economics paper 1

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

15 Terms

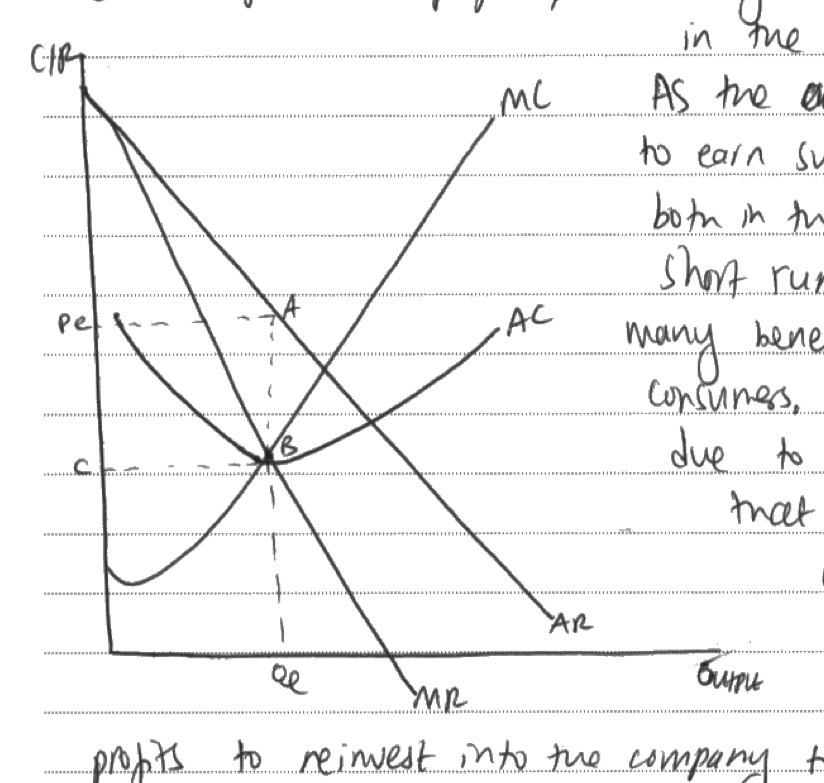

How do you use a monopoly cost and revenue diagram to find output, price, and profit?

Output/ equilibrium

MC = AR (profit max output)

Price

Go up to AR from output to show price

Profit

AR > AC supernormal profit

AR = AC normal profit

AR < AC loss

Way to remember MICRO effects for CPM

Consumers = PCCS

Price

costs rise or supply falls → firms raise prices → consumers have to pay more → some consumers buy less → consumer welfare falls

more competition → firms cut prices → consumers can buy at a lower cost → real purchasing power rises → consumers benefit

Choice

more firms enter the market → greater competition and product differentiation → consumers have more options → consumers are more likely to find a product that suits their preferences → consumer welfare rises

firms leave the market or a monopoly grows → fewer products become available → consumers have less choice → satisfaction may fall

Consumer surplus

price falls while willingness to pay stays the same → consumers pay less than they were prepared to pay → the gap between willingness to pay and actual price increases → consumer surplus rises

price rises → consumers pay closer to or above what they were happy to pay → the benefit they gain from each purchase falls → consumer surplus falls

Satisfaction/ welfare

quality improves or prices fall → consumers get better value for money → more utility is gained from consumption → consumer welfare rises

prices rise, quality falls, or choice shrinks → consumers gain less benefit from consuming the product → satisfaction and welfare fall

Producers = CRAP 🐒💩

Costs

a tax or wage increase raises business expenses → cost of production rises → AC and MC increase → firms output will decrease or prices may rise

a subsidy, better technology, or lower raw material prices reduce expenses → costs fall → firms can produce more cheaply → profitability may improve

Revenue

demand rises → firms sell more output (at a higher price?) TR increases

demand falls → fewer units are sold → TR falls → firms may have less money to reinvest

