ap micro

1/234

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

235 Terms

Scarcity

Unlimited wants, limited resources

Land

Scarce resource: Natural resources

Labor

Scarce resource: physical labor, skill, amount of effort put into a task by paid workers

Capital

scarce resource: Monetary value- divided into physical and human

Physical capital

Tools/goods used to produce other good/service

Human capital

Education and training an individual has that is used in the production of a good/service

entrepreneurship

scarce resource: ability to create a business

fixed resources

resources that remain constant regardless of the level of production or activity

opportunity cost

things u give up in order to buy a good/service

if there’s an opportunity cost, the good is scarce

how do u know if an item is scarce?

if theres not enough of it for everyone who wants it

trade- off

things u lose in order to use a scarce resource

scarcity vs shortage

scarcity: less available than ppl want

shortage: quantity supplied is less than quantity demanded at the current price

how do we decide who are the consumers?

command- someone in charge decides

and prices

traditional economy

“what, how, and whom to produce for” are all determined by cultural traditions

market economy

“what, how, and whom to produce for” are all determined by individuals and prices (private businesses/capitalism)

command economy

“what, how, and whom to produce for” are all determined by the gov (communism)

what kind of economy does the U.S. have?

a mixed economy of all three

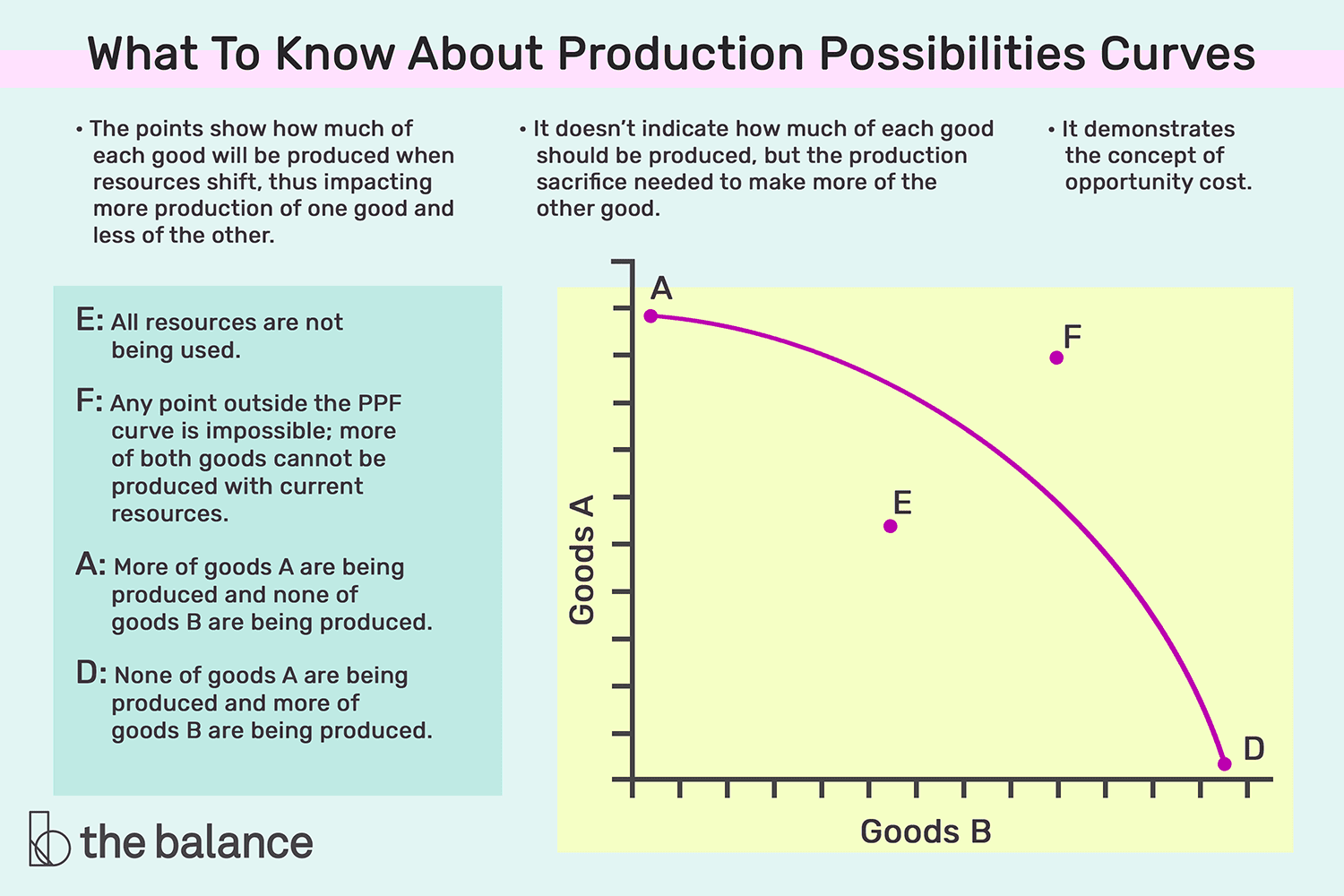

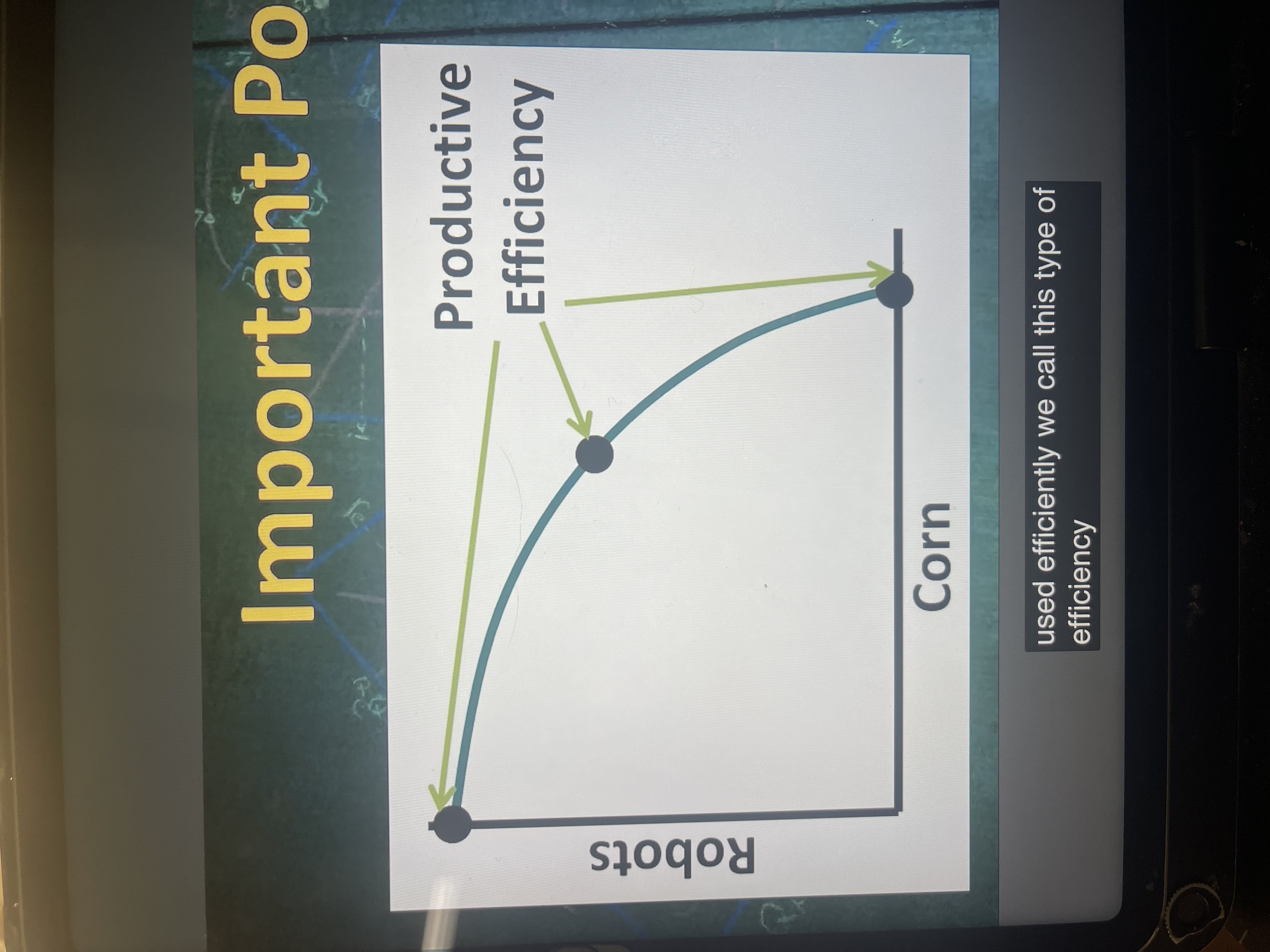

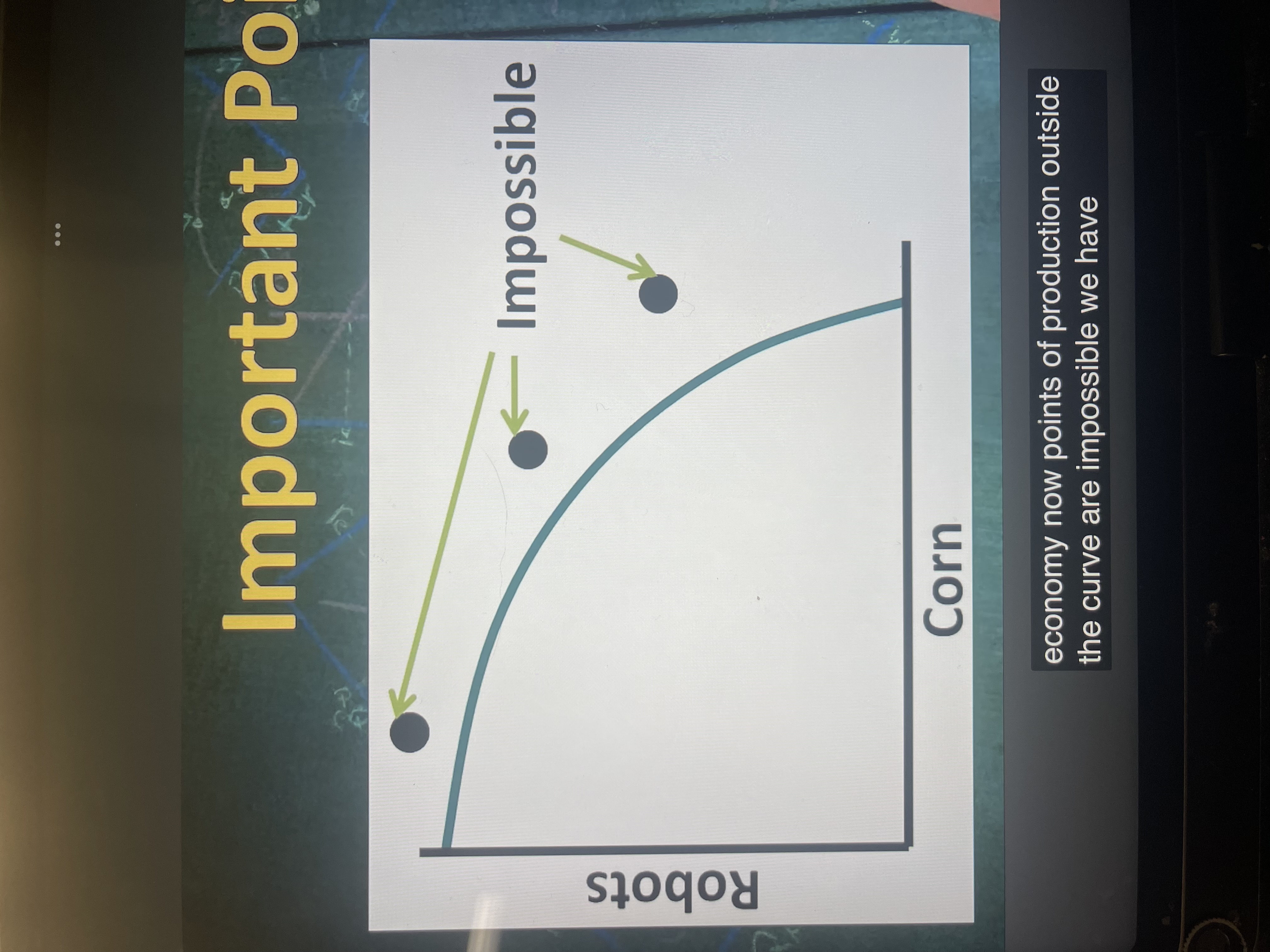

production possibilities curve (PPC)

a graph that shows all combinations of 2 goods that can be produced with fixed resources

