3.2 - financial accounts and structure, depreciation

1/17

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

18 Terms

formula total costs

variable + fixed

formula sales revenue

price x quantity

final accounts

Financial statements prepared at the end of an accounting period

balance sheet

profit or loss statement.

internal shareholder interest in final accounts

shareholders

to see where their money was spent

to see how well their investments have performed

employees

to asses the likelihood of pay increase and job security

managers

to judge operations efficiency

to set targets and plan

external shareholder interest in final accounts

competitors

to compare financial performance

government

to examine for tax purposes

financiers

to assess credibility of debt repayment

suppliers

to decide whether trade credit should be approved

types of intangible assets

brands

patents

copyrights

reputation

trademarks

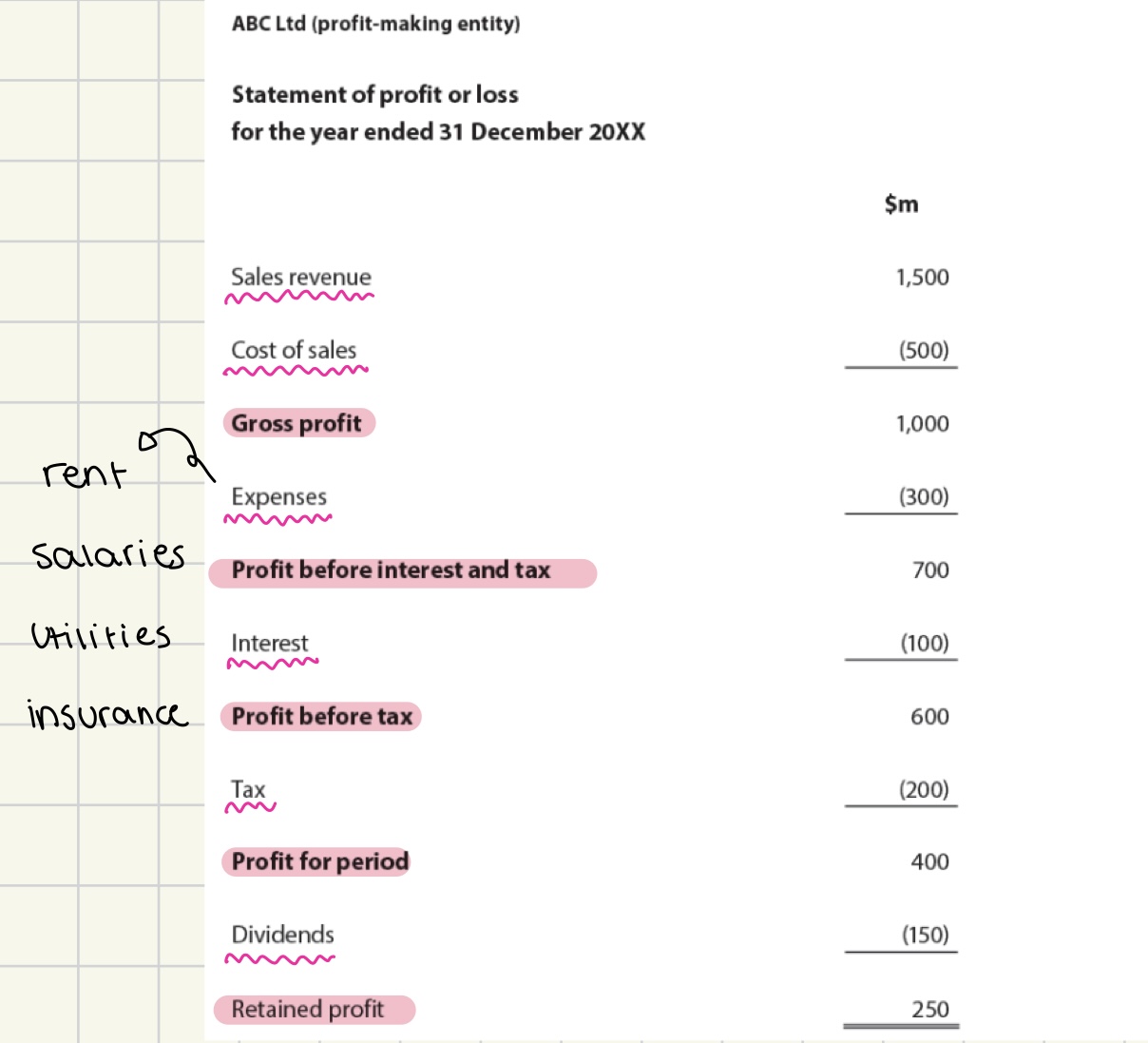

statement of profit or loss

A financial statement that summarizes revenues, costs, and expenses during a specific period, showing the company's profitability.

