final exam

0.0(0)

Card Sorting

1/118

There's no tags or description

Looks like no tags are added yet.

Last updated 11:06 PM on 4/30/23

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

119 Terms

1

New cards

The central problem of economics is the

fact that human wants exceed the availability of resources

2

New cards

\

Because of scarcity,

Because of scarcity,

Both choices must be madeand there are not enough goods to satisfy everyone. \n

3

New cards

Opportunity cost may be defined as the

value of the most desired goods or services that are forgone to obtain something else

4

New cards

Factors of production are

the resources used to create output.

5

New cards

Based on the figure, if a student wants to achieve a grade-point average of 3.0, he or she should study an average of

30 hours per week

6

New cards

Which of the three basic economic questions deals with choosing the correct mix of \n output?

what to produce

7

New cards

GDP is the total value of all _________ goods and services produced within a nation's \n borders in a given time period

**final**

8

New cards

Economic growth

is an increase in output or real GDP

9

New cards

_________GDP is adjusted for inflation

Real

10

New cards

Nominal GDP is affected by changes in

output and prices

11

New cards

\

A market exists for the sale and purchase of.

A market exists for the sale and purchase of.

\

\n D) illegal drugs, computer services, and nuclear warheads.

\n D) illegal drugs, computer services, and nuclear warheads.

12

New cards

Market participants include

consumers, business firms, governments, and foreigners.

13

New cards

A movement along the supply curve is the same as a

change in the quantity supplied

14

New cards

\

If supply is unchanged, a decrease in the demand for soft drinks will cause equilibrium price to

If supply is unchanged, a decrease in the demand for soft drinks will cause equilibrium price to

\

\n B) fall and equilibrium quantity to fall.

\n B) fall and equilibrium quantity to fall.

15

New cards

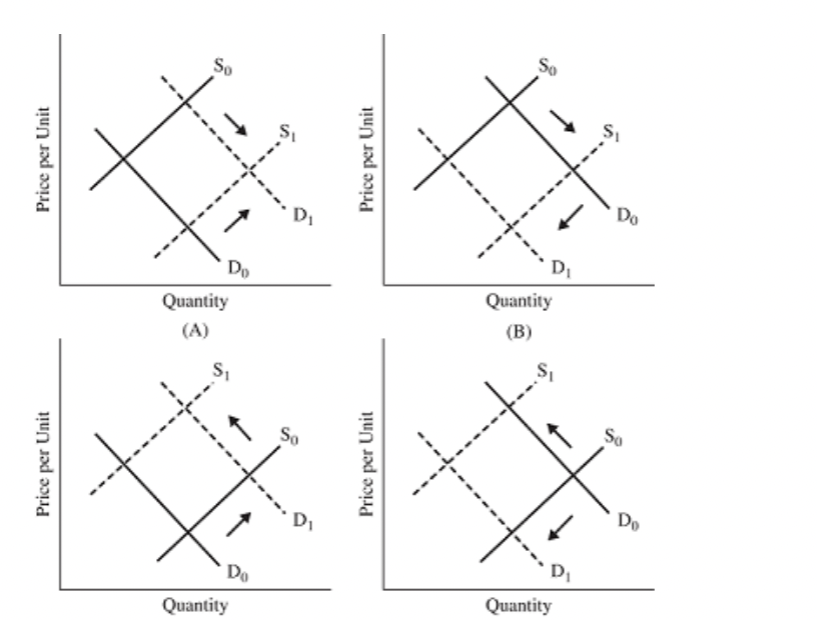

Which panel represents the changes in the market for beef when the price of corn (cattle feed) \n rises and the Surgeon General reports that red meat contributes to coronary disease?

D

16

New cards

A market shortage occurs when

the market price is below equilibrium.

17

New cards

\

A price ceiling does all of the following except

A price ceiling does all of the following except

\

\n B) create excess supply.

\n B) create excess supply.

18

New cards

Which of the following would not cause the market supply of cell phones to change?

A reduction in the desire for cell phones causes the price to fall.

19

New cards

The law of demand states that

price and quantity demanded are inversely related

20

New cards

The pleasure or satisfaction obtained from goods and services is known as

utility.

21

New cards

The law of demand and the law of diminishing marginal utility are related since both

assume that the first units consumed have more utility than subsequent units.

