Chapter 5 - The Financial Sector

1/118

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

119 Terms

Interest Rate

The interest rate is a price, calculated as a percentage of the amount borrowed, charged by lenders to borrowers for the use of their savings for one year.

Savings-Investment Spending Identity

Savings and investment spending are always equal for the economy as a whole.

Budget surplus

The difference between tax revenue and government spending when tax revenue exceeds government spending.

Budget deficit

The difference between tax revenue and government spending when government spending exceeds tax revenue.

Budget balance

The difference between tax revenue and government spending.

National Savings

The sum of private savings and the budget balance, is the total amount of savings generated within the economy.

Capital Inflow

The net inflow of funds into a country

Wealth

The value of a household’s accumulated savings.

Financial Asset

A paper claim that entitles the buyer to future income from the seller.

Physical Asset

A claim on a tangible object that gives the owner the right to dispose of the object as he or she wishes.

Liability

A requirement to pay money in the future.

What are the three tasks of a financial system?

Reducing transaction costs, reducing risk, and providing liquidity.

transaction costs

The expenses of negotiating and executing a deal.

Financial risk

Uncertainty about future outcomes that involve financial losses and gains.

Diversification

An individual can engage in diversification by investing in several different assets, so that the possible losses are independent events.

Liquid

An asset is liquid if it can be quickly converted into cash without much loss of value.

Illiquid

An asset is illiquid if it cannot be quickly converted into cash without much loss of value.

Loan

A lending agreement between an individual lender and an individual borrower.

Default

Occurs when the borrower fails to make payments as specified by the loan or bond contract.

Loan-backed security

An asset created by pooling individual loans and selling shares in that pool.

Financial intermediary

An institution that transforms the funds it gathers from many individuals into financial assets.

Mutual funds

A financial intermediary that creates a stock portfolio and then resells shares of this portfolio to individual investors.

Pension fund

A type of mutual fund that holds assets in order to provide retirement income to its members.

Life insurance company

Sells policies that guarantee a payment to a policyholder’s beneficiaries when the policyholder dies.

Bank Deposits

A claim on a bank that obliges the bank to give the depositor his or her cash when demanded.

Bank

A financial intermediary that provides liquid assets in the form of bank deposits to lenders and uses those funds to finance the liquid investment spending needs of borrowers.

Money

Any asset that can easily be used to purchase goods and services.

Currency in Circulation

Cash held by the public.

Checkable Bank Deposits

Bank accounts on which people can write checks.

Money Supply

The total value of financial assets in the economy that are considered money.

Medium of Exchange

Any asset that individuals acquire for the purpose of trading goods and services rather than for their own consumption.

Store of Value

A means of holding purchasing power overtime.

What are the three roles of money?

It is a medium of exchange, a store of value, and a unit of account.

Unit of Account

A measure used to set prices and make economic calculations.

Commodity Money

A good used as a medium of exchange that has intrinsic value in other uses.

Commodity-Backed Money

A medium of exchange with no intrinsic value, whose ultimate value is guaranteed by a promise that it can be converted into valuable goods.

Fiat Money

A medium of exchange whose value derives entirely from its official status as a means of payment.

Monetary Aggregate

An overall measure of the money supply.

Near-moneys

Financial assets that can’t be directly used as a medium of exchange, but can be readily converted into cash or checkable bank deposits. Ex. Savings Accounts

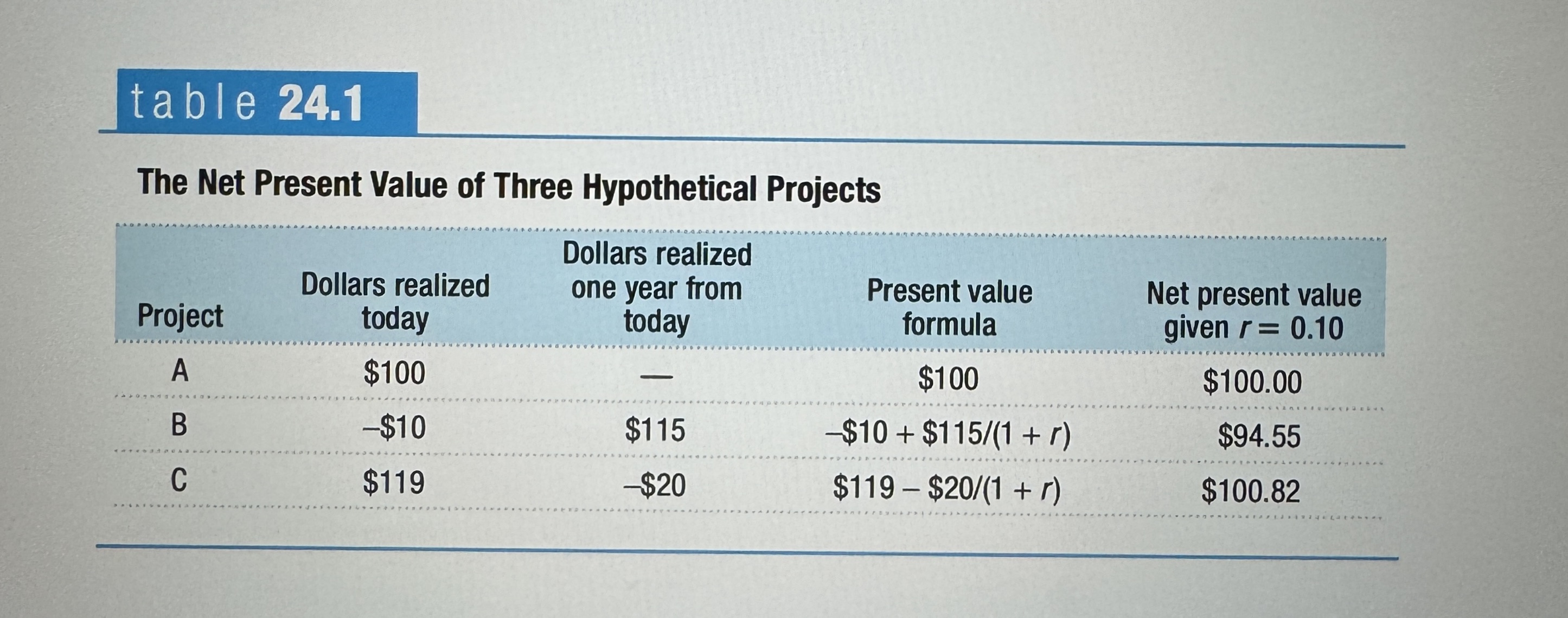

Present value

The present value of $1 realized one year from now is $1/(1 + r): The amount of money you must lend out today in order to have one dollar in one year. It is the value to you today of one dollar realized one year from now. r = interest rate. Use powers above the parentheses to go further than 1 year. $1/(1 + r)² etc.

Net Present Value

The present value of current and future benefits minus the percent value of current and future costs.

Bank Reserves

The currency banks hold in their vaults plus their deposits at the federal reserve.

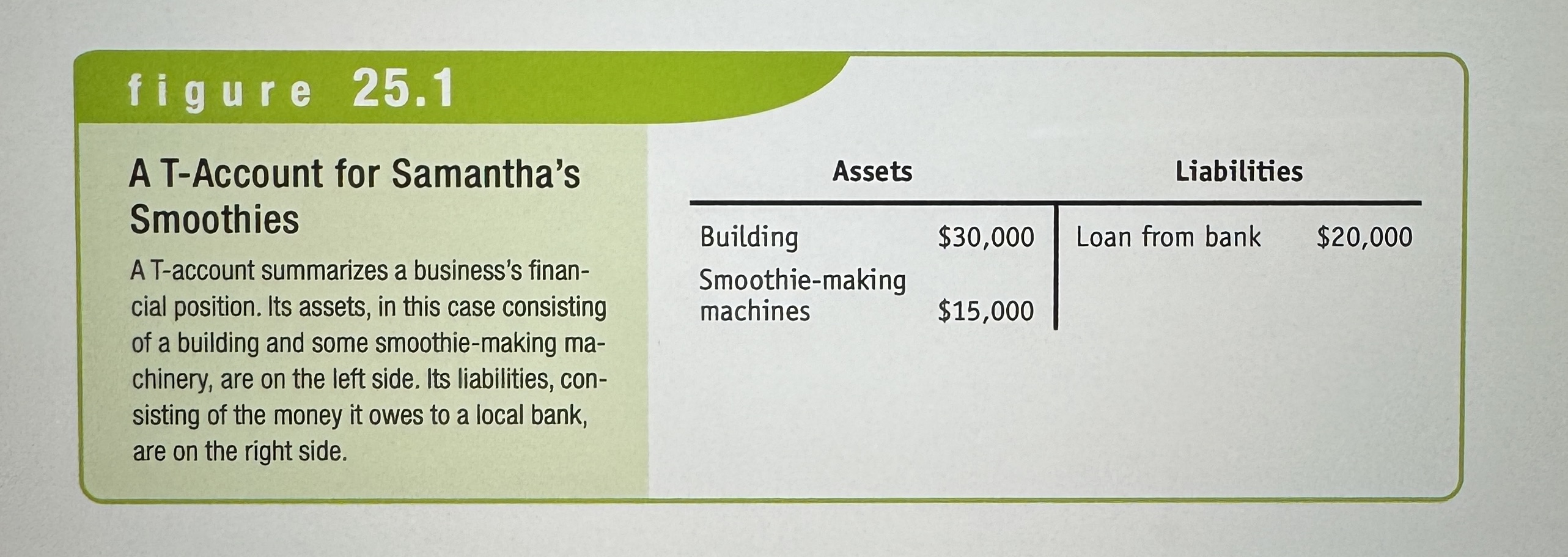

T-account

A tool for analyzing a businesses financial position by showing, in a single table, the businesses assets on the left and liabilities on the right.

Reserve Ratio

The fraction of bank deposits that a bank holds as reserves.

Required Reserve Ratio

The smallest fraction of deposits that the federal reserve allows banks to hold.

Bank Run

A phenomenon in which many of the banks depositors try to withdraw their funds due to fears of a bank failure.

Deposit insurance

Guarantees that a banks depositors will be paid even if the bank can’t come up with the funds, up to a maximum amount per account.

Reserve requirements

Rules set by the federal reserve that determine the required reserve ratio for banks.

Discount Window

An arrangement in which the federal reserve stands ready to lend money to banks.

What are four bank regulations?

Banks have deposit insurance, capital requirements, reserve requirements, and the discount window.