productive efficiency on PPC

the points r on the curve, meaning it’s an efficient use of resources

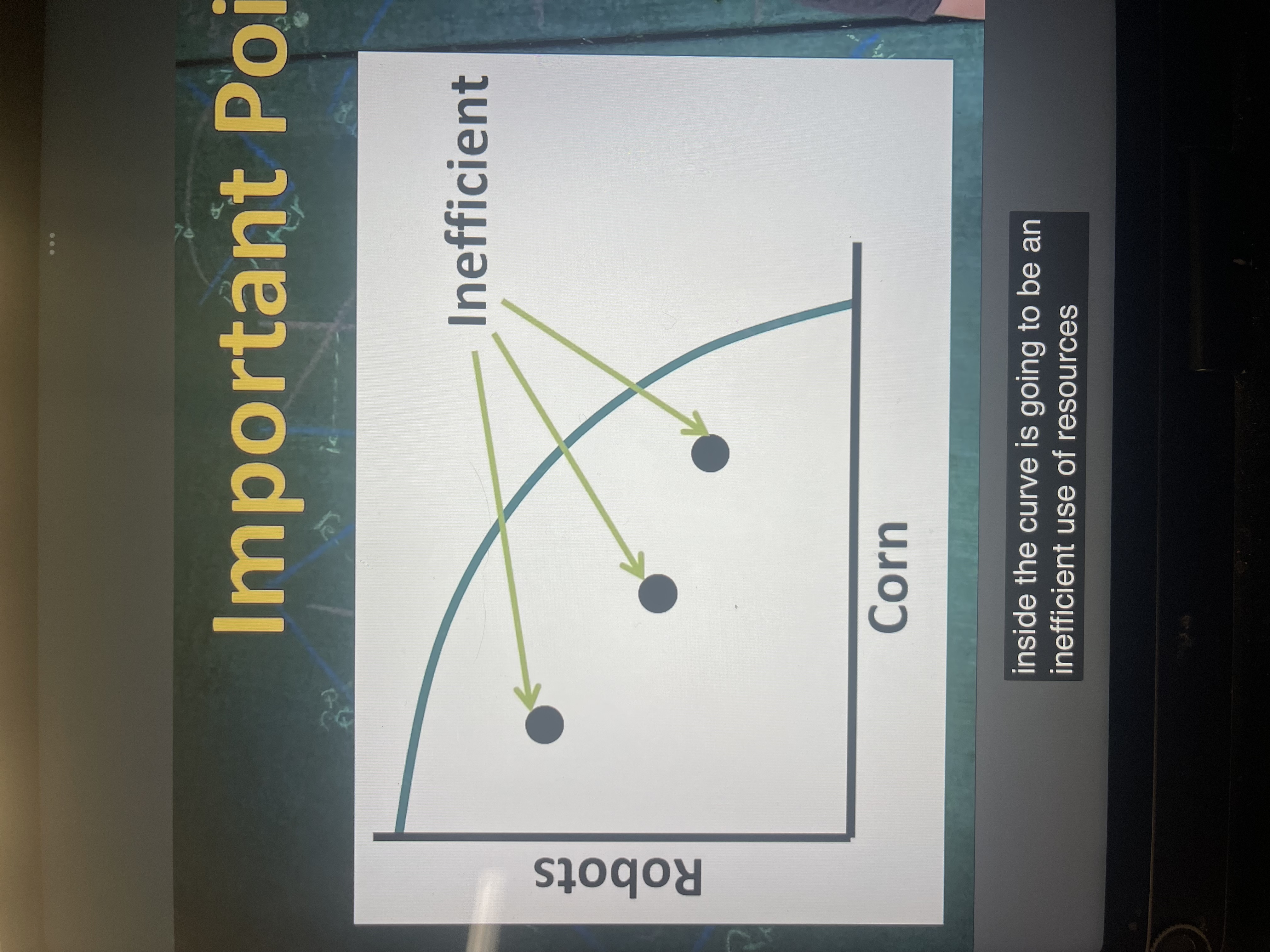

inefficient use on PPC

points on the inside of the curve, meaning some resources are not being used to its full potential

impossible points on PPC

points outside of the curve, meaning they’re beyond this economy’s possible production

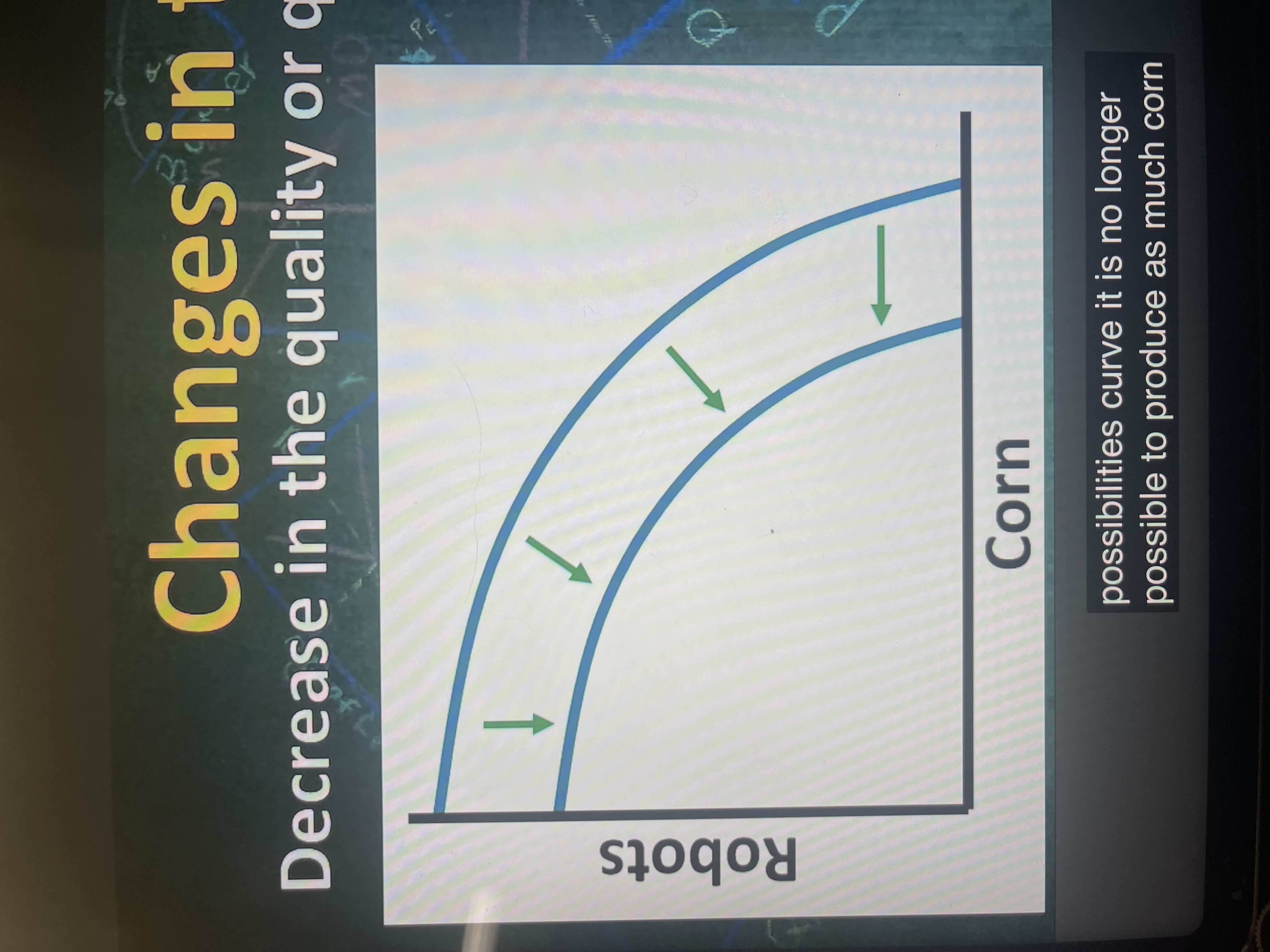

a shift inward of a PPC means..

a decrease in the quality or quantity of resources

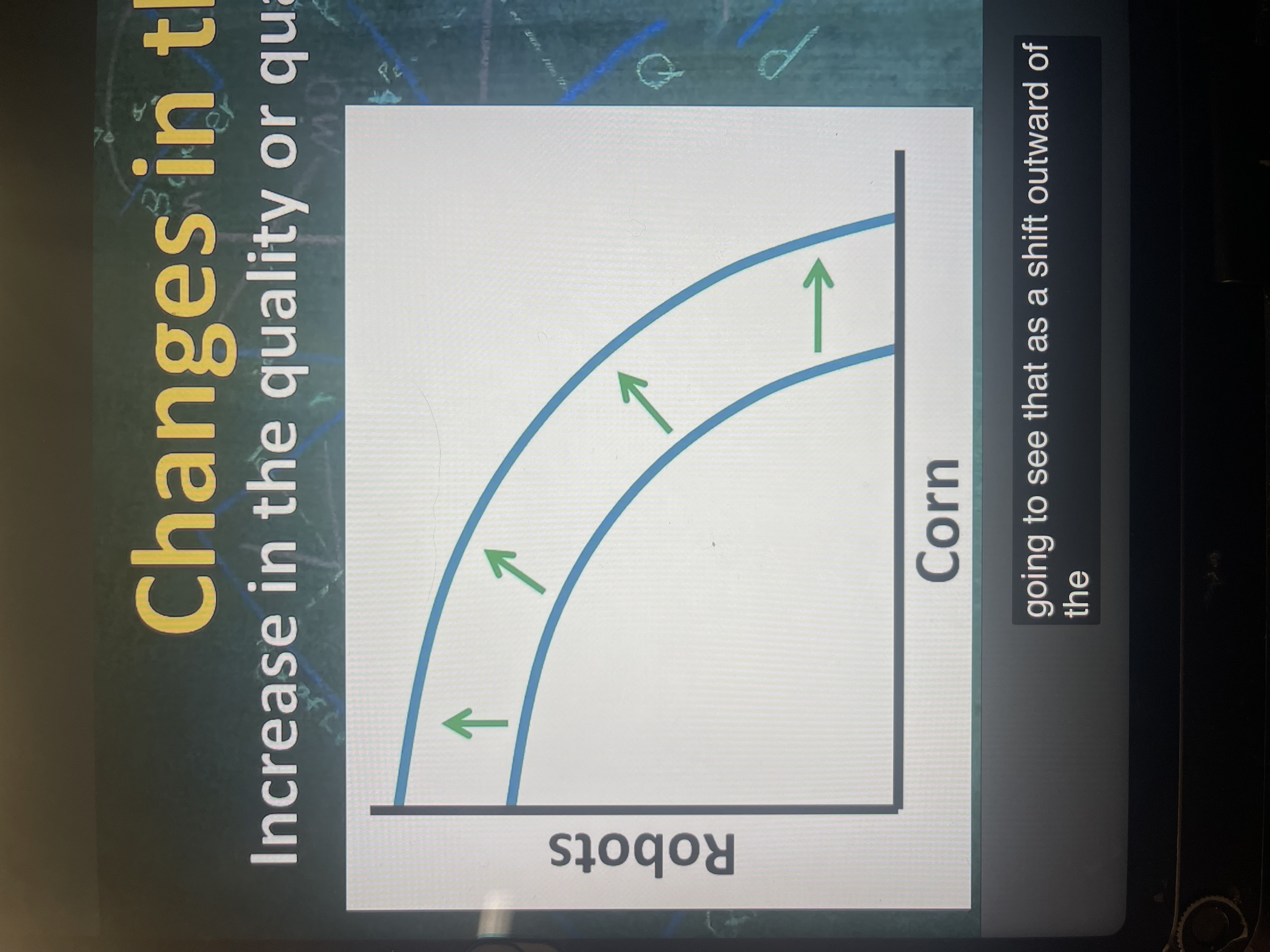

a shift outward of a PPC means..

