Economics Unit 1 flashcards

1/25

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

26 Terms

economics:

study of how society allocates scarce resources among unlimited wants and needs

microeconomics examines

how producers and consumers interact in individual markets

macroeconomics examines

the factors that affect the economy as a whole

the economic decision rule

if the benefits are greater than the costs; do it

if the costs are greater than the benefits; dont do it

cost benefit analysis is the process of

weighing up strengths and weaknesses of a policy, choice, or action, and then coming up with a judgement/decision

opportunity cost

the next best thing is sacrificied or given up as a result of a choice

trade off

anything that is given off as the result of a choice

free goods

something that is so abundant that it is not scarce and it can be considered free

economic goods

something that is scarce and has competition for it is known as an economic good

incentive

something that motivates an individual to act a certain way

the three parts of the basic economic problem

WHAT should be produced and how much?

HOW should things be produced?

for whom (WHO) should things be produced

societies often answer the basic economic with three solutions

Planned (command) economy

Free market economy

Mixed market economy

resources are seperated into four categories (factors of production)

Land

Labour

Capital

Entrepreneurship

The Production Possibilities Curve (PPC) is a

graph which shows the tradeoff between the production of two different items

the PPC easily illustrates the concepts of

scarcity, choice, opportunity cost, and efficiency

the PPC demonstrates

the maximum combinations of two types of output that can occur in an economy if all resources are being used efficiently and technology is fixed

the law of increasing opportunity cost is when

increasing the quantities of one good can only be accomplished by sacrificing ever-increasing quantities of another good

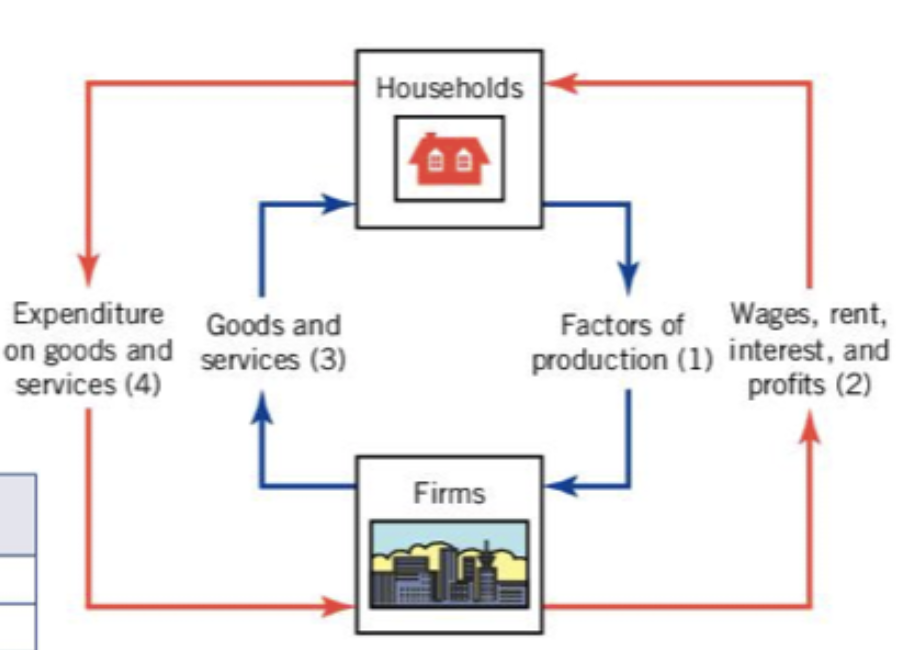

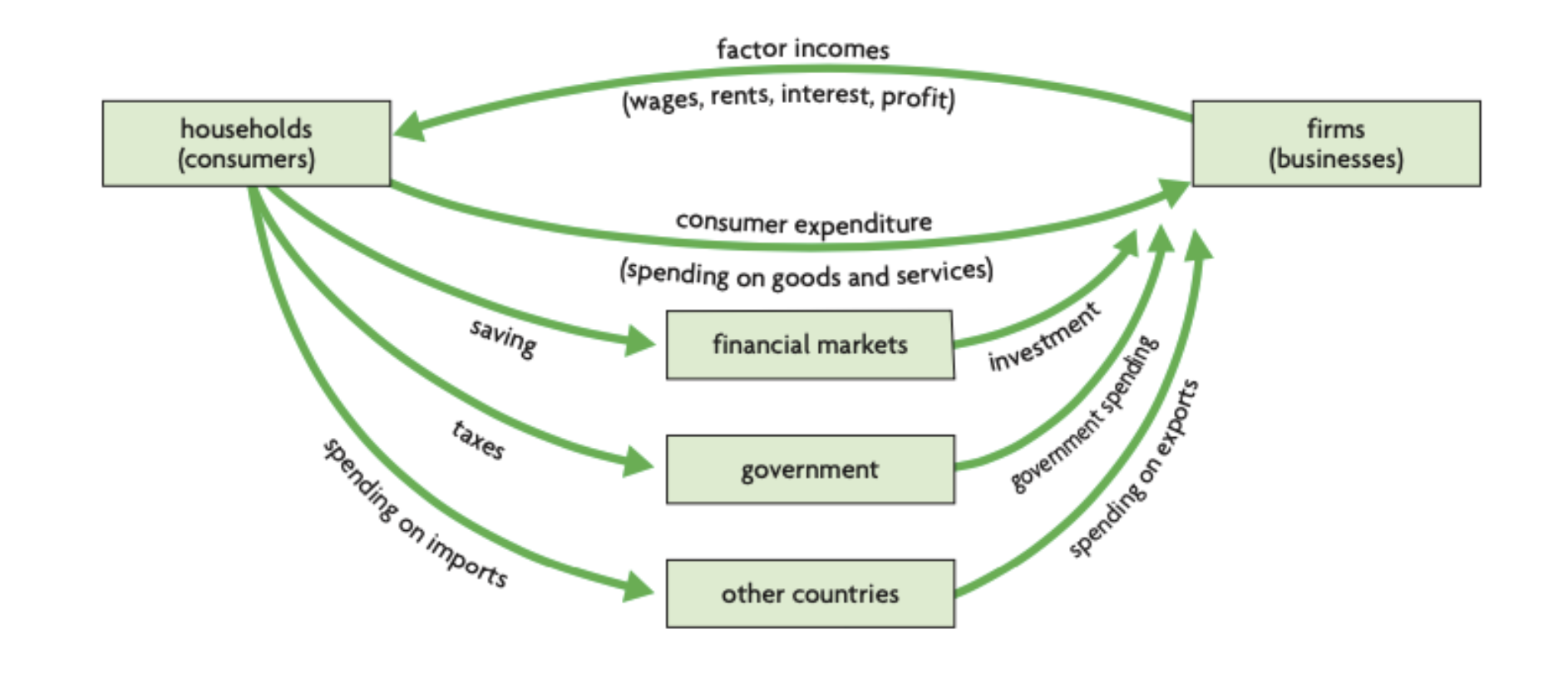

the economy can be illustrated by the

circular flow model, in which households supply the factors of production and firms provide payments to the factor

not all money stays in the domestic consumer economy, some money leaves the economy through

leakages

leakages can be

governments taking money from consumers in the form of taxes

consumers saving some of their income in financial institutions

households and businesses spendingmoney on imports, sending the money to foreign producers

money can also enter the economy in form of

injections

injections can be

government spending on public services, infrastructure and salaries

the financial sector investing money into firms

foreign households purchasing exports, injecting money into the economy

this a diagram displaying

the circular flow of income with leakages and injections

the ceteris paribus assumption is when economists assume

“all other things being equal”