AP Chap 10 & 11

1/103

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

104 Terms

binomial assumption

says that an underlying price can only move up or down one level from its current position in a single period. once it’s moved one level it’ll have to wait until the next period to move again. a period is about a few seconds

how to find the stock price after an up/down movement

from multiplying the initial stock price with the up/down state value. it’s usually >1 for upstate and <1 for downstate

absence of arbitrage

to use a fair price that is risk free

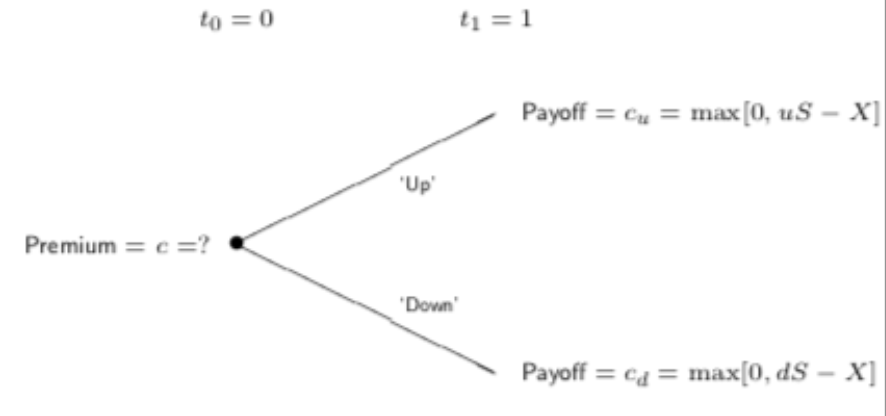

how to find the option payoff for up/down state

by finding the max difference between the stock price after movement and the exercise price for the call option

payoff premium

the difference between the option payoff for the up and down state

risk free asset

a zero coupon bond in one period with the face value of one dollar

the 2 methods for pricing call options

replicating a portfolio or by the risk neutral method

how does the replicating portfolio work

by imposing no abitrage and to say that the price of the call option must be exactly equal to the cost of setting up the replicating portfolio

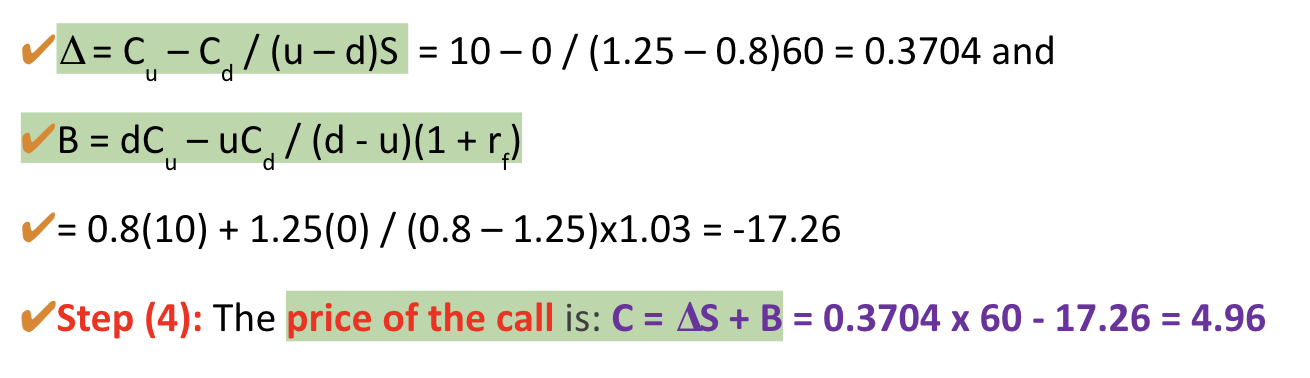

formula for the price of the call

where delta is the difference between the two states of the stock price and b is the amount borrowed

why does the final call price not relate to the state movement

the replicating portfolio is meant to match the option payoff exactly in all possible outcomes. this is cus it’s meant to find the fair price through arbitrage and not to track the fluctuating market price

how to find the call price with the replicating portfolio method

work out the payoff (max[u/dS - X]) for the up and down to replicate it, then find the difference for ∆S then find the amount borrowed B and then apply the formula C = ∆S + B to the the derivative

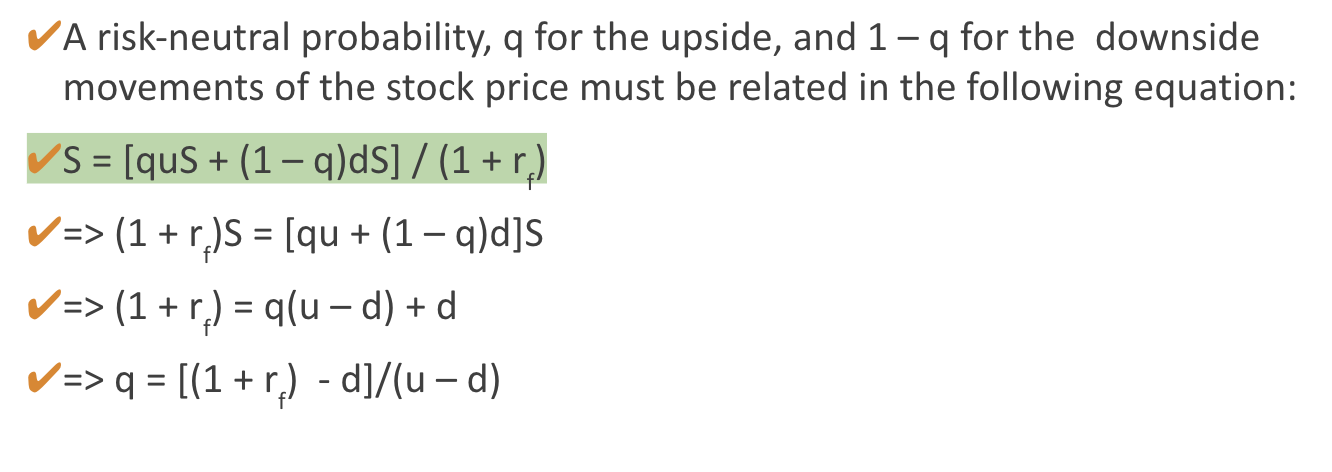

formula for risk neutral probability regarding the stock price and its movements

formula for the up/down state price at a risk neutral probability

c = 1/1+r [uSq+(1-q)dS]

