OS Worksheet perfect competition

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

TRUE/FALSE

Each market structure has certain key characteristics that distinguish it from the other structures

TRUE

TRUE/FALSE

In practice, it is sometimes difficult to decide precisely which market structure a given firm or industry most appropriately fits.

TRUE

TRUE/FALSE

In perfect competition, no single firm produces more than an extremely small proportion of output, so no firm can influence the market price.

TRUE

TRUE/FALSE

At the other end of the continuum of market environments from perfect competition is pure monopoly, which involves a single seller

TRUE

TRUE/FALSE

Unlike monopoly, oligopoly allows for some competition between firms; unlike competition, individual firms have a significant share of the total market for the good being produced

TRUE

TRUE/FALSE

Oligopolies do not pay attention to the actions of competing firms.

FALSE

TRUE/FALSE

It would be possible to have perfect competition without easy market entry and exit.

FALSE

TRUE/FALSE

Perfectly competitive firms are price takers because their influence on price is insignificant.

TRUE

TRUE/FALSE

A perfectly competitive market is approximated most closely in highly organized markets for agricultural commodities

TRUE

TRUE/FALSE

A perfectly competitive firm cannot sell at any figure higher than the current market price and would not knowingly charge a lower price, because it could sell all it wants at the market price

TRUE

TRUE/FALSE

In a perfectly competitive market, individual sellers can change their output without altering the market price.

TRUE

TRUE/FALSE

In a perfectly competitive industry, the market demand curve is perfectly elastic at the market price.

FALSE

TRUE/FALSE

The perfectly competitive model does not assume any knowledge on the part of individual buyers and sellers about market demand and supply—they only have to know the price of the good they sell.

TRUE

TRUE/FALSE

In a perfectly competitive market, marginal revenue is constant and equal to the market price.

TRUE

TRUE/FALSE

For a perfectly competitive firm, as long as the price derived from expanded output exceeds the marginal cost of that output, the expansion of output creates additional profits

TRUE

TRUE/FALSE

Producing at the profit-maximizing output level means that a firm is actually earning economic profits

FALSE

TRUE/FALSE

A competitive firm earning zero economic profits will be unable to continue in operation over time.

FALSE

TRUE/FALSE

A firm will not produce at all unless the price is greater than its average variable costs.

TRUE

TRUE/FALSE

As new firms enter an industry where sellers are earning economic profits, the result will include a reduction in the equilibrium price.

TRUE

TRUE/FALSE

In long-run equilibrium, perfectly competitive firms make zero economic profits, earning a normal return on the use of their capital.

TRUE

Which market structure has the largest number of firms?

a. perfect competition

b. monopolistic competition

c. oligopoly

d. monopoly

a. perfect competition

Which of the following is false?

a. Monopolistically competitive firms produce differentiated products.

b. Oligopolistic firms produce a substantial fraction of the output of their industry.

c. A monopoly is the single seller of a product without a close substitute.

d. Only a perfectly competitive firm has no power to influence the market price for its

product.

e. All of the above are true

e. All of the above are true

An individual perfectly competitive firm

a. may increase its price without losing sales.

b. is a price maker.

c. has no perceptible influence on the market price.

d. sells a product that is differentiated from those of its competitors.

c. has no perceptible influence on the market price.

When will a perfectly competitive firm’s demand curve shift?

a. never

b. when the market demand curve shifts

c. when new producers enter the industry in large numbers

d. when either b or c occurs

d. when either b or c occurs

In a market with perfectly competitive firms, the market demand curve is and the demand curve facing each

individual firm is .

a. upward sloping; horizontal

b. downward sloping; horizontal

c. horizontal; downward sloping

d. horizontal; upward sloping

e. horizontal; horizonta

b. downward sloping; horizontal

A perfectly competitive firm seeking to maximize its profits would want to maximize the difference between

a. its marginal revenue and its marginal cost.

b. its average revenue and its average cost.

c. its total revenue and its total cost.

d. its price and its marginal cost.

e. either a or d

c. its total revenue and its total cost.

