IB Introduction to Economics

1/65

Earn XP

Description and Tags

Includes Chapter 1: What is Economics? & Chapter 2: How do economists approach the world?

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

66 Terms

Economics

the study of how resources are allocated to satisfy the unlimited needs and wants of individuals, governments, and firms in the economy.

Economic Agents

Economic decision makers that interact for the purpose of production and consumption. They are households, firms, and governments.

Microeconomics

the study of the actions of firms & households.

Deals with specific markets/segments in the economy

Welfare and profit maximization

assumes rationality of individuals

Macroeconomics

the study of the operations of the economy as a whole.

Deals with broad economic topics, based on decisions made by governments and countries.

maximization of economic goals

less consensus due to different schools of thought

more emphasis on statistics and empirical data

WISE ChoICES

key concepts of IB Economics. They are:

Well-being

Interdependence

Scarcity

Efficiency

Choice

Intervention

Change

Equity

The Basic Economic Problem

How to best allocate scarce resources to satisfy the unlimited wants and needs of individuals, firms, and governments

Factors of Production

are the four categories of resources that are required to produce any good or service, namely land, labor, capital and enterprise.

Land

natural capital

includes every natural resource

renewable and non-renewable resources

Labor

human capital

both physical and intellectual labor

Capital

physical capital

all-man made resources

Entrepreneurship

the ability to innovate, take business risks, and seek new opportunities for the opening and running of business.

the skills, creativity, and risk-taking ability that a business person requires to combine and manage the other factors of production

National Minimum Wage

price floor in the labor market. Employers are required to pay at least this amount to their employees

Profit

total revenue minus total cost.

Income

sum of collective rewards from all factors of production in the production process.

Scarcity

shortage of resources in the economy at any moment in time.

Needs

essential goods & services for human survival

Wants

goods & services that are human desires

Goods

tangible products that can be produced, bought, and sold.

Services

intangible products provided by firms & individuals and paid for by customers

Economic Goods

a.k.a products. goods & services that have utility.

Renewable Resources

Resources that can be used repeatedly and replenish naturally.

Opportunity Cost

the cost of an economic decision measured in terms of the best alternative choice forgone.

Free Goods

products with a natural abundance of supply; do not require any deliberate effort in acquisition. There is no opportunity cost attached to these goods.

Private Sector

The sector of the economy where private firms and individuals produce goods and services.

Public Sector

the sector of the economy where the government produces or supplies certain goods and services.

Economic System

describes the way in which an economy is organized and run, including alternate views on how resource should be allocated

Free Market Economy

Economic system that relies on the market forces of demand and supply to allocate scarce resources via the private sector of the economy

Planned Economy / Command Economy

Economic system where the government (or public sector) allocates scarce resources.

Mixed Economy

Economic system that with some resources being owned and controlled by private individuals and firms while others being owned and controlled by the government. Combination of free market + planned economies.

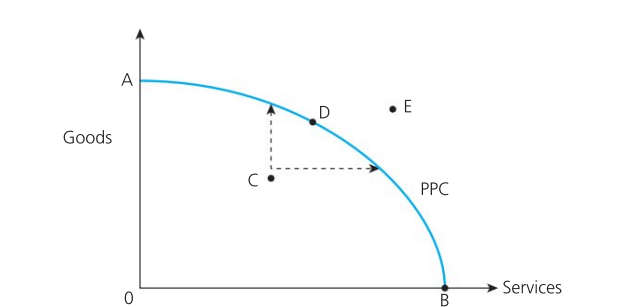

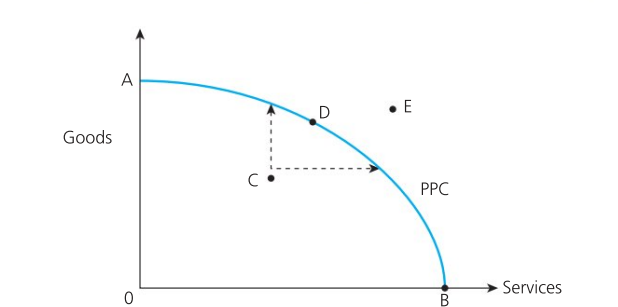

Production Possibility Curve (PPC)

Model of the maximum combination of two products that an economy can produce, when all its resources are used efficiently. It show the productive capacity of the economy at any moment of time

Marginal Rate of Transformation / Rate of Substitution

Gradient of the PPC; shows the opportunity cost of the two products.

