MACRO EXAM 1 (prep from slides)

1/200

Earn XP

Description and Tags

CHAPTERS 2, 3, 4,5,6,7,8,9,10,11

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

201 Terms

Economics

focuses on the behavior and interactions of economic agents.

The study of choices “in the ordinary business of life”

toolkit to understand your decisions and the decisions of others

Microeconomics

Studies individual decisions (consumption, production, etc)

Macroeconomics

Studies aggregate economic phenomena ( Economic growth, inflation, etc)

Cost- Benefit Principle

Compare the costs and benefits of a choice

Choose only if the cost is less than the benefits

This choice generates economic surplus

Willingness to pay

The most I am willing to pay reveals the benefit of the choice

Opportunity Cost

The next best alternative you have to give up to get it

Marginal Benefit(MB)

The extra benefit from one extra unit

Marginal Cost(MC)

The extra cost from one extra unit

Economic surplus

If something is worth doing, keep doing it until your marginal benefits is at least as large as your marginal costs.

Interdependency Principle

Your choice depends on everything and everyone else

Between your individual choices

-Buy a new car — eat out?

Between economic actors

- Buy a white SUV— one less white SUV left for others

Between markets

- Gas price (increases) —> EV?

Through time

- Buy a car now? Next year?

Diminishing MB

MB of each additional unit is smaller than MB of previous unit

Law of demand

The tendency for quantity demanded to be higher when price is lower.

Higher price —> lower quantity demanded

Demand curve

shows how many units I buy for each level of price

Marginal benefit curve shows MB associated with each quantity

Price equals

Marginal benefits ( rule makes them identical)

Downward-sloping demand curve

Reflects diminishing marginal benefit

Law of demand: the tendency for quantity demanded to be higher when the price is lower.

Price change

Causes a movement along the demand curve

Shift in the demand curve: Think about demand for ice cream

What will happen if price falls?

What if temperature rises?

If prices fall or temperature rises, the demand curve shifts to the right. Buy more ice cream at the same price

Shift in the demand curve: Think about demand for ice cream.

What will happen if the temperature falls?

If the temperature falls, the demand shift left, and people buy less ice cream at the same price.

What are Key demand shifters?

Income

Preferences

Price of related goods

Expectations

Congestion and network effects

The type and number of buyers

Demand shifters: Income

In general, quantity demanded for each price(increases) when income(increases)

Demand curve shifts to the right as income (rises)

Normal goods

A good for which higher income causes an increase in demand

Inferior good

A good for which higher income causes a decrease in demand

Examples: Fast-food meals, non-organic fruits and vegetables

Demand shifters 2: Preferences

Changes in your preferences can shift your demand curve

Example:

life altering event

marketing, influencers, and fashion cycles

social pressure

Season/Weather

complementary Goods

Go well with each other.

When the price of one good (increases), the demand for another good (decreases)

Example: Iphone and Iphone cases

Substitute Goods

Are alternative to each other

When the price of one good(increases), the demand for another good(increases)

Example: Coca-Cola Pepsi

Expectations

Whats going to happen in the future can influence your current demand.

Network Effect

More useful because other people use it

Example: Instagram, Snapchat, Facebook

If more people use such a good, your Demand (increases)

Congestion Effect

Less valuable because other people use it

Example: North Avenue during rush hour

If more people use such a good, your demand (decreases)

Increase in demand

A shift of the demand curve to the right.

An increased quantity is demanded at each and every price.

Decrease in demand

A shift of the demand curve to the left.

A decreased quantity is demanded at each and every price.

Demand curve shifts right

Consider the US bicycle market. Illustrate how the demand curve for bicycles will be affected by shifting accompanying graphs.

Bike lane expands nationwide

Demand curve shifts left

Consider the US bicycle market. Illustrate how the demand curve for bicycles will be affected by shifting accompanying graphs.

Subway system improves significantly

Demand curve shifts right

Consider the US bicycle market. Illustrate how the demand curve for bicycles will be affected by shifting accompanying graphs.

Gov’t announces to impose tariffs on bicycles next year

Movement along the demand curve

If the only thing changing is the price of the good itself

changes in price cause changes in quantity demanded

Change in quantity demand

caused only by a change in the price of the good itself. This is movement along the demand curve.

Change in demand

Caused by factors other than the good’s price( like preferences, income, price of related goods, or special occasions)

This is a change in demand

Consumers are buying less candy because cookies are on sale

This is a change in quantity demand

Consumers are buying more candy because its on sale.

