Economics 11HL Unit 1

5.0(1)

Studied by 38 peopleCard Sorting

1/50

Earn XP

Last updated 12:37 AM on 9/14/23

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

51 Terms

1

New cards

Factors of Production

Land, labour, capital, entrepreneurship

2

New cards

Land

natural resources

3

New cards

Labour

human resources

4

New cards

Capital

production of goods

5

New cards

Entrepreneurship

management

6

New cards

Scarcity

limited availability of economic resources relative to society’s unlimited demand for goods and services

7

New cards

Efficiency

Maximized production using supply and based off of individual choices (demand) or making the best possible use of scarce resources

8

New cards

Choice

not all needs and wants can be satisfied, so choices have to be made

9

New cards

Oppurtunity cost

what you give up to have something else

10

New cards

Economic cost

accounting/financial cost + oppurtunity cost

11

New cards

Sustainability

ability of the present generation to meet its needs without compromising the ability of the future generation(s) to meet their own needs

12

New cards

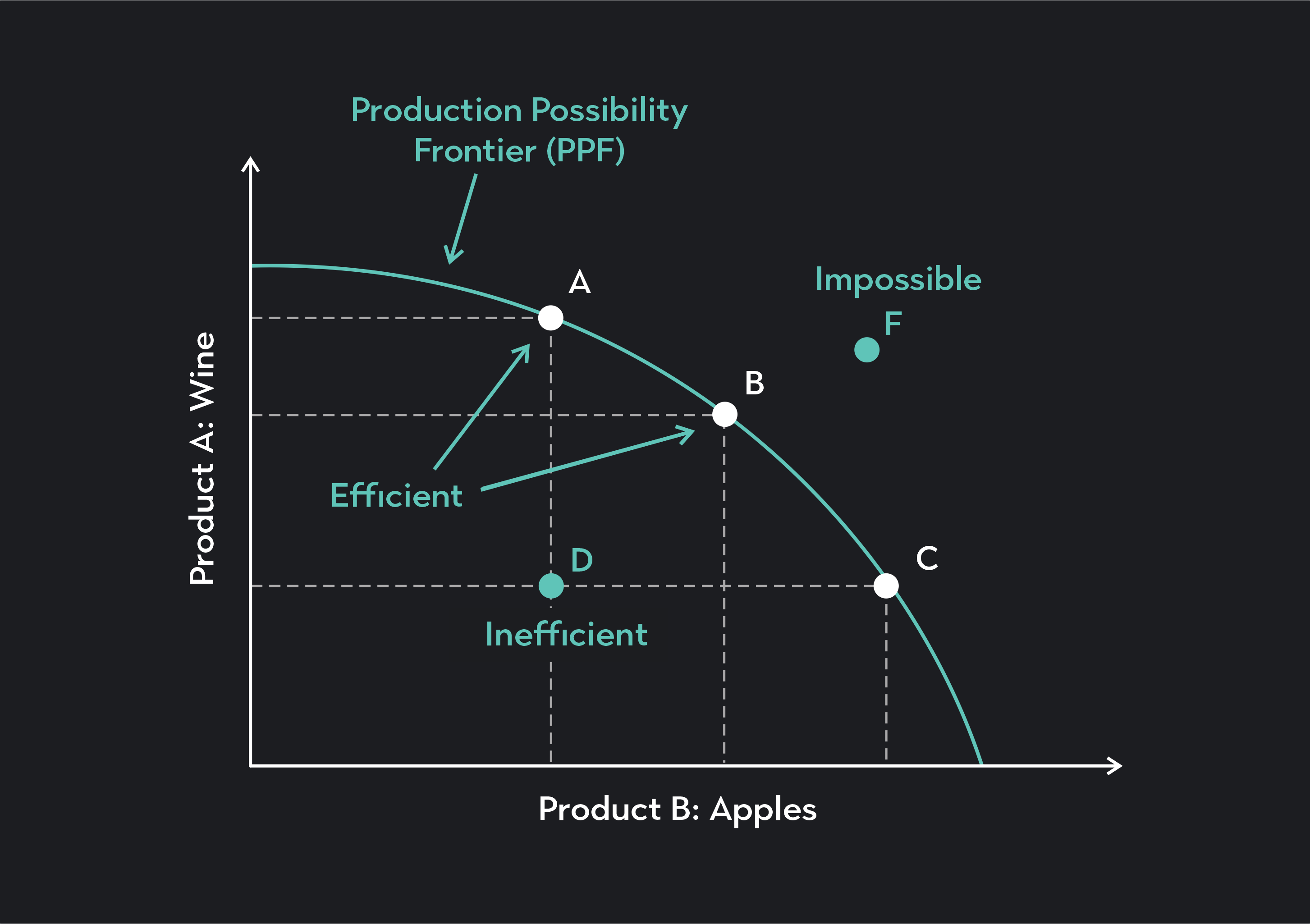

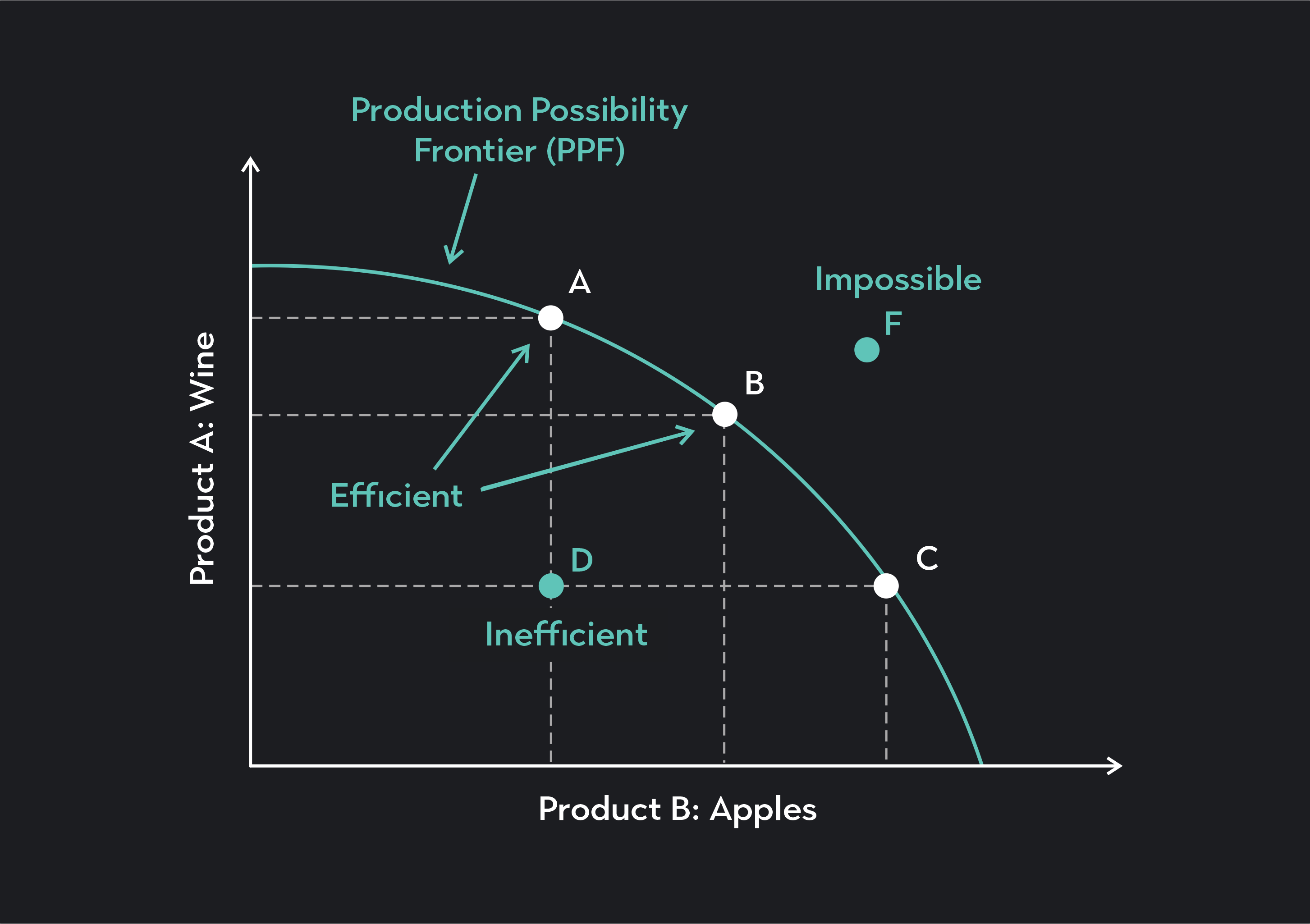

Production Possibilities Curve (PPC)

a graph which indicates the different possible choices a firm can make to maximize profit while maintaining maximum efficiency

Difference between Price 1 and Price 2 is not the same as the difference between Price 2 and Price 3 (oppurtunity cost)

curve is named PPF (Production Possibility Frontier)

Difference between Price 1 and Price 2 is not the same as the difference between Price 2 and Price 3 (oppurtunity cost)

curve is named PPF (Production Possibility Frontier)

