5.5 Break-even analysis

1/5

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

6 Terms

Contribution

the sum of money that remains after all direct and variable costs have been taken away from sales revenue

Contribution per unit

The proportion of the selling price for each unit of product that will go toward paying off total fixed costs

Total contribution

The quantity of product needed to go towards paying off total fixed costs

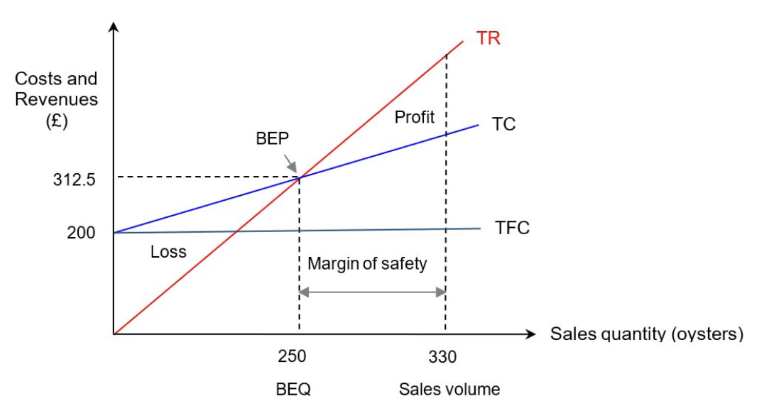

Break-even chart

x-axis : Sales quantity, y-axis : cost and revenue

Target profit quantity

(Fixed cost + Target Profit) / (Price - Average variable cost)

limitations of break-even chart as a decision making tool

Involves assumptions that:

All cost functions are linear

Sales revenue function is linear

All output will be sold

Not useful to a dynamic business environment due to its static nature.

Ignore other quantitative and qualitative factors.