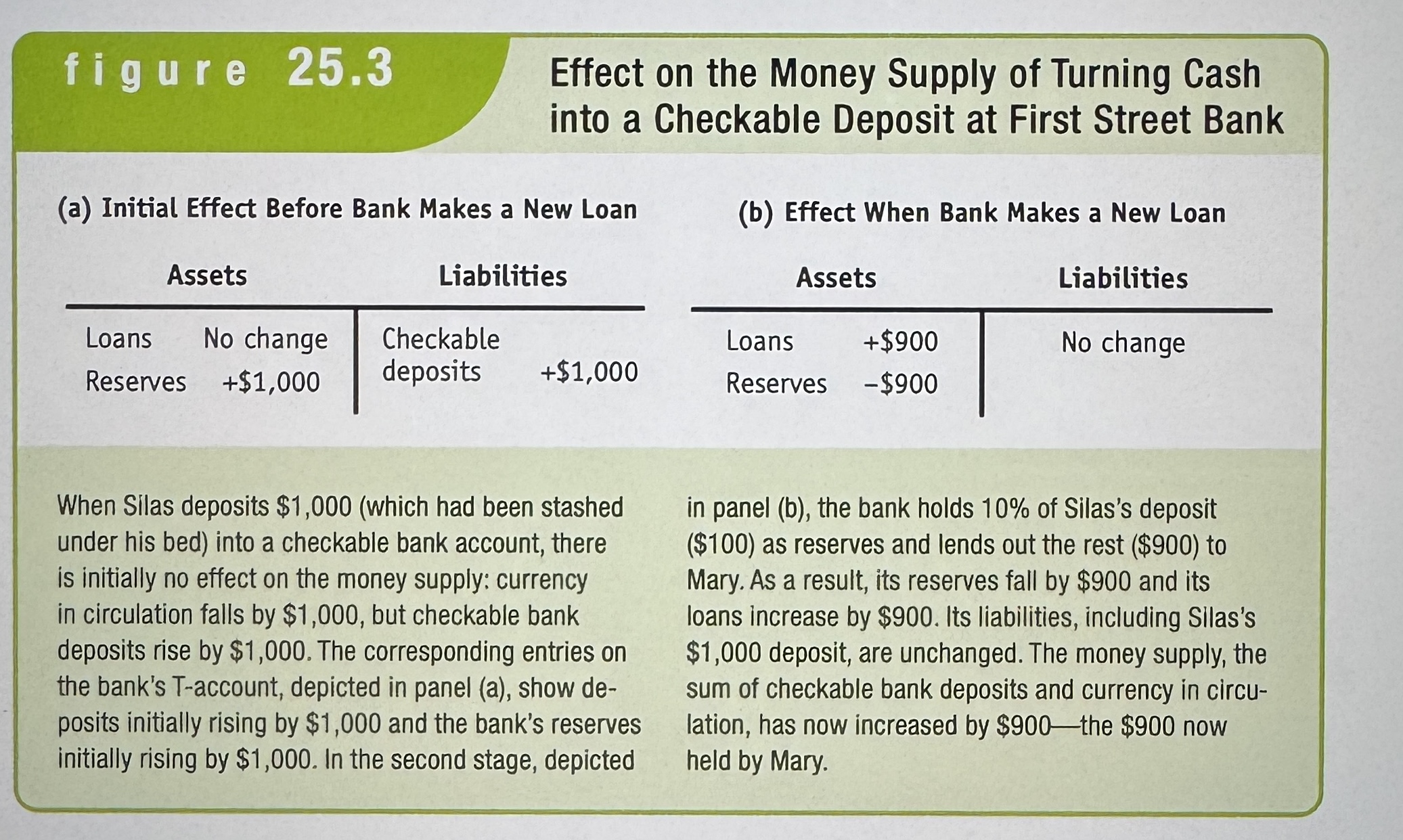

Effect on the Money Supply of Turning Cash into a Checkable Deposit at First Street Bank

Ex.

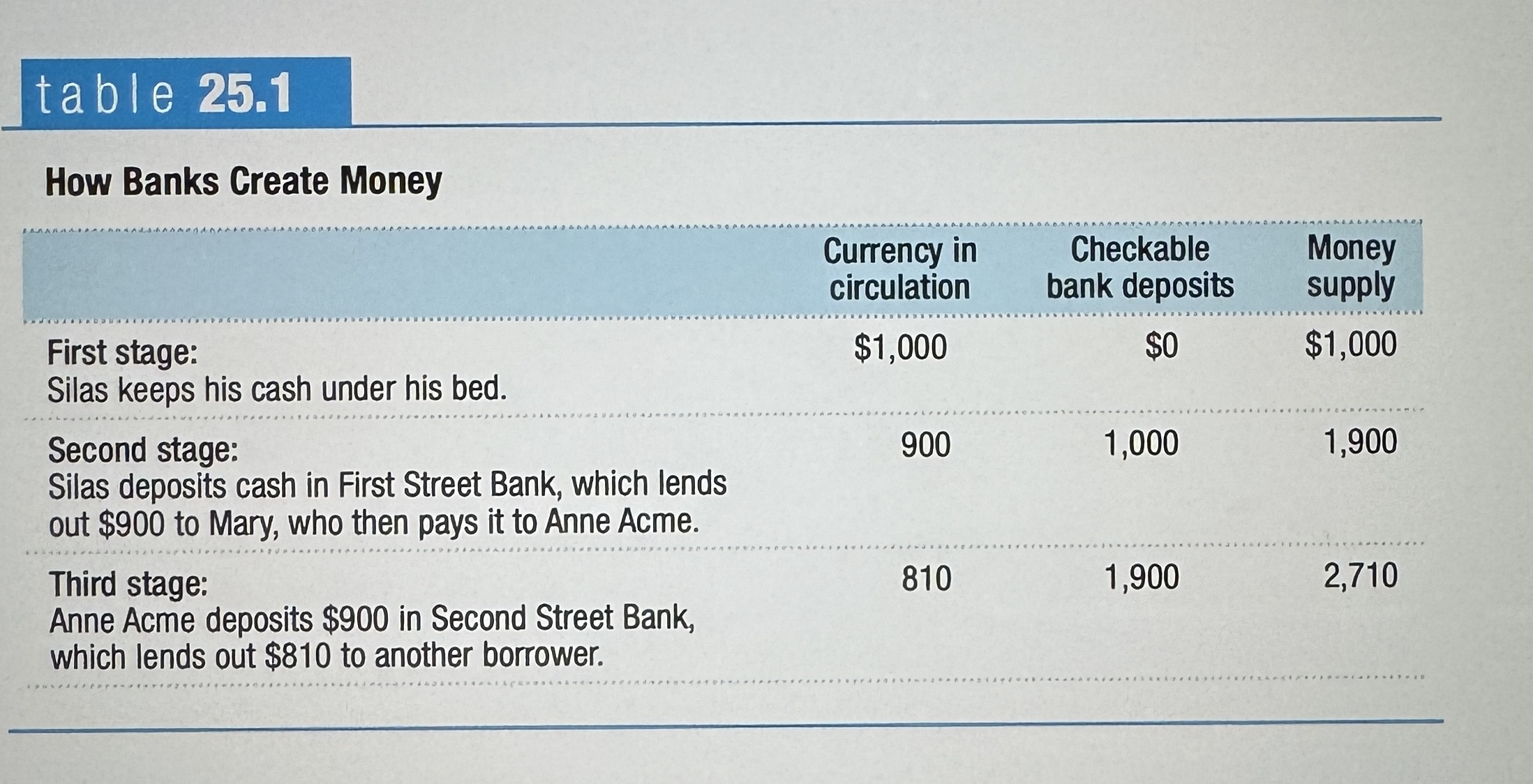

How Banks Make Money

Ex.

Excess Reserves

A banks reserves over and above its required reserves.

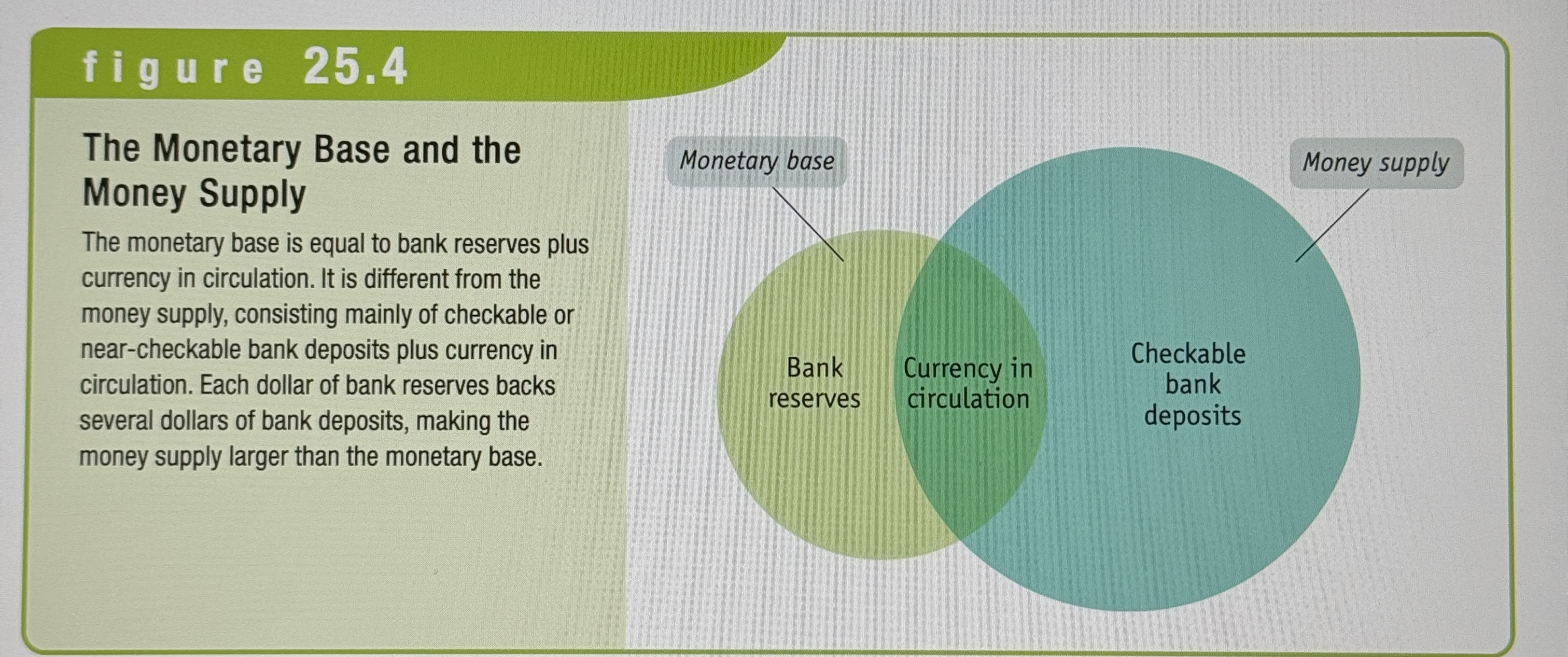

Monetary Base

The sum of currency in circulation and bank reserves.

Money Multiplier

The money multiplier is the ratio of the money supply to the monetary base. It indicates the total number of dollars created in the banking system by each one dollar addition to the monetary base.

The Monetary Base and the Money Supply

Ex.