13

New cards

Assumptions of the PPC

technology, time, and factors of production (FOP) is constant

only two goods are produced in this market

all of society’s income goes towards these two goods

only two goods are produced in this market

all of society’s income goes towards these two goods

14

New cards

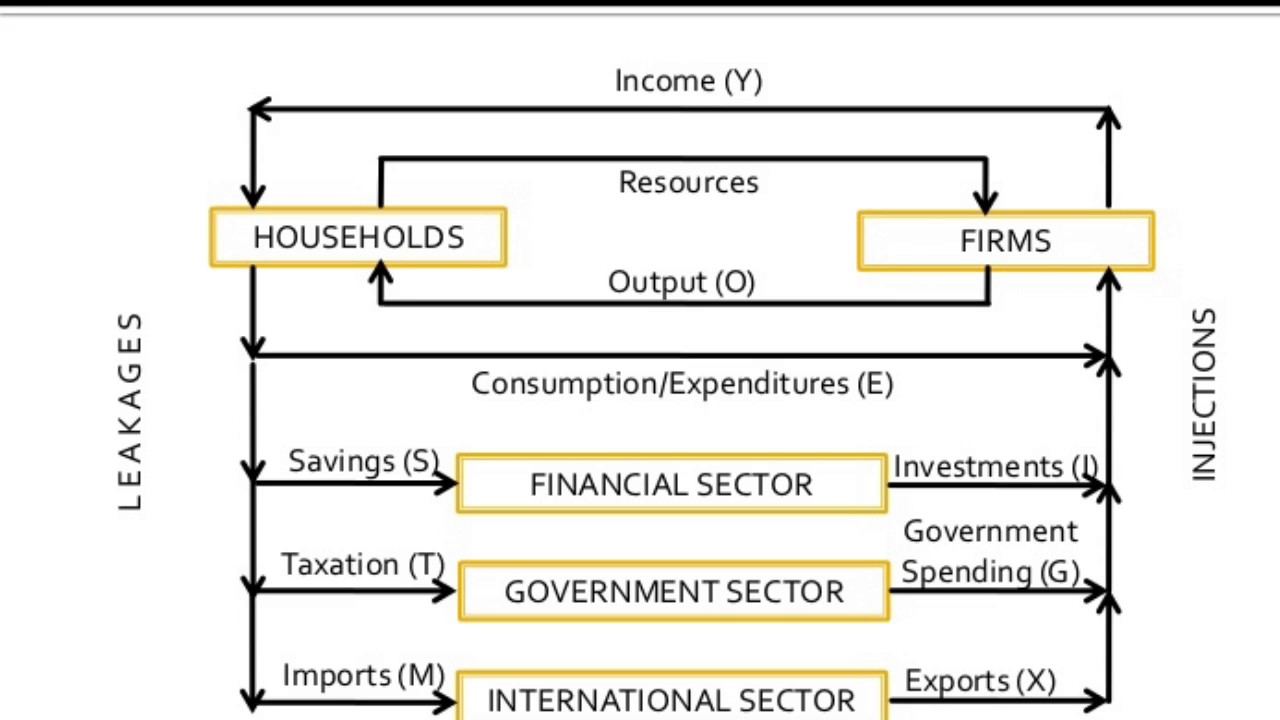

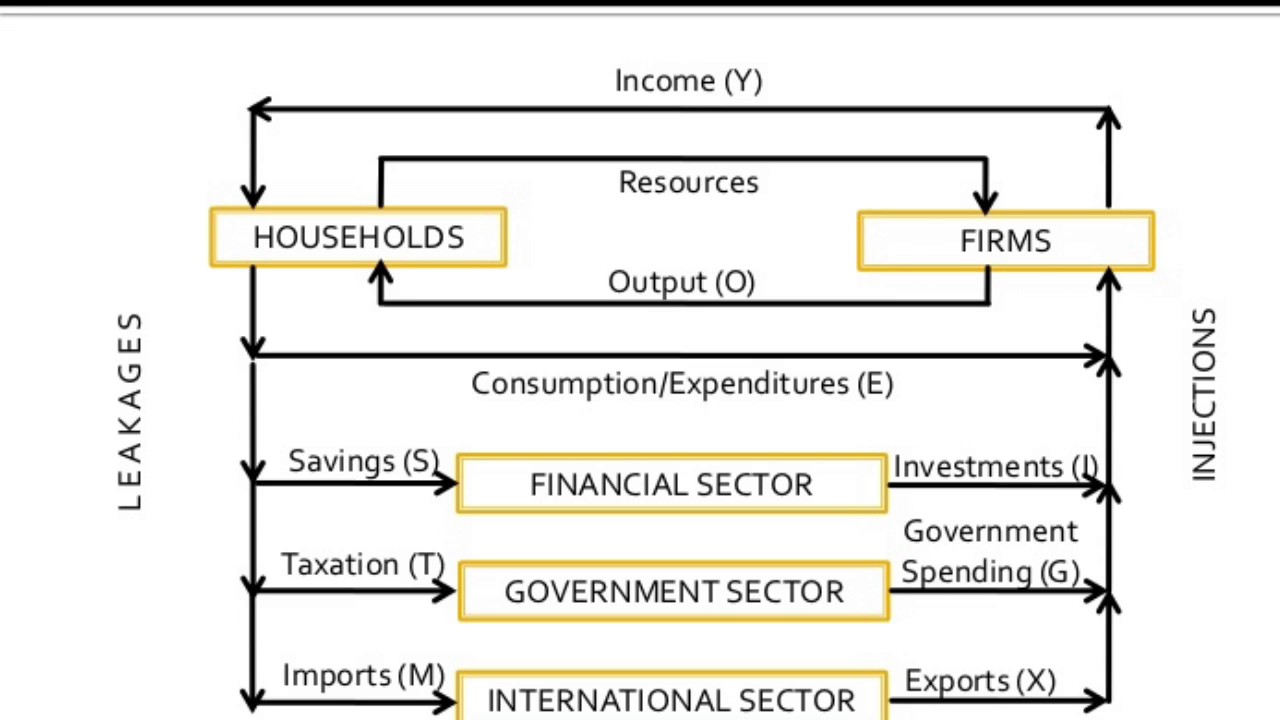

Circular Flow Diagram

GDP = C + I + G + (X-M)

Consumption, Investment, Government, eXports, iMports

Simplification of reality that takes out certain factors and makes them constant

Consumption, Investment, Government, eXports, iMports

Simplification of reality that takes out certain factors and makes them constant

15

New cards

Methodology

Positive and Normative

16

New cards

Positive

Scientific perspective on economics (hypothesis + data)

Verifiable in principle

All other things remain equal (certeris parabus)

Verifiable in principle

All other things remain equal (certeris parabus)

17

New cards

Normative

Subjective value judgement

Cannot be objectively verified/measured

Nonquantifiable adjectives (important, ought to, must, etc.)