increase in the quality or quantity of resources

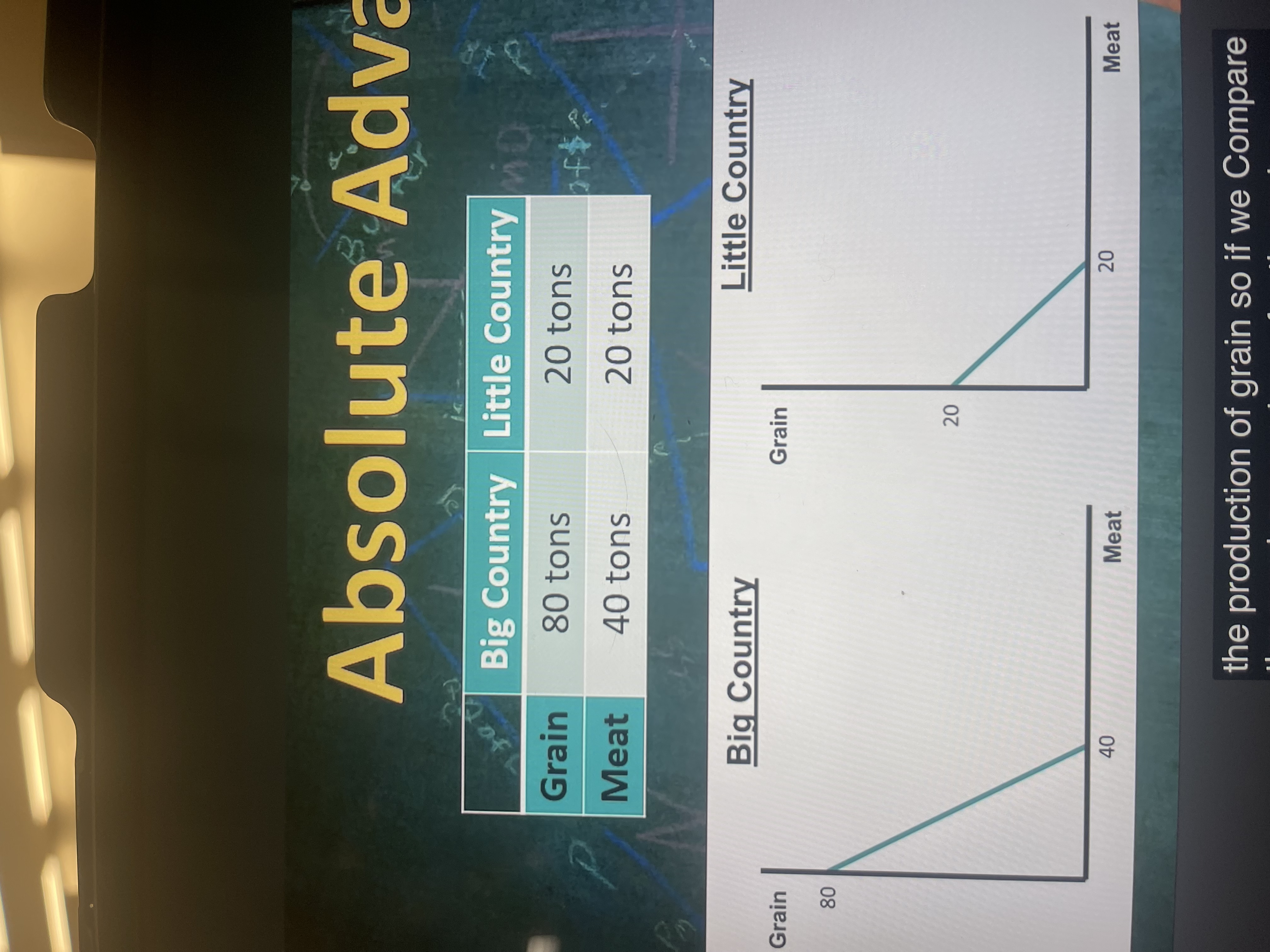

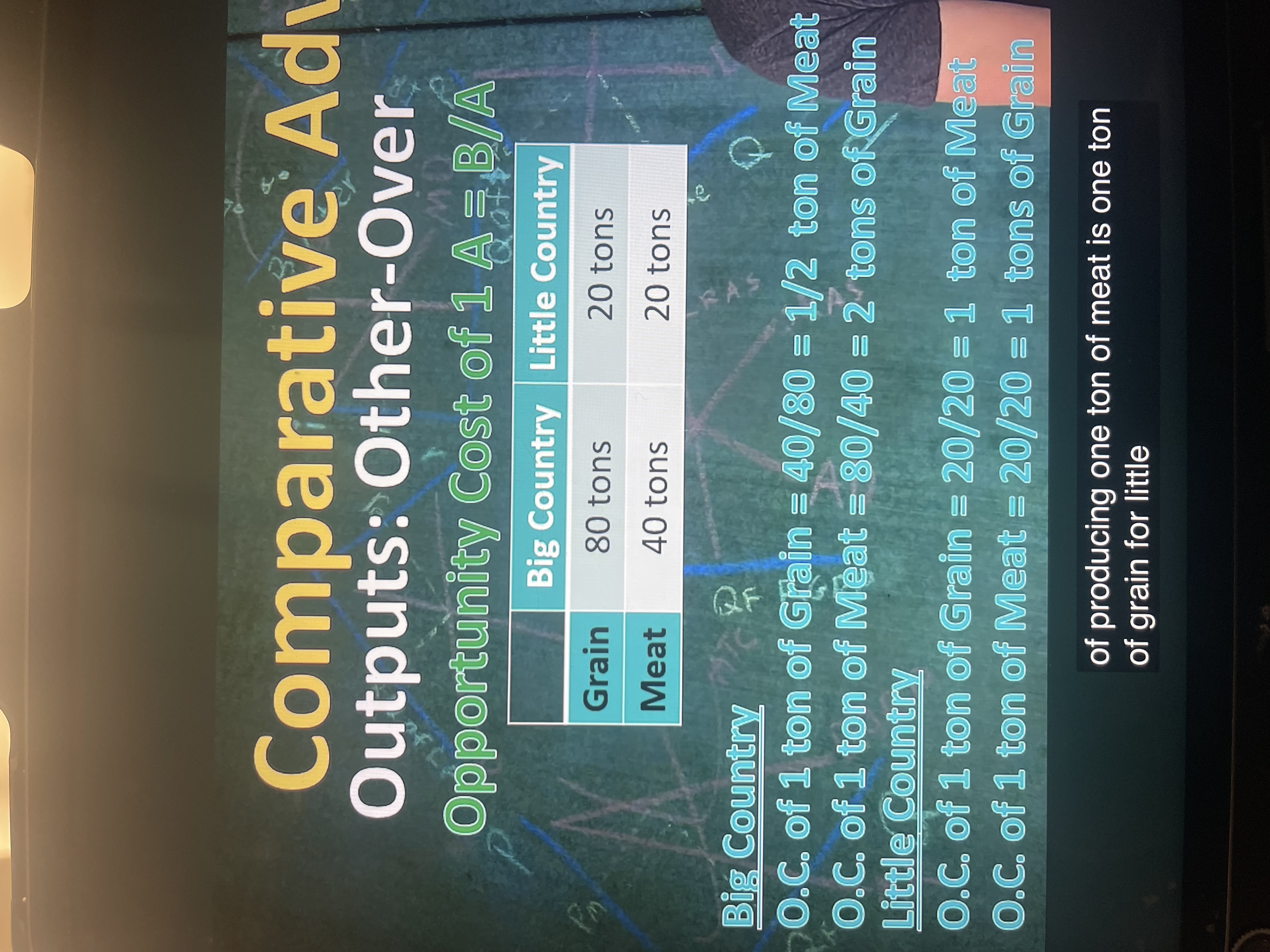

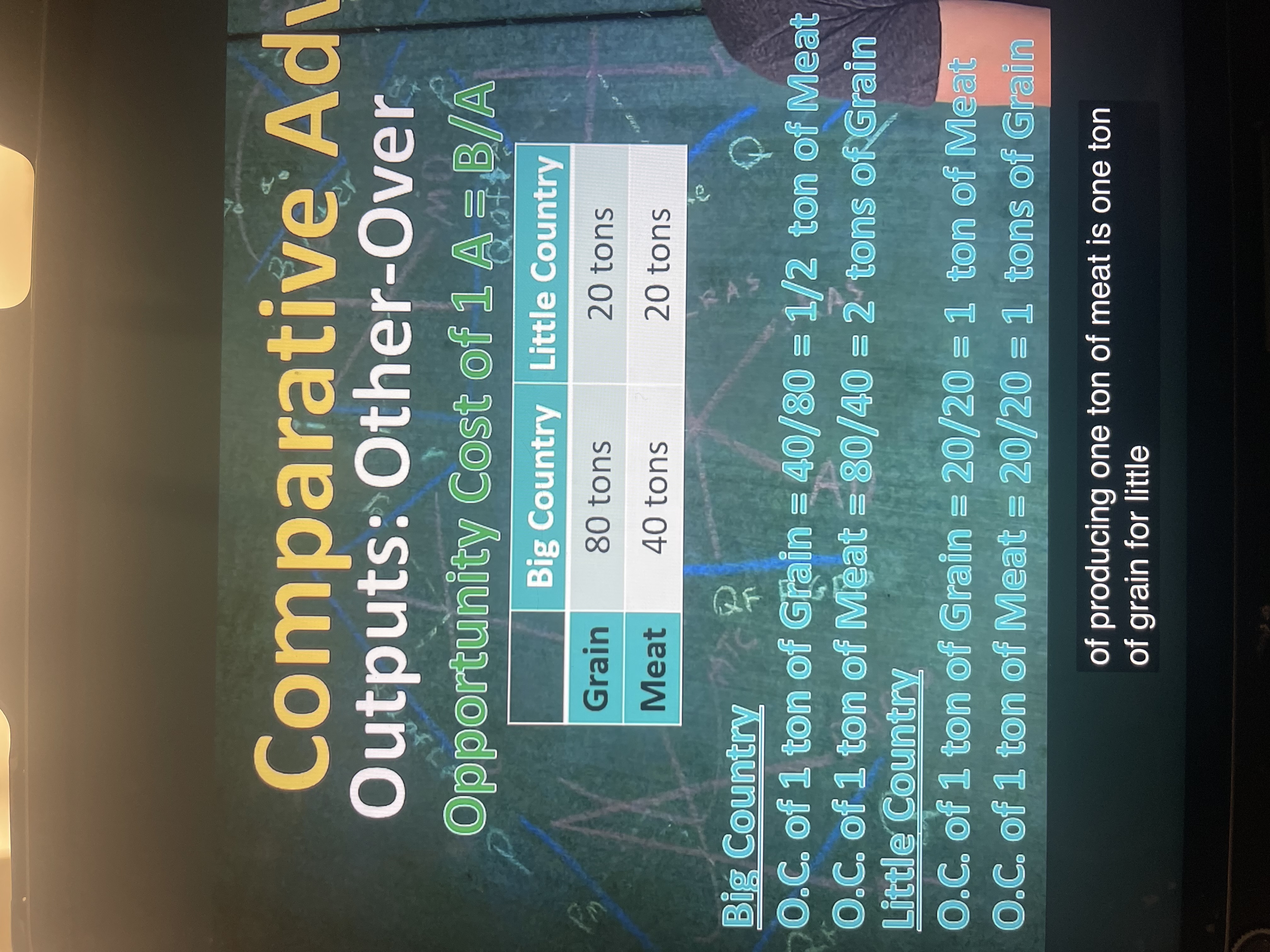

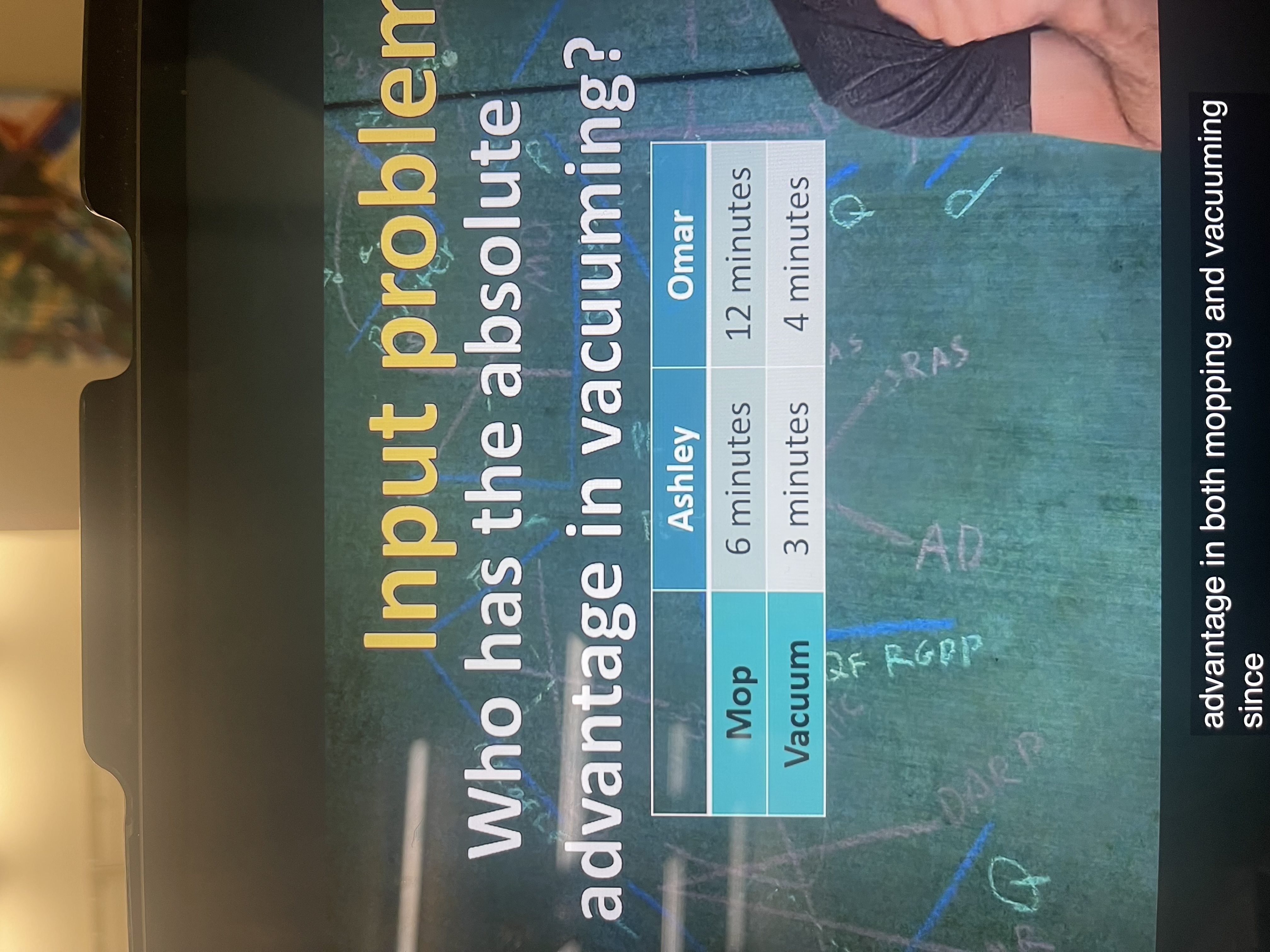

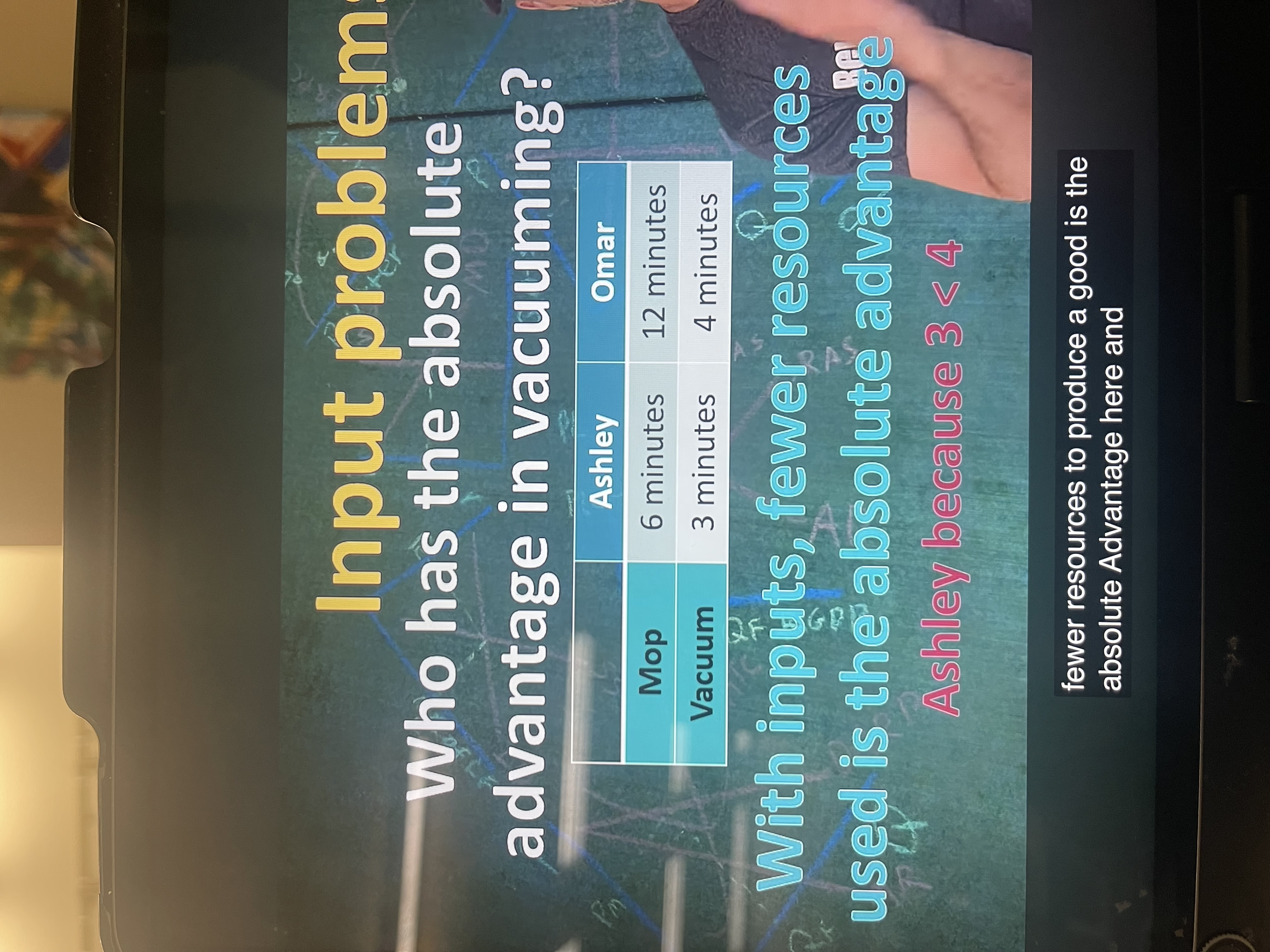

absolute advantage

ability to produce more goods with fixed resources or the same amount of goods with fewer