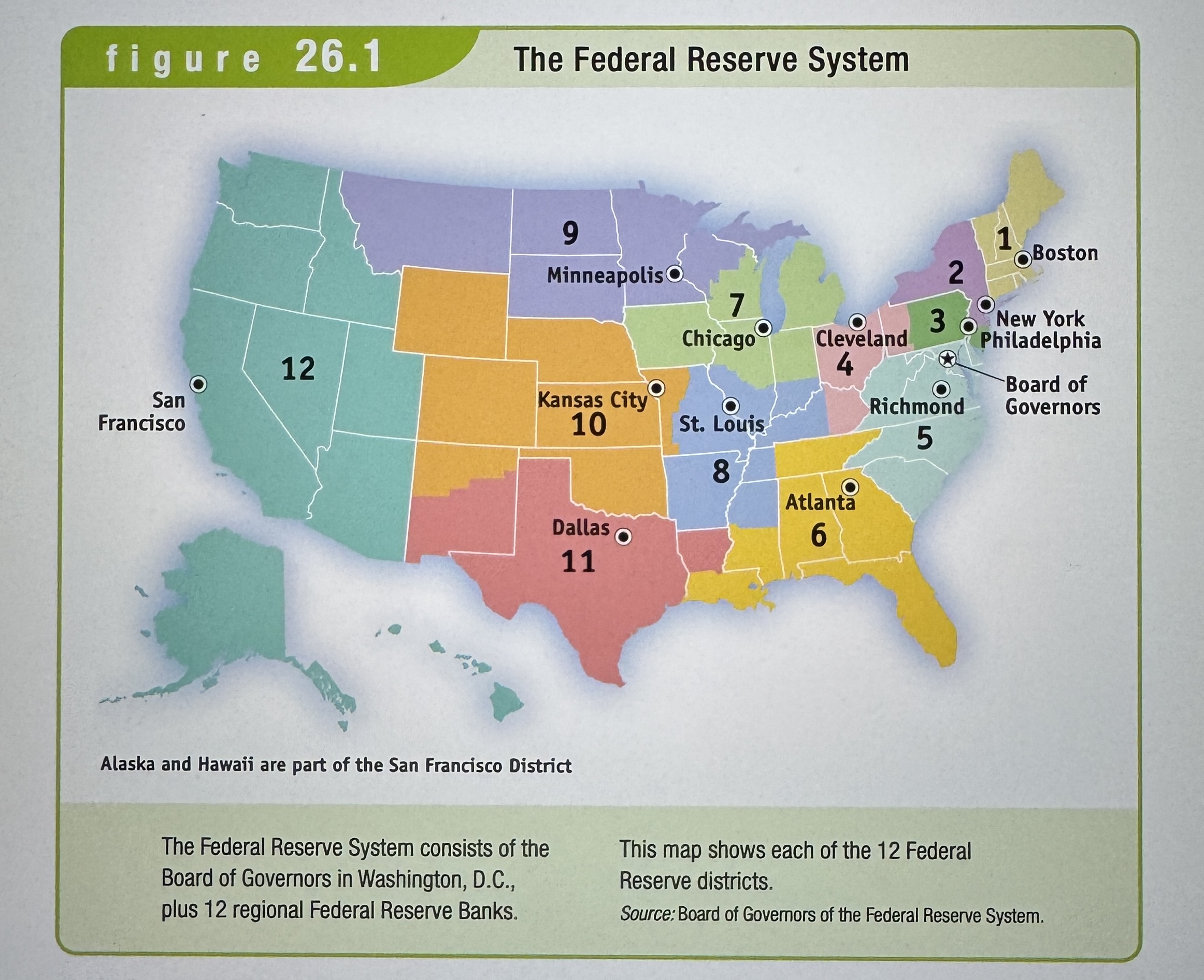

Central bank

An institution that overseas and regulates the banking system and controls the monetary base.

The Federal Reserve System

Ex.

Commercial bank

Excepts deposits and is covered by a deposit insurance.

Investment bank

trades in financial assets and is not covered by deposit insurance.

A Saving and Loan (Thrift)

Another type of deposit – taking bank, usually specialized in issuing home loans.

Leverage

A financial institution engages in leverage when it finances its investments with borrowed funds.

Balance Sheet Effect

The reduction in a firms net worth from falling asset prices.

Vicious Cycle of Deleveraging

Takes place when asset sales to cover losses produce negative balance sheet effects on other firms and forces creditors to call in their loans, forcing sales of more assets and causing further decline in asset prices.

Subprime Lending

Lending to homebuyers who don’t meet the usual criteria for being able to afford their payments.

Securitization

A pool of loans is assembled and shares of that pool are sold to investors.

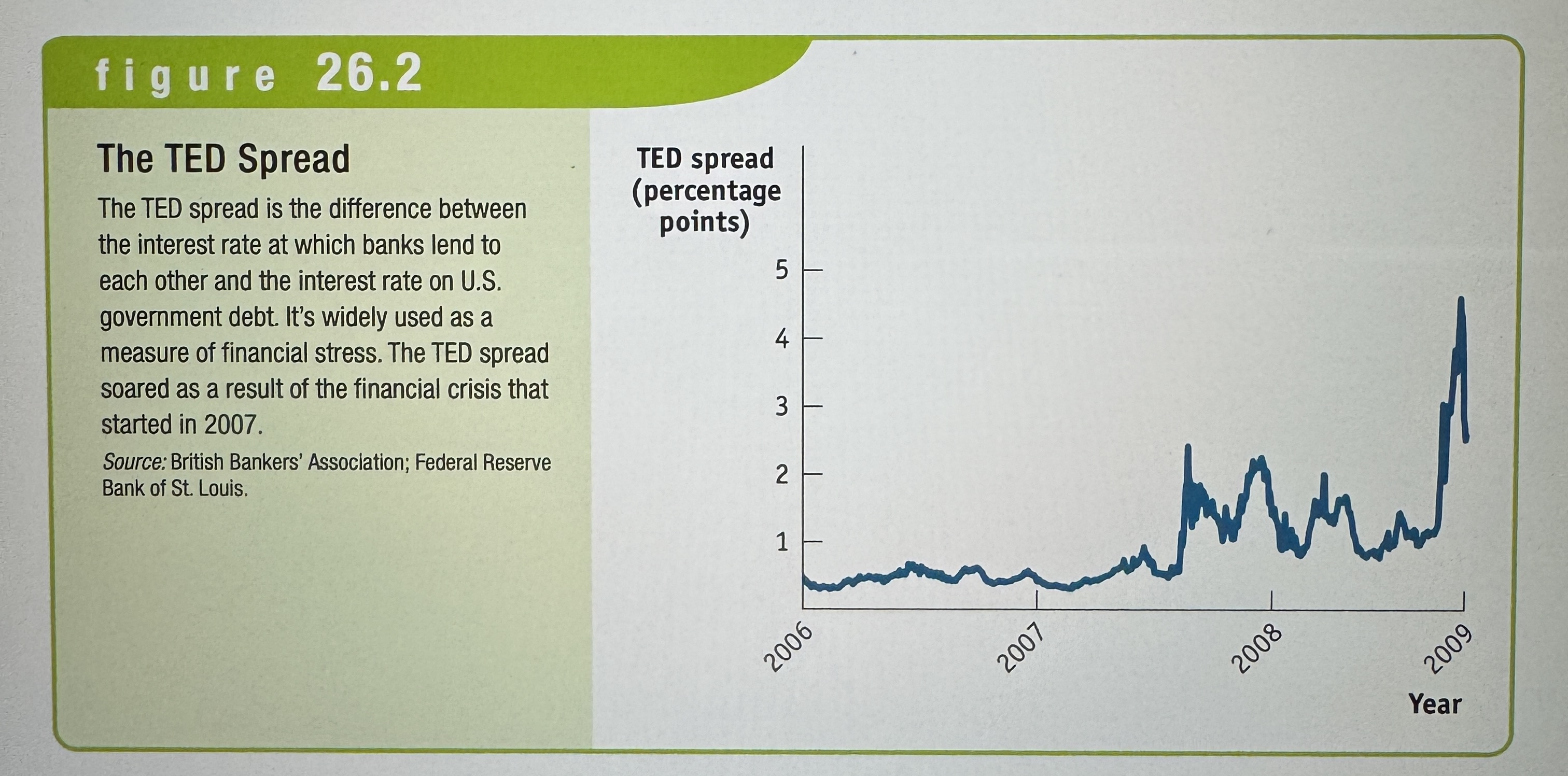

TED Spread

Ex.

The functions of the federal reserve system

It provides financial services, supervises, and regulates banking institutions, maintains the stability of the financial system, and conducts monetary policy.

Federal funds market

Allows banks that fall short of the reserve requirement to borrow funds from banks with excess reserves.

Federal funds rate

The interest rate determined in the federal funds market.

Discount rate

The interest rate the FED (Federal Reserve) charges on loans to banks.

