production functions & cost curves

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

23 Terms

what do firms have to decide?

whether and what quantity of a good to produce, whether to enter or exit the market (assume perfectly competitive market)

what determines the cost of production?

the cost of inputs

Q = f(K,L) where K and L are production inputs

L = labour

K = capital

what are fixed production inputs?

an input that cannot be varied in the short-term (eg. factories)

what are variable production inputs?

an input that can be varied by the firm at any time (eg. labour)

how do we calculate marginal product (MP) of an input?

marginal product of an input = change in total output by increasing that input by one unit

change in Q / change in input

MPinput depends on how much of each input you already have (100th labourer is less useful than 2nd labourer)

what is the law of diminishing marginal returns (DMR) for an input?

as more of a variable input is added, the MP of that input will decline

what are fixed costs of production?

the costs of fixed inputs paid in the short-term

what are variable costs of production?

the costs of variable inputs that the producer chooses to purchase in the short-term

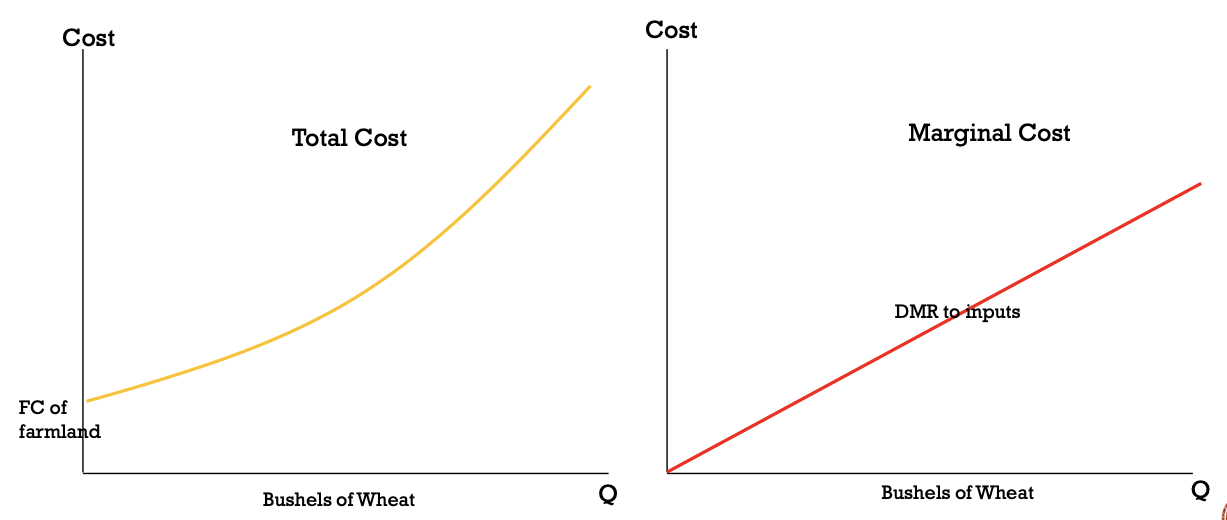

how do we calculate marginal cost of production?

marginal cost = total cost for producing the next unit of the good

change in TC / change in Q

MC depends on how much has already been produced

MC never contains fixed costs as they are the same no matter how many units are produced

what does diminishing marginal returns to inputs suggest?

that as Q increases, marginal costs will increase

(not worth employing the 100th labourer as they will yield a smaller increase in Q for the same price as the 99th labourer)

how do total cost & marginal cost curves differ?

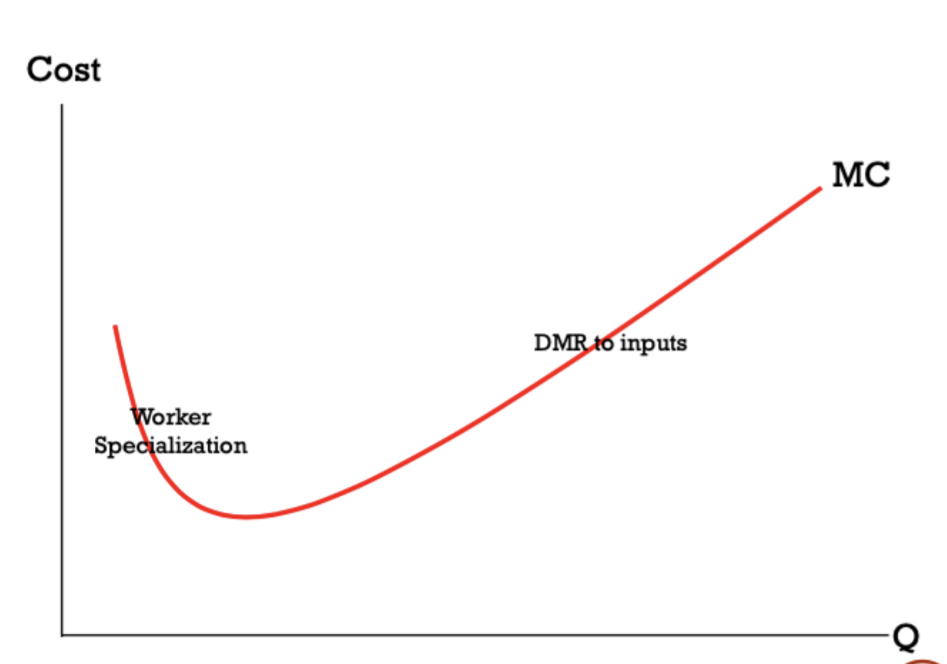

what is the exception to diminishing marginal returns?