Law of supply

The tendency for quantity to be higher when the price is higher.

Higher prices leads to more supply

Movements along the supply curve

if price changes, market supply changes to the point on the curve

price change causes a movement along the supply curve

Key supply shifters

Input prices

Productivity and Technology

Prices of related outputs

Expectations

The type and numbers of sellers

Productivity growth

Producing more output with fewer inputs.

often driven by technological change

New oven with three times more baking racks

Production capacity increases

The supply of baked goods increase

Industrial robots in an automobile factory

Robots make production more efficient

The supply of vehicles increases

Complements-in-production

Are made together

Donut holes and donuts

Your supply of a good (increases) when the price of another good(increases)

Substitutes-in-production

Are alternative use of your resources

Wheat or corn on your farm

Your supply of a good(decreases) when the price of another good(increases)

If new sellers enter the market

Total quantity supplied at each prices increases

supply curve shifts to the right

If sellers exit the market

Total quantity supplied at each price decreases

supply curve shifts to the left

Equilibrium

A stable situation with no tendency for change.

A market is in equilibrium when the quantity supplied equals the quantity demanded.

Equilibrium Quantity

The quantity demanded and supplied in EQBM

Equilibrium Price

The price at which the market is in EQBM

Surplus Pushes the Price down

As price falls

The Quantity demanded rises

The Quantity Supplied falls

Shortage

When quantity demanded exceeds quantity supplied.

The price is below the equilibrium price

A shortage pushes the price up

Surplus

When quantity demanded is less than quantity supplied

Whenever the price is above the equilibrium price, a surplus pushes the price down.