Cannot be objectively verified/measured

Nonquantifiable adjectives (important, ought to, must, etc.)

18

New cards

Adam Smith

“the invisible hand” is a metaphor for efficient allocation of resources by society

laissaz faire

laissaz faire

19

New cards

Karl Marx

labour theory of value

decreasing rates of profit and increasing concentration of wealth

more caring towards the masses

decreasing rates of profit and increasing concentration of wealth

more caring towards the masses

20

New cards

Keynes

counter-cyclical government and multiplier

argued that governments had an important management role in macroeconomics

provided a foundation for modern macroeconomics

full employment is a special case and is not frequently occuring

incentive to invest is too weak and the urge to hoard cash is too strong

without necessary investment, the economy maximizes the unfull employment which increases productivity

argued that governments had an important management role in macroeconomics

provided a foundation for modern macroeconomics

full employment is a special case and is not frequently occuring

incentive to invest is too weak and the urge to hoard cash is too strong

without necessary investment, the economy maximizes the unfull employment which increases productivity

21

New cards

19th century classical economic ideas

Bentham, Jevon, Menger, Walras

22

New cards

Bentham

utilitarianism - most happiness among greatest number of people

utility - property in any object tends to produce benefits/advantages/pleasure/good/happiness or to prevent the opposite

utility - property in any object tends to produce benefits/advantages/pleasure/good/happiness or to prevent the opposite

23

New cards

Margin

theory of how prices are derived

derived from consuming something

not total utility, but extra utility of consuming

derived from consuming something

not total utility, but extra utility of consuming

24

New cards

Say’s Law

unemployment cannot exist for long periods because production would create its own demand

25

New cards

Jevon’s Paradox

as technological advancements increase efficiency of labour, demand will increase thus not changing efficiency and waste

26

New cards

Carl Menger

subjective theory of value - in an exchange, both parties always profit as they trade something they think is less valuable for something they think is more valuable

27

New cards

Leon Walras

Walras’ Law - the existence of excess supply in one market must be matched by excess demand in another market so that both factors are balanced out

28

New cards

Milton Friedman

economic theory should be subject to empirical corroboration to test its relevance to the real world

prediction is a key factor

not the realism of the assumptions but the accuracy

prediction is a key factor

not the realism of the assumptions but the accuracy

29

New cards

Robert Lucas Jr.

individual’s rational expectations of inflation and government policies

30

New cards

Friedman + Lucas

the role of markets in bringing the economy back to a situation where there is full employment without any government intervention

31

New cards

Free Sector Diagram

Injections - investment (I), government spending (G), exports (X)

Leakages - savings (S), tax (T), imports (M)

if injections = leakages, the economy is in equilibrium/static

Leakages - savings (S), tax (T), imports (M)