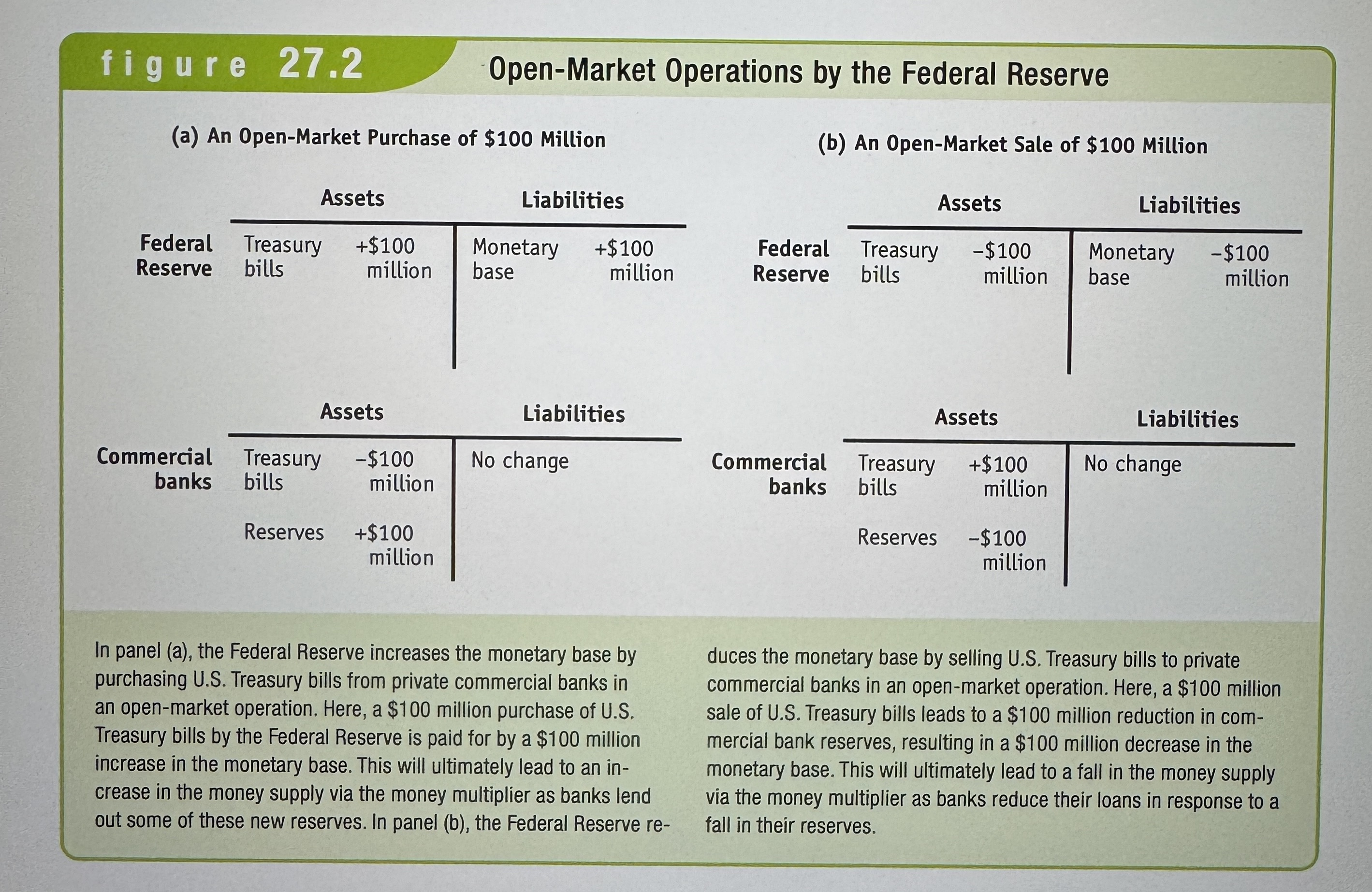

Open-Market Operations

A purchase or sale of government debt by the FED.

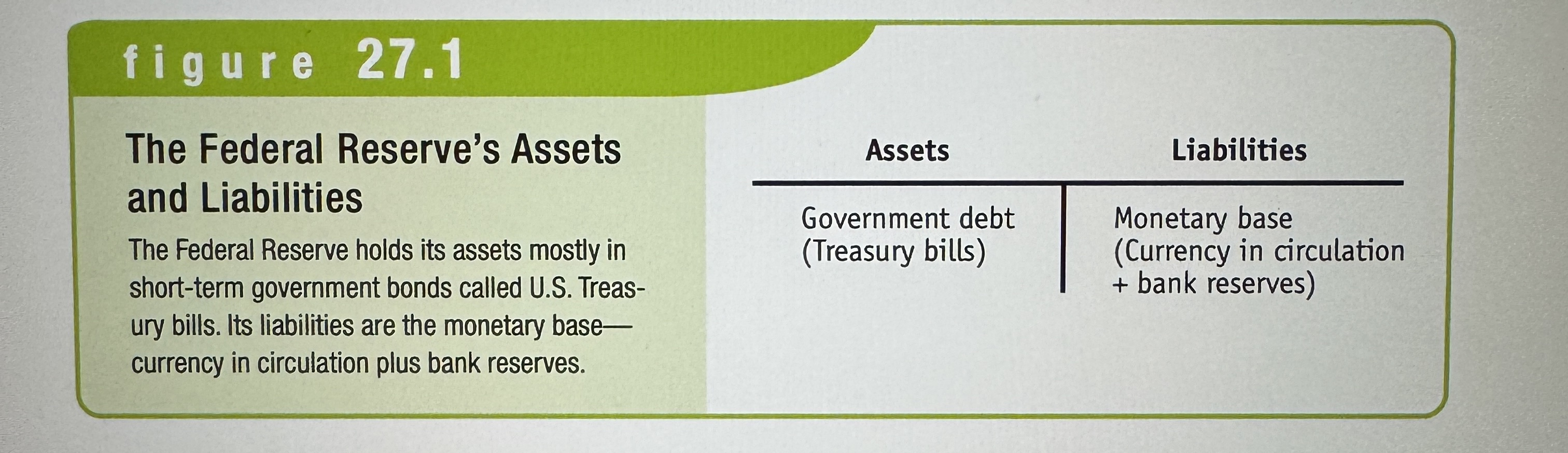

The federal reserves assets and liabilities

Ex.

Open-Market Operations by the Federal Reserve

Ex.

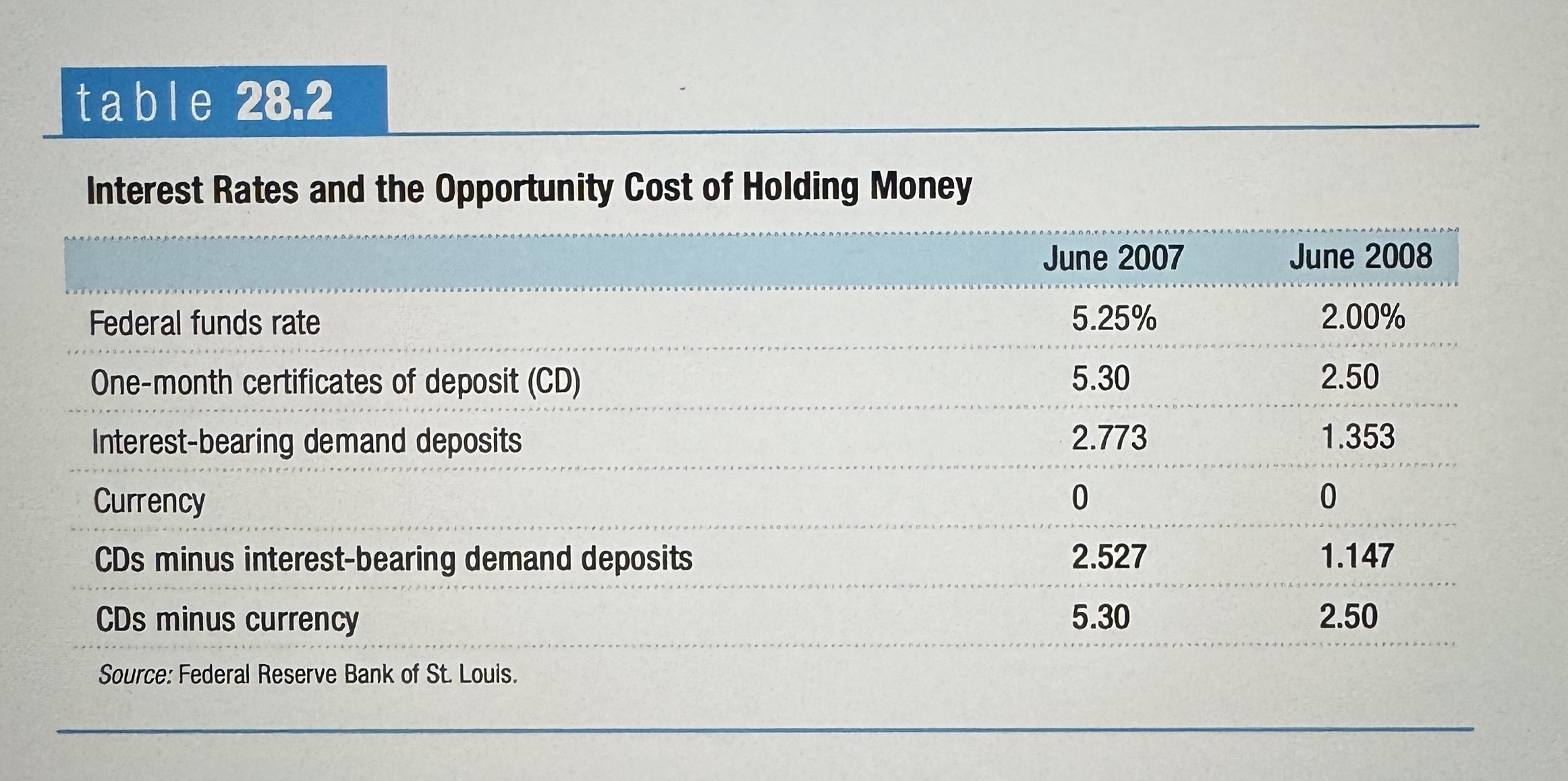

Short-term interest rates

The interest rates on financial assets that mature within less than a year.

Interest Rates and the Opportunity Cost of Holding Money

Ex.

Long-term interest Rates

Interest rates on financial assets that mature a number of years in the future.

