Lecture 12 - Inventories and Biological assets

1/63

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

64 Terms

What is the objective of IAS 2?

Accounting treatment measurement and cost recognition of inventory

What does IAS 2 focus on?

Determine cost and when to recognise expense

What is inventory?

Assets held for sale

What else is included in inventory?

Work in progress for sale

What else counts as inventory?

Materials and supplies used in production or services

What must be confirmed in inventory valuation?

Physical existence and ownership

What must be determined in valuation?

Unit cost of inventory items

What may be required after valuation?

Write down to net realisable value (NRV)

What does inventory cost include?

Purchase costs conversion costs and other related costs

What must costs relate to?

Bringing inventory to present location and condition

Give examples of purchase costs?

Price import duties transport

Give examples of conversion costs?

Labour and overheads

How is inventory cost measured?

Specific identification or cost formulas

What does specific identification involve?

Tracking actual cost of each individual item

What cost formulas are allowed?

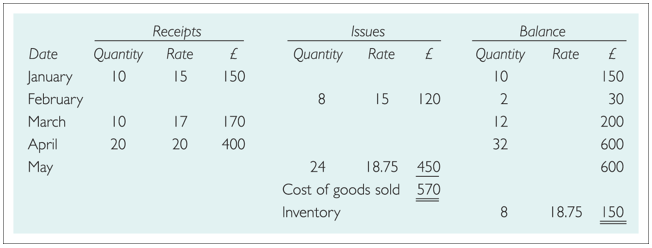

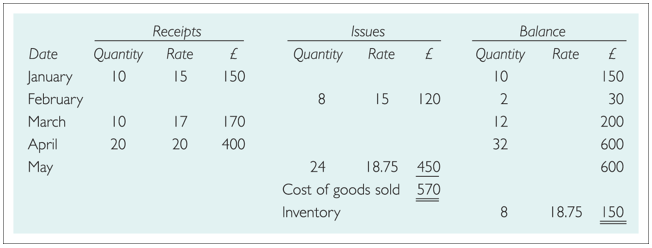

FIFO and weighted average

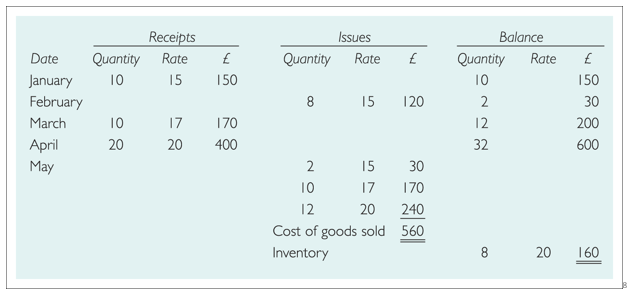

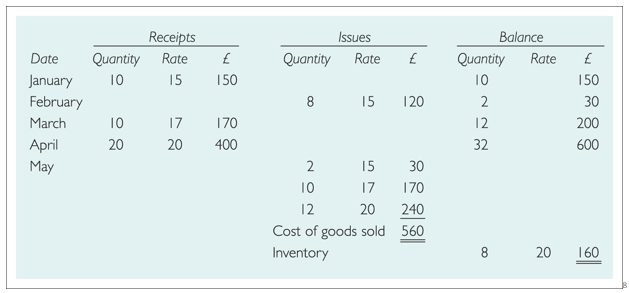

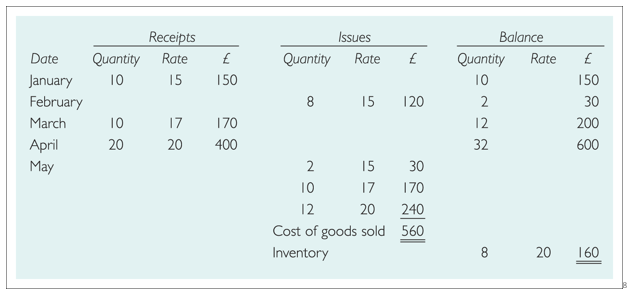

What is FIFO?

First-in, first-out

What does FIFO assume?

Earliest items purchased are sold first

What remains in closing inventory under FIFO?

Most recently purchased items

What effect in rising prices?