resources AKA who is better at producing a particular good

which country has the absolute advantage of grain here?

the big country does (80 vs 20 tons)

comparative advantage

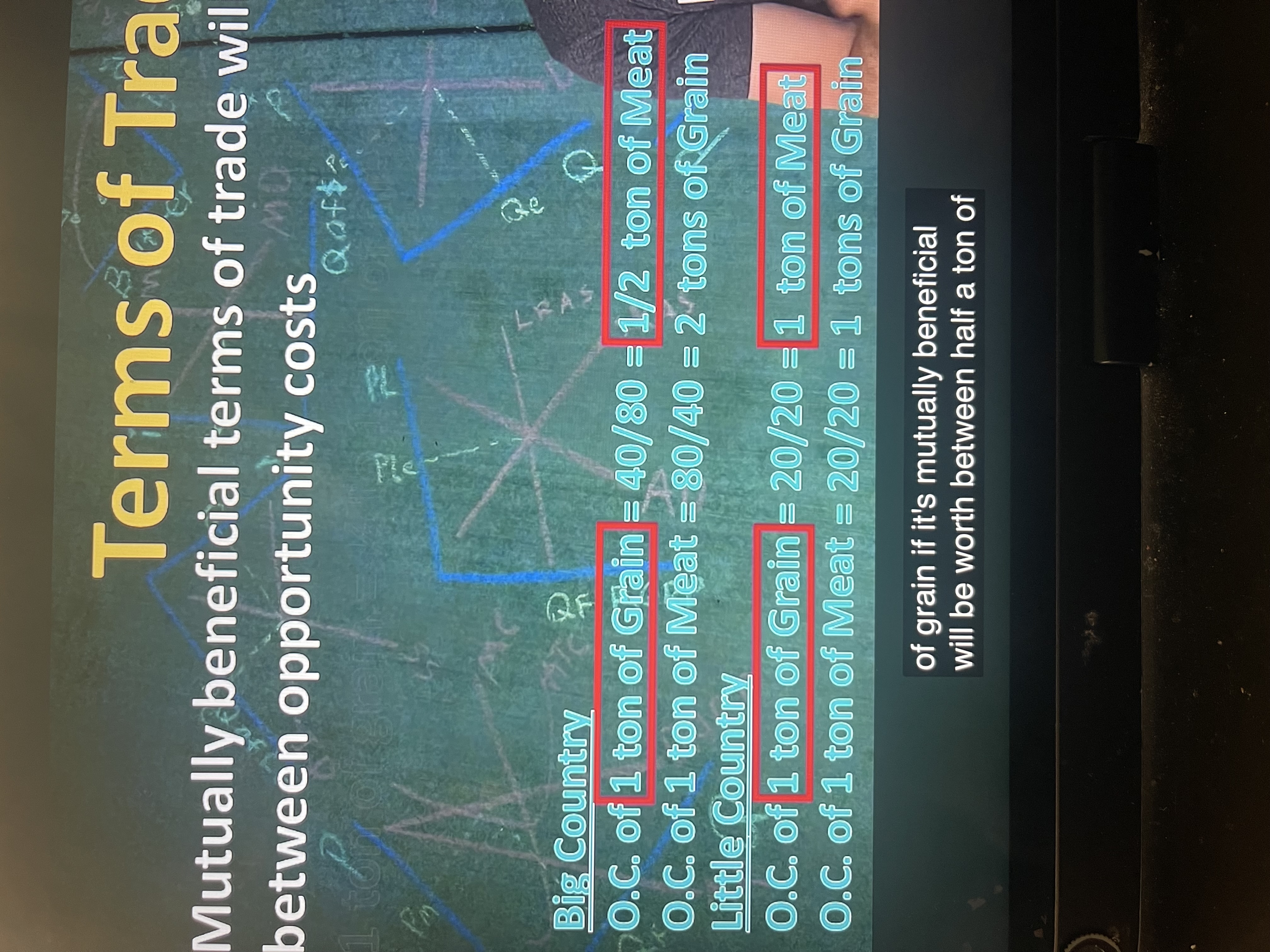

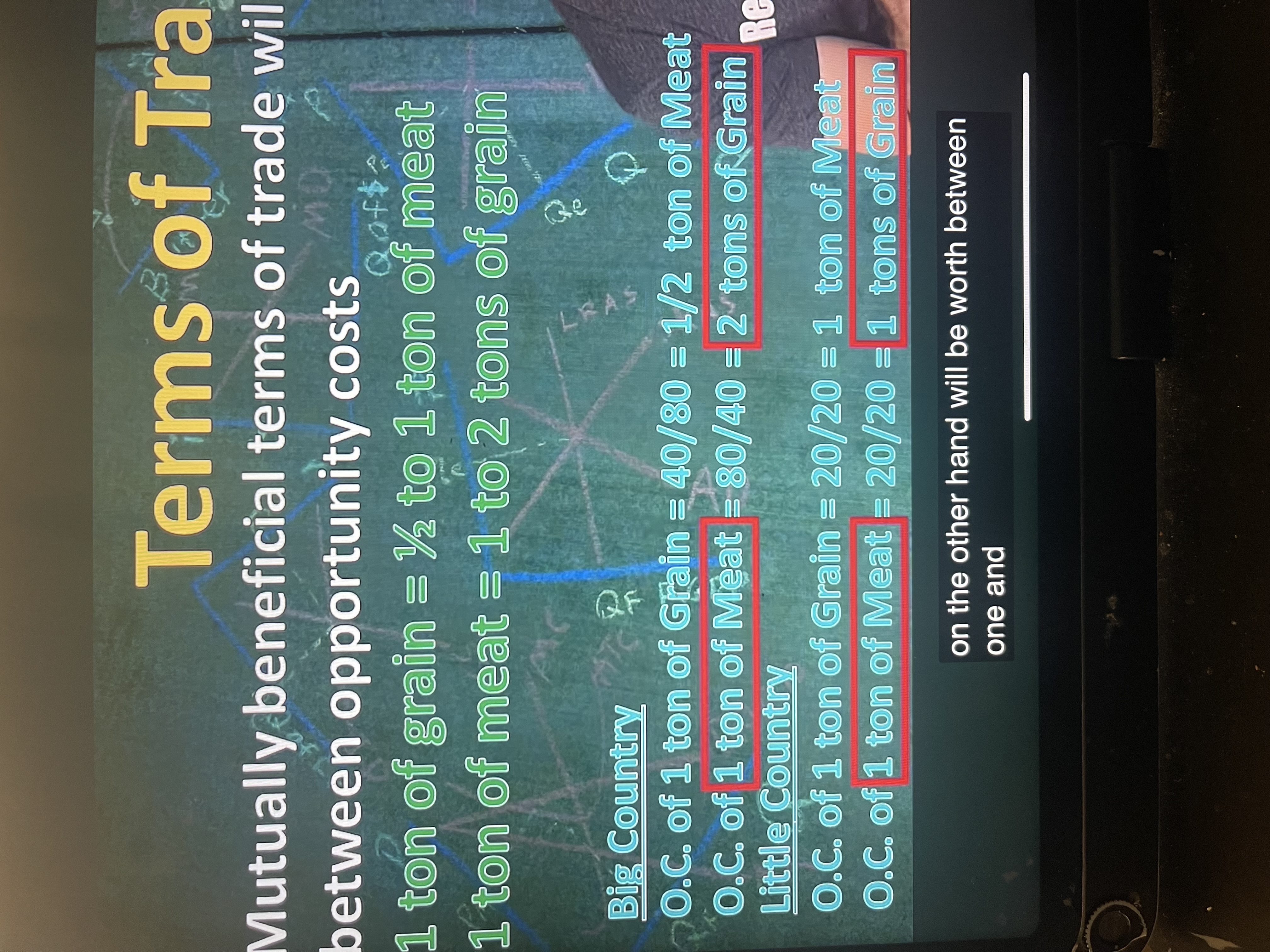

ability to produce something at a lower opportunity cost

what is an output problem in comparative advantage?

