Microeconomics Unit 2-3

1/51

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

52 Terms

Accounting Profit

The difference between total revenues and explicit costs only (Net Income)

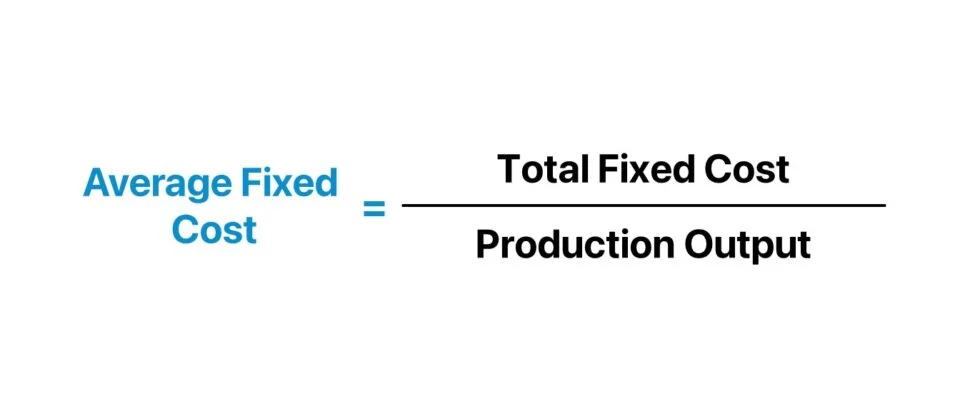

Average Fixed Cost

A firm's total fixed cost divided by total output (Cost that does not change with the change in the number of goods and services produced)

Average Fixed Cost (Formula)

Average Product

Total product divided by the variable input used in production (Average outputs produced by each input)