Pareto Efficiency

Occurs when it is not possible to make one person better off without making someone else worse off.

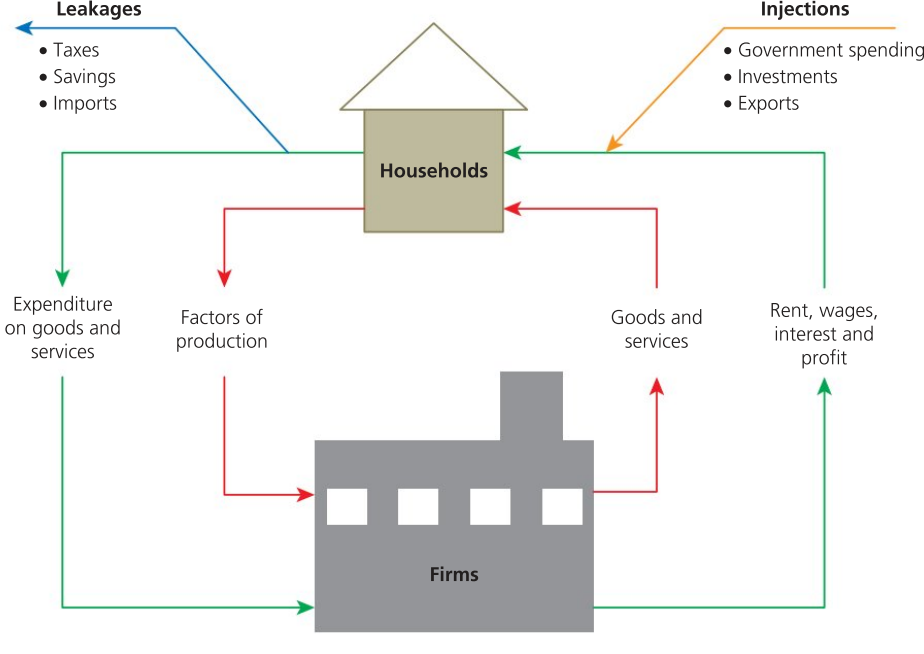

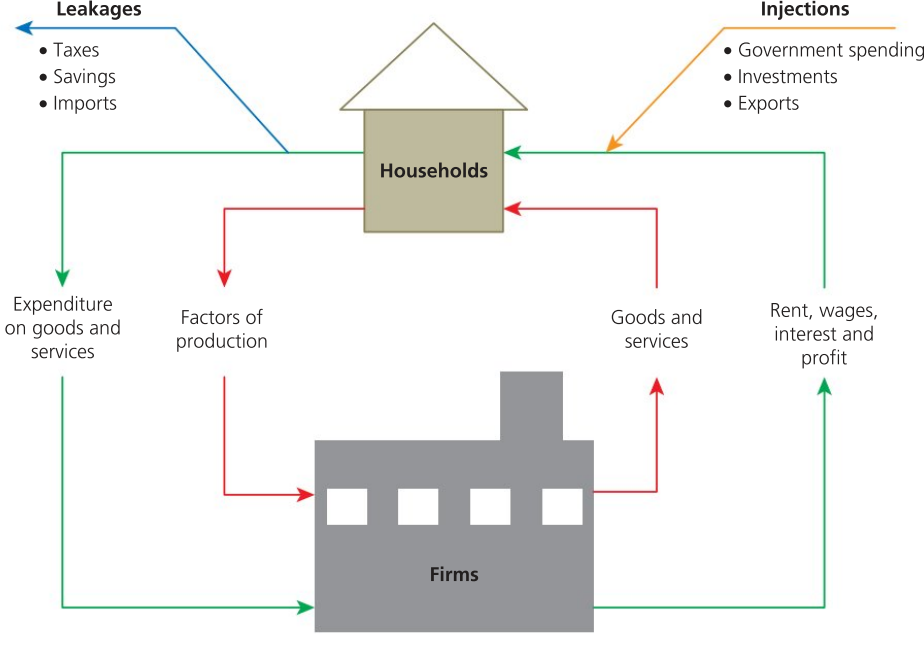

Circular Flow of Income

Model used to explain how economic activity and national income are determined based on the interactions of economic decision makers.