22

New cards

When income changes, there is a _________ the _________ curve

shift of; demand

23

New cards

The price elasticity of demand is defined as the

percentage change in quantity demanded divided by the percentage change in price

24

New cards

If demand is inelastic, then

quantity demanded is not very responsive to changes in price

25

New cards

A good whose demand is not very responsive to a change in price is

inelastic

26

New cards

If the price elasticity of demand is 0.5 and a firm raises its price by 10 percent, the total \n revenue will

elastic

27

New cards

If the price elasticity of demand is 0.5 and a firm raises its price by 10 percent, the total \n revenue will

rise by 5 percent

28

New cards

The objective of advertising, from an economic perspective, is to shift the demand curve \n to the

right and decrease price elasticity of demand

29

New cards

Which of the following does not influence the price elasticity of demand?

the costs of production

30

New cards

An investment in human and nonhuman capital will result in

an increase in the marginal physical product of labor

31

New cards

A production function describes

he maximum amount of output attainable from a given combination of factor inputs

32

New cards

If the first, second, third, and fourth worker employed by the firm add 15, 21, 12, and 8 \n units of total product respectively, we can conclude that

after the second worker marginal product declines

33

New cards

Profit is the difference between

total revenue and total cost

34

New cards

When producing jeans, which of the following are not a variable cost in the short run?

rent paid for the use of a factory

35

New cards

Marginal cost is equal to

he change in total cost divided by the change in output

36

New cards

Refer to the figure. What is the marginal cost of the 12th unit of output

$72 per unit

37

New cards

As output increases, fixed costs

do not change

38

New cards

The long run refers to

a period of time long enough for all inputs to be varied

39

New cards

Economic cost is

\

he value of all resources, both explicit and implicit, used to produce a good or \n service.

he value of all resources, both explicit and implicit, used to produce a good or \n service.

40

New cards

The number and relative size of firms in an industry define the type of

market structure.

41

New cards

Market structure is determined by

he number and relative size of firms in a specific market

42

New cards

Competitive firms cannot individually affect market price because

their individual production is insignificant relative to the production of the industry

43

New cards

Which of the following is characteristic of a perfectly competitive market?

There are low barriers to entry

44

New cards

\

If the market price is $50, marginal cost equals $45, and average total cost equals $40, \n the firm should

If the market price is $50, marginal cost equals $45, and average total cost equals $40, \n the firm should

increase output

45

New cards

If marginal cost equals price, then _________ is at a maximum

profit

46

New cards

In which of the following industries is the firm referred to as a price taker?

perfect competition

47

New cards

High profits in a perfectly competitive industry indicate that consumers would like

more of that industry's goods

48

New cards

\

In a perfectly competitive industry

In a perfectly competitive industry

marginal cost equals price.

49

New cards

A horizontal demand curve for a firm indicates that

the firm has no market power

50

New cards

Which of the following is true for a monopolist?

Profit is maximized at a production level where marginal cost equals marginal \n revenue

51

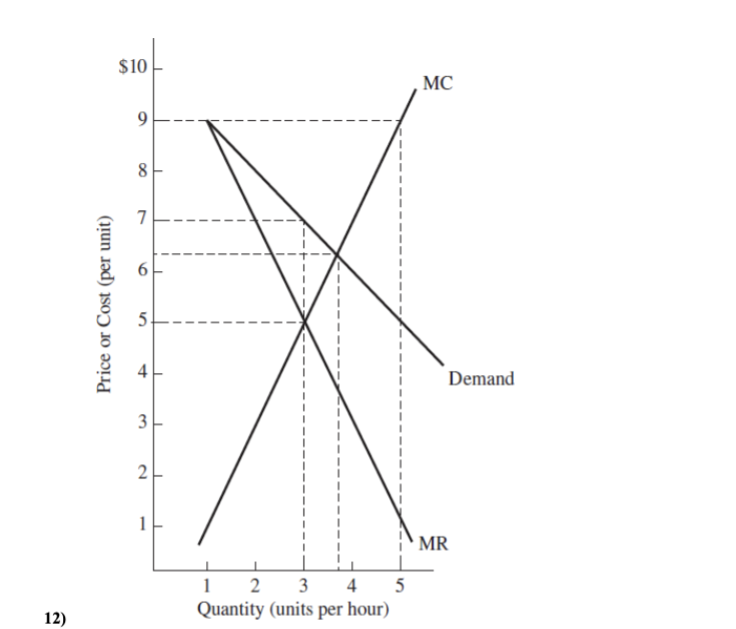

New cards

Refer to the figure. The profit-maximizing level of output for this monopolist is

3 units per hour

52

New cards

firm were forced to behave as if it were in a perfectly competitive market, the profit-maximizing \n price would be

between $6 and $7 per unit

53

New cards

How do monopolists set the output level and price for their products?

Output is set at the intersection of marginal revenue and marginal cost, while price is \n set based on the demand curve

54

New cards

A monopolist

charges a higher price than a competitive firm, ceteris paribus

55

New cards

Under both monopoly and perfect competition, a firm

operates where marginal revenue equals marginal cost.

56

New cards

Which of the following is not consistent with a monopoly industry?

Many firms produce identical or similar products.

57

New cards

Monopolists are price

makers, but perfectly competitive firms are price takers

58

New cards

An industry dominated by one firm is

a monopoly

59

New cards

The market structure for the airline industry is determined by

he number of carriers servicing a given route

60

New cards

A monopolist sets its price

on the demand curve, at the rate of output where marginal revenue equals marginal cost

61

New cards

Obstacles that make it difficult or impossible for would-be producers to enter a market \n are known as

barriers to entry

62

New cards

An industry in which only two firms compete to supply a particular product is best \n characterized by which of the following market structures?

duopoly

63

New cards

Which of the following is an example of monopolistic competition?