worker specialisation

as soon as a 2nd person is employed, each can perform specialised tasks

at first, adding workers increases efficiency; when everyone is fully specialised, then DMR kicks in

how do we graph marginal costs taking into account worker specialisation?

MC is first downward sloping

eventually slopes upwards as everyone is specialised

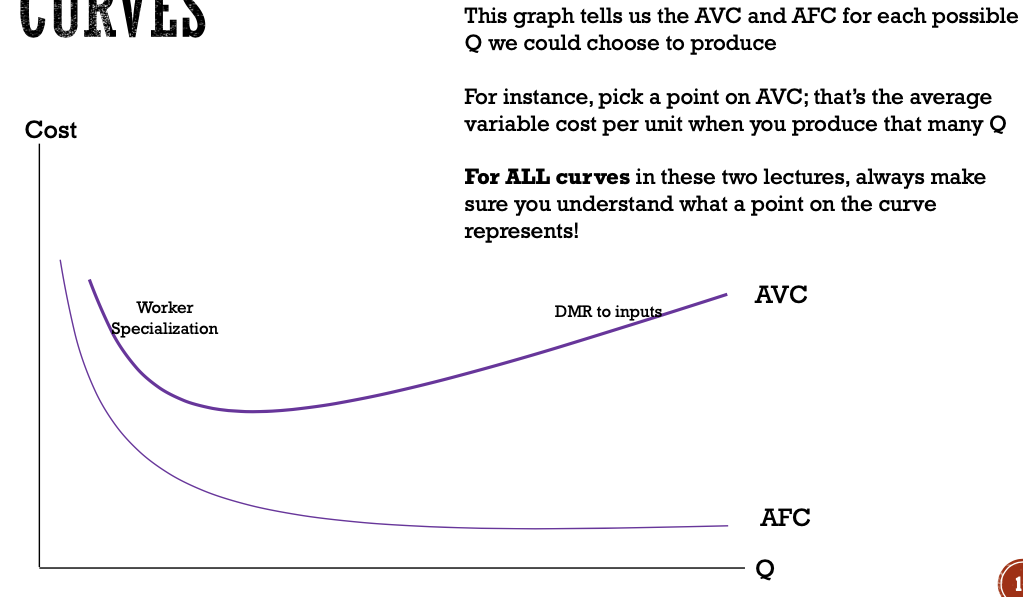

how do we calculate average total cost (ATC)?

total cost / quantity

ATC = average variable costs + average fixed costs

how do we graph average variable costs (AVC) & average fixed costs (AFC)?

AVC is initially downward sloping due to worker specialisation, then upward due to DMR to inputs

AFC is decreasing with respect to Q, since TFC is constant

how do we get the ATC curve from the AVC & AFC curves?