when the numbers/variables we’re given are finished products aka outputs. the formula for output problems is good A= good B/good A

which country has the comparative advantage in grain?

big country does bc its opportunity cost is ½ ton of meat, while little country’s is 1 ton of meat. big country loses less bc it has a smaller opportunity cost

what would a mutually beneficial trade be for these two countries?

in between ½ -1 ton of meat in exchange for in between 1-2 tons of grain. it’s mutually beneficial if the trade is between the 2 countries’ opportunity costs

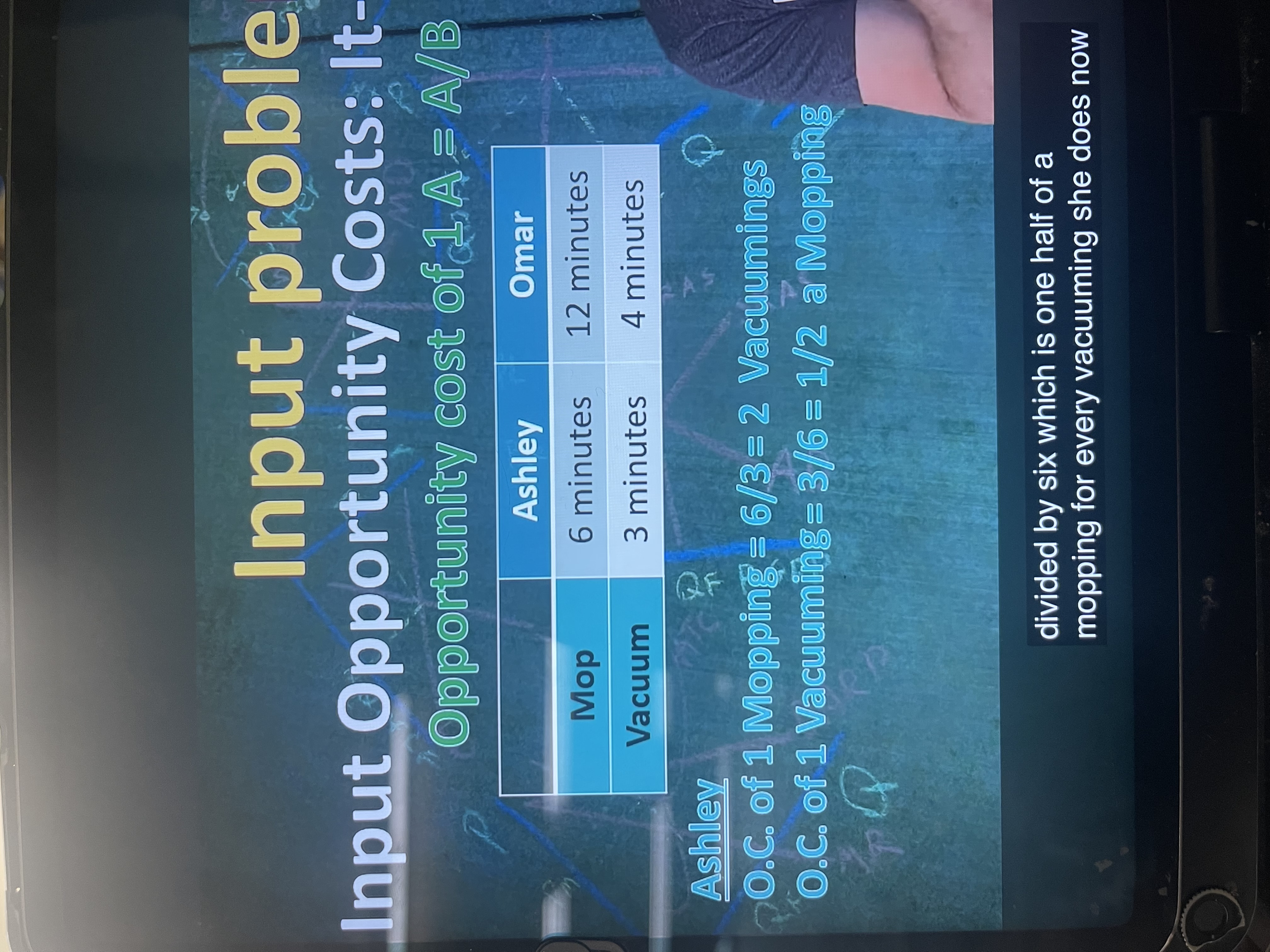

what is an input problem in comparative advantage?

when the variables are inputs of things that go into the production of a good/service (like time) the formula for the opportunity cost is good A = good A/ good B

Opportunity cost

The value of the alternative you didn’t choose (split into explicit and implicit costs)

Explicit costs

Money paid for a choice

Implicit costs

Value of the opportunities lost when u made a choice

How do you calculate an opportunity cost?

You add the explicit and implicit costs together

Total cost

Basically opportunity cost

Total benefit

Enhancement to wellbeing

Total net benefit

Total benefit - total cost = total net benefit

If the net benefit is positive, it means the benefits outweighed the costs. If it’s negative, the costs outweighed the benefits.

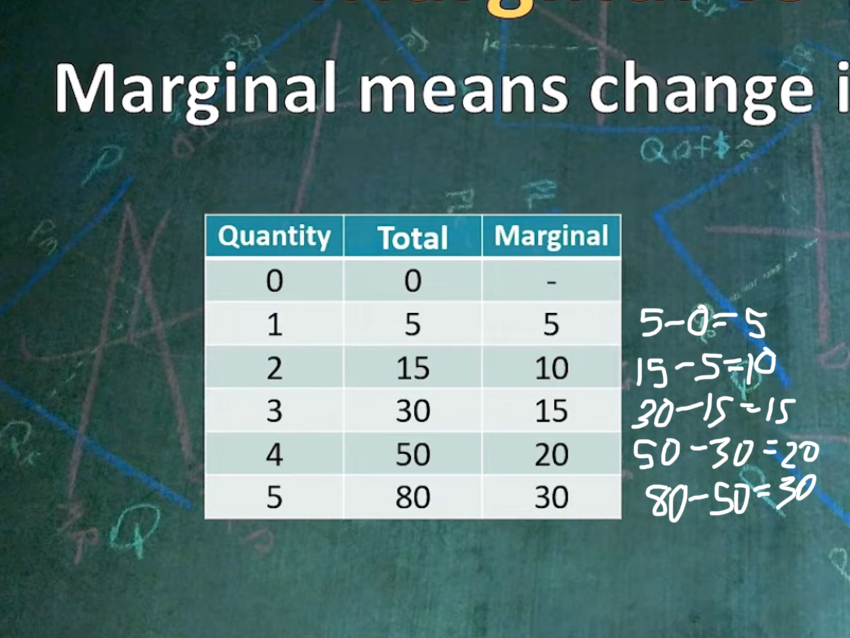

Marginal

Change in the total

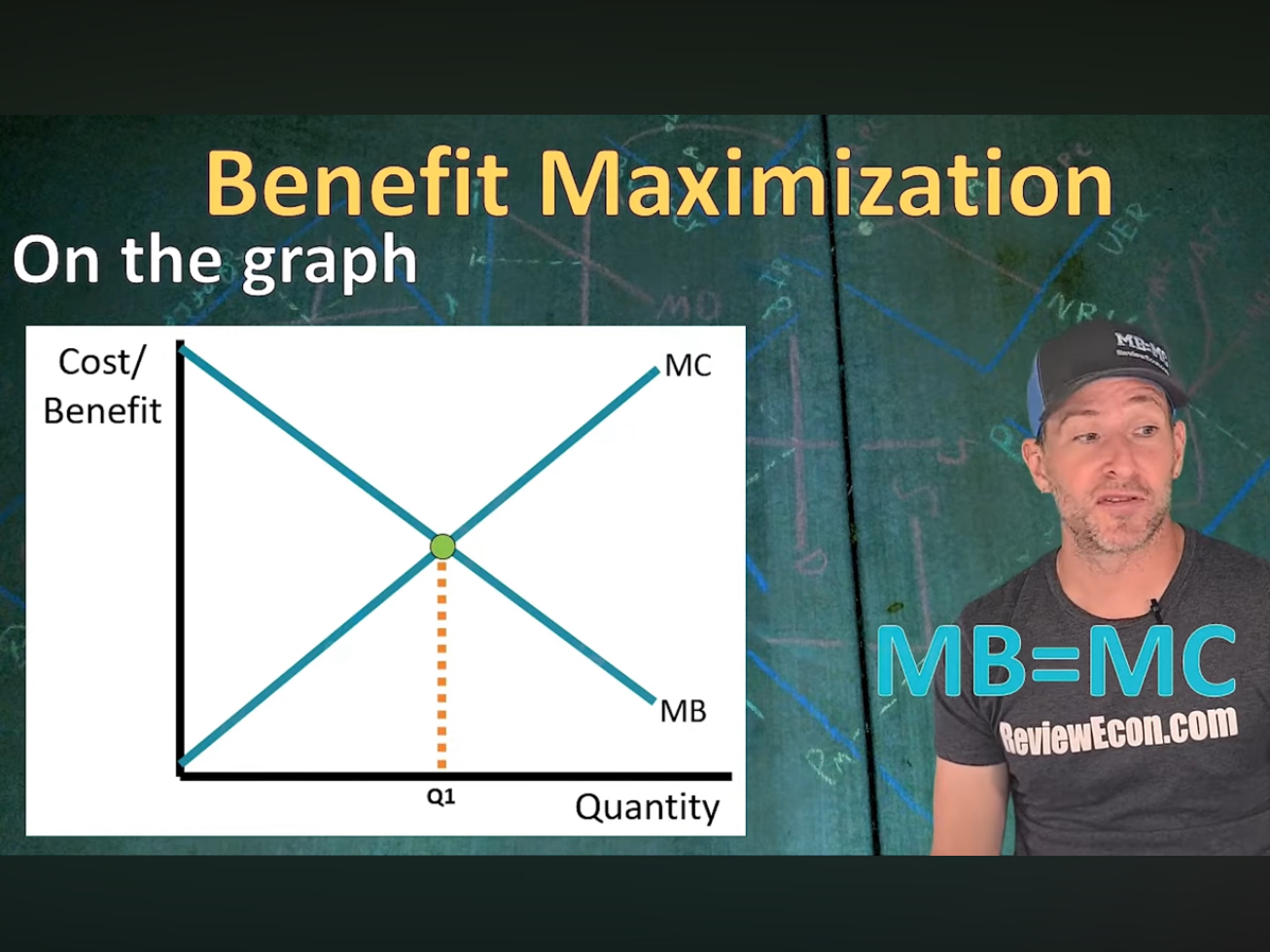

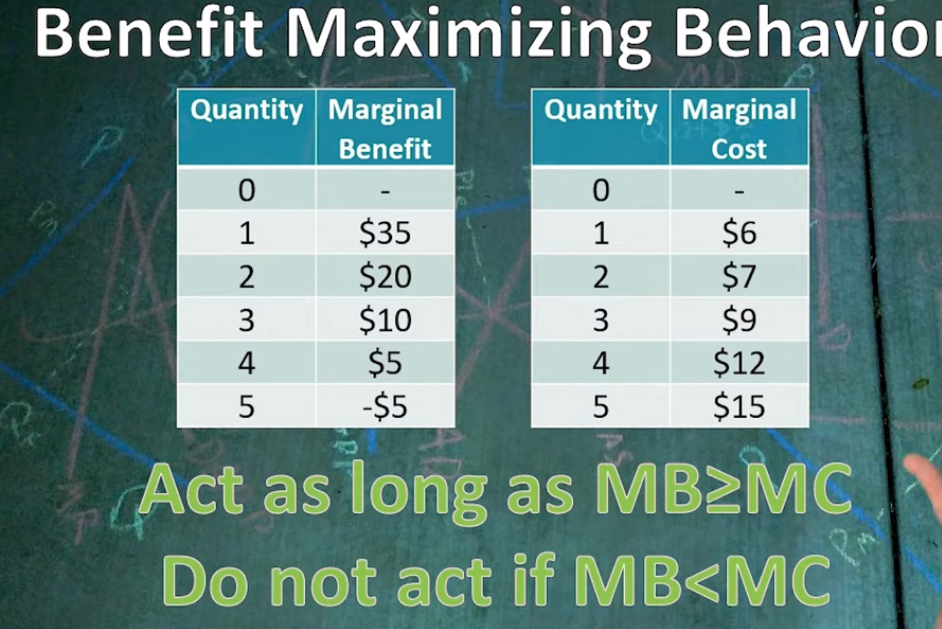

Formula for benefit maximization (finding best choice)

MB=MC (the choice is good if the marginal benefit is greater than or equal to the marginal cost)

What is the best quantity to buy here?