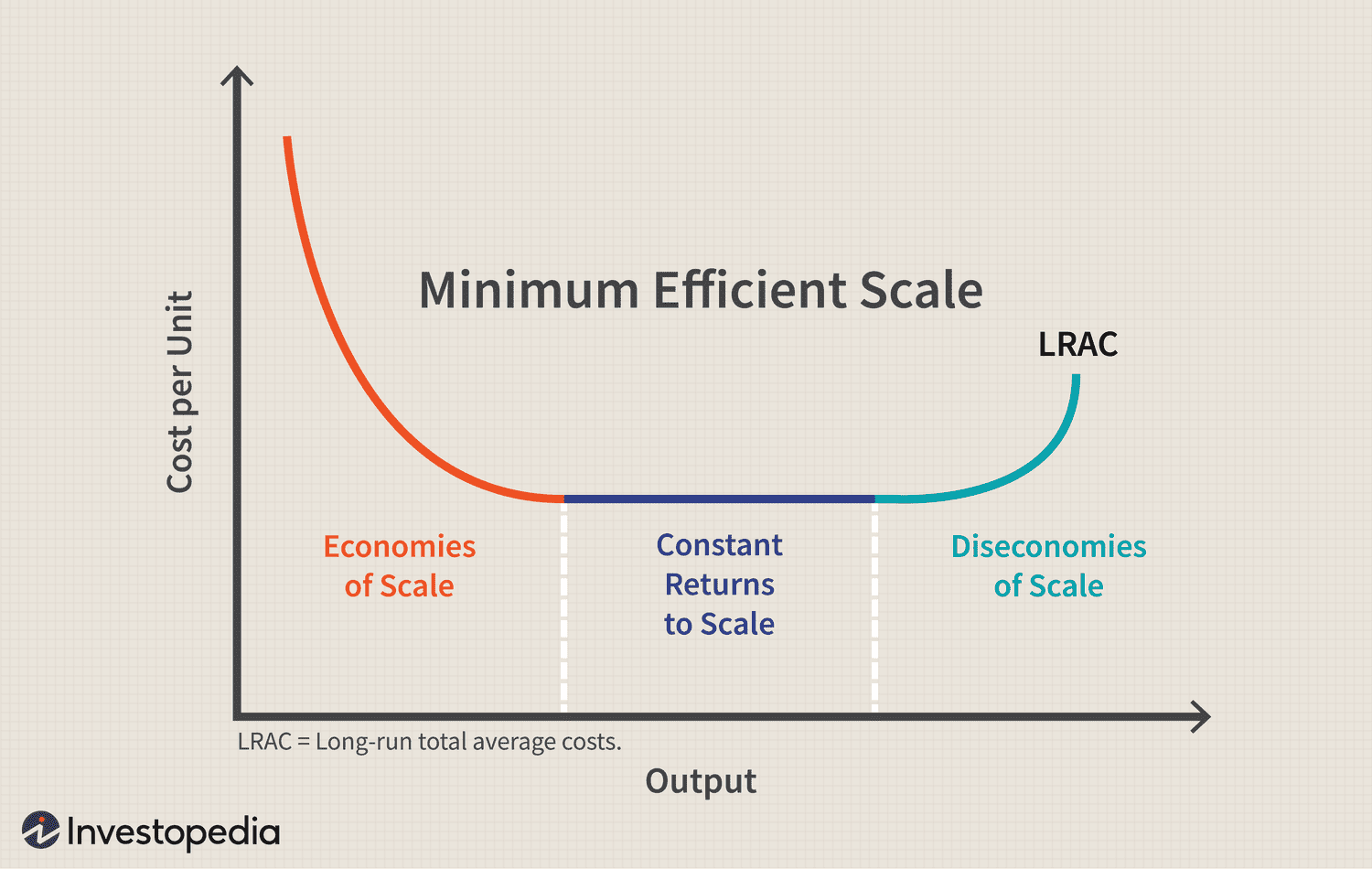

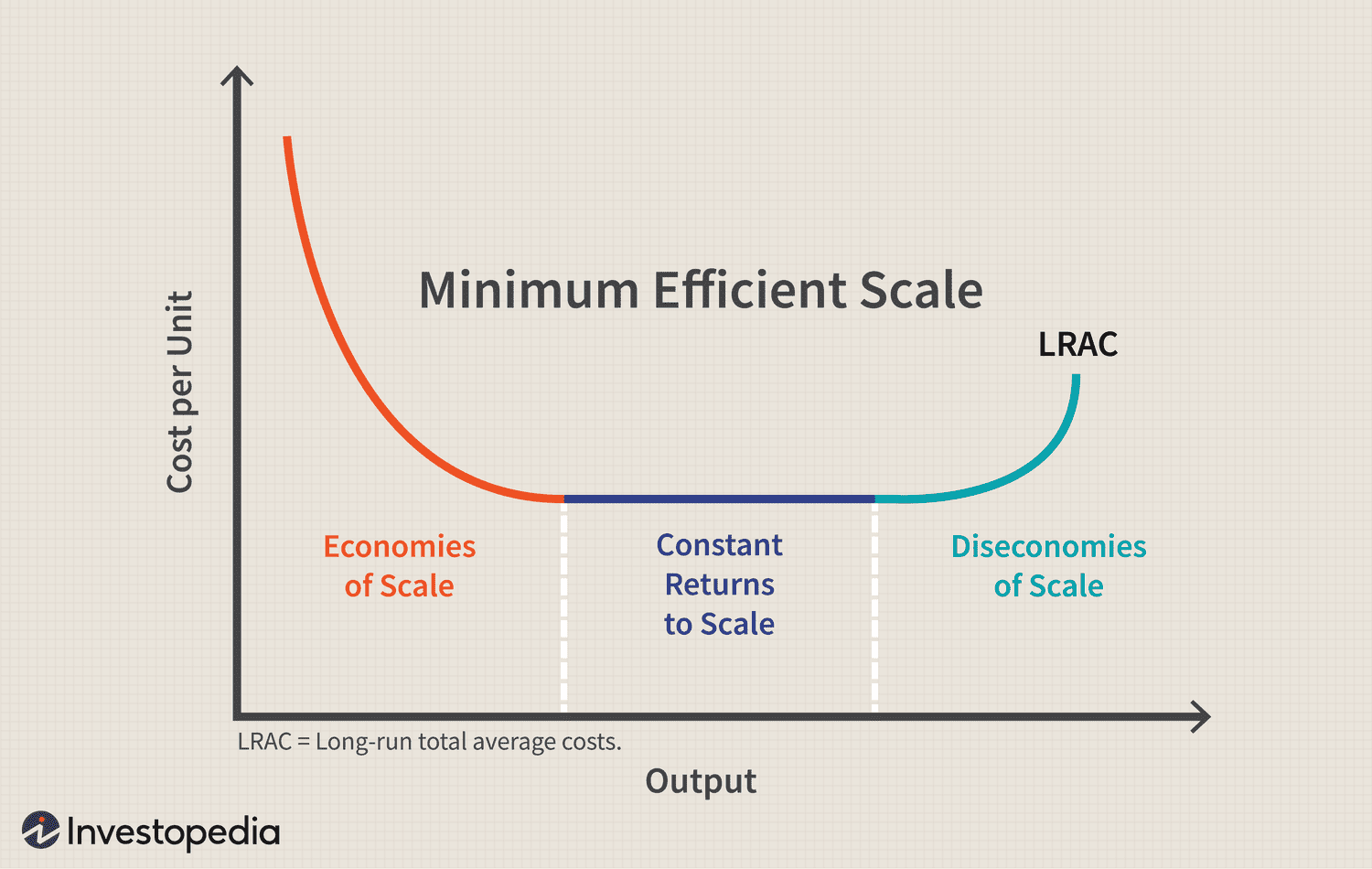

Diseconomies of Scale

As a firm's output increases, its LRATC curve increases. (When a company or business grows so large that the costs per unit increase)

LRATC

Long-Run Average Total Cost

Economies of Scale

The cost advantages companies gain from increasing their output

Economic Profit

Total revenues subtracted by both explicit and implicit costs; this is the type of profit referred to in Economics (Net Profit)

Excise Tax

A per-unit tax placed on the sales of a specific product

Fixed Costs

These costs do not change when quantity changes in the short run, but can change in the long run (costs that are independent of volume)

Law of Diminishing Marginal Returns

The range of output over which smaller and smaller additional units of output are produced as successive equal increments of variable input are added to fixed quantities of other inputs in the short run. (Simplify This)

Long Run

Period of time over which supply can fully adjust to changes in demand (in the long run)

Lump-Sum Tax

A fixed tax on producers regardless of the amount produced [affects average fixed cost and average total cost]

Marginal Cost

What is costs to produce an additional unit of output

Marginal Product

How much additional output is produced when an input is added by a firm

Normal Profit

Zero economic profit [where an entrepreneur will not be better off in any other venture] (Company's total costs are equal to its total revenue)

Per-Unit Tax

A tax on each additional unit produced [affects variable costs: marginal cost, average total cost, and average variable cost]

Short Run

Period of time over which supply cannot fully adjust to changes in demand due to fixed resources

Total Costs

The total fixed and variable costs

Variable Costs

These costs change as production increases

TC (Formula)

TVC + TFC

ATC (Formula)

AVC + AFC or TC/Q

MC (Formula)

ΔTC/ΔQ

AVC

Average Variable Costs

AFC

Average Fixed Costs

TVC

Total Variable Costs

ATC

Average Total Cost

TC

Total Cost

TFC

Total Fixed Costs

Q

Quantity or Quantity Demanded

MC

Marginal Cost

