ECON 11 1ST LE

1/131

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

132 Terms

Economics 1

explores the behavior of the financial markets, including interest rates, exchange rates, and stock prices.

Economics 2

The subject examines the reasons why some people or countries have high incomes while others are poor; it goes on to analyze ways that poverty can be reduced without harming the economy.

Economics 3

It studies business cycles—the fluctuations in credit, unemployment, and infl ation—along with policies to moderate them.

Economics 4

Studies international trade and fi nance and the impacts of globalization, and it particularly examines the thorny issues involved in opening up borders to free trade.

Economics 5

It asks how government policies can be used to pursue important goals such as rapid economic growth, efficient use of resources, full employment, price stability, and a fair distribution of income.

Economics 6

The study of how societies use scarce resources to produce valuable goods and services and distribute them among different individuals.

goods are scarce and that society must use its resources efficiently

Two ideas that run through all economics

Fact of scarcity and the desire for efficiency

Why will the concerns of economics will not go away

One in which goods are limited relative to desires

Situation of scarcity

Efficiency

The most effective use of a society’s resources in satisfying people’s wants and needs

Economic efficiency

Requires that an economy produce the highest combination of quantity and quality of goods and services given its technology and scarce resources

When no individual’s economic welfare can be improved unless someone else is made worse off

When an economy is producing efficiently

Essence of economics

To acknowledge the reality of scarcity and then figure out how to organize society in a wat shich produces the most efficient use of resources

microeconomics and macroeconomics

Two major subfields of economics

Adam smith

Founder of microeconomics

Microeconomics

Concerned with the behavior of individual entities such as markets, firms, and hourseholds

Adam Smith

He identified the remarkable efficiency properties of markets nd explained how the self-interest of individuals working thorugh the competitive market can produce a societal economic benefit

Microeconomics 1

moved beyond the early concerns to include the study of monopoly, the role of international trade, finance, and many other vital subjects

Macroeconomics 1

Concerned with the overall performance of the economy

1936

is when macroeconomics exist in its modern form

John Maynard Keynes

Published his revolutionary General Theory of Employment, Interest and Money that made macroeconomics exist in its modern form

Macroeconomics 2

Examines a wide variety of areas, such as how total investment and consumption are determined

Macroeconomics 3

How central banks manage money and interest rates, what causes international financial crises, and why sone nations grow rapidly while others stagnate

Scientific approach

Economist use this approach to understand economic life

Scientific approach

Observing economics affairs and drawing upon statistics and the historical record

analyses and theories

This is where economics often relies on

Theoretical approach

Allows economist to make broad generalization, such as those concerning advantages of international trade and specialization or the disadvantages of tariffs and quotas

Econometrics

A specialized technique developed by economists which applies the tools of statistics to economics problems

Econometrics 2

With the use of this, economist can sift through mountains of data to extract simple relationship

Post hoc fallacy 1

Involves the interference of causality

Post hoc fallacy

Occurs when we assume that, because one event occurred before another event, the first event caused the second event

Post hoc, ergo propter hoc

This means “after this, therefore necessarily because of this”

Failure to hold other things constant

The argument assumes that other things were constant

Fallacy of composition

When you assume what is true for the part is also true for the whole

Positive economics 1

Describes the fact so of an economy

Normative economics 2

Involves value judgement

Positive economics 2

deals with the questions that can all be resolved by reference to analysis and empirical evidence

Normative economics 2

Involved ethical precepts and norms of fairness

Normative economics 2

There are no right or wrong answers to the question because it involve ethics and values rather than facts

Normative economics 3

can be resolved only by discussions and debates over society’s fundamental values

Ultimate goal of economics science

To improve the living conditions of people in their everyday lives

what, how, for whom

The three fundamental questions of economic organization

What

What commodities are produced and in what quantities?

How

Determines who will do the production, with what resources, and what production techniques they will use

For whom

Who gets to eat the fruit of economic activity?

Alternative economic systems

Is where different societies are organized, and economics studies various mechanisms that a society can use to allocate the resources.

command economy 1

Government makes most economics decisions, with those in top of the hierarchy giving economics commands to those further down the ladder.

Market economy 1

Decisions are made in markets, where individuals or ent enterprises voluntarily agree to exchange goods and services

Market economy 2

it is one in which individuals and private firms make the major decisions about production and consumption

Firms

They produce commodities that yield the highest profits by the techiniques of production that are least costly.