improving gross profit

increasing sales revenue

increasing selling price

selling greater quantities

reducing cost od sales

cheaper suppliers

buying in bulk

improving profit before interest and tax

reduce expenses

move to cheaper location

install energy efficient equipment

find cost-effective suppliers

improving gross surplus

increase funding

sponsors and fundraising

increase sales revenue

increase selling price

sell greater quantities

reduce cost of sales

cheaper suppliers

buy in bulk

improving surplus before interest and tax

reduce expenses

seek volunteers to reduce staffing costs

move to cheaper location

install energy efficient equipment

find cost-effective suppliers

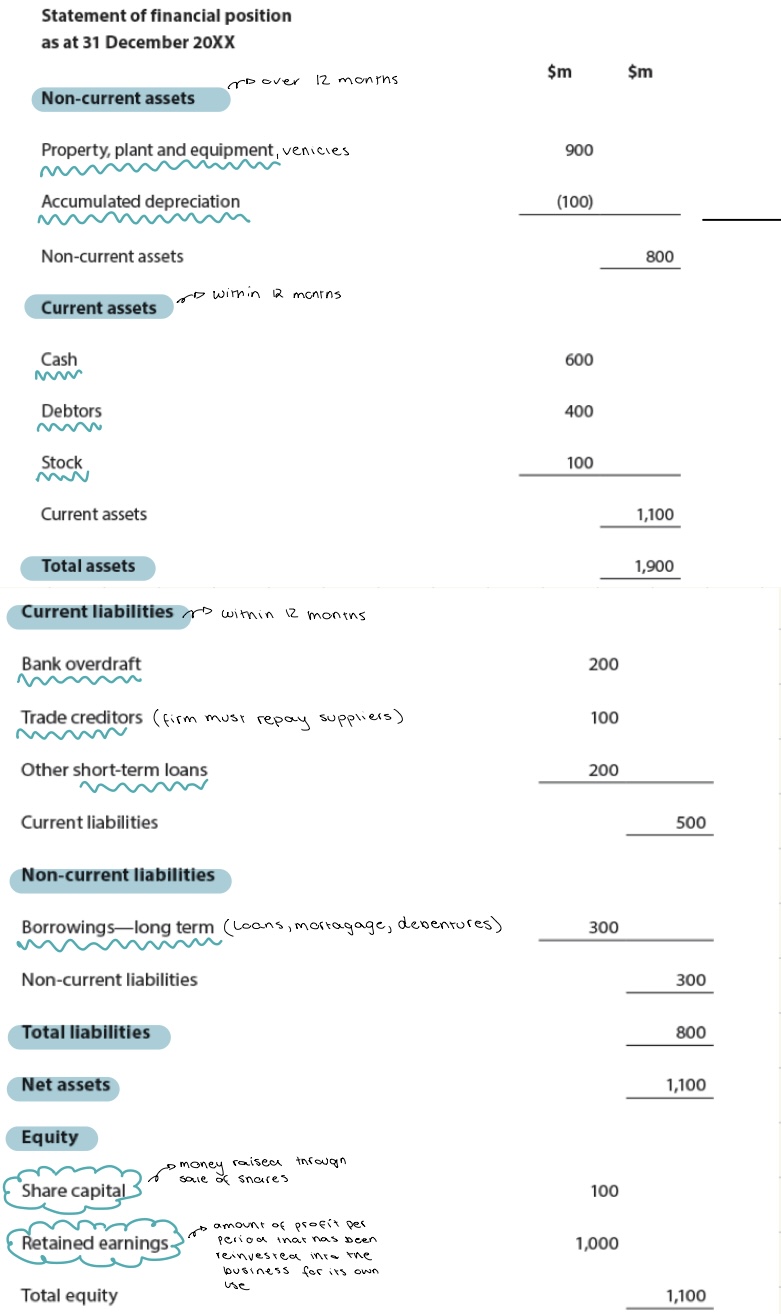

balance sheet/ statement of financial position

A financial statement that summarizes a company's assets, liabilities, and shareholders' equity at a specific point in time, providing a snapshot of its financial condition.