A perfectly competitive firm maximizes its profit at an output in which

a. total revenue exceeds total cost by the greatest dollar amount.

b. marginal cost equals the price.

c. marginal cost equals marginal revenue.

d. all of the above are true

d. all of the above are true

The minimum price at which a firm would produce in the short run is the point at which

a. price equals the minimum point on its marginal cost curve.

b. price equals the minimum point on its average variable cost curve.

c. price equals the minimum point on its average total cost curve.

d. price equals the minimum point on its average fixed cost curve.

b. price equals the minimum point on its average variable cost curve.

If a perfectly competitive firm finds that price is greater than AVC but less than ATC at the quantity where its

marginal cost equals the market price,

a. the firm will produce in the short run but may eventually go out of business.

b. the firm will produce in the short run, and new entrants will tend to enter the industry over

time.

c. the firm will immediately shut down.

d. the firm will be earning economic profits.

e. both b and d are true.

a. the firm will produce in the short run but may eventually go out of business.

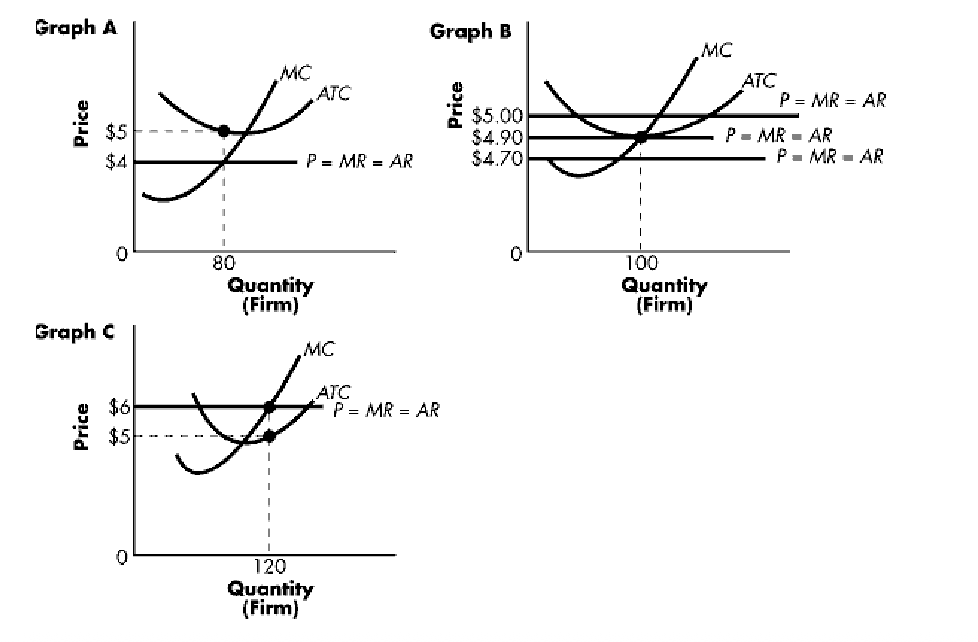

