Microeconomics - Chapter 11

1/33

Earn XP

Description and Tags

Behind the Supply Curve: Inputs and Costs

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

def of a firm

an organization that produces goods or services for sale

what is production

the process of turning input to outputs

what is the production function

the relationship b/w the quantity of inputs a firm uses and the quantity of output it produces.

what is a fixed input

an input whose quantity is fixed for a period of time and cannot be varied

what is a variable input

an input whose quantity the firm can vary at any time

what is the long run

the period in which all input can be varied

what is the short run

the period in which at least one input is fixed

what is the total product curve

the curve shows how the quantity of output depends on the quantity of the variable input for a given quantity of the fixed input

what is the marginal product and what does MPL stand for

marginal product is the additional quantity of output that is produced by using one more unit of that input and MPL stands for marginal product of labor

what is MPL

it’s the change in output resulting from an additional unit in the amount of labor input (change in quantity/change in labor)

the MP is the slope of the

total product curve

what do I mean by a unit of labor

an additional hour of labor or an additional week (time)

what is a fixed cost

a cost that does not depend on the quantity of output produced. its the cost of the fixed input

what is a variable cost

a cost that depends on the quantity of output produced. Its the cost of variable input.

what is the total cost

the sum of the fixed cost and the variable cost of producing that quantity of output

equation of the total cost

TC= FC+VC

what is the total cost curve

the curve shows how total costs depends on the quantity of output

the total cost curve becomes..

steeper as more output is produced

why does the total cost curve become steeper

because of diminishing returns

what is the marginal cost

its the change in total cost generated by one additional unit of output

equation of marginal cost

MC=change in TC/change in quantity of output

why is the marginal cost curve upward sloping

more and more of the variable input must be used to produce each additional unit of output as the amount of output already produced rises. since each unit of the variable input must be paid for, the cost per additional unit of output also rises

what are the 3 different average costs

average total cost, fixed cost, and variable cost

equation for average total cost

ATC= TC/Q (output produced)

equation for average fixed cost

AFC=FC/Q (output produced)

equation for average variable cost

AVC= VC/Q (output produced)

what are the effects on average total costs when increasing output

spreading effect and diminishing returns effect

explain the spreading effect

the larger the output leads to lower average fixed cost

explain the diminishing returns effect

the larger the output, leads to a higher average variable cost

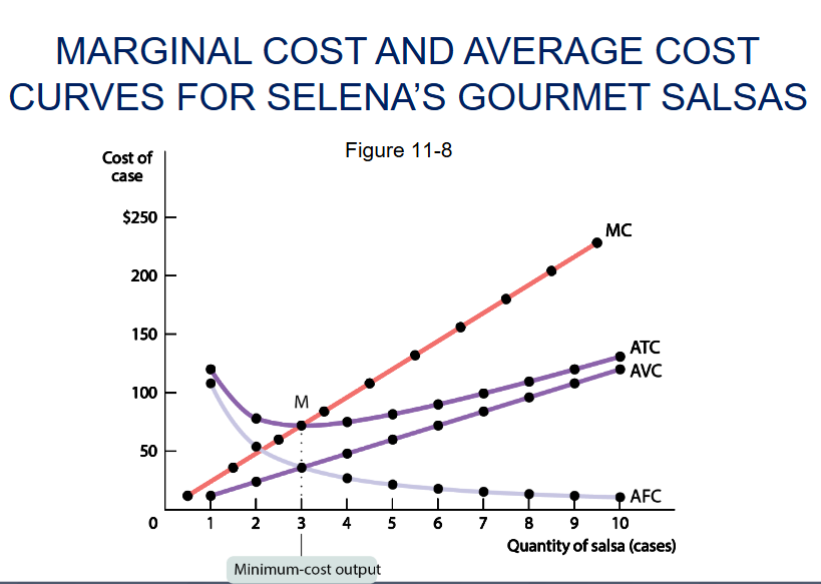

draw the marginal cost and average cost curves together

at high levels output the spreading effect is

what is increasing returns to scale (economies of scale)

when long-run average total cost declines as output increases

what is decreasing returns to scale (diseconomies of scale)

when long-run average total cost increases as output increases

what are constant returns to scale

when long-run average total cost is constant as output increases