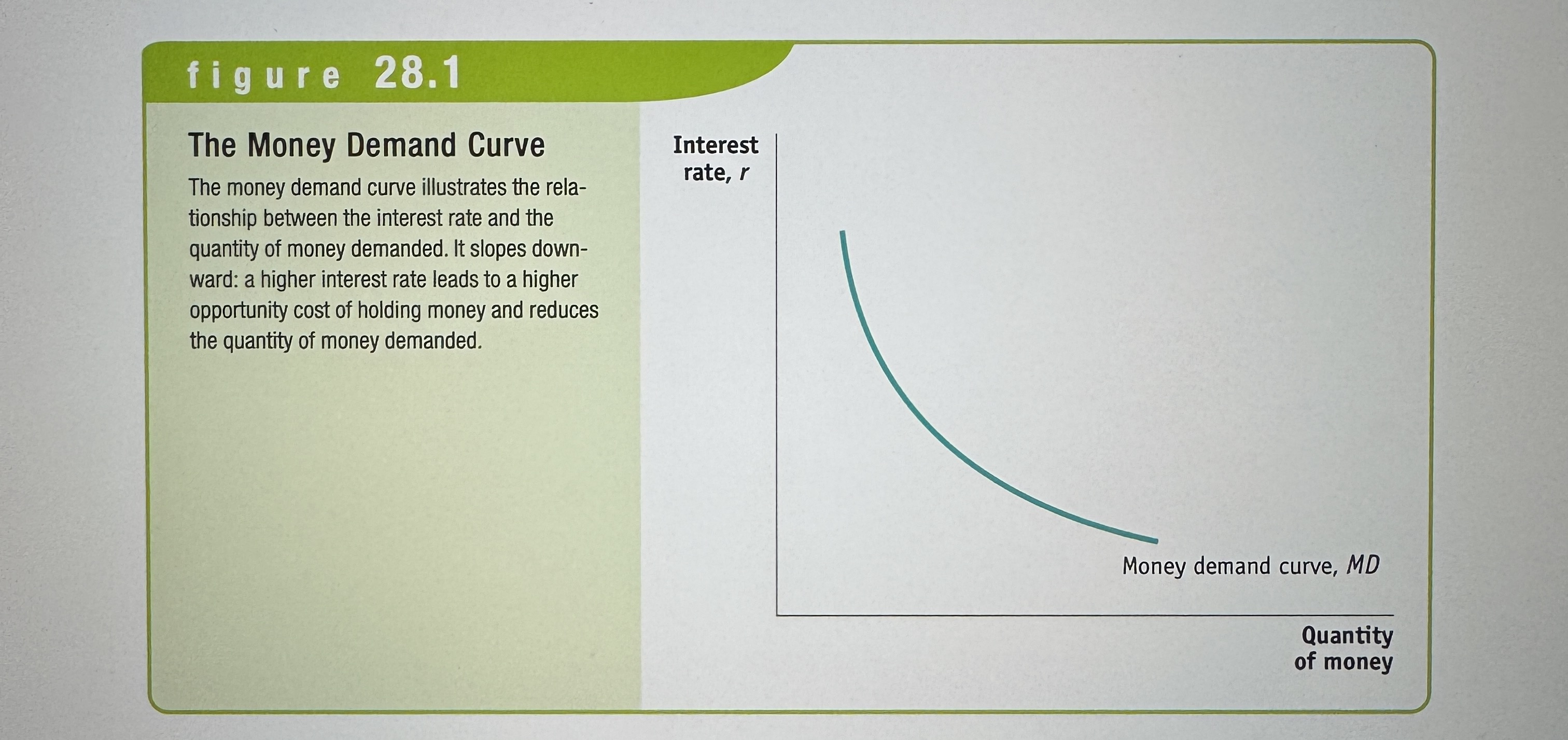

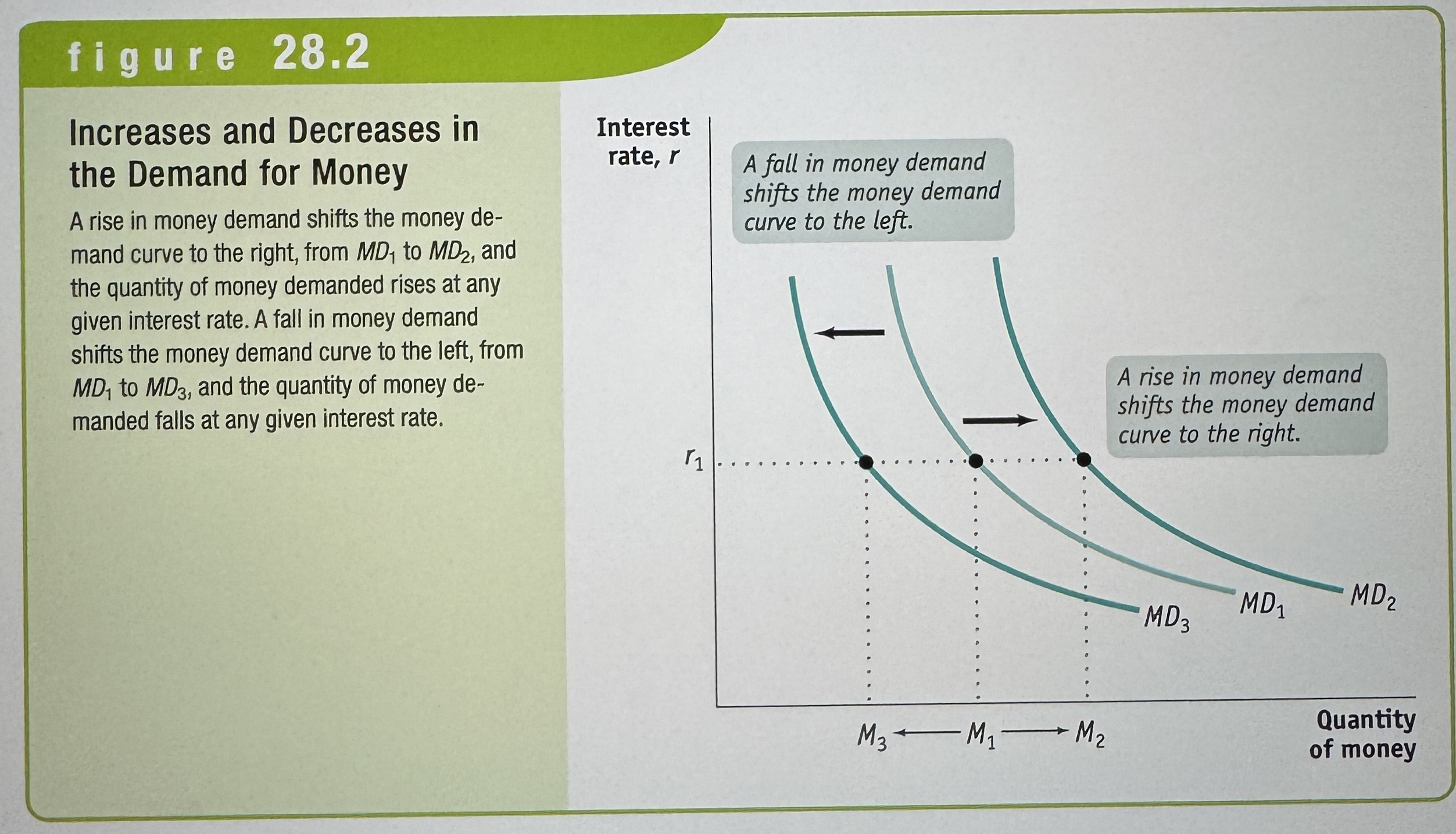

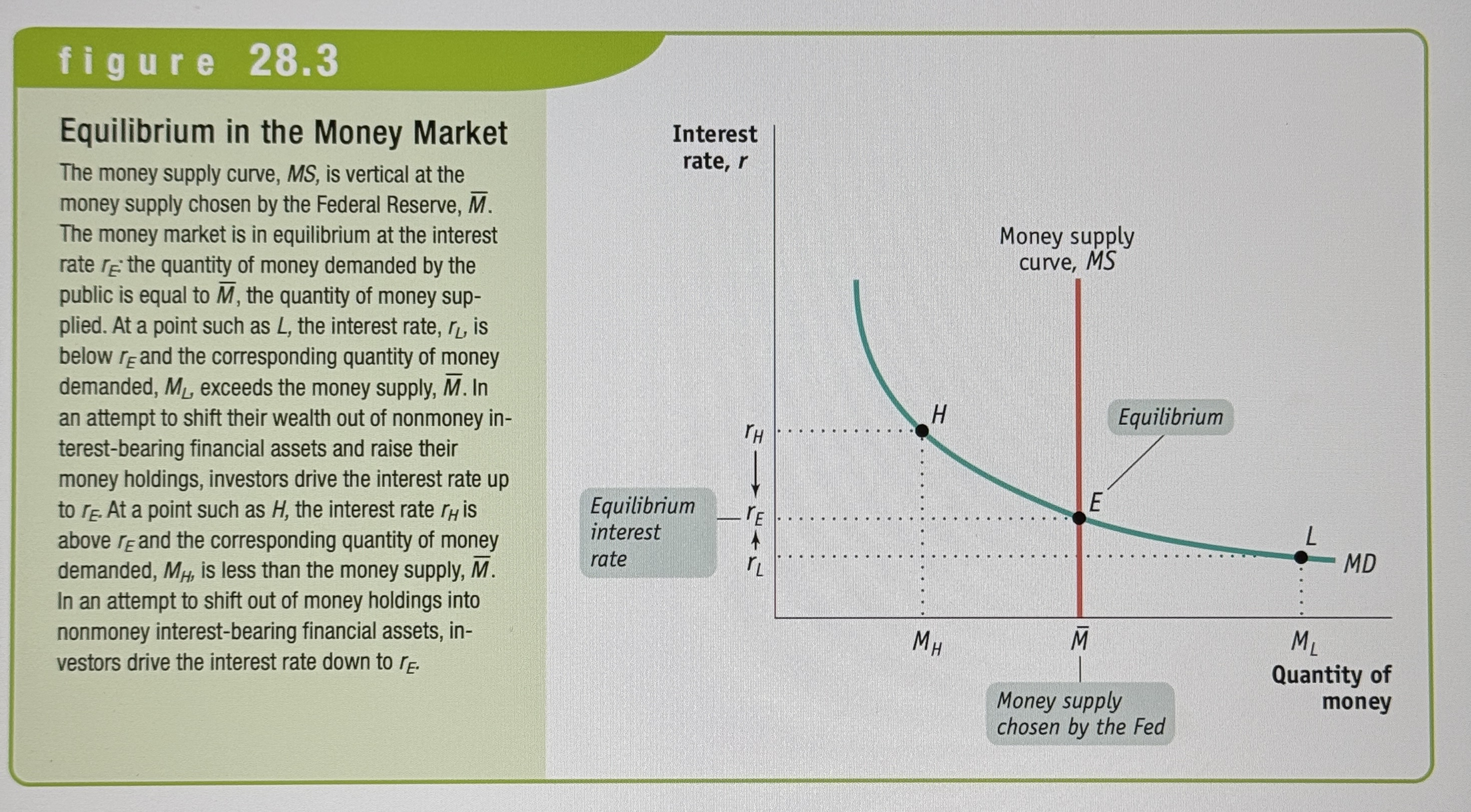

Money demand curve

Shows the relationship between the quantity of money demanded, and the interest rate.

Increases and Decreases in the Demand for Money

Ex.

What are the shifters of the money demand curve?