Consumption

It is determined by individual’s decisions about how to apend the wages and property incomes generated by their lenor and property ownership

Laissez-faire

The extreme case of a market economy in which the government keeps its hands off economic decisions

Command economics 2

The government makes all important decisions about production and distribution

Command economy 3

The government owns most of the means of production. It also owns and directs the operations of enterprises in most industries

Command economy 4

The government is the employer of most workers and tells them how to do their jobs and it decides how the output of the society is to be divided among different goods and services

Command economy 5

The government answers the major economics questions thorough its ownership of resources and its power to enforce decisions

Government

It plays an important role in overseeing the functioning of the market. It pass laws that regulate economic life, produce educational and police services, and control pollution

Inputs

These are commodities or services that are used to produce goods and services

Outputs

These are the various useful goods or services that result from the production process and are either consumed or employed in further production

factors production

It is the other term for inputs

Labor

It consists of the human time spent in production

Capital resources

It is a form of durable goods of an economy, produced in order to produce yet other goods

Capital goods

It includes machines, roads, computers, software, trucks, steel mills, automobiles, washing machines, and building

What 2

Outputs to produce and in what quantity

How 2

With what inputs and techniques, to produce the desired outputs

For whom 2

The outputs should be produced and distributed

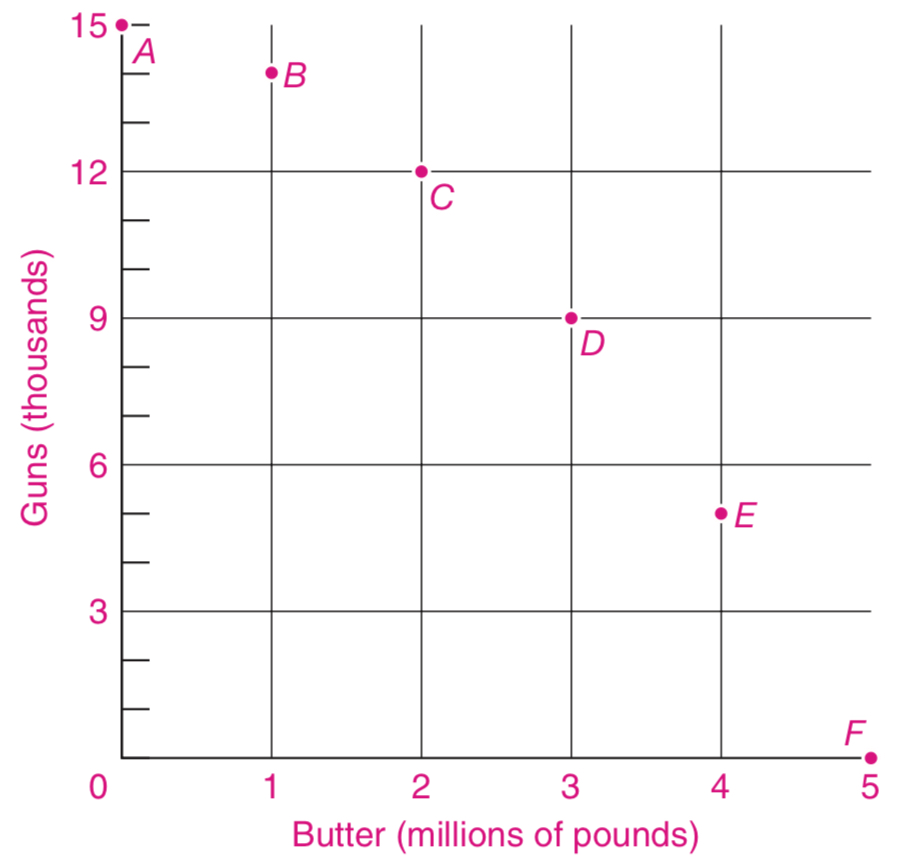

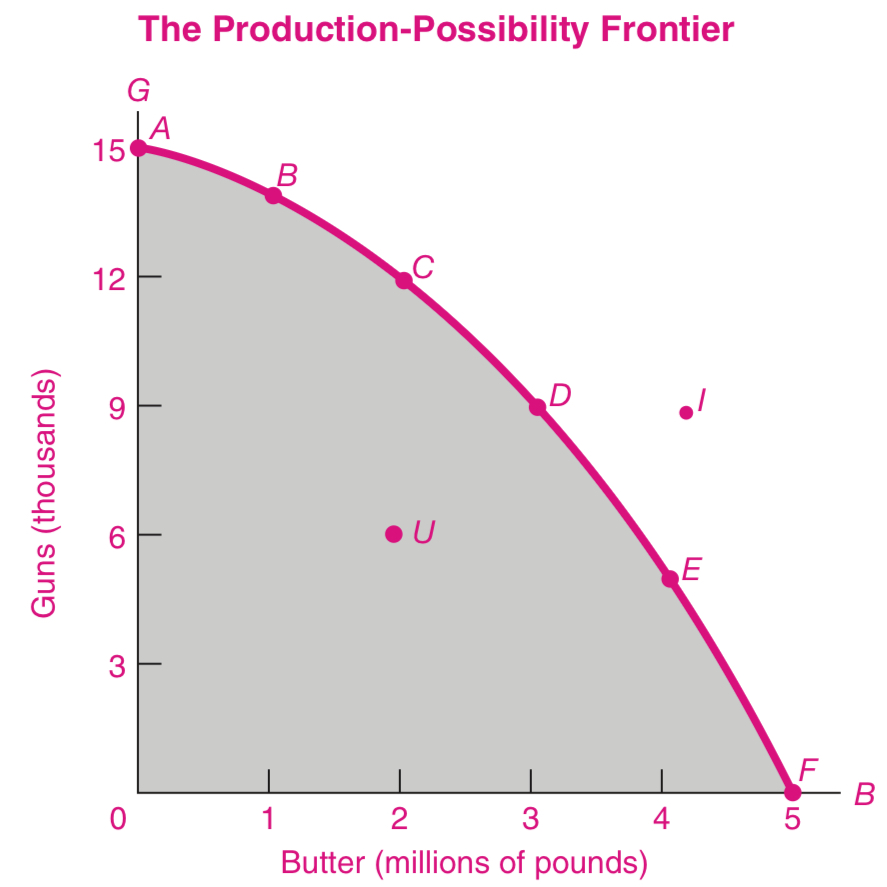

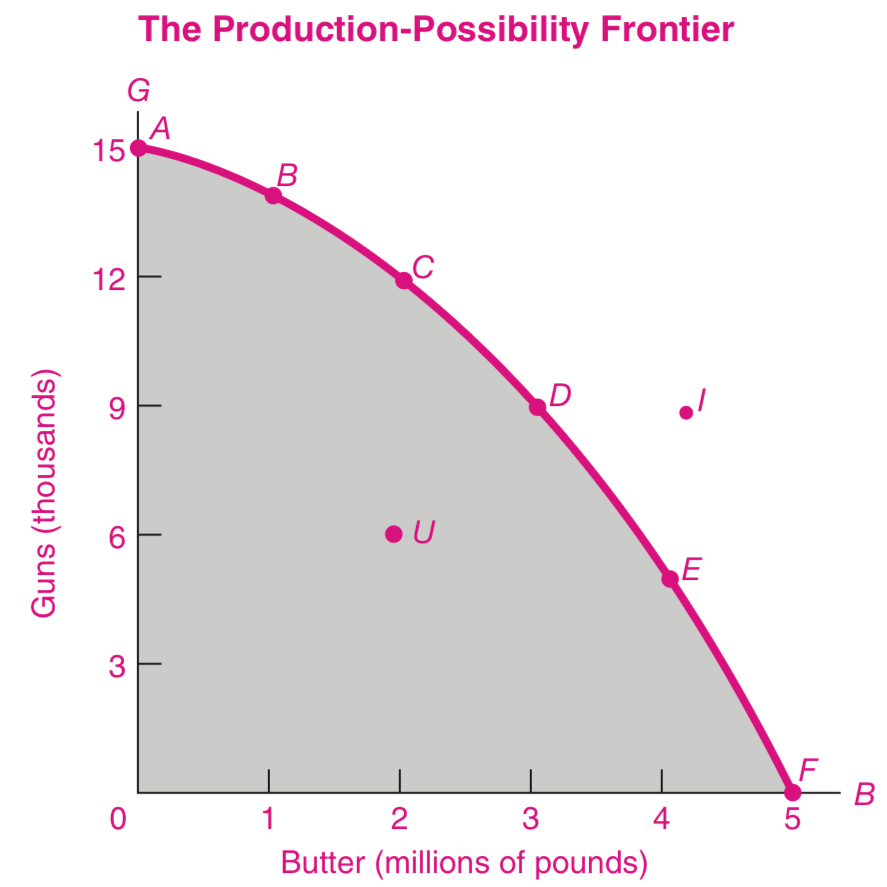

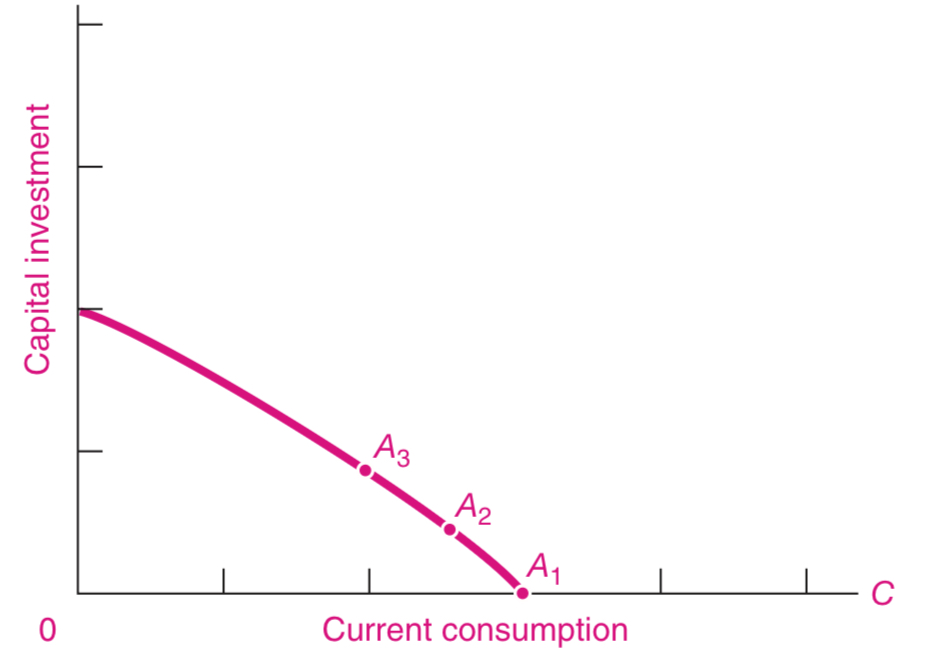

Production Possibility Frontier

It shows the maximum quantity of goods that can be efficiently produced by an economy, given its technological knowledge and the quantity of available inputs

The maximal amount of good

This depends on the quantity and quality of the economy’s resources and productive efficiency with which they are used

production possibility frontier graph

Inefficient