Higher profit lower cost of sales

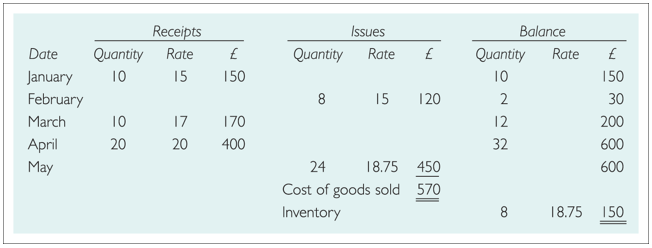

What does weighted average method (AVCO) do?

Calculates average cost per unit after each purchase

When is a new average calculated?

After each purchase

What cost is used for closing inventory?

Most recent weighted average cost

Is LIFO allowed under IAS 2?

No - it is prohibited

What is LIFO?

Last-in, first out

Why is LIFO rejected?

Uses outdated costs not realistic

What effect can LIFO have on profit?

Lower reported profit and lower tax

Why is closing inventory valuation important?

It affects profit and financial position

What risk arises from valuation methods?

Profit smoothing

(Adjusting inventory to stabilise profit)

How can it be manipulated?

Over/under valuation

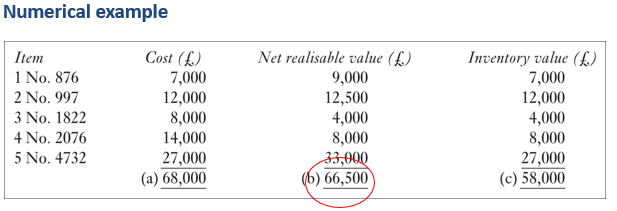

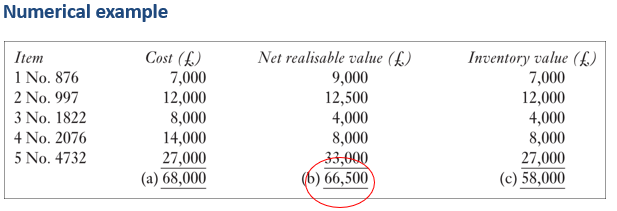

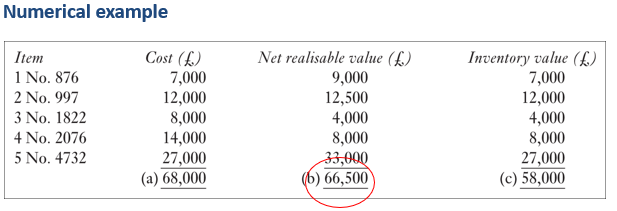

What is the NRV rule?

Inventory measured at lower of cost and NRV

What is NRV?

Selling price minus completion and selling costs

What costs are deducted in NRV?

Costs to complete and sell inventory

Why apply NRV rule?

Avoid overstating assets

What manipulation can occur at year-end?

Cut-off errors and timing issues

What can be suppressed?

Invoices not recorded

How can NRV be manipulated?

Using subjective estimates

What can be manipulated in low profit periods?

Overhead allocation to inventory

What risk exists with obsolescence?

Overestimating inventory usefulness

What may be inaccurate?

Physical inventory count

What do auditors verify?

Existence of inventory

What else do auditors verify?

Ownership of inventory

What else do auditors assess?

Condition of inventory items

What must be disclosed about inventory?

Accounting policies

What must be disclosed about cost?

Carrying amount

What must be disclosed about expenses?

Inventory expense

What must be disclosed about NRV?

Write-downs and reversals

What is IAS 41 about?

Accounting for agricultural activity

What is agricultural activity?

Transformation of living assets into produce

What is a biological asset?

Living plant or animal

What is agricultural produce?

Harvested output from biological asset

How are biological assets measured?

Fair value less costs to sell

Why not cost-based measurement?

Assets grow and change continuously

When is a biological asset recognised?

Control probable benefits reliable measurement

What must be probable?

Future economic benefits

What must be measurable (and reliable)?

Fair value or cost

What standard applies before harvest?

IAS 41

What standard applies after harvest?

IAS 2

What happens at harvest?

Becomes inventory

What must be recognised each period?

Gain or loss from fair value changes

Why is this important?

Impacts profit directly

What causes price changes?

Market price movements

What causes physical changes?

Growth ageing or production

What else increases value?

Birth of new assets

Why is IAS 41 important?

Fair value changes affect profit