(Depends on PED)

Abnormal profit

Productivity/ production

investing in training or tech improves efficiency → workers produce more per hour → productivity rises → unit costs may fall → firms become more competitive

higher costs or weaker demand → firms reduce output → less production → eos may be lost → average costs may rise

Market = PECS 🐣(when u try to enter a market u PEC at the shell out of your comfort zone)

Price

the equilibrium price

Efficiency

Allocative efficiency

Price moves closer to marginal social cost or marginal cost → output is closer to what consumers and society actually want → resources are allocated better → allocative efficiency improves

Productive efficiency

Firms cut waste or gain economies of scale → average costs fall → goods are produced at lower cost → productive efficiency improves

Dynamic efficiency

Firms invest in R&D or innovation → better products and production methods develop over time → long-run efficiency improves

Competition

barriers to entry fall → more firms enter the market → competitive pressure increases → prices may fall and quality may rise

one firm gains strong market power → rivalry weakens → prices may rise and choice may fall → consumers may lose out

Supply and demand/ Sales

the amount of sales

Monopsony (labour)

Definition: where there’s only one buyer in the market

Irl when economists talk about monopsonies it means a firm has some level of monopsony power

This gives them control over the price or wage

Example: NHS, teachers

Supermarkets is also an example as they collude together to act as a monopsony

LABOUR

Lower wages/ prices → reduce costs → maximise profits

Government policies/ ways to fight monopsony power

NMW/: set above equilibrium → excess supply or unemployment for over-25s in the UK the NMW is £7.50

Trade unions: a group of workers who collectively bargain to improve employee welfare (used as NMW does not effect working conditions) → for example NUT (national union of teachers, shorter hours and higher pay)

Maximum wages: eg for footballers → many activists have suggested the maximum wage within a company could be set at 20x the lowest wage

Occupational and geographical immobility (in labour as workers have fewer alternatives so the employer has more power over them)

IN GENERAL

Regulations

Minimum price

Effect of monopsonies

On suppliers: lower revenue and profit, less investment, risk of exit, lower dynamic efficiency, pressure to cut costs

On consumers: lower prices/ affordability, lower quality, less choice

Evaluation: depends of whether lower costs are passed on, increases efficiency, not pure monopsony so exploitation is limited, depends on elasticity of supply (labour), short run/long run effects, gov intervention may reduce damage, depends on size of suppliers, reduce dynamic efficiency,

Information gaps: incomplete information, asymmetric information

Information gaps: when consumers or producers lack the information needed to make an informed decision

Information gaps happen when consumers or producers do not have full information, so they make poor decisions. This can cause market failure because goods may be overconsumed, underconsumed, overproduced, or underproduced. As a result, resources are misallocated and allocative efficiency falls.

Incomplete information: when someone doesn’t have full information about the benefits or costs of their decision

Asymmetric information: when one party knows more than another party in a transaction

Information gaps happen when consumers or producers do not have full, accurate, or clear information, so they make uninformed decisions.

Why they matter:

They can cause market failure because the wrong amount of a good is consumed or produced, so resources are misallocated and allocative efficiency falls.

Core chain:

Information gap → poor decision-making → overconsumption / underconsumption / overproduction / underproduction → market failure

Consumer information gaps:

consumers may not understand the risks of a product

consumers may not know the true quality of a product

consumers may misunderstand labels

consumers may underestimate long-term costs or benefits

Producer information gaps:

firms may misjudge consumer demand

firms may produce too much or too little

overproduction can lead to waste

lack of market knowledge can reduce efficiency

Examples:

Merit goods: consumers underestimate benefits, so they underconsume

Demerit goods: consumers underestimate harm, so they overconsume

Food waste: consumers misunderstand best before and use by, or producers overestimate demand

Merit goods chain:

Consumers underestimate benefits → demand too low → underconsumption → market failure

Demerit goods chain:

Consumers underestimate harm → demand too high → overconsumption → market failure

Food waste chain:

Consumers/producers lack information → poor decisions or overproduction → food is wasted → resources are misallocated

Main efficiency problem:

Information gaps lead to allocative inefficiency.