if injections = leakages, the economy is in equilibrium/static

32

New cards

Assumptions made in behavioural economic graphs

1. People are rational/consistent

2. Utility is maximized

3. People have access to all information at all times

33

New cards

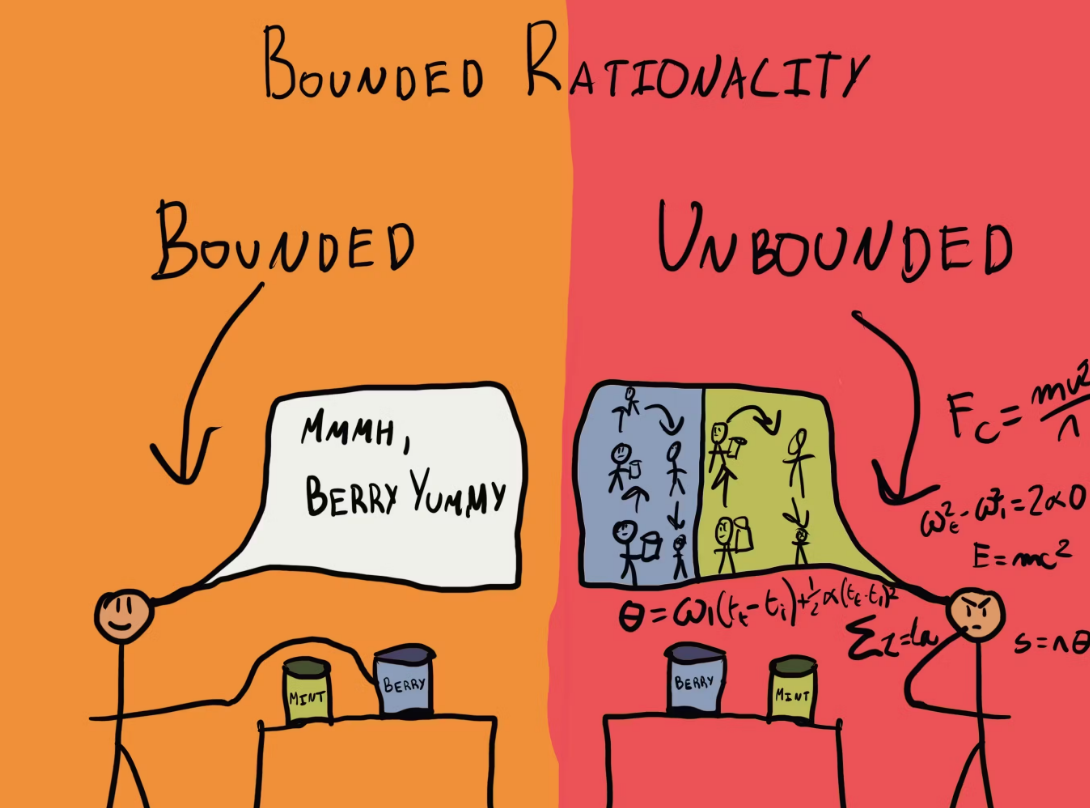

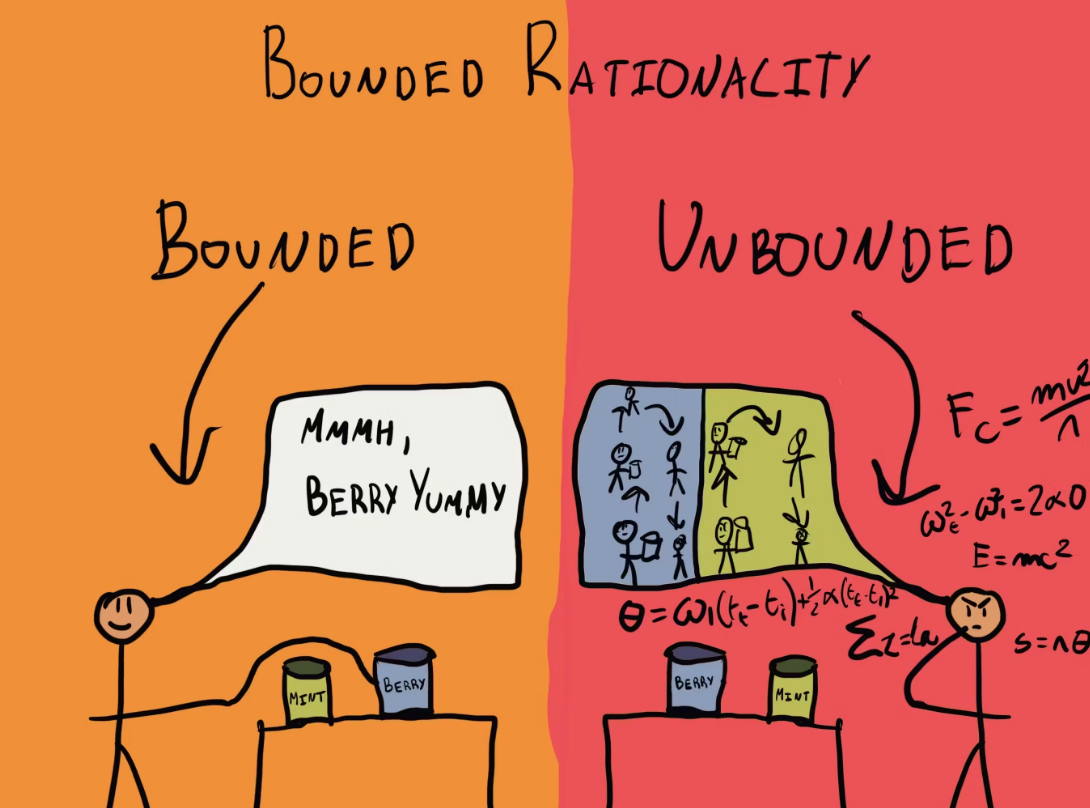

Bounded Rationalism

all rationality is lost past a certain point

34

New cards

Thinking Fast/Slow

heuristics where people use rule of thumb to make quick decisions

35

New cards

Present Bias

people under-invest because the benefits come in the future, and people generally would want benefits in the present

36

New cards

Representative Individual

one person is recorded/measured and “cloned” to create a larger demographic

37

New cards

Nudging

preserving freedom but helping people make decisions when they can’t/don’t (default)

38

New cards

Hot-hand fallacy

belief that a winning streak leads to further success

39

New cards

Bias 1 - overconfidence

a belief that one’s skill/judgement are better than they truly are, or that probability of success is higher than it actually is (health club membership example)

40

New cards

Bias 2 - Hyperbolic Discounting

tendency of people to make the present much more important than even the near future while making economic decisions (example: credit cards)

41

New cards

Bias 3 - Framing effects

Endowment effect - possessing a good makes it more valuable

Loss aversion - a framing bias in which consumers choose a reference point around which losses hurt more than gains feel good

Anchoring - a framing bias in which a person’s decision is influenced by specific pieces of information given

Loss aversion - a framing bias in which consumers choose a reference point around which losses hurt more than gains feel good

Anchoring - a framing bias in which a person’s decision is influenced by specific pieces of information given

42

New cards

Bias 4 - Sunk cost fallacy

the mistake of allowing sunk costs to affect decisions

example: Robert Griffin III (NFL, Washington Redskins)

example: Robert Griffin III (NFL, Washington Redskins)

43

New cards

Degrowth communism

the economy is big enough already, when is the stopping point for growth?

focus growth on more important aspects such as healthcare and not consumption as it raises healthcare costs