add them together

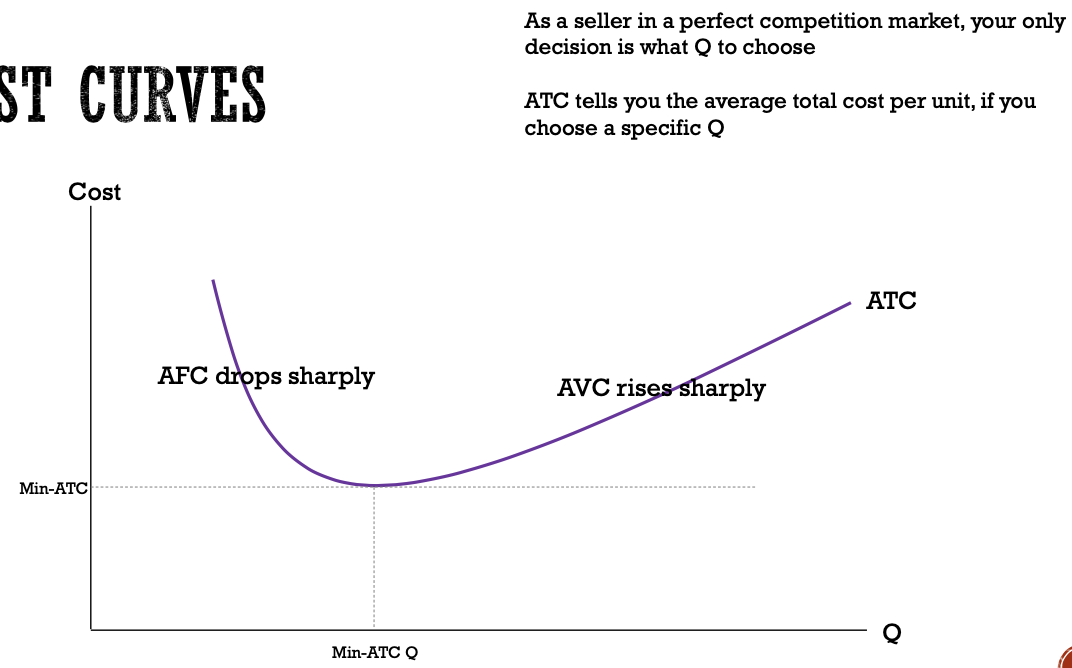

how does ATC look compared to Q?

at low Q, AFC dominates and ATC decreases when Q increases

at high Q, AVC dominates and ATC increases when Q increases

this leads to an ATC curve that is first decreasing at low Q and then increasing

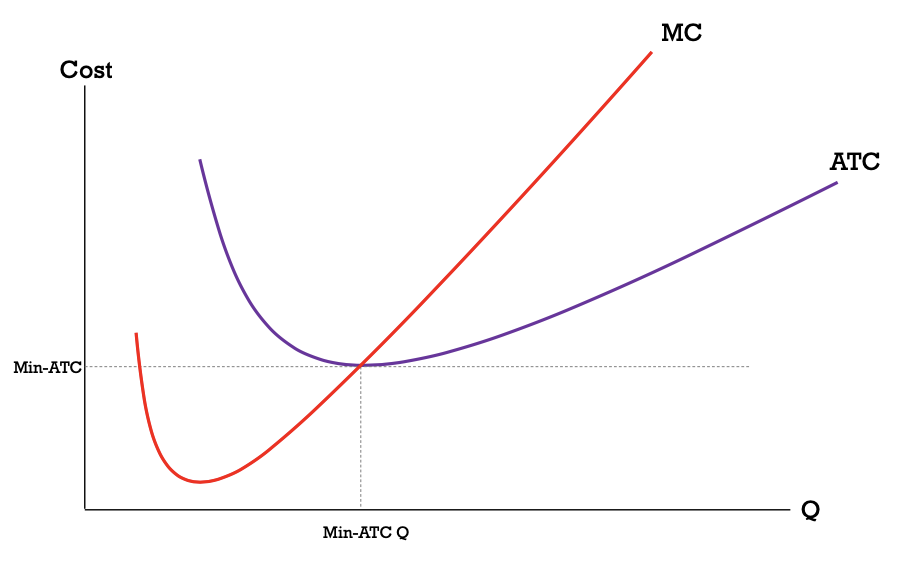

what does the minimum on the ATC curve represent?

this is the min-ATC quantity where the firm can produce each unit for the minimum possible ATC

this is the minimum-cost output where MC = ATC

what does the minimum on the AVC curve represent?

the AVC curve intersects which MC at its local minimum

this is the min quantity at which the firm can produce for the least possible AVC

how do we calculate profits?

profits = revenue - costs

total revenue = P x Q

what are explicit costs?

accounting costs

eg. out of pocket payments such as wages

what are implicit costs?

opportunity costs

eg. what else could you have bought such as forgone wages when you are self-employed

cost curves include implicit costs to get overall economic profit

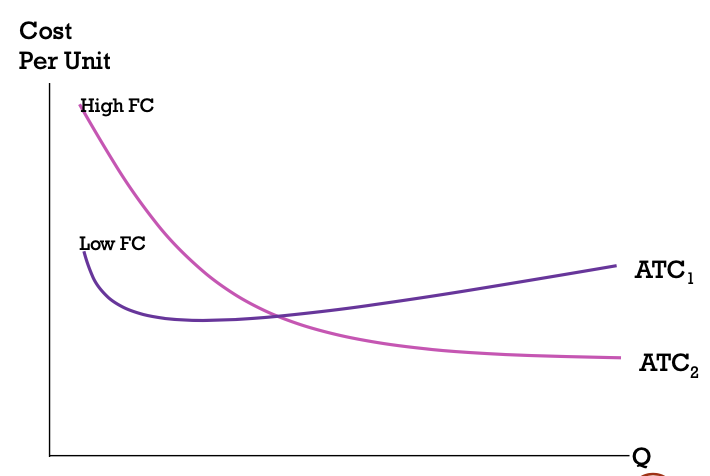

in the long run, what does a cost curve look like with a high FC compared to a low FC?

in the short run, FC cannot be changed

in the long run, choose the best FC investment for your expected Q

in this example, overall ATC is less if you invest in a high FC