Evaluation:

it may not just be information gaps; sometimes it is irrational behaviour

government may try to fix the problem through better labelling, education, advertising, regulation, taxes or subsidies

the extent depends on the product and how informed consumers/producers are.

Irrational behaviour

Irrational behaviour is when consumers make decisions that are not in their own best interests, even when they have enough information.

Why it matters:

It can cause market failure because consumers may make poor choices, so resources are misallocated and allocative efficiency falls.

Core chain:

Irrational behaviour → poor choices → overconsumption / inefficient decisions → market failure

Examples of irrational behaviour:

impulse buying

overconsumption

poor self-control

present bias

addiction or habit

ignoring long-term consequences

Difference from information gaps:

Information gaps = consumers do not know enough

Irrational behaviour = consumers may know the facts but still choose badly

Main efficiency problem:

Irrational behaviour leads to allocative inefficiency because too many or too few resources are allocated to certain goods and services.

Evaluation:

sometimes the problem is information gaps, not irrational behaviour

irrational behaviour is more important in some markets than others

government can try to reduce it using taxes, nudges, regulation, or education

however, government policies may not fully change consumer behaviour

Merger

A merger is when two firms join together to become one business.

Why firms merge:

increase market share

reduce competition

gain economies of scale

increase profit

enter new markets

gain more market power

Types of merger:

Horizontal merger

two firms in the same industry and at the same stage of production merge

example: two supermarkets merge

Vertical merger

two firms at different stages of production merge

example: a manufacturer merges with a supplier

Conglomerate merger

two firms in different industries merge

example: a food company merges with a clothing company

Advantages of mergers:

economies of scale

greater market power

lower average costs

removal of duplication

possible survival against bigger rivals

Disadvantages / problems of mergers:

integration costs: legal, rebranding, retraining, management time spent reorganising the business

rationalisation costs: redundancy payments, reconstructing departments

diseconomies of scale

reduced competition

higher prices

less choice

regulatory scrutiny

Useful chain:

Merger → larger market share → less competition → more market power → possible higher prices / lower choice

Evaluation:

economies of scale may take time

the firm may become too large and suffer diseconomies of scale

lower costs may not be passed on to consumers

competition authorities may block the merger

some mergers may help firms compete more effectively

How do you label and use a monopoly cost and revenue diagram?

Pmax = MC = MR → stack up to P

Pallo = P = MC (the value consumers place on the last unit produced is equal to the opportunity cost of the resources used to make it. This shows the socially optimal level of output.)

Pprod = when AC is at its lowest

What are the main types of efficiency in economics and how do you apply them?

1. Allocative efficiency

producing the right quantity

occurs where P = MC

means consumer benefit from the last unit equals the cost of producing it

if price is above marginal cost, too little is being produced

How to apply it:

monopoly: usually allocatively inefficient because it produces where MC = MR, not P = MC

taxes/subsidies: can reduce or improve allocative efficiency depending on whether output moves closer to the socially efficient level

externalities: government intervention may improve allocative efficiency by correcting overconsumption or underconsumption

2. Productive efficiency

producing at the lowest average cost

occurs where AC is at its lowest point

means the firm is producing as cheaply as possible per unit

How to apply it:

mergers: economies of scale may lower AC and improve productive efficiency

monopoly: may be productively inefficient if it does not produce at minimum AC

competition: can force firms to cut costs and become more efficient

3. Dynamic efficiency

efficiency over time

happens when firms invest in innovation, R&D, training, and new technology

means products and production methods improve in the future

How to apply it:

monopoly: may be dynamically efficient if supernormal profit is invested in innovation

mergers: larger firms may have more funds for research and development

monopsony: squeezing supplier profits may reduce investment and lower dynamic efficiency

