Chapter 1 AP Econ

1/21

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

22 Terms

economics

how society makes the best choices under scarcity

scarcity

limited resources

everything is assumed to be scare

forces us to choose something over another

opportunity cost

what you give up to get something else

behavior

all actions are done with purpose

to increase utility (the satisfaction allowed from a g/s)

act in self interest but not selfishness

marginal analysis

= marginal benefits vs. marginal costs

marginal = extra

= (added benefits vs. added costs)

example of marginal analysis

buying a bigger engagement ring

marginal benefit = higher anticipated pleasure

marginal cost = higher cost than original

does obtaining the marginal benefits always come at a marginal cost of something else?

yes; since everything is scarce, obtaining the marginal benefit from something always comes at a marginal cost of something else

economic principles

generalization

ceteris paribus = assume other things equal → only one variable changes

positive economics

facts, cause/effect, subjective

normative economics

values, judgement, opinions, objective

budget line/ constraint

represents all possible combinations of consumption of 2 goods at fixed costs.

interior

attainable because you don’t have to use all of provided money but inefficient because you don’t maximize profit

anterior

unattainable because you don’t have enough money

4 factors of production

land

labor

capital

entrepreneurial ability

land

all natural resources

labor

physical and mental exertion in production of goods and services

cannot be forced labor → no cost on slavery

capital

assets used to be produce goods

capital goods = physical assets to produce other goods/services

not money → money is a means to buy capital goods, not a resource itself

capital goods = facilitate production of consumer goods

consumer goods = directly satisfy individual wages/needs

entrepreneurial ability

person combines [land, labor, and capital] into a business venture

takes risks, makes decisions

production possibilities model

PP table = shows different combinations of 2 products that can be produced with limited resources

PP curve/constraint/frontier = graph

what is the law of increasing opportunity cost

when the line gets steeper → giving up more of one product to produce another

describe the behavior of the points on the PPC

any point on the PPC is an efficient use of resources, in which there is a max employment

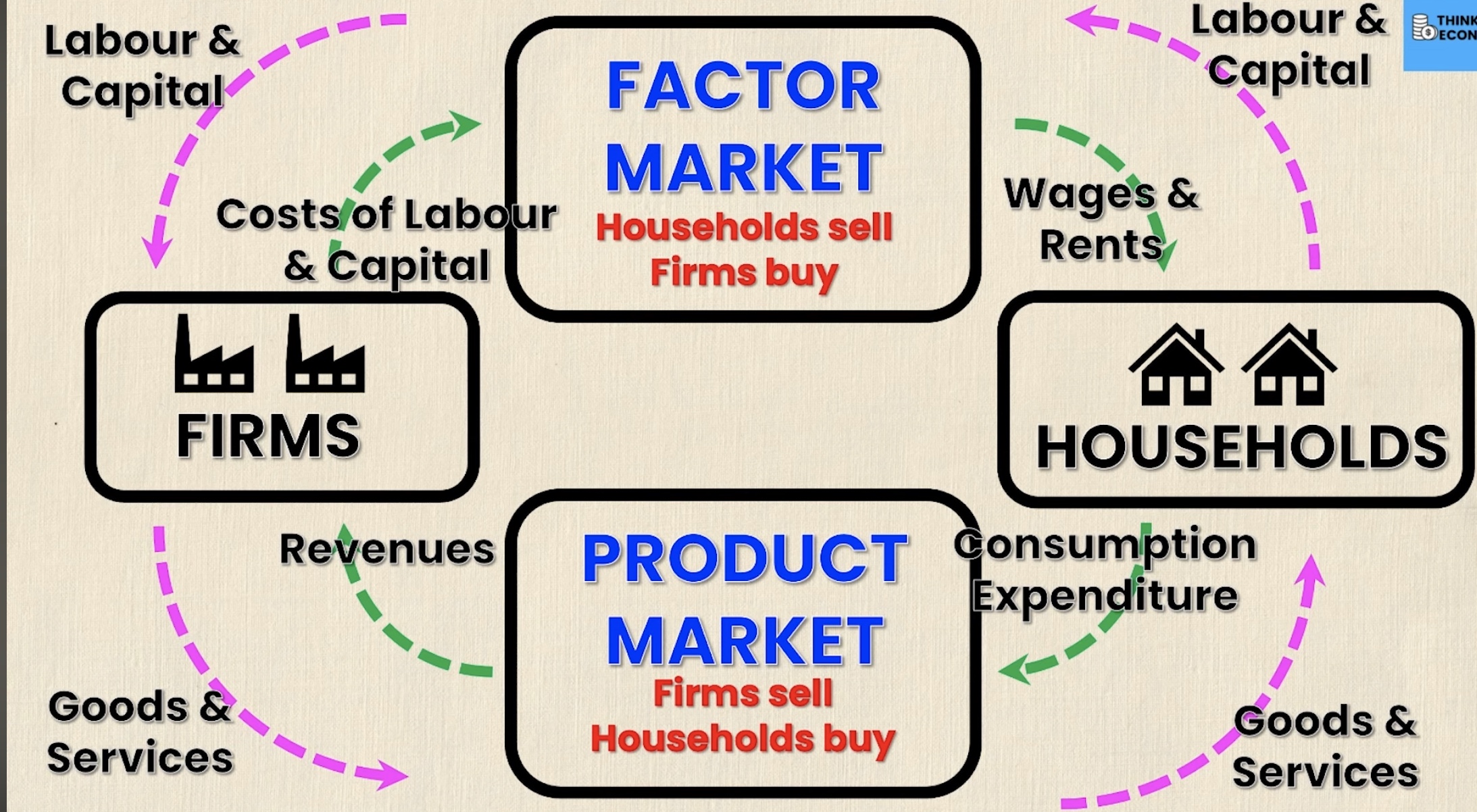

draw a circular flow model