Gains from trade

Efficiency

Access to cheaper/better quality products

Economies of scale

Competition, innovation, knowledge spillovers

Varirty

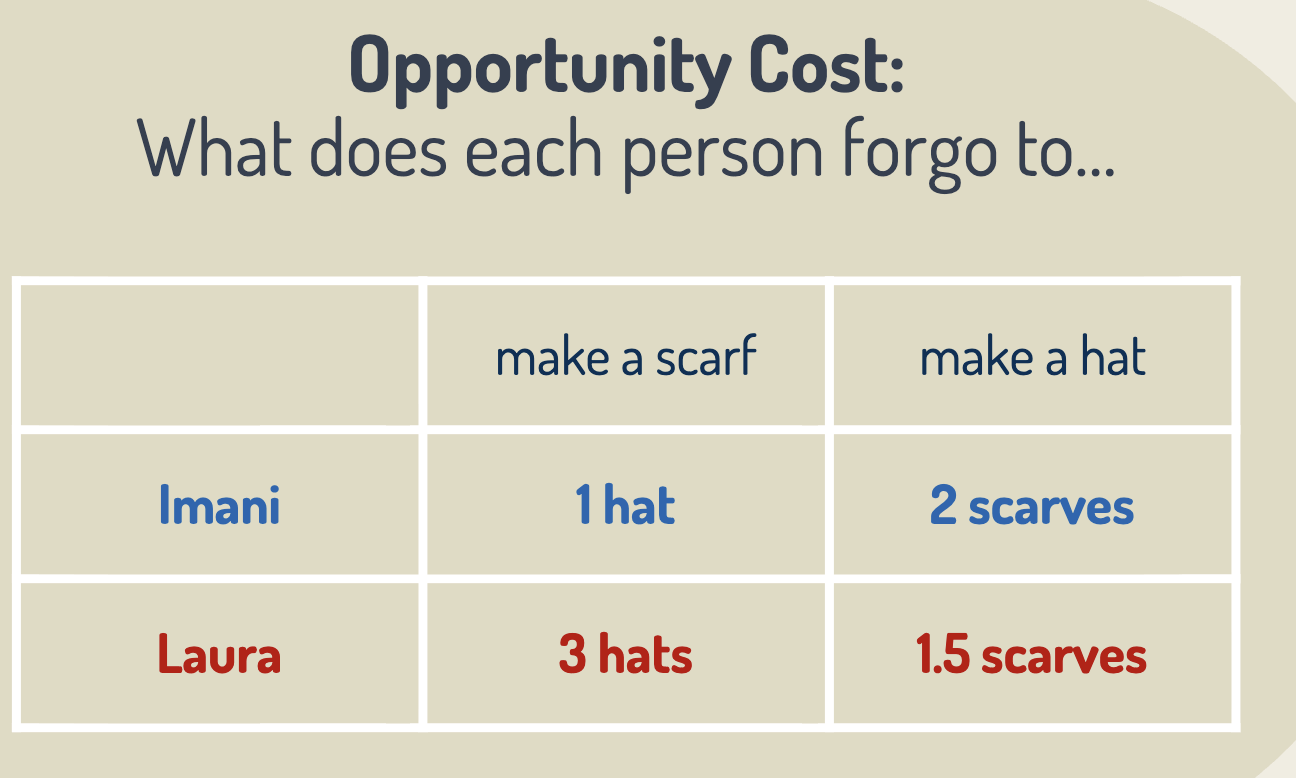

Comparative Advantage

The ability to do a task at a lower opportunity cost

Absolute advantage

The ability to do a task using fewer inputs..

Tells you who is best at a task, Not who should do the task.

Who has a comparative advantage in the production of hats

Laura

Abundant inputs

Sell what you have a lot

Abundant inputs are determined by

Geography, climate, and natural resources

Specialized skills

Countries with similar inputs may have different production techniques.

Unique skills, production methods, or expertise can lower opportunity costs.

Mass Production

Benefits of mass production

(Sometimes called economies of scale)

specialized skills

A source of comparative advantage

Economic Surplus

Consumer surplus+ producer surplus

World supply

Total quantity of a good supplied by all manufactures around the world, at each price.

World Demand

Total quantity of a good demanded by all buyers around the world, at each price.

World price

The price that a product sells for in the global market.

Imports

Domestic consumers are the winners, and domestic sellers are the losers.

Exports

Domestic consumers are the losers, and domestic sellers are the winners

Effect of imports

Domestic price falls

Domestic quantity demanded rises, and domestic quantity supplied falls

Economic surplus rises overall

Effect of exports

Domestic price rises

Domestic quantity demanded falls, and domestic quantity supplied rises

Economic surplus rises overall

GDP

Gross Domestic Product: The market value of all final goods and services produced within a country in a given year.

Market Value

Common unit is necessary—> value each product at its market price.

market price x quantity

Circular flow of income and Resources

Households and businesses are interconnected through input/output markets

Input market

Households sell labor and businesses buy labor

Output Market

Households buy products and buisnesses sell products.

Y=

GDP

C=

Consumption

I=

Investment

G=

Government purchases

NX=

Net Exports

Consumption

household spending on final goods and services.

Clothes, shoes, food, gas, internet bill, haircuts, cars.

Rent and imputed rent (for house owners)

Investment

Spending on new capital, assets that increase the economy’s productive capacity.

Any long-lasting good used in a business

Research and development spending, office furniture, equipment

Government purchases

Government purchases of goods and services

spending on schools, highways, military

Excluded transfer payments: payments that transfer income from one person to another

Net exports

Spending on exports minus spending on imports

Exports

goods or services produced domestically and purchased by foreign buyers.

Imports

goods or services produced overseas and purchased by domestic buyers.

Value added

the amount by which the value of an item is increased at each stage of production.

total spending

Y=C+I+G+NX

Total output

Y={value added

Total income

{(labor income + capital income)

Limitations of GDP

Market prices (cannot equal) Our values

Non-market activities are excluded

The shadow economy is missing

Environmental degradation isn’t counted.

Leisure doesn’t count

GDP ignores distribution

GDP ignores distribution

GDP measures the size of pie, not how they are distributed.

Leisure doesn’t count

GDP counts the benefit of work but omits the cost of work

Extra work—> less time to spend with family or friends

Environmental degradation isn’t counted

Natural resources have no value until transformed into something else

GDP ignores the costs of environmental degradation

Example: Forest→ Lumber

New cars → pollution

The shadow economy is missing

Economic activities out of view of the government are missing

Non-market activities are excluded

Doing your own laundry

cooking your own meals

raising and taking care of your child(or pet)

Market prices (cannot equal) our values

GDP is the market value of all final goods or services

benefit > price if you enjoy economic surplus

Nominal GDP

GDP measured in today’s prices

Useful for analyzing what GDP is right now, based on the prices you face right now.

What is the nominal GDP for this year and last year?

Last year, your local grocery store sold milk for $3.40 per gallon. This year, that same gallon of milk is priced at $4.20

Last year’s nominal GDP will use $3.40 per gallon.

This year’s nominal GDP will use $4.20 per gallon.

Real GDP

GDP measured in constant prices

excludes the effects of price changes

measures the real change in production.

focuses on changes int he quantity produced