Many firms supply similar products, each with some consumers who show significant \n brand loyalty

64

New cards

If a firm can change market prices by altering its output, then it

faces a horizontal demand curve

65

New cards

The demand for labor is a derived demand because

we demand what labor produces and not labor itself

66

New cards

A firm should continue to hire workers until the marginal revenue product is equal to

the market wage rate

67

New cards

A minimum wage impacts the labor market by causing

an increase in the quantity of labor supplied and a decrease in the quantity of labor \n demanded.

68

New cards

Unions are able to maintain above-equilibrium wages by

excluding some workers

69

New cards

The opportunity cost of working is the

value of leisure time that is given up in the process

70

New cards

A market failure means that the economy is definitely producing

a suboptimal mix of output.

71

New cards

The optimal mix of output is

the most desirable combination of output attainable with existing resources, \n technology, and social values

72

New cards

A private good is unique because

nonpayers can be prevented from consuming it

73

New cards

Which of the following is most likely a private good?

cars

74

New cards

A public good is

the source of the free-rider dilemma

75

New cards

Public goods

can be consumed by more than one person at the same time

76

New cards

Which of the following is most likely a public good

a park

77

New cards

Externalities are the

generate a gap between social costs or benefits and private costs or benefits

78

New cards

If a good generates an external cost, the market will produce

too much of the good

79

New cards

The term externalities refers to

all costs and benefits of a market activity borne by a third party

80

New cards

Alternating periods of growth and contraction in real GDP define

the business cycle

81

New cards

Which of the following is a basic measure of macroeconomic performance?

growth in output

82

New cards

GDP is defined as

he market value of all final goods and services produced in a country in a year

83

New cards

A recession is technically _________ quarters or more of declining output or real GDP

2

84

New cards

The unemployment rate is calculated by dividing

the number of unemployed by the size of the labor force and multiplying by 100

85

New cards

According to the Population and Labor Force Data table, what is the unemployment rate in \n Year 10?

10\.00 percent

86

New cards

Joseph is unemployed. He was working at a thrift shop in Indiana but decided to go back to \n school full time to become an engineer. He would be classified as

not in the labor force

87

New cards

Unemployment that occurs when there are not enough jobs for the number of people in the \n labor force is referred to as

cyclical unemployment

88

New cards

According to macroeconomists, a goal for the economy is

zero cyclical unemployment.

89

New cards

Price stability refers to

the absence of significant changes in the average price level

90

New cards

The difference between market demand and aggregate demand is that

aggregate demand applies to all goods and market demand applies to a specific good

91

New cards

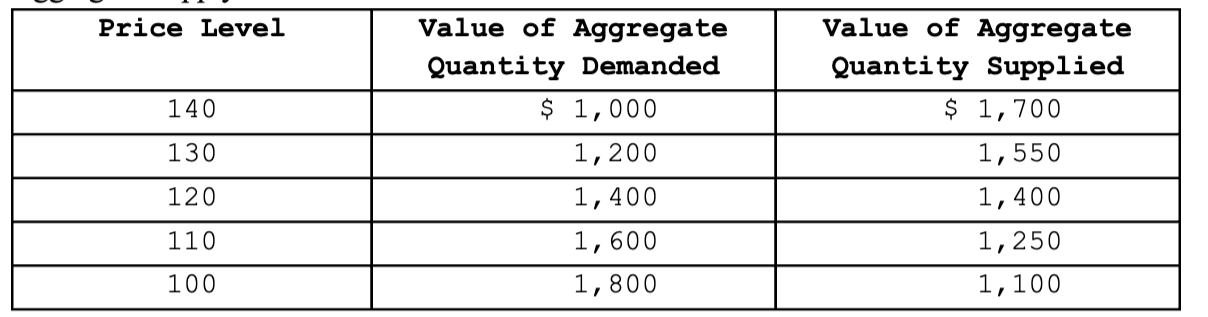

According to the Aggregate Supply and Demand table, at what output level does macro \n equilibrium occur?

$1,400

92

New cards

What fiscal policy tools are used to shift the aggregate demand curve?

government spending and taxes

93

New cards

Inflation occurs when

aggregate demand increases faster than output

94

New cards

Expenditures by households on final goods and services is referred to as

consumption

95

New cards

When money is used to pay for goods and services, it is functioning as a

medium of exchange

96

New cards

Money is functioning as a store of value when you

decide to save your cash to pay for tuition next semester

97

New cards

Money creation occurs when

banks make loans to borrowers

98

New cards

Banks are most profitable when

loans are initiated

99

New cards

The key decision-maker for U.S. monetary policy ise

the Board of Governors

100

New cards

Which of the following is not a basic monetary policy tool used by the Fed

the income tax rate