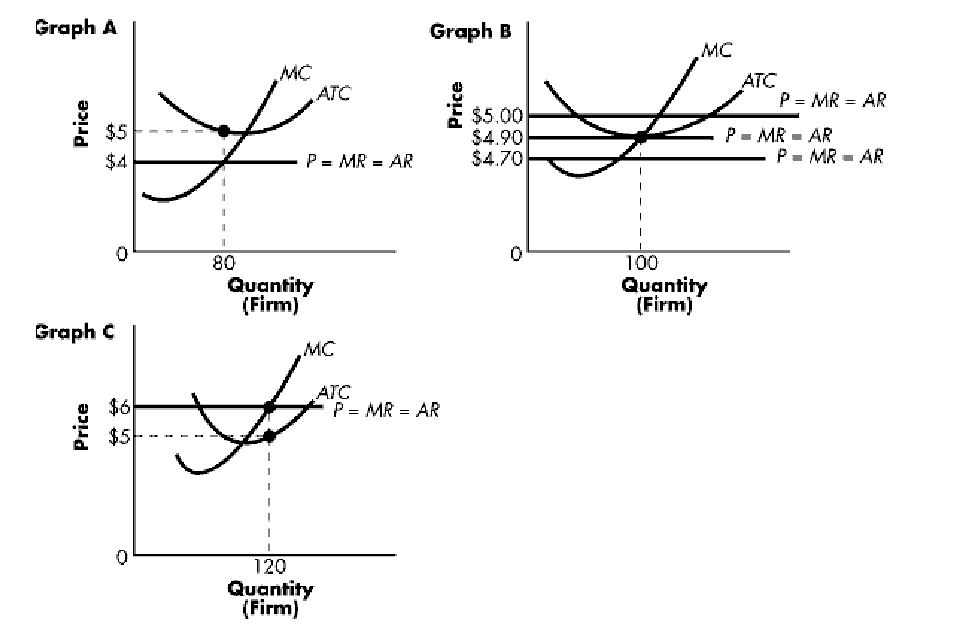

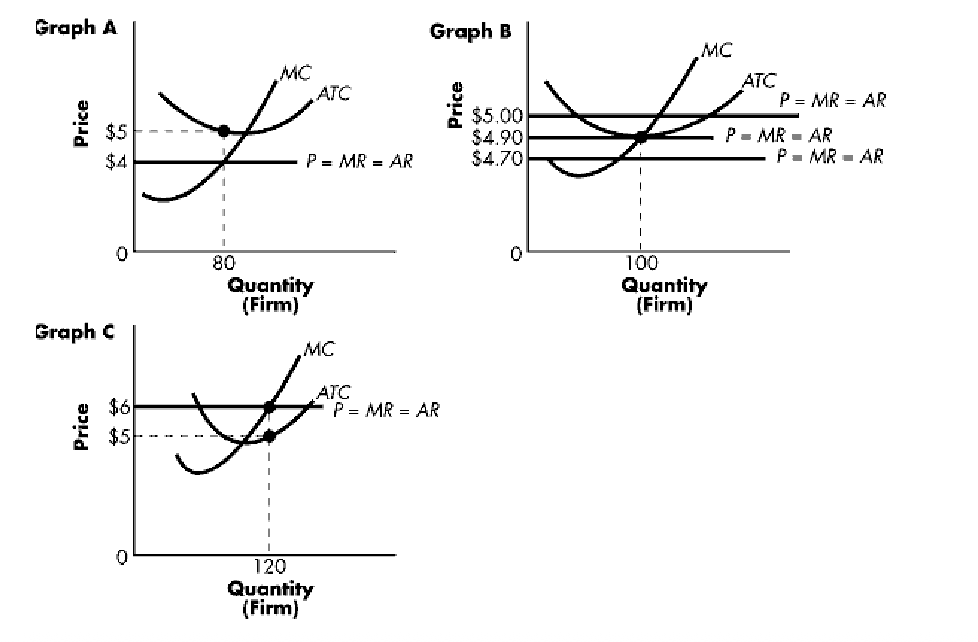

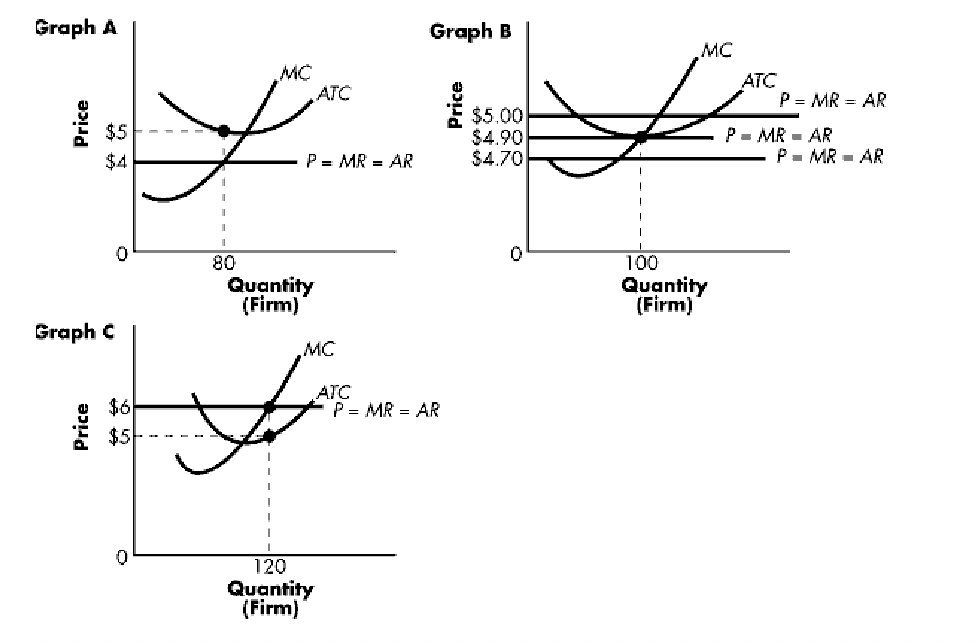

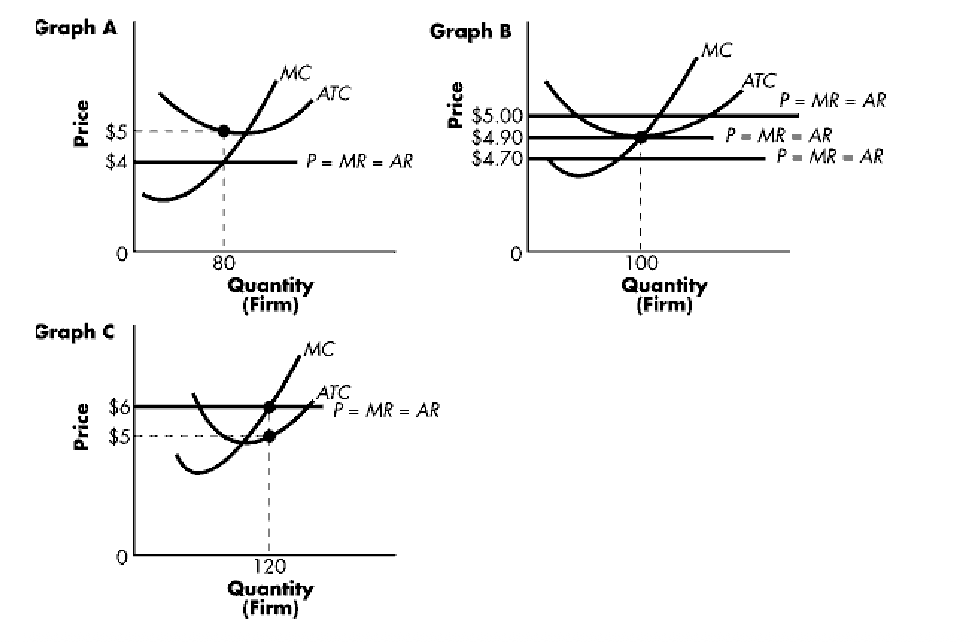

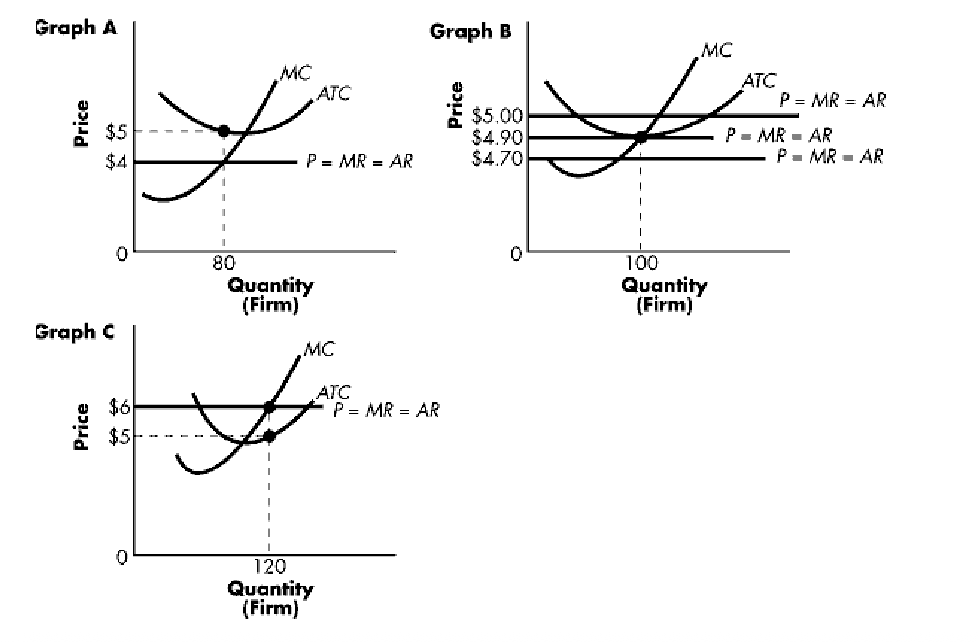

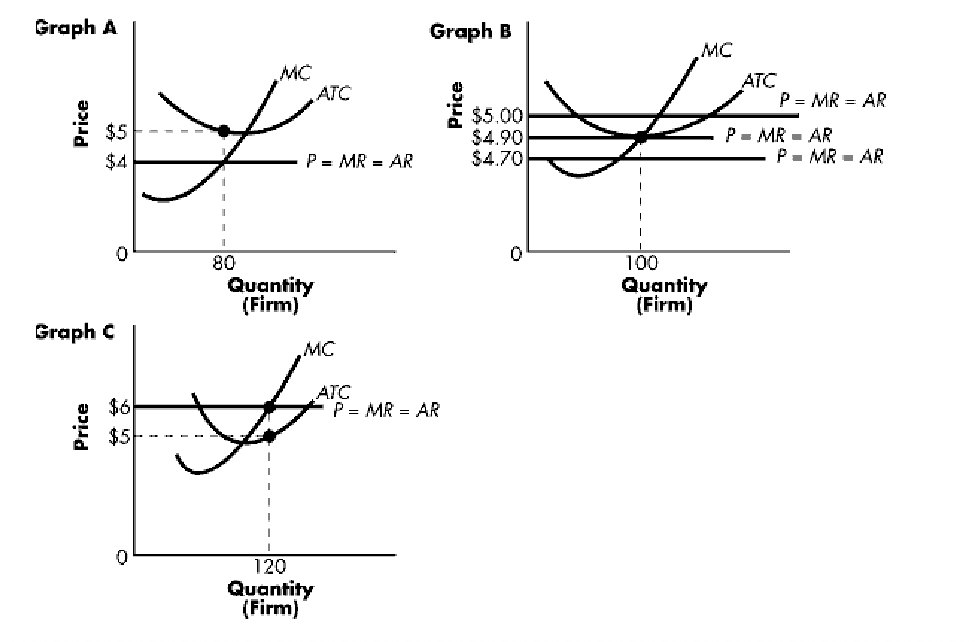

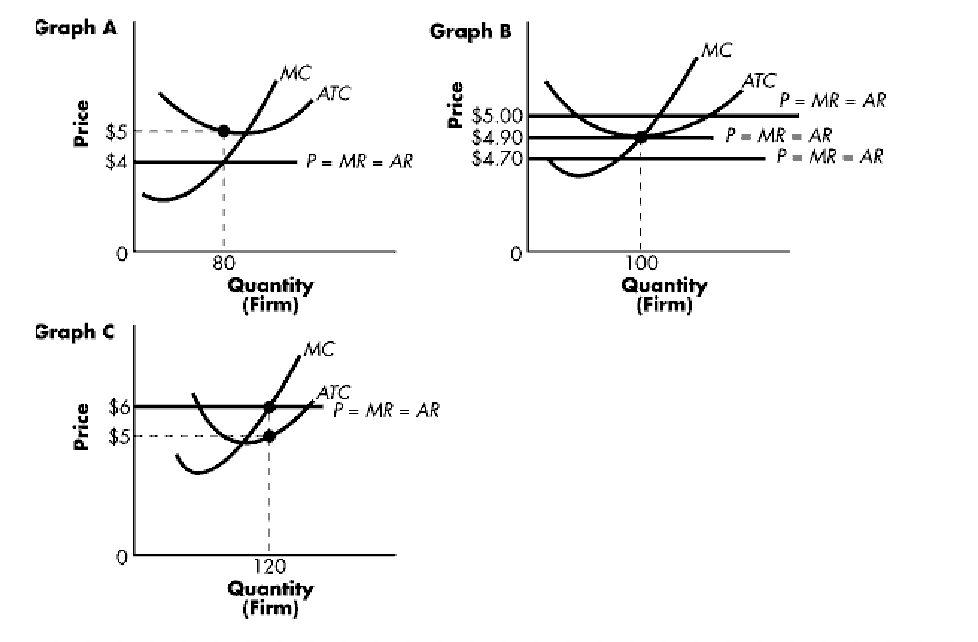

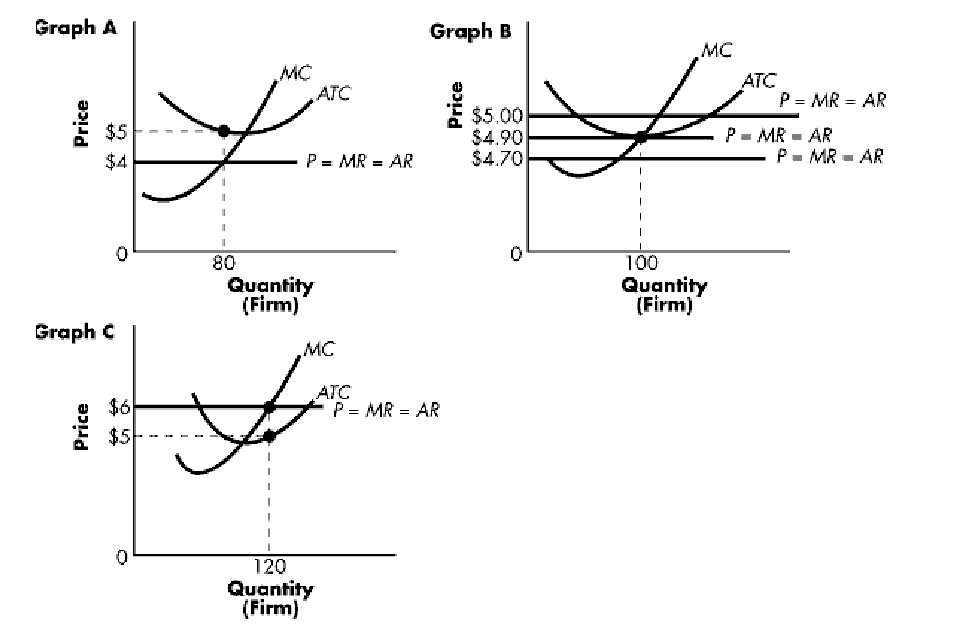

Refer to Exhibit 1. Graph A exhibits a price-taking firm:

a. experiencing a loss of $80.

b. making a profit of $80.

c. making a profit of $400.

d. experiencing a loss of $400.

a. experiencing a loss of $80.

Refer to Exhibit 1. Graph B exhibits a price-taking firm:

a. which will lose money when the market price equals $4.90.

b. which will make an economic profit when the market price equals $4.90.

c. which will break even when the market price equals $4.90.

d. which will shut down when the market price equals $4.90

c. which will break even when the market price equals $4.90.

Refer to Exhibit 1. If the market price increased to $5 in Graph B, this firm should:

a. immediately shut down.

b. increase output.

c. decrease output.

d. continue producing the same level of output

b. increase output.

Refer to 1. If the market price decreased to $4.70 in Graph B, this firm should:

a. immediately shut down if price is greater than average variable cost.

b. increase output.

c. decrease output.

d. continue producing the same level of output.

c. decrease output.

Refer to Exhibit 1. Graph C exhibits a price-taking firm:

a. experiencing a loss of $120.

b. making a profit of $120.

c. making a profit of $720.

d. experiencing a loss of $600.

e. which is breaking even

b. making a profit of $120.

Refer to Exhibit 1. Total revenue for the firm in Graph C equals:

a. $120.

b. $150.

c. $600.

d. $720.

e. none of the above

d. $720.

Refer to Exhibit 1. Total revenue for the firm in Graph A equals:

a. $40.

b. $80.

c. $320.

d. $400.

e. none of the above

c. $320.