3 because that’s the last quantity where the marginal benefit is greater than the marginal cost

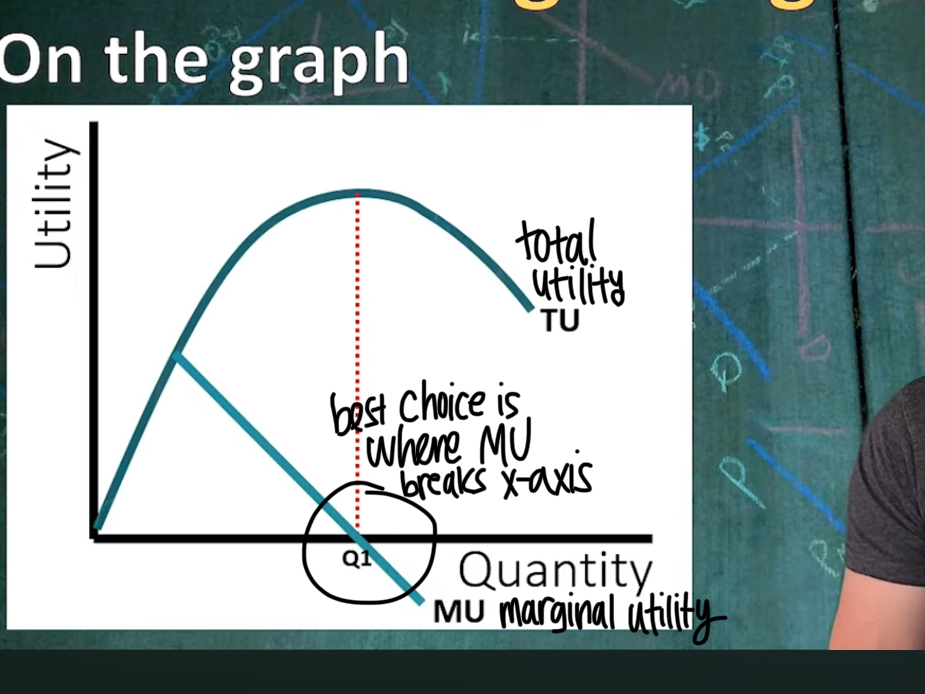

Utility

Satisfaction gained by consumers when consuming the good/service

Law of diminishing marginal utility

The marginal utility decreases as the quantity of the good increases

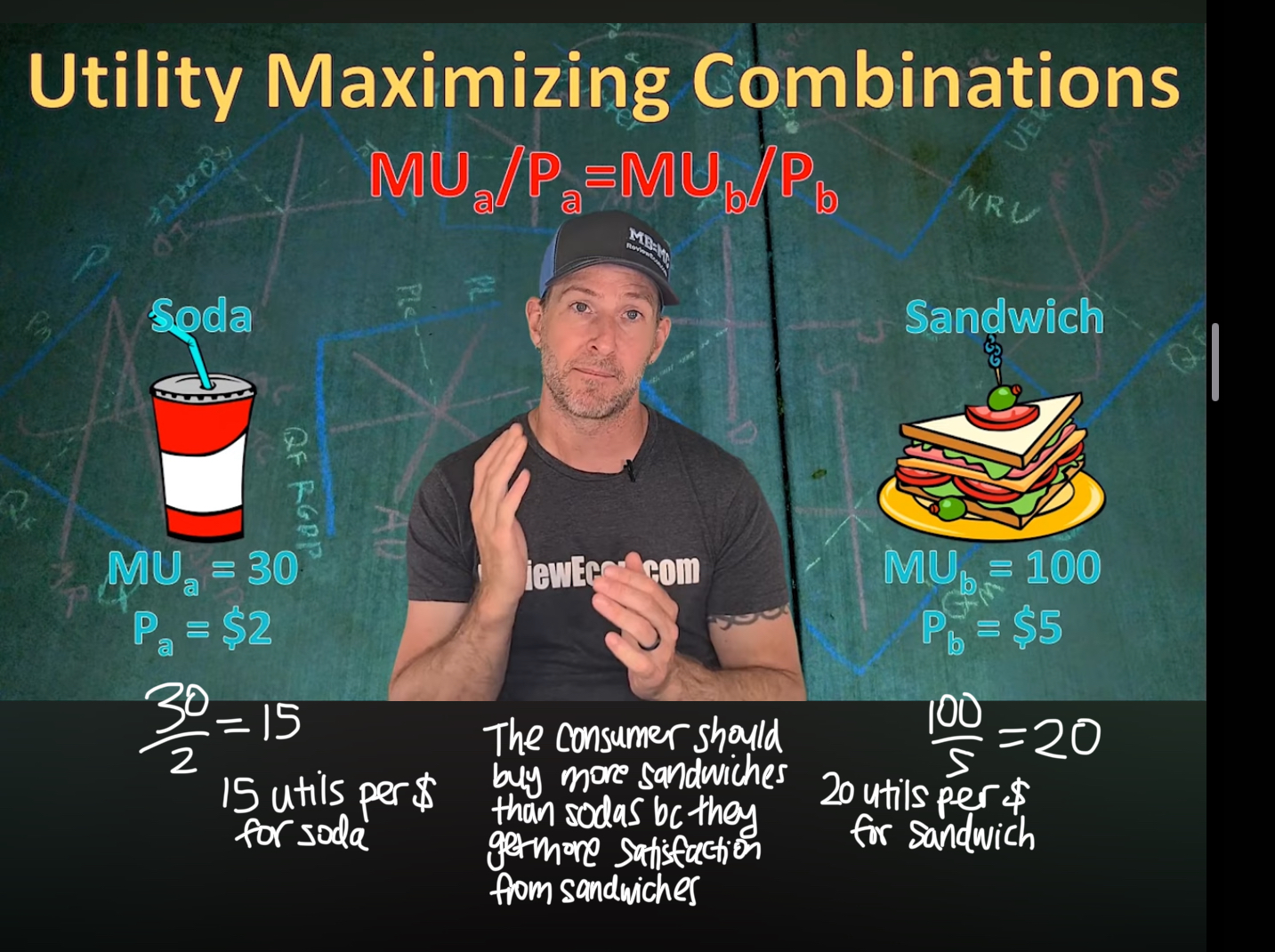

What’s the formula for utility maximization

Marginal utility of product A/price of product A = Marginal utility of product B/price of product B

Law of demand

Consumers buy more at low prices and buy less at high prices

Substitution effect

An increase in price makes substitutes of the product more attractive, and vice versa

Income effect

An increase in price will decrease a consumer’s power to purchase things in their income

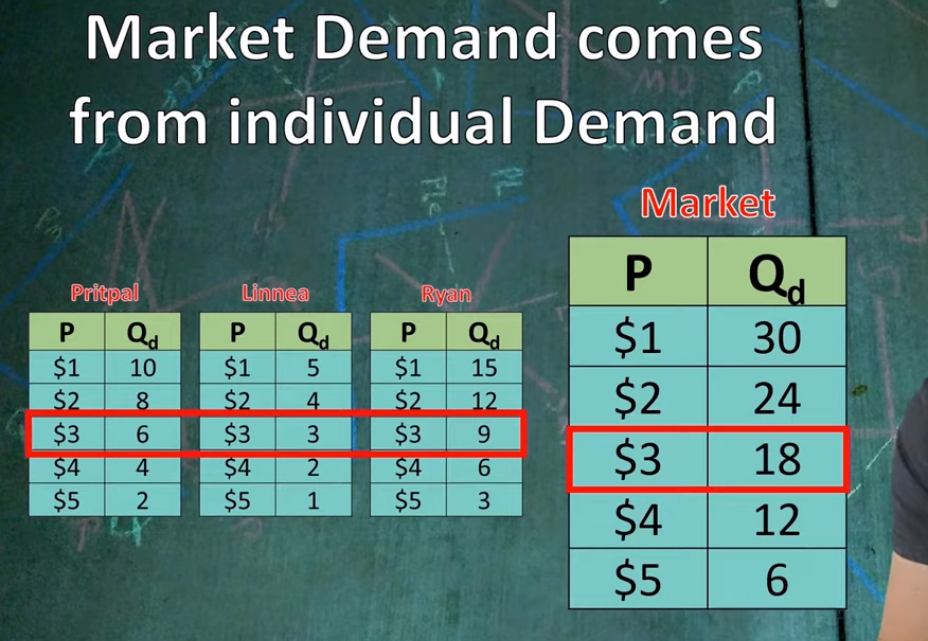

How do you create a market demand table?

By adding up the individual demands of what consumers would pay for the product

Demand vs quantity demanded

Demand is the entire demand curve for that product, while quantity demanded is just specific to one price of the product. Price changes quantity demanded and not the whole demand (same goes for supply vs quantity supplied)

What does it mean when the demand curve shifts to the right?

The demand increased

What does it mean when the demand curve shifts to the left?

The demand decreased

Which factors shift demand?

Tastes and preferences

market size (# of buyers)

price of related goods (substitutes or complements)

changes in income (normal goods or inferior goods)

expectations for the future (like expecting the price to increase in the future)

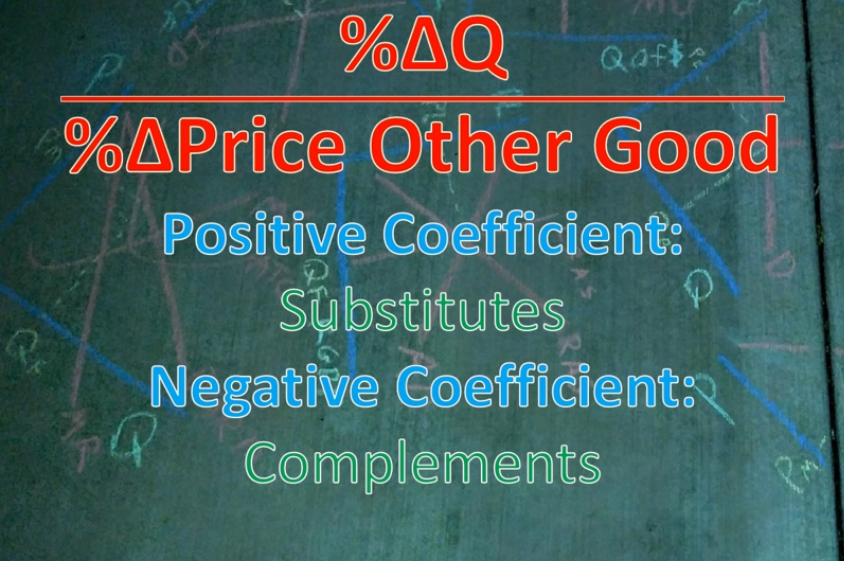

Substitute goods

Products that can replace each other

Complement goods

Goods that are paired together. If one product becomes more expensive, the complement’s demand curve will shift to the left

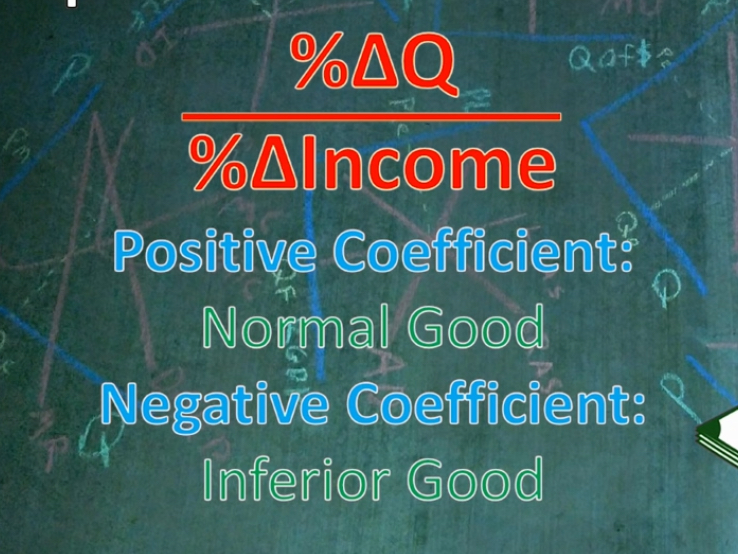

Normal goods

If the consumer income increases, they will buy more normal goods (luxury goods like cars)

Inferior goods

When a consumer’s income increases, they actually buy less of inferior goods (like canned soup or instant ramen)

Law of supply

Producers sell more at high prices and less at low prices

Which factors shift supply?