![<p><span>c = 1/1+r [uSq+(1-q)dS]</span></p>](https://assets.knowt.com/user-attachments/f8e1435a-1245-403a-b4ba-bf381fd1f955.png)

the 3 ways to find the value of a European put call is

put call parity, no arbitage approach and the risk neutral approach

put call parity

when the sum of the current spot price and put is equal to the sum of the call and the current strike price.

current strike price formula

PV(X) = X/1+r

the value of the call/put at the up node

why would it be good to exercise an american call early

the call is more than the difference between sell and strike, so the payoff from an early exercise is less than selling the call before it expires as it makes it more ITM through time

why is it better to exercise an american call early if the stock is going to pay a dividend

if the stock pays a dividend, the stock price would fall making the call price fall too, so it's better to exercise the call before the stock price falls when they pay the dividend

why is better to exercise an american put early when the stock price has fallen

when the stock price falls its better to exercise immediately if the payoff (exercise price - the amount the price has fallen) is more than the put price in the 2nd period (down state)

in the money (ITM)

when a call option's market price exceeds the strike price

when should an option be exercised at ITM

if it’s ITM by at least as much as the fees for the underlying (current market price) transaction

should options be exercised before expiration

no as it gives away inherent value which could be earned if you wait till maturity. unless it’s american, then it’s good if the strike price is higher than the market price

when should equity call options be exercised

only should be exercised early on the day before an ex dividend date

when is early exercise good for deep ITM options

only if the dividend value is more than the t value (what could be earned by waiting). when the strike price is significantly lower for a call or higher for a put than the current market price for an underlying asset

plain vanilla options

european and american calls and puts

3 differences between european and american call options

american can be exercised any time before the expiration date/maturity while european can only be exercised on maturity. european has lower premiums while american has higher premiums due to its flexibility. american is used more for individual stocks while european is used more for index options

exotic options

options with more complicated payoffs

lookback call

the option is to buy the underlying asset at the minimum price which the asset reaches during the life of the option. The payoff is max[ST −Smin ,0]

average strike asian call

the option is to buy the underlying asset at the average price of the asset during the life of the option. The payoff is max[ST −Save ,0]

average price asian call

the option is to buy the underlying asset at a fixed strike price, but with the payoff based on the average price of the asset during the life of the option The payoff is max[Save −K,0]

difference between binomial option pricing and black scholes option pricing

binomial option pricing views time as discrete, meaning during the period, the price moves up or down in fixed steps while black sholes option pricing views time as moving continuously, and therefore the price evolves continuously. mathematically, t eventually tends to 0 while the number of steps tends to ∞

what does the black scholes formula say the option price is

the expected gain from exercising less the expected cost of exercise.

call premium

when the market price is higher than the strike price cus it's the extra amt you're getting paid for exercising before the maturity date

underlying price

current market price

the call premium factor affecting the black scholes option price

call premium increases as the underlying price rises, so when the market price is higher than strike, you earn more, making it a more valuable asset and increasing the underlying price as well

put premium

when the strike price is higher than the market price so it's a loss for the buyer but good for the seller

the put premium factor affect the black scholes option price

put premium decreases as the underlying price increases as it the put would then have less payoff

call prices factor affecting the black scholes option price

call prices decrease when the exercise price is increased as the value of the option has decreased

put prices factor affecting the black scholes option price

put prices increase as the exercise price increases, making the payoff of the put higher and therefore the value higher

the 6 factors affecting the black scholes option price

call premium, put premium, call price, put price, volatility and time affecting the call and put prices, interest rates effects on call and put values

how does the interest rate affect the value of a call and put

when the interest rate increases, the value of the call decreases as it encourages saving and therefore increases interest income, while the value of a put decreases due to the interest that can be earned from shorting the stock would be higher

how does volatility and time affect call and put prices

it increases the them as it is more likely they will then be ITM

shorting a stock

when you borrow a security then sell it so that you can buy it at a lower price again later

the 2 methods to find volatility

estimate volatility from the history of the underlying price or retrieve the volatility parameter from the price of an already traded option on the same underlying

implied volatility

the market’s forecast or expectation for future volatility based on the past volatility

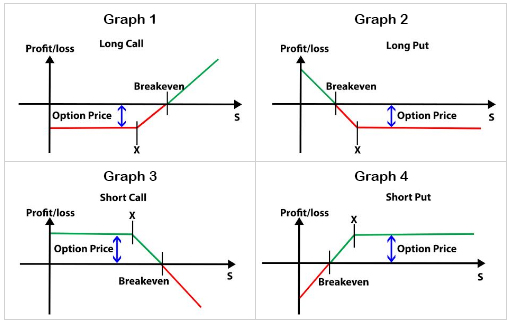

payoff graphs for long short put and call

for put, it’s put up for sale something that had a life before and so it’s increasing or decreasing from the y axis. for call, it’s call for purchase and it didn’t have a life before so it starts as a constant and then increases or decreases