Economics: Market Power-Quant & Market Characteristics & graphs

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

24 Terms

Total Product(TP)

No. variable factors(V) × Average Product(AP)/Total output firm produces in given time period

Average Product(AP)

TP/V; output produced on average by each unit of variable factor

Marginal Product(MP)

ΔTP/ΔV; extra output produces by using extra unit of variable factor

Total Fixed Cost(TFC)

No. fixed factors × Cost. fixed factors; total cost of fixed assets firm uses in given time period

Total Variable Cost(TVC)

No. variable factors × Cost. variable factors; total cost of variable assets firm uses in given time period

Total Cost(TC)

TFC + TVC; total cost of all fixed & variable factors used to produce certain output

Average Fixed Cost(AFC)

TFC/Q; fixed cost per unit of output

Average Variable Cost(AVC)

TVC/Q; variable cost per unit of output

Average Total Cost(ATC)

AFC + AVC or TC/Q; total cost per unit of output

Marginal Cost(MC)

ΔTC/ΔQ; increases of total cost of producing extra unit of output

Total Revenue(TR)

P × Q; total amount of money firm receives by selling a product

Average Revenue(AR)

TR/Q=P×Q/Q=P; revenue firm receives per unit of sales

Marginal Revenue(MR)

ΔTR/ΔQ; extra revenue gained by firm selling 1 more unit of the product in given time period

