlierAnnual method smooths income

→ Often gives lower NIC

What is the employment allowance?

Deduct up to £10,500 from employer NIC

Applies to total employer liability (not per employee)

Some employers are excluded

What is Class 1A National Insurance?

Paid by employer only

On non-cash benefits (benefits in kind)

Additional cost to employer

Examples: car, accommodation, medical insurance

What counts as benefits for NIC?

Non-cash benefits provided by employer

Use cash equivalent value (same as income tax)

Are reimbursed expenses subject to NIC?

NIC if genuine business expense

NIC applies if it’s a private expense

Key idea:

Business = no NIC

Private = NIC

How is mileage treated for NIC?

Up to 45p per mile → NO NIC

Above 45p → Excess is taxable for NIC

Formula:

(Actual – 45p limit) = NIC amount

Why might employees prefer benefits over salary?

Salary → subject to Class 1 NIC (employee + employer)

Benefits → subject to Class 1A only (employer only)

Employee saves NIC

What are the key NIC rules to remember?

Class 1 → salary

Class 1A → benefits

Employer pays more NIC than employee

Directors → annual basis

Mileage: 45p limit

Business expenses → no NIC