4. X-inefficiency

waste, slack, or poor cost control due to lack of competition

happens when firms become complacent and do not try hard enough to minimise costs

How to apply it:

monopoly: may become X-inefficient because there is little competitive pressure

competition: can reduce X-inefficiency by forcing firms to become leaner and more efficient

How to know which one to use in an essay:

price/output problem → allocative efficiency

costs/economies of scale → productive efficiency

innovation/investment → dynamic efficiency

lack of competition/complacency → X-inefficiency

How many KAA and EV marks are in a 5, 8, 10, 12, 15 and 25 markers and what the structure is for each

5 = 2K, 2Ap, 1An

8 = 2K, 2An, 2Ap, 2 EV

10 = 6 KAA + 4 EV

12 = 8 KAA + 4 EV

15 = 9 KAA + 6 EV

25 = 16 KAA + 9 EV

Evaluation points for micro

Use DEPTHS:

D = Depends on the scale / size

depends on how big the tax, subsidy, merger, market power, or intervention iS

E = Elasticity

depends on PED, PES, XED, or elasticity of labour supply

P = Passed on or not

depends on whether lower costs or higher costs are passed on to consumers

T = Time period

short run and long run effects may be different

H = How far behaviour changes

depends on whether consumers, firms, or workers actually respond

S = Substitutes / side effects / government failure

depends on availability of substitutes, unintended consequences, or policy failure

This may be limited if there are close substitutes.

However, the policy may create unintended consequences.

Government failure may occur if the policy is badly designed or hard to enforce.

Measures of inflation

The main measures of inflation are:

CPI = Consumer Prices Index

RPI = Retail Prices Index

CPI (Consumer Prices Index)

the main official measure of inflation in the UK

measures the average change in the price of a weighted basket of goods and services

used to track changes in the cost of living over time

does not include mortgage interest payments

Definition:

CPI measures the average change in the price of a weighted basket of goods and services over time.

RPI (Retail Prices Index)

an older measure of inflation

also measures changes in the price of a basket of goods and services

includes some housing-related costs, such as mortgage interest payments

usually gives a higher inflation rate than CPI

Definition:

RPI measures changes in the price of a basket of goods and services, including some housing costs such as mortgage interest payments.

Basket of goods and services

a sample of products that reflects typical household spending

includes items such as food, clothing, transport, entertainment, and bills

is updated over time to reflect changes in consumer habits

Weighted index

different items are given different weights based on how important they are in average household spending

goods people spend more money on have a larger effect on the inflation measure

for example, housing or transport usually has a bigger weight than small everyday items

Why weights matter:

They make the measure more realistic because not all products are equally important.

Evaluation / limitations of inflation measures

they are only averages, so they may not reflect the experience of every household

different groups have different spending patterns, so inflation may feel higher or lower for different people

the basket and weights may not perfectly reflect all consumers

quality changes are difficult to measure, because a price rise may reflect improvement rather than pure inflation

new goods take time to be added to the basket

CPI and RPI can give different results because they include different items

PED + factors that effect it

PED > 1 = elastic

PED < 1 = inelastic

PED = 1 = unitary elastic

Usually negative because price and quantity demanded move in opposite directions

SPLAT

S — Substitutes

The more close substitutes, the more elastic demand.

P — Proportion of income

If a good takes up a large share of income, demand is more elastic.

L — Luxury or necessity

Luxuries tend to be elastic; necessities tend to be inelastic.

A — Addiction / habit / brand loyalty

Addictive goods and goods with strong brand loyalty tend to be inelastic.

T — Time period

Demand is usually more inelastic in the short run and more elastic in the long run because consumers have more time to adjust.

What is the difference between revenue and sales maximisation

Rmax = maximise money coming in → MR = 0

Smax = maximise quantity sold → AR = AC

Draw a monopoly diagram with Pmax, cost and profit shown