Input prices- cost of resources for production of the product

Government tools (taxes, subsidies, regulations)

Number of sellers/competition

Technology (will usually increase supply)

Price of other goods (some goods become more profitable to sell)

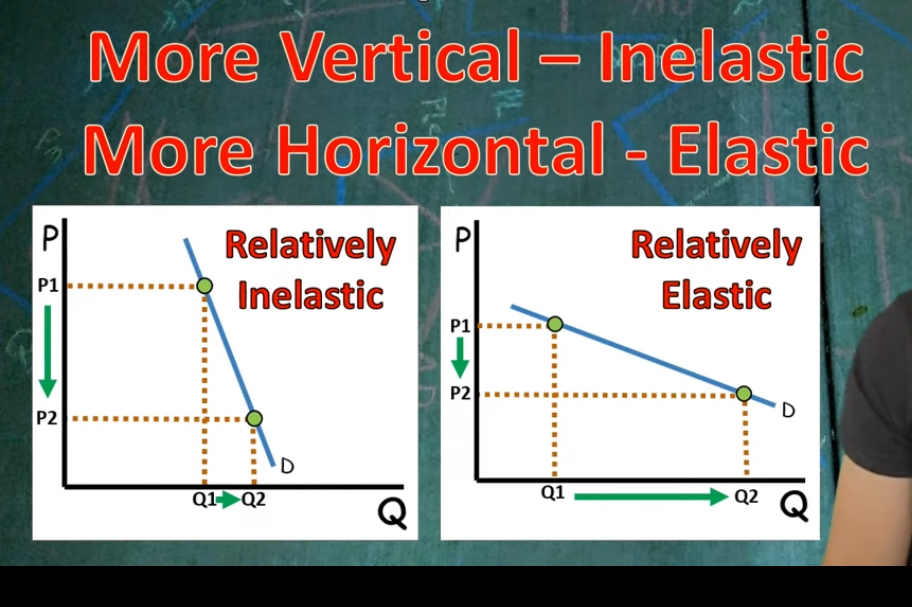

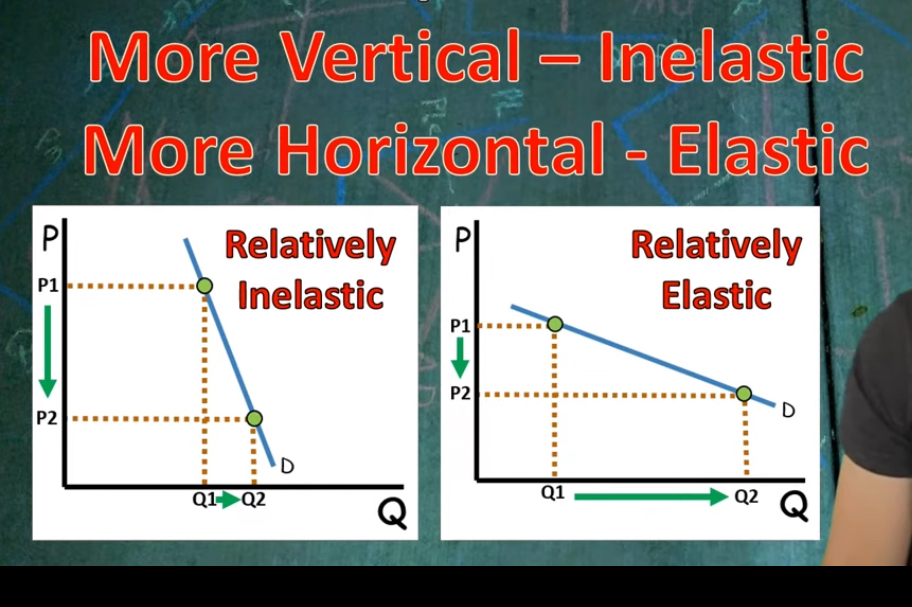

Price elasticity

How sensitive a product is to price changes (if its quantity demanded changes easily due to price changes)

Inelastic

It’s not sensitive to price changes. Goods are inelastic if it’s a necessity and there are few substitutes

Elastic

It is sensitive to price changes. Goods are elastic if it’s a luxury item and there are lots of substitutes

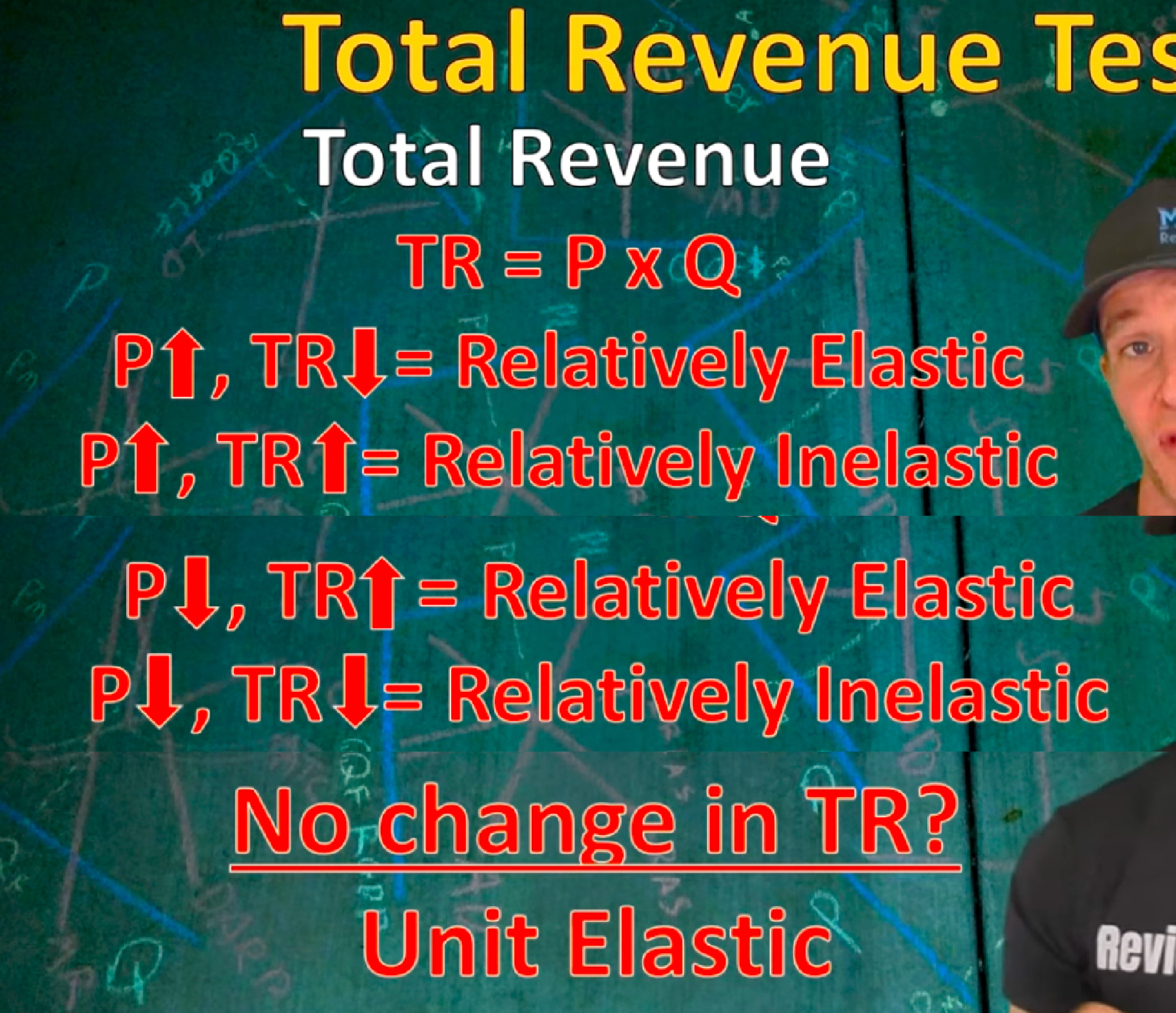

Total revenue formula

Total revenue= price X quantity sold

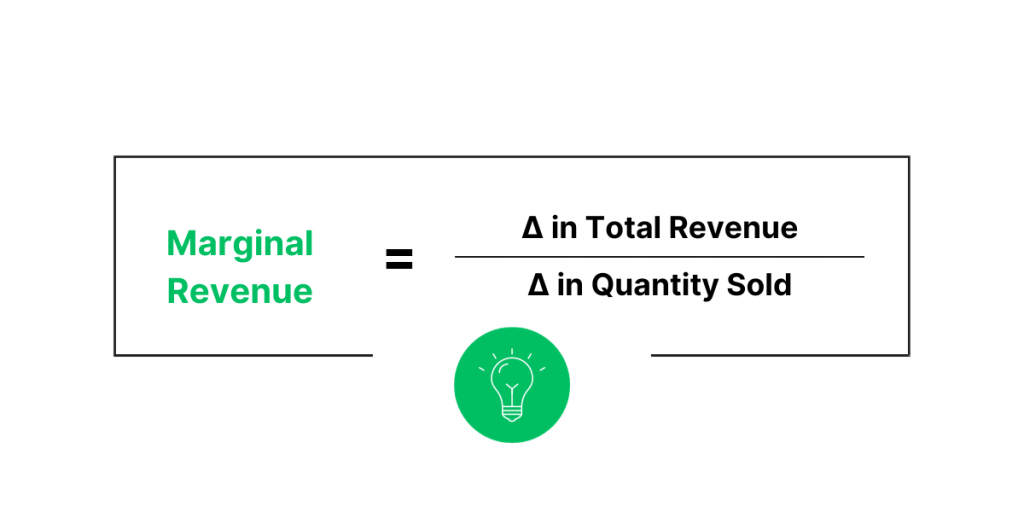

Marginal revenue test

Change in total revenue/ change in quantity sold

Positive = elastic

Zero = unit elastic

Negative = inelastic

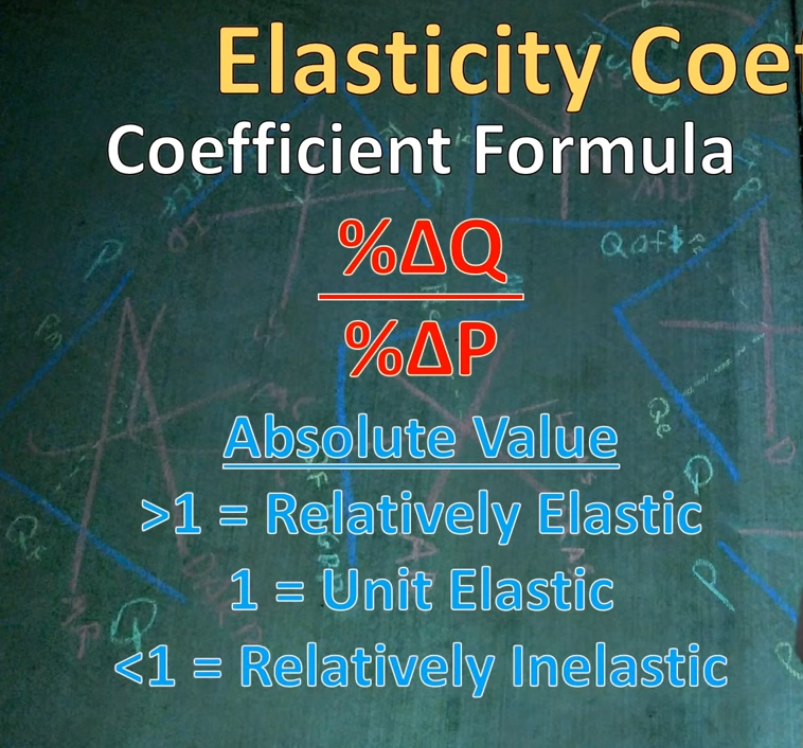

Elasticity coefficient formula

Percentage change in quantity/ percentage change in price (this formula applies to elastic for demand and supply)