Refer to Exhibit 1. Total revenue for the firm in Graph B at a market price of $4.90 equals:

a. $490.

b. $500.

c. $4.90.

d. $0.

e. none of the above

a. $490.

Refer to Exhibit 1. Total costs for the firm in Graph B at a market price of $4.90:

a. equals $500.

b. equals $490.

c. equals $470.

d. equals $4.90.

e. cannot be determined from the information provide

b. equals $490.

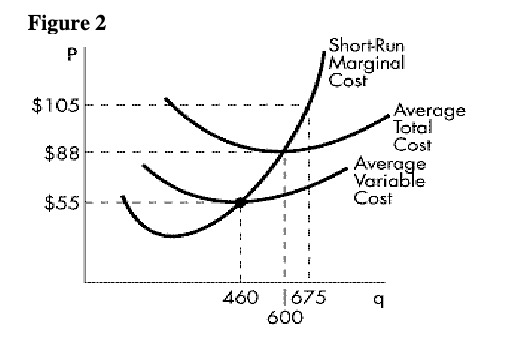

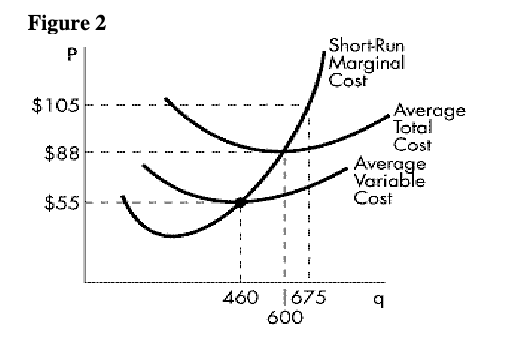

Refer to Figure 2. When the market price equals $54, the firm:

a. should shut down.

b. should continue operating temporarily despite an economic loss because the firm is able to

cover all of its variable costs.

c. should continue operating temporarily despite an economic loss because the firm is able to

cover a portion of its fixed costs.

d. should continue operating because the firm is making a profit.

e. both b. and c. are true.

a. should shut down.

Refer to Figure 2. Suppose the market price equals $88 and the firm is currently producing 600 units of output. In this situation, the firm:

a. is maximizing profit.

b. should increase production of output in order to maximize profit.

c. should decrease production of output in order to maximize profit.

d. should shut down in order to minimize economic losses

a. is maximizing profit.

Refer to Figure 2. When the market price equals $105, and the firm sells 675 units of output, the firm:

a. is earning a normal profit.

b. is earning positive economic profits.

c. is experiencing a loss, but should continue operating temporarily because business

conditions may improve.

d. is experiencing a loss and should shut down

b. is earning positive economic profits.

The entry of new firms into an industry will likely

a. shift the industry supply curve to the right.

b. cause the market price to fall.

c. reduce the profits of existing firms in the industry.

d. do all of the above.

d. do all of the above.

Which of the following statements concerning equilibrium in the long run is incorrect?

a. Firms will exit the industry if economic profits equal zero.

b. Firms are able to vary their plant sizes in the long run.

c. Economic profits are eliminated as new firms enter the industry.

d. The market price equals both marginal cost and average total cost.

a. Firms will exit the industry if economic profits equal zero.

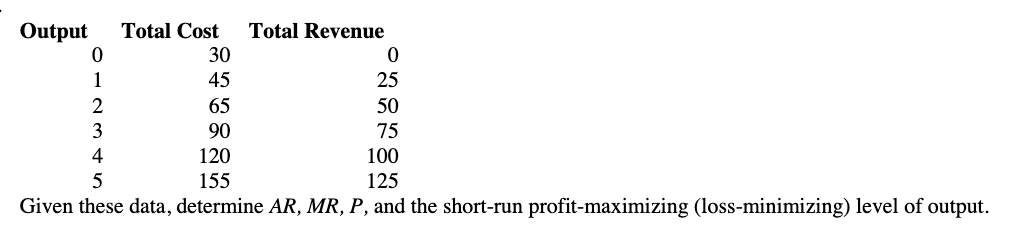

AR, MR and P = 25; Output level is at 3 (MR = MC at this point)