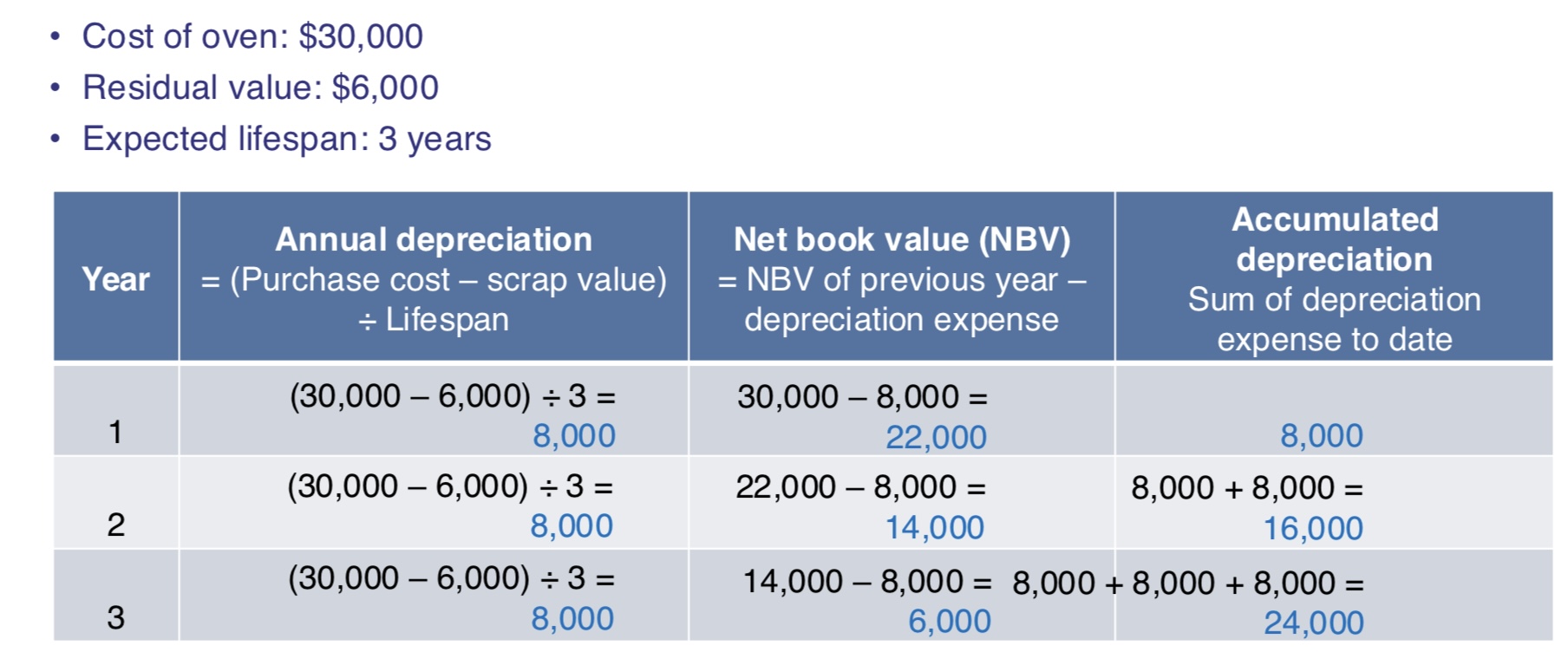

depreciation

The reduction in the value of a non-current asset over time, usually due to wear and tear.

straight line method for calculating depreciation

annual depreciation = (purchase cost- resale value) / lifespan in years

+simple to calculate and understand

-not realistic as some assets loose a much larger % of their value at the beginning of life span