Perfect Competition

Large no. firms

Price takers; each firm so small compared to the size of the industry

Homogeneous goods; no brand names

No barriers to entry/leave for firms

Perfect knowledge of the market by producers & consumers

No long-run abnormal profits/losses

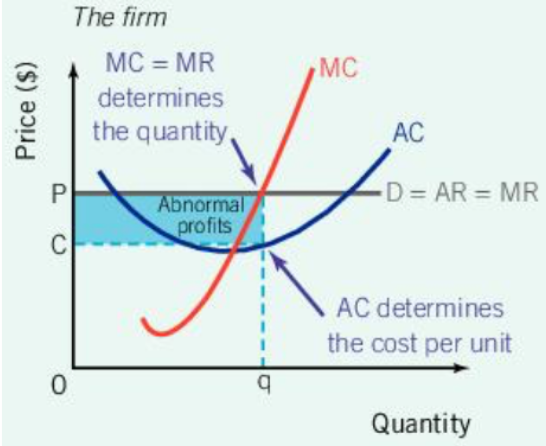

Short-Run Abnormal Profit: Perfect Competition

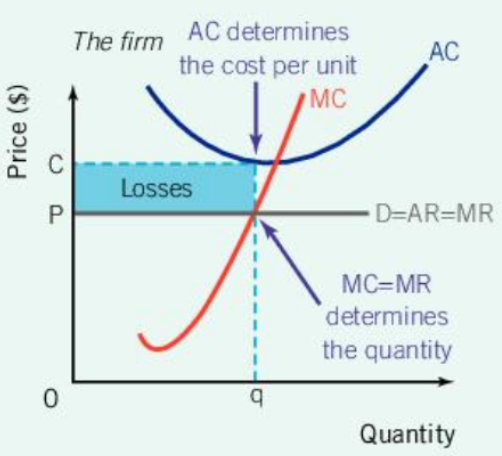

Short-Run Loss: Perfect competition

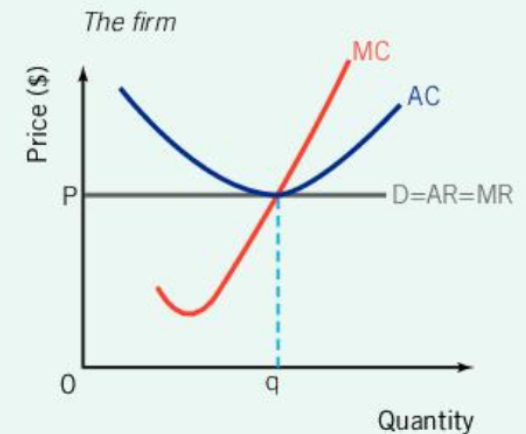

Long-Run Normal Profit: Perfect Competition

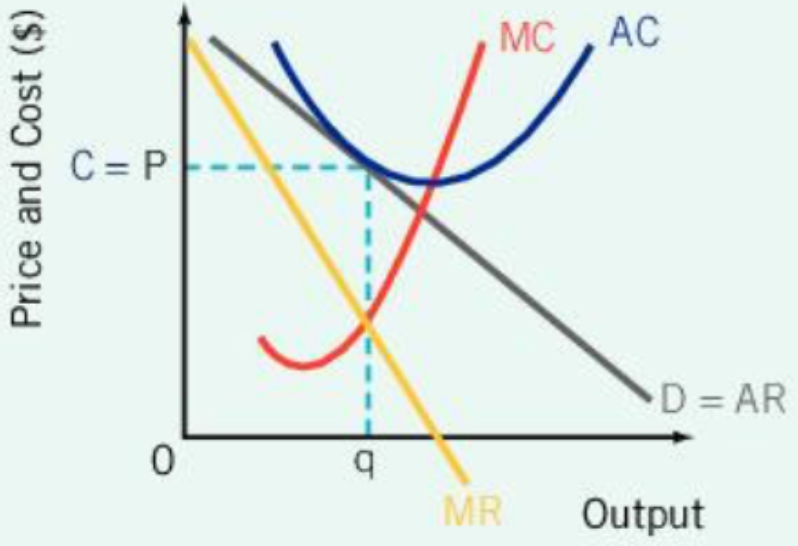

Monopolistic Competition

Large no. small firms

No barriers to entry/exit

No long-run abnormal profits/losses

Firms produce slightly differentiated products; branding→Price makes to some extent; some market power but small relative to size of industry(relatively elastic demand curve)

Monopoly

Only 1 firm producing a product; firm=industry

Existing barriers to entry→Keep out new firms/maintain monopoly/make long-run abnormal profits

Oligopoly

Few firms dominating an industry

Produce nearly identical products, highly differentiated products, or slightly differentiated products

Distinct barriers to entry such as large-scale production or distinct branding

Price rigidity

Non-price competition: firms don’t compete w/prices; brand names, marketing, advertising, packaging

Interdependence: 1 firms’ action have major effects on others

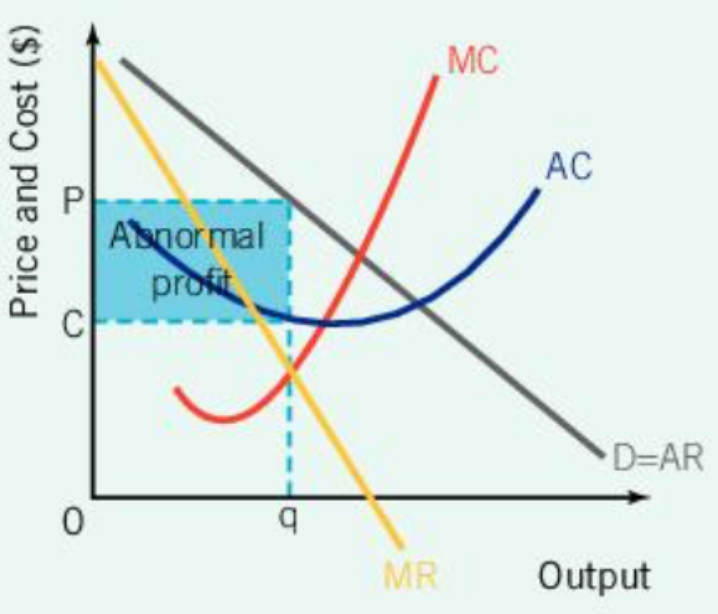

Short-Run Abnormal Profit: Monopolistic Competition, Monopoly, Collusive Oligopoly

Short-Run Loss: Monopolistic Competition, Monopoly

Allocative Efficiency

MC=AR; suppliers of firms produce optimal mix of G & S required/desired by consumers

Productive Efficiency

MC=AC; Firms combine resources most efficiently & resources are not wasted by inefficient use