Point U

Infeasible

Point I

Same PPF

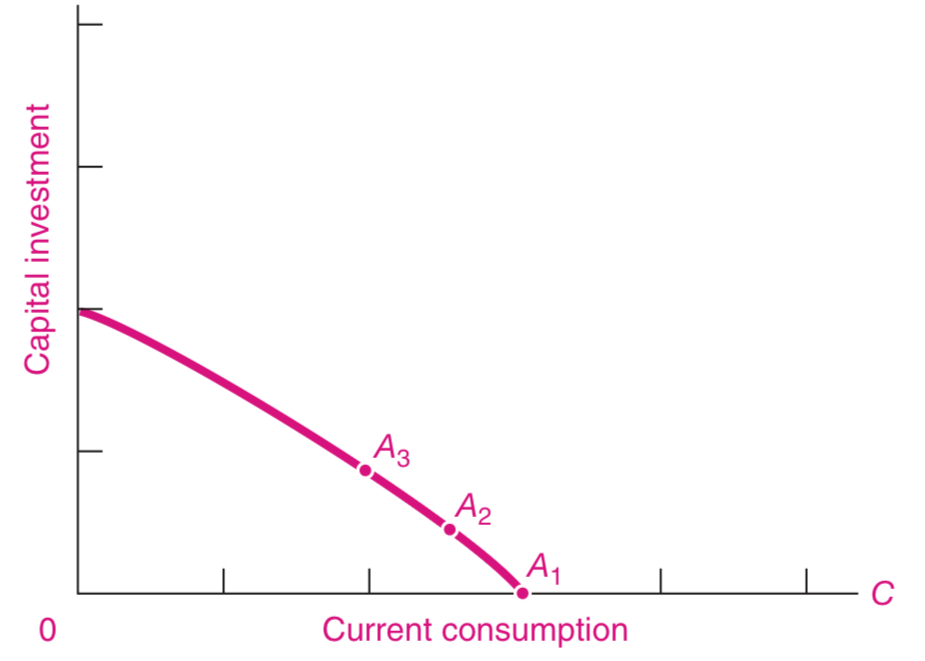

Point A1

The PPF will move outward

Point A2 and A3

Poor countries

Country that can afford little of public goods like public health and primary education

By sacrificing current consumption and producing more capital goods

With this, a nation’s economy can grow more rapidly, making possible more of both goods (consumption and investment) in the future

Time

Coin of your life. It is the only coin you have, and only you can determine how it will be spent

Opportunity cost

The next-best good that is forgone

Pierce the veil

We need to do this in economics to examine the real impacts of alternative decisions.

Productive efficiency

It occurs when an economy cannot produce more of one good without producing less of another good

Substitution

It is the law of life in a full-employment economy, and the production-possiblity frontier depicts the menu of society’s choices

Variable

It is an item of interest that can be defined and measured and that takes on different values at different times or places

Slope

Represents the change in one variable that occurs when another variable changes