Changes in the aggregate price level

Changes in real GDP

Changes in technology

Changes in institutions

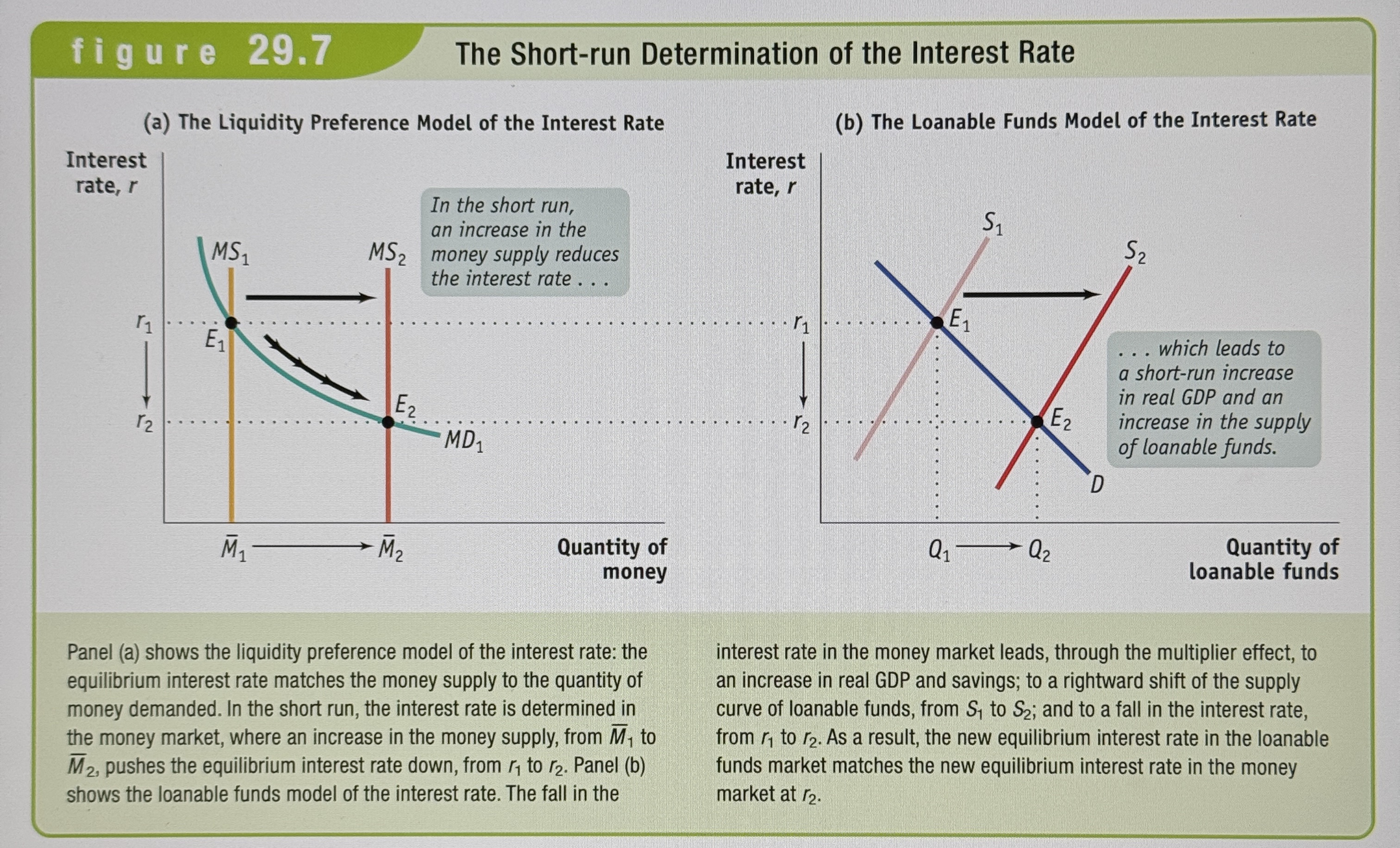

The liquidity preference model of the interest rate

Says that the interest rate is determined by the supply and demand for money.

Money Supply Curve

Shows how the quantity of money supplied varies with the interest rate.

Equilibrium in the money market

Ex.

what are the two models of the interest rate?

The liquidity preference model, and the loanable funds model.