Closed Economy

Part of the circular flow of income. Includes households, firms, with the addition of government i.e. domestic economic decision makers.

Open Economy

art of the circular flow of income. Includes households, firms, with the addition of government and foreign sector (accounts for imports and exports)

Leakages / Withdrawals (W)

Take money out of the circular flow of the income. They are savings (S), taxation (T) and imports (M), that is, W = S + T + M.

Injections (J)

Put money into the circular flow of the income. They are government spending (G), export earnings (X) and investment expenditure (I), that is, J = G + I + X

Economic Methodology

Study of processes, practice, and principle in relation to economics as a social science. Includes the models, theories, and assumptions apart of the discipline.

Positive Economics

Study of what the economy actually is. Study of economics that is provable. based on logic, reasoning and empirical evidence

Logic

refers to rationality and reasoning in explanations of economic phenomena and policy.

Hypothesis

An assumption, notion or educated guess before conducting research

Model

A hypothesis that has been tested repeatedly, is proven or rejected, and can be used to explain the real world

Theory

A broad generalization used to explain situations supported by economic evidence or data from models

Ceteris Paribus

Latin phrase which means “all other factors remaining constant”. Allows economists to explain the cause and effect of specific economic variables.

Empirical Evidence

first-hand data and information collected through observation and experimentation.

Refutation

the act of a statement or theory being proved wrong or false by empirical evidence

Normative Economics

Study of what an economy should be and it’s supposed to work. It considers the opinions and beliefs of people. It is subjective.

Value judgements

the beliefs of individuals and societies about what is right and what is wrong

Equity

Concept in which there is economic fairness in the distribution of resources.

Equality

Concept in which all are equal and should have equal recognition. It is about collectivism and social fairness

Economic Thought

Refers to the historical account of different economic ideas, beliefs, and principles over time.

Laissez-faire

Approach to economics that allows transactions to take place without government interference.

Invisible Hand

metaphor used to describe how the behaviors and decision-making of individuals ends up benefitting society as a whole because they are incentivized to act in their own self-interest

Finite Resources

factors of production being limited in supply

Classical Economics

main economic school of thought during the 18th-19th centuries. focuses on self-regulation of market forces to allocate resources efficiently.

Utility

refers to the level of satisfaction derived from the consumption of a product

Marginal Utility

refers to the satisfaction gained from the consumption of additional units of a product

Law of Diminishing Marginal Utility

As individuals consume more of a product, the satisfaction gained from each additional unit of consumption (marginal utility) declines.

Say’s Law

The ability to purchase a product depends on the ability to produce or supply (which generates income). Supply creates it’s own demand

Marxism

approach to macroeconomic policy that focuses on meeting the needs and values of the masses, rather than for the privilege of a minority of capitalists.

Keynesian Economics

Interventionist approach to macroeconomic policy. The idea that increased government expenditure and lowering taxes will stimulate demand in the economy

Monetarists

economists that believe monetary policy is a more powerful and effective macroeconomic stabilization policy than fiscal policy

Monetarism

Macroeconomic school of thought that emphasizes monetary policy analysis and the role of money supply in the economy.

New Classical Counter Revolution (NCCR)

Economic school of thought that favored supply-side macroeconomic policies. Led to popularity in privatization of state-owned companies and the withdrawal of government regulation of markets.

Sustainability

The ability to conduct economics indefinitely, achieving economic goals that increase living standards without jeopardizing the needs and wants of future generations.

Circular Economy

an economic system in which raw materials, components and other resources are used sustainably to generate output.