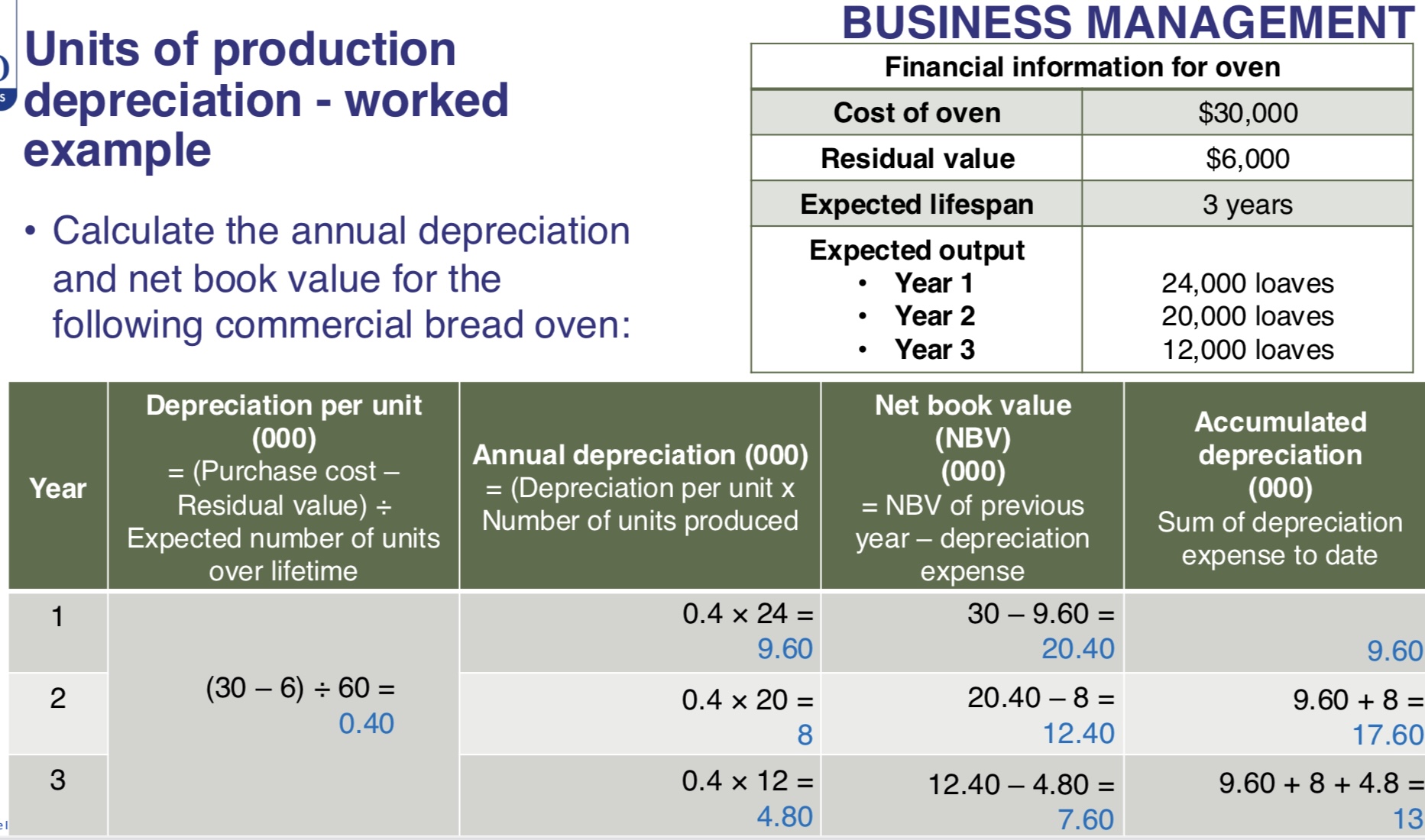

units of production depreciation method

depreciation/unit/time = ((cost of asset - resale value) / total estimated units of production) x actual units produced

+gives better insight into true running costs of non-current assets

-harder to calculate

cash flow

cash/liquid assets available for the daily running of a business with the day-to-day expenditures

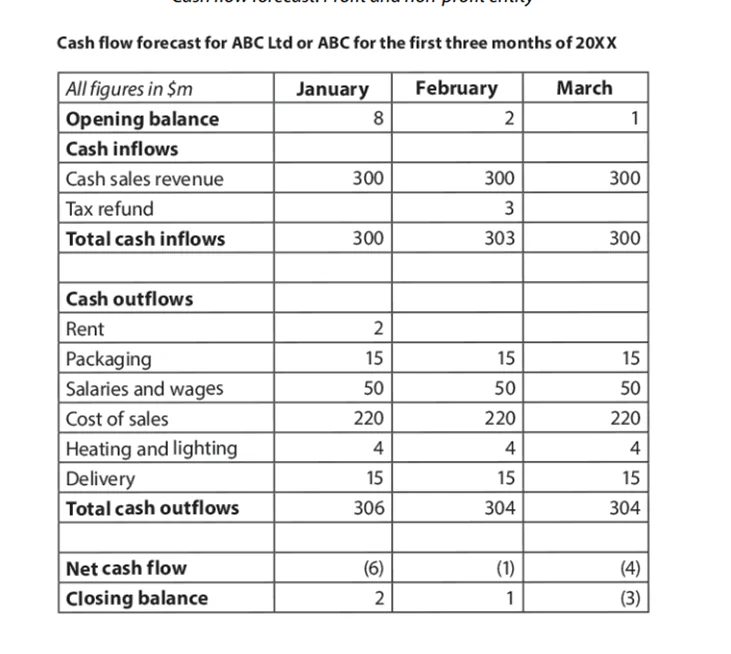

cash flow forecast

financial document which shows the expected movement of cash in and out of the business over a period of time to help manage liquidity and plan for future cash needs.

working capital cycle

the period of time it takes for a business to convert its current assets and liabilities into cash. This cycle reflects how efficiently a company manages its working capital.