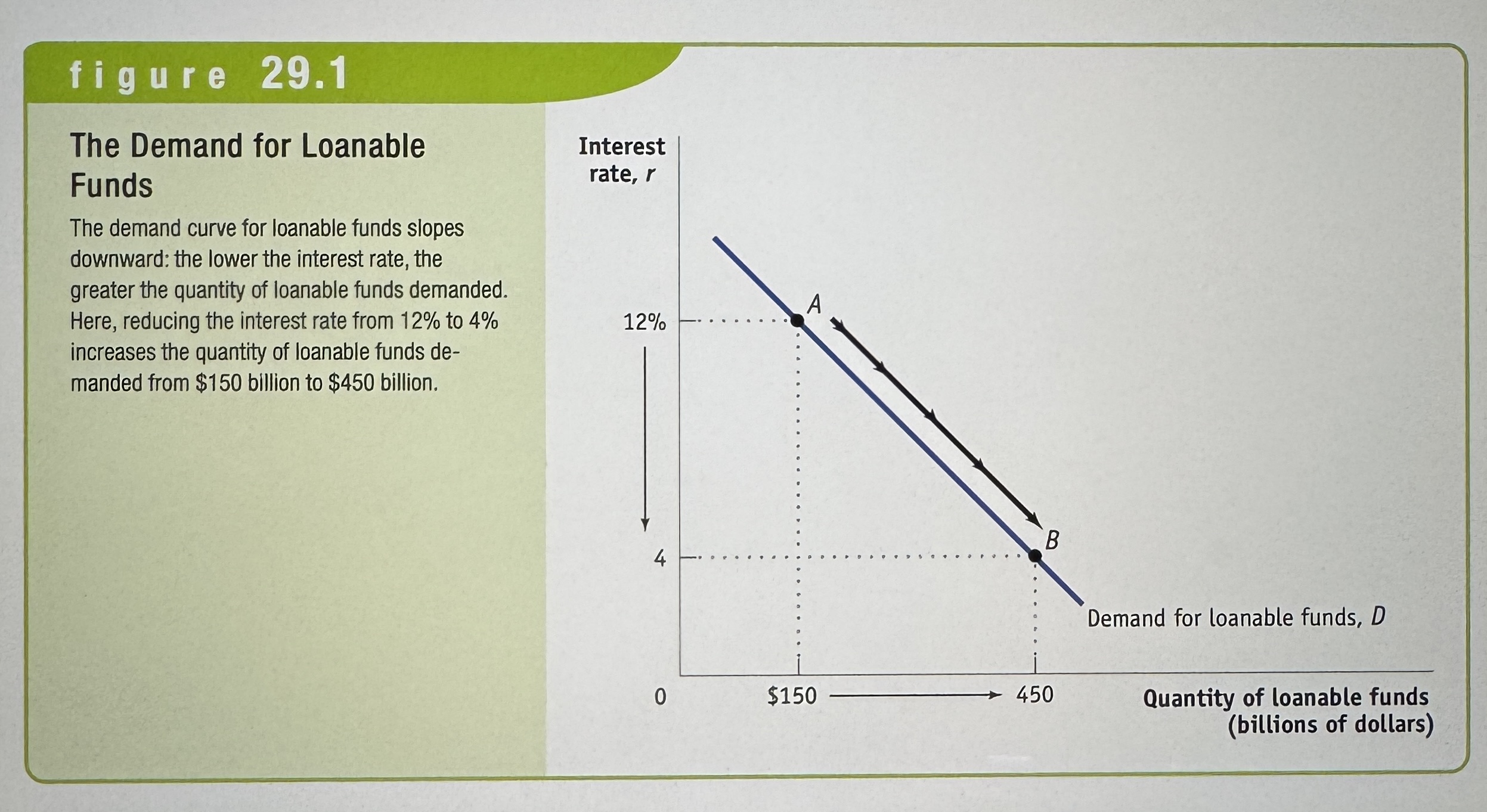

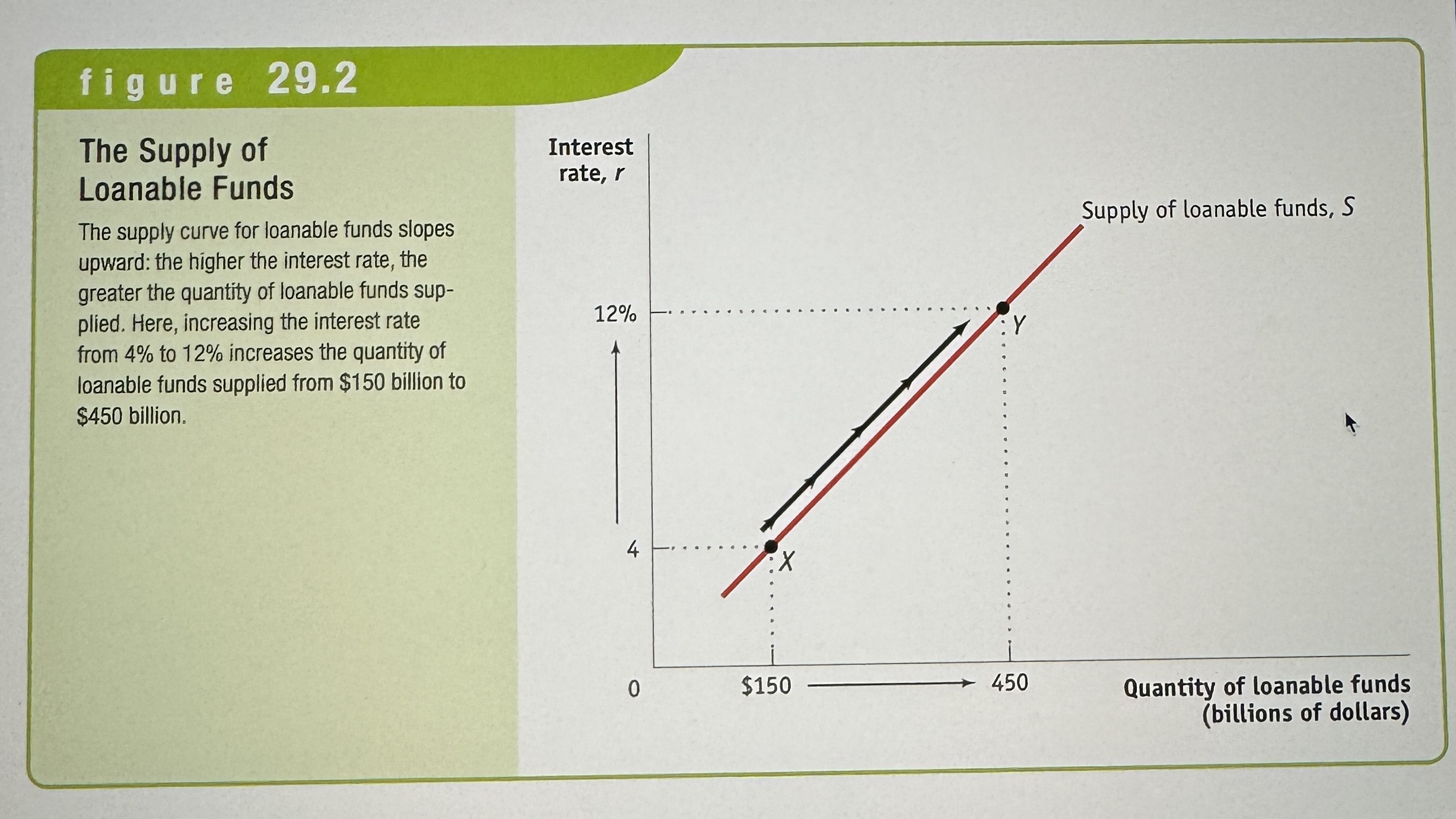

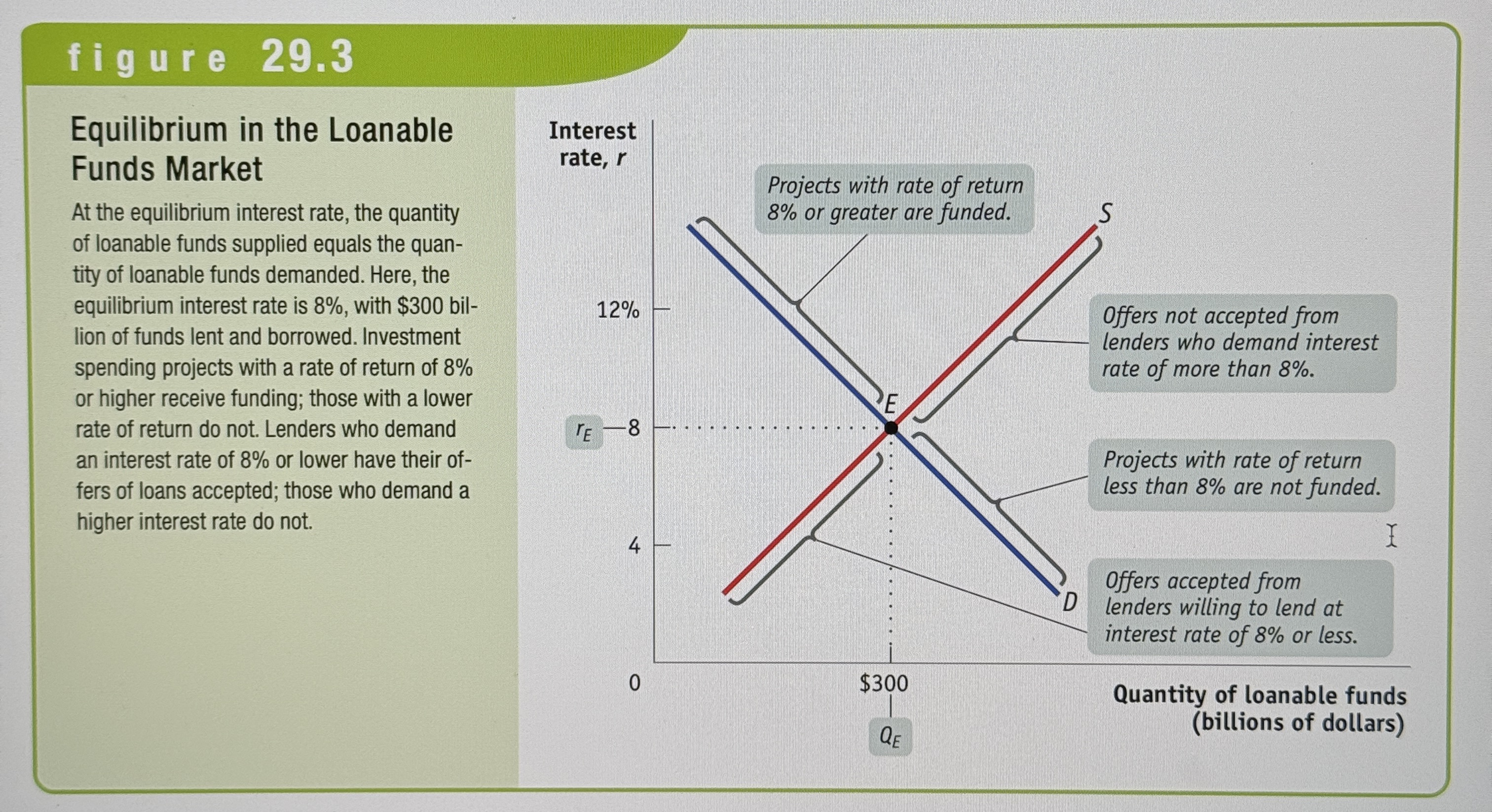

Loanable funds market

A hypothetical market that illustrates the market outcome of the demand for funds generated by borrowers and the supply of funds provided by lenders.

Rate of return

The rate of return on a project is the profit earned on the project expressed as a percentage of its cost.

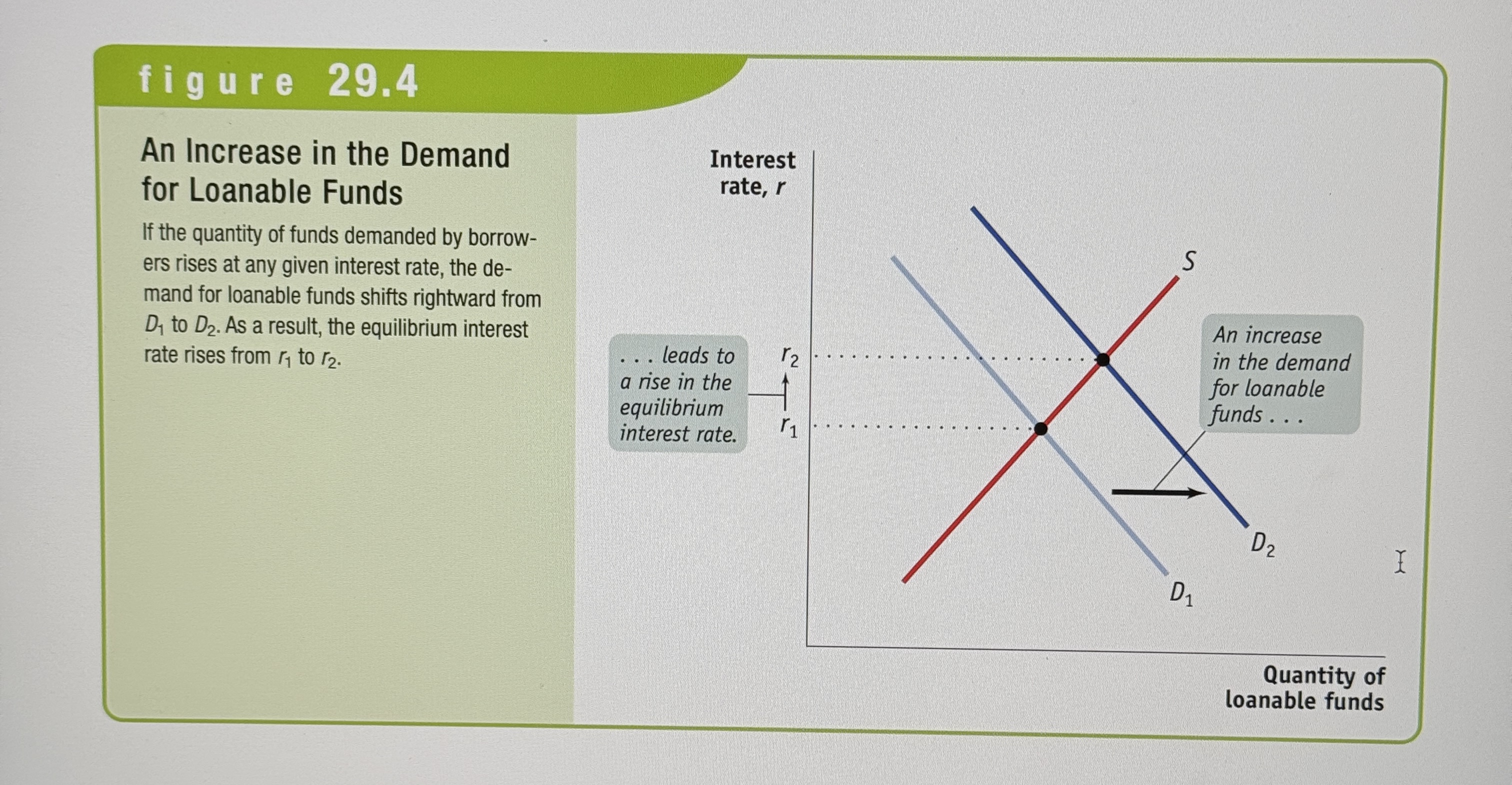

The demand for loanable funds

Ex.

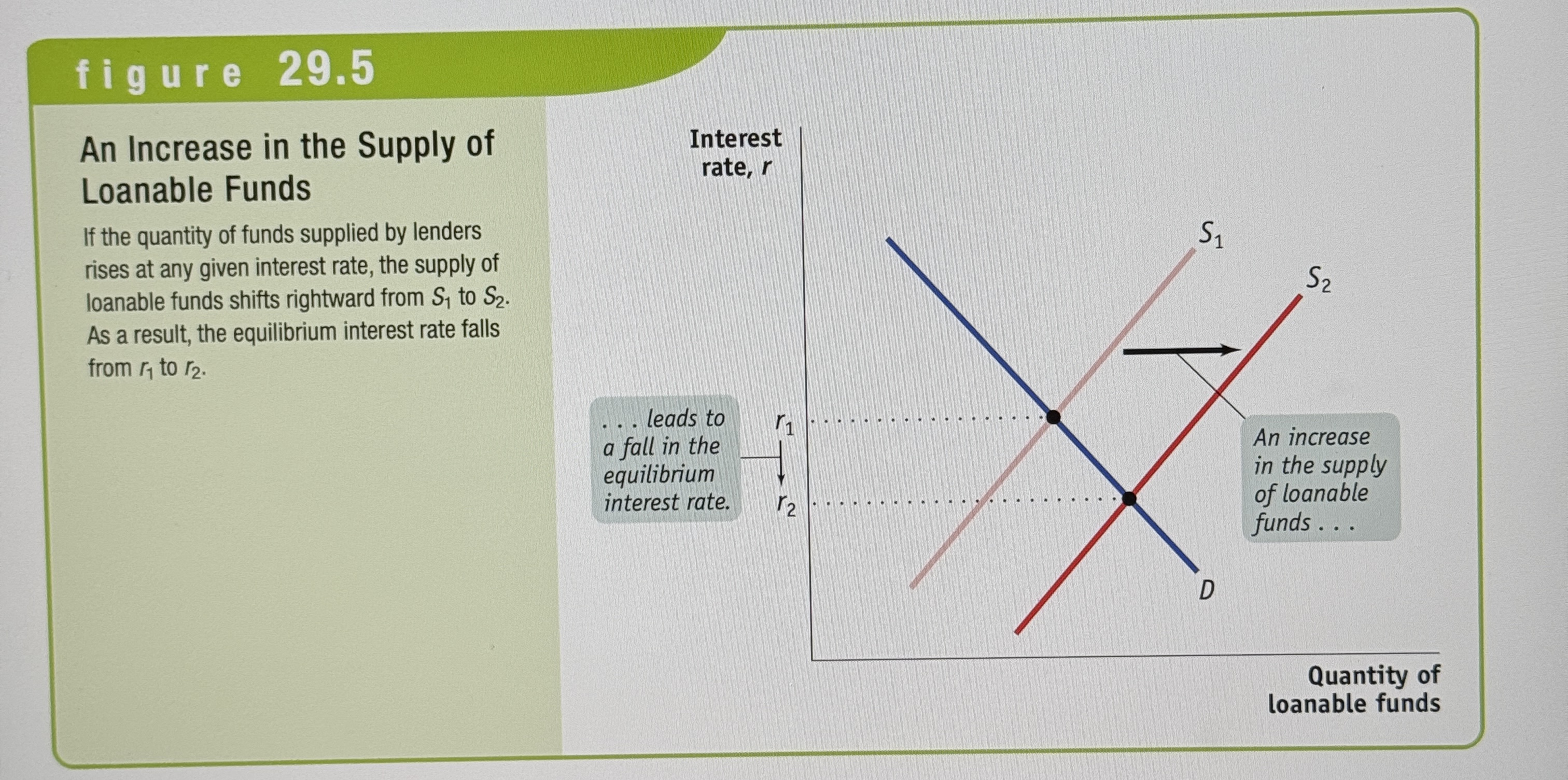

The supply of loanable funds

Ex.