AFC (Formula)

TFC/Q

AVC (Formula)

TVC/Q

Monopolistic Competition

Market structure characterized by many medium-sized firms who need to be innovative and differentiate their products in price and nonprice ways (Companies need to be innovative and appeal to buyers in order to stand out from competitors)

Monopoly

one firm constitutes the market selling a product for which there are no close substitutes (One company has total control over an industry)

Oligopoly

Market structure characterized by relatively few sellers who act interdependently and/or collusively to be price-makers and to control markets (Where an industry is dominated by a small group of influential companies)

Perfect Competition

Market structure characterized by a large number of sellers with a homogenous product, infinitely elastic demand for firms, and no barriers to entrty or exit

Economic Efficiency

The allocation of resources to most productive and desired uses

Profit-Maximizing (Loss-Minimizing) Criterion

the level of output at which MR = MC

MR

Marginal Revenue

Shut-Down Point

In the short run, the firm should shut down when price is less than AVC

Shut-down Point (Formula)

P < AVC

P

Price

Perfectly Competitive Firm's Demand Function (Formula)

P = MR

Profit Maximizing Criterion (Formula)

MR = MC

Socially Optimal Price [under perfect competition in the long run] (Formula)

P = MC

In the Long Run for a Perfectly Competitive Firm (Formula)

P = minimum average cost

Profit or Loss (Formula)

(P - ATC)*q

Herfindahl Index

the sum of the square of market shares of firms in a particular market or industry [used to measure the level of concentrated power of firms in an industry]

Natural Monopolies

Monopolies that have extensive economies of scale and can provide a product at a lower cost than can several firms (a type of monopoly in an industry with high barriers to entry and start-up costs that prevent any rivals from competing)

Price-Discrimination

This practice charges different customers with different prices for the same products

Fair-Pricing Return [In A Regulated Monopoly]

P = ATC (at intersection of demand curve and average total cost curve)