focus growth on more important aspects such as healthcare and not consumption as it raises healthcare costs

44

New cards

Interdependence

a consideration of possible economic consequences of interdependences is essential when conducting economic analysis

nothing in the economy is self-sufficient, so they interact with one another (the greater the scale of interaction, the greater the interdependence)

nothing in the economy is self-sufficient, so they interact with one another (the greater the scale of interaction, the greater the interdependence)

45

New cards

Linear economy

Take → make → waste

resource extraction → production → distribution → consumption → disposal

resource extraction → production → distribution → consumption → disposal

46

New cards

Circular Economy

Take → Make/remake → Distribute → Use/re-use/repair → Selectively dispose → Enrich/recycle → Take

aims to minimize waste and promote a sustainable use of natural resources

aims to minimize waste and promote a sustainable use of natural resources

47

New cards

Problems with the circular economy

1. No clear definition (too vague in the definitions and different defitions clash with one another)

2. Ignores scientific principles (you cannot create or destroy matter/energy)

3. Lack of scale (hard to scale up to a global level)

48

New cards

Systems Perspective

taking into account all of the behaviours of a system as a whole in the context of its environment

49

New cards

Economic efficiency

socially constructed concept with its politics and its political implications

public goal, competing with other public priorities

to improve the state of one party, you must hurt another

society gets maximum net benefits

public goal, competing with other public priorities

to improve the state of one party, you must hurt another

society gets maximum net benefits

50

New cards

Eco-efficiency

production of goods/services while using fewer resources and creating less waste and pollution

creating more value through an increase in resource productivity and a decrease in resource intensity

leads to less resource consumption

creating more value through an increase in resource productivity and a decrease in resource intensity

leads to less resource consumption

51

New cards

Economic Well-being

refers to levels of prosperity, economic satisfaction and standards of living among the members of a society