Equilibrium in the Loanable Funds Market

Ex.

Shifts on the Demand for Loanable Funds

Changes in the perceived business opportunities and changes in the government’s borrowing.

Shifts on the Supply for Loanable Funds

Changes in private savings behavior and changes in capital inflows.

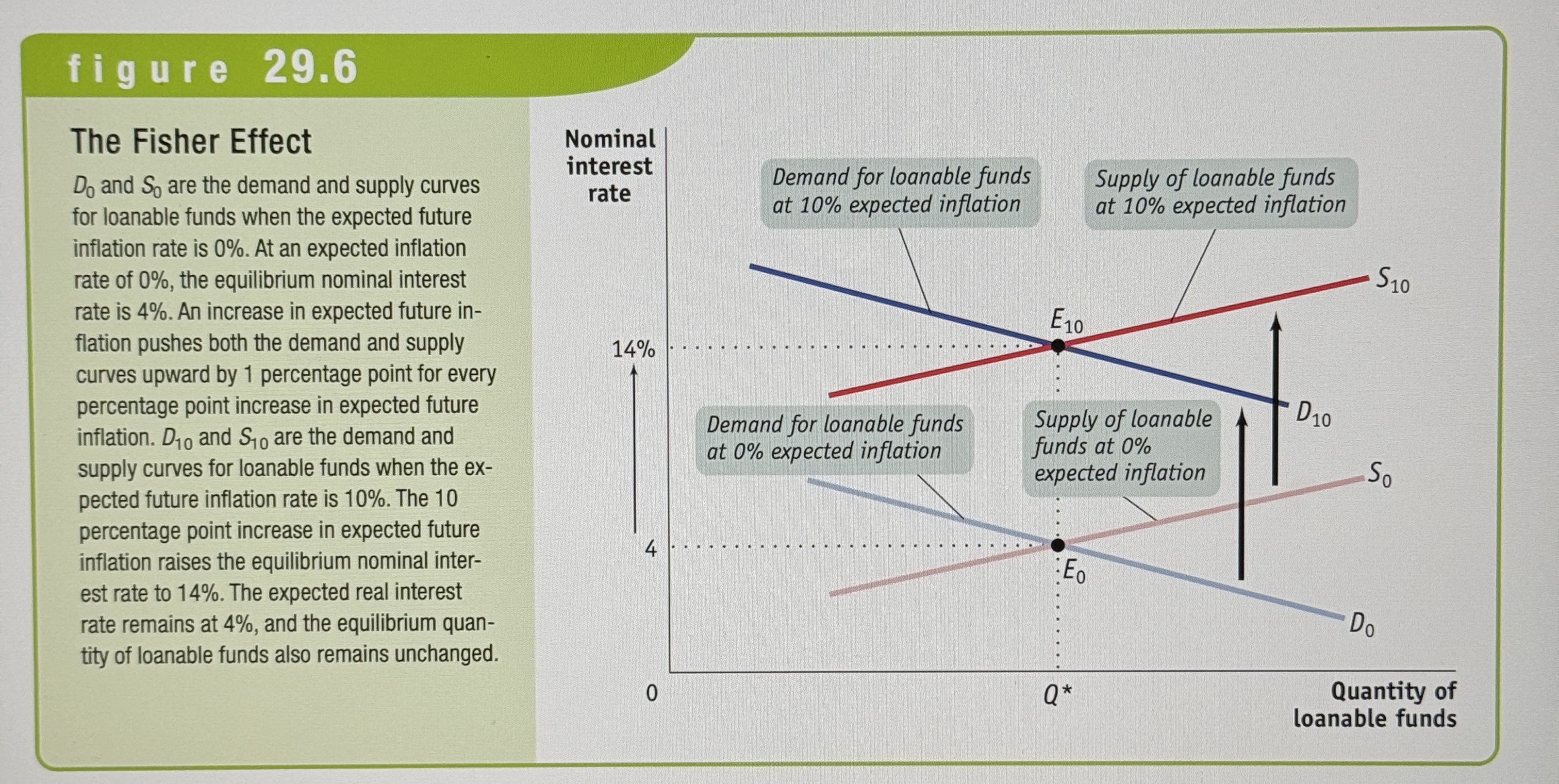

Real Interest Rate

Real Interest Rate = Nominal Interest Rate - Inflation Rate

Fisher Effect

An increase in expected future inflation drives up the nominal interest rate, leaving the expected real interest rate unchanged.

The Short-run Determination of the Interest Rate

Ex.

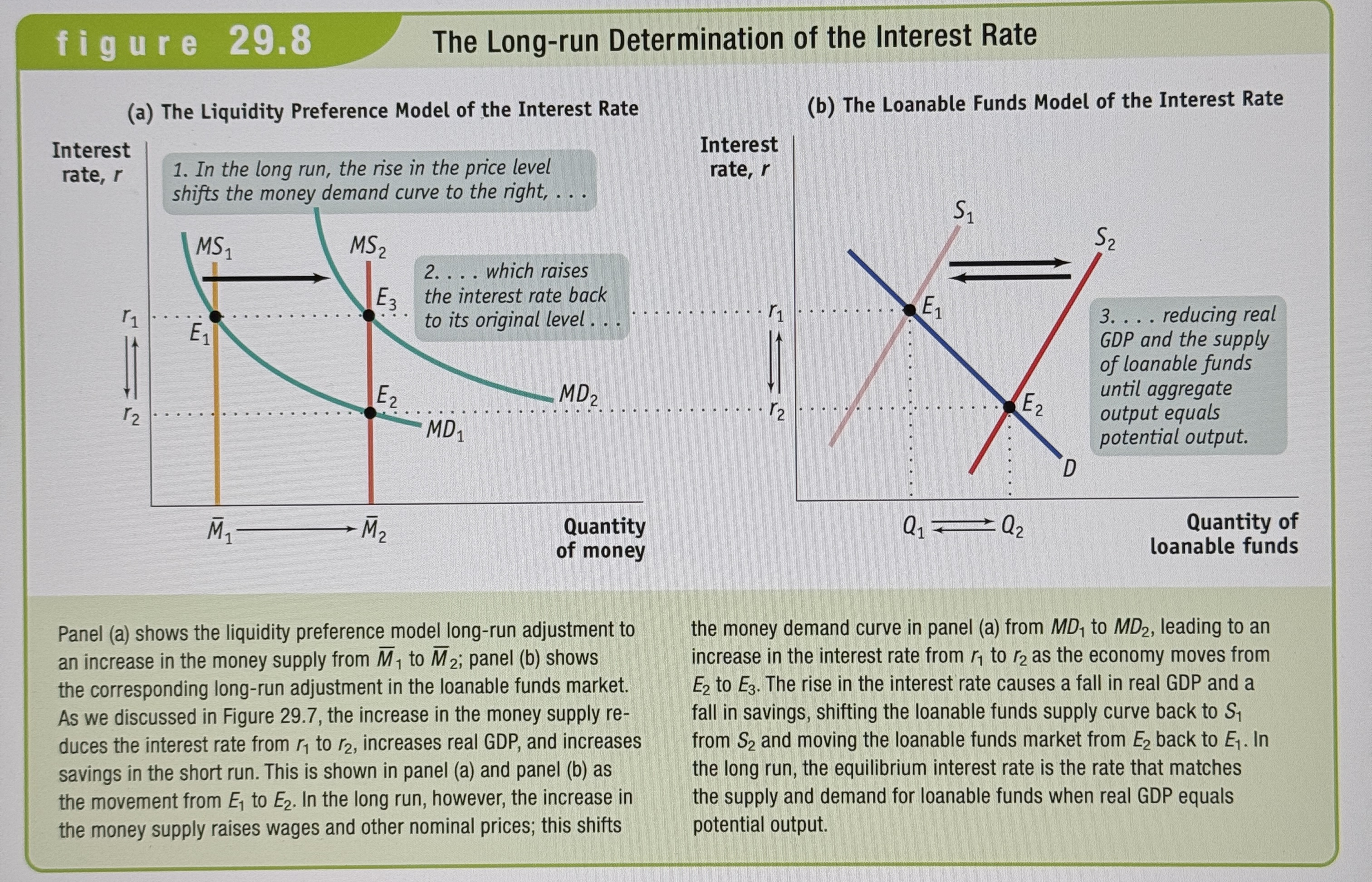

The Long-run Determination of the Interest Rate

Ex.

Summary #1

Investment in physical capital is necessary for long-run economic growth. So in order for an economy to grow, it must channel savings into investment spending

Summary #2

According to the savings-investment spending identity, savings and investment spending are always equal for the economy as a whole. The government is a source of savings when it runs a positive budget balance, also known as a budget surplus; it is a source of dissavings when it runs a negative budget balance, also known as a budget deficit. In a closed economy, savings is equal to national savings, the sum of private savings plus the budget balance. In an open economy, savings is equal to national savings plus capital inflow of foreign savings. When a capital outflow, or negative capital inflow, occurs, some portion of national savings is funding investment spending in other countries.

Summary #3

Households invest their current savings or wealth their accumulated savings-by purchasing assets. Assets come in the form of either a financial asset, a paper claim that entitles the buyer to future income from the seller, or a physical asset, a claim on a tangible object that gives the owner the right to dispose of it as desired.

A financial asset is also a liability from the point of view of its seller. There are four main types of financial assets: loans, bonds, stocks, and bank deposits. Each of them serves a different purpose in addressing the three fundamental tasks of a financial system: reducing transaction costs-the cost of making a deal; reducing financial risk-uncertainty about future outcomes that involves financial gains and losses; and providing liquid assets-assets that can be quickly converted into cash without much loss of value (in contrast to illiquid assets, which are not easily converted).

Summary #4

Although many small and moderate-size borrowers use bank loans to fund investment spending, larger companies typically issue bonds. Bonds with a higher risk of default must typically pay a higher interest rate. Business owners reduce their risk by selling stock. Although stocks usually generate a higher return than bonds, investors typically wish to reduce their risk by engaging in diversification, owning a wide range of assets whose returns are based on unrelated, or independent, events.

Most people are risk-averse, viewing the loss of a given amount of money as a significant hardship but viewing the gain of an equal amount of money as a much less significant benefit. Loan-backed securities, a recent innovation, are assets created by pooling individual loans and selling shares of that pool to investors. Because they are more diversified and more liquid than individual loans, trading on financial markets like bonds,they are preferred by investors. It can be difficult, however, to assess their quality.

Summary #5

Financial intermediaries- institutions such as mutual funds, pension funds, life insurance companies, and banks-are critical components of the financial system.

Mutual funds and pension funds allow small investors to diversify and life insurance companies allow families to reduce risk.