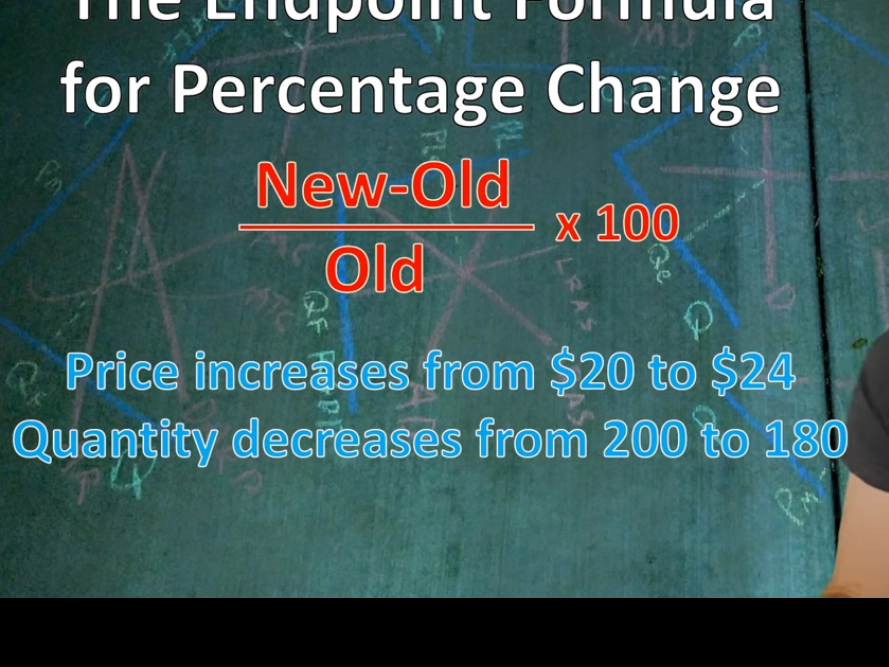

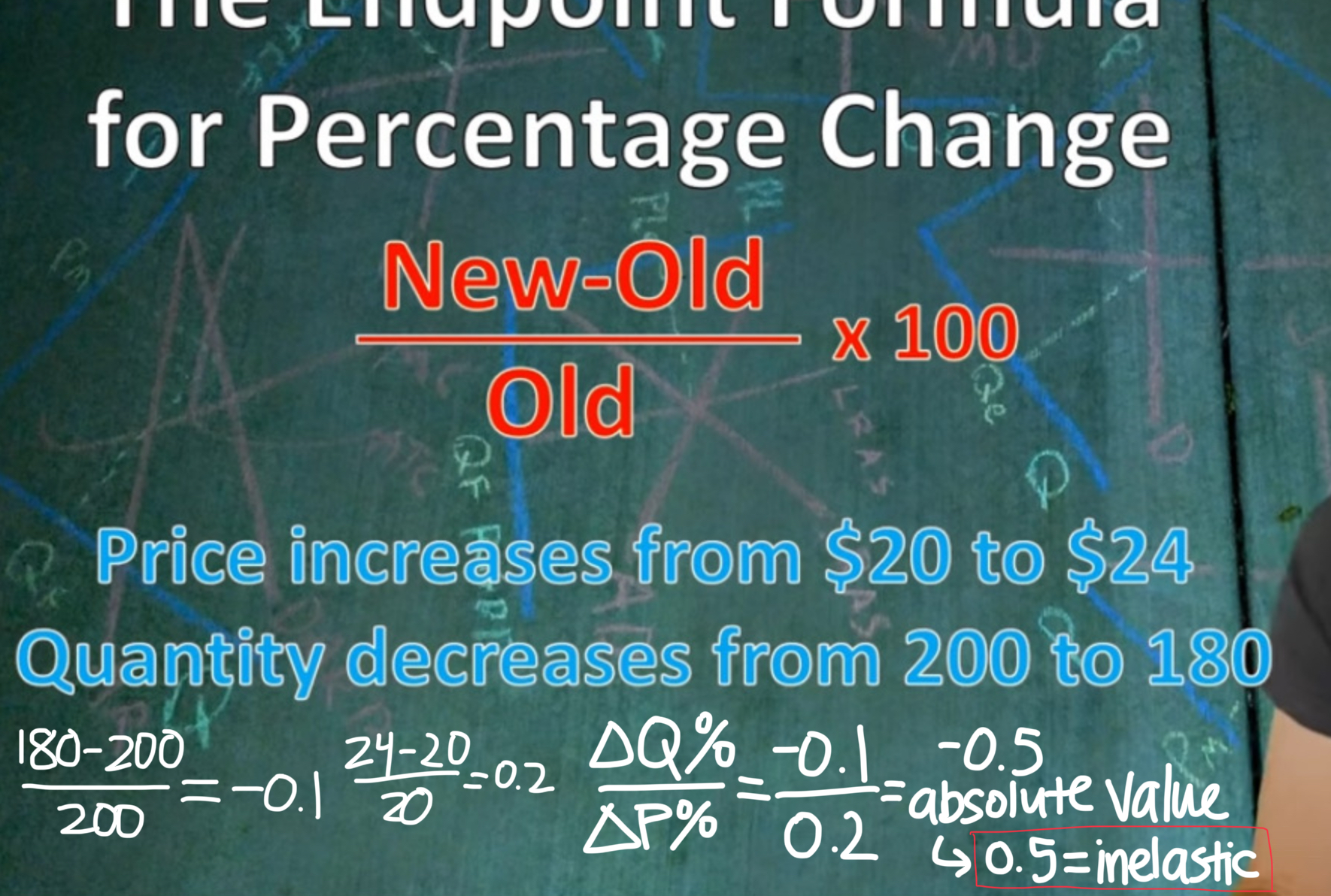

Percentage change formula

New-old/ old

Given this info, determine the elasticity

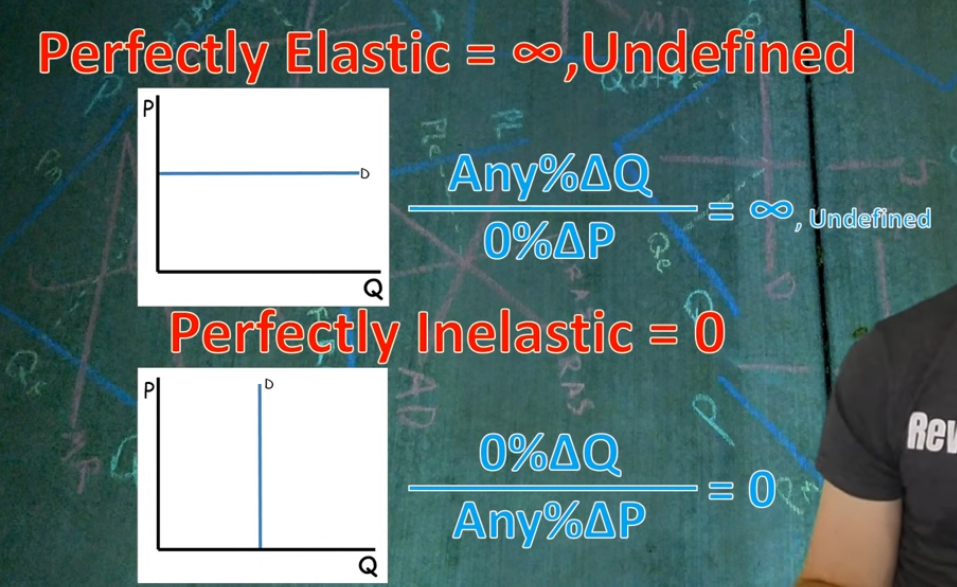

What do graphs of perfectly elastic/inelastic look like?

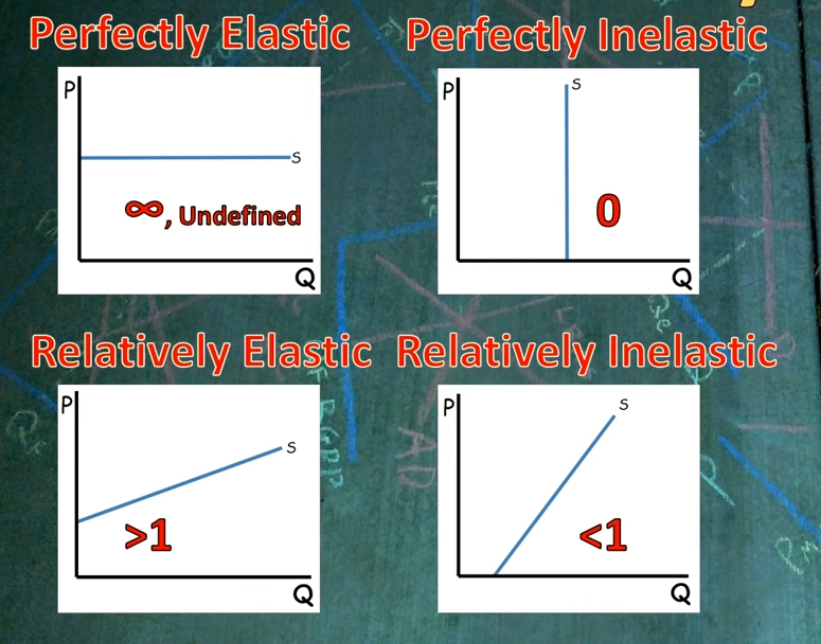

What do elasticity of supply graphs look like?

Income elasticity

How much a change in income impacts the quantity ppl buy

Income elasticity formula

Percentage change in quantity/ percentage change in income

Cross price elasticity

How the price of one good impacts the demand for another good

Cross price elasticity formula

Percentage change of quantity in one good/ percentage change of price in another good

Market equilibrium

Quantity demanded = quantity supplied

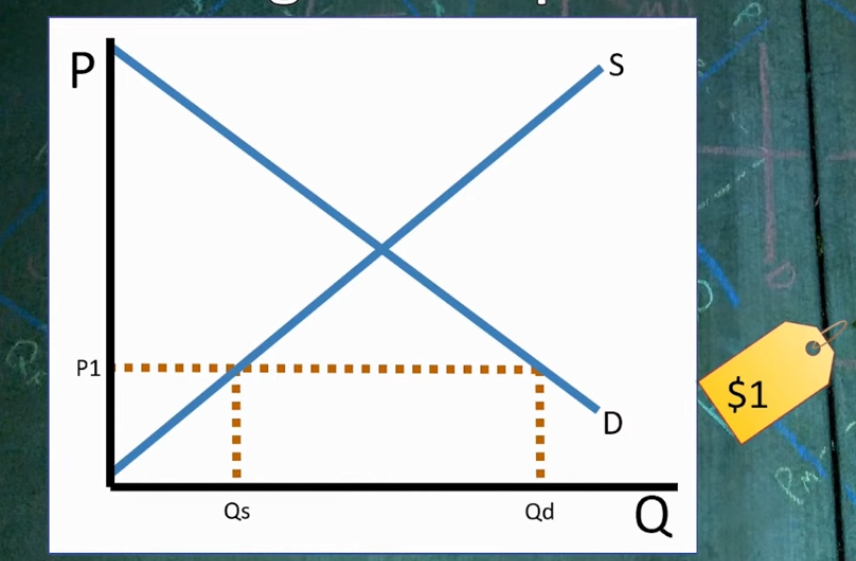

Surplus

When the price is above the market equilibrium, so the quantity demanded is less than the quantity supplied

How to calculate the amount of surplus

Quantity supplied - quantity demanded

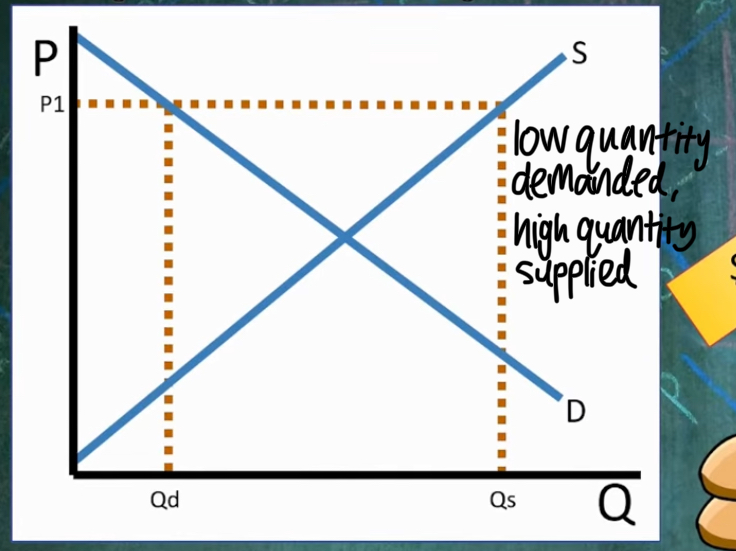

Shortage

When the price is below the market equilibrium, so the quantity demanded is more than the quantity supplied

How to calculate the amount of shortage

Quantity demanded - quantity supplied

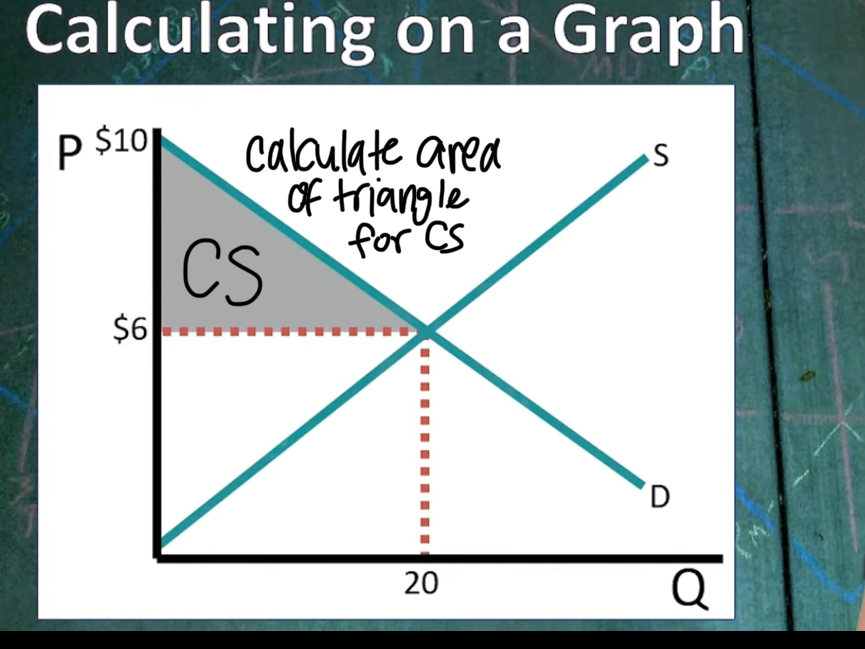

Consumer surplus

Difference between the value that the product has to the consumer and the price the consumer pays. Marginal utility - price = consumer surplus

Producer surplus

Difference between the marginal cost of production and the price of product. Marginal cost-price= producer surplus

Economic surplus

Benefit gained for producers and consumers. Consumer surplus + producer surplus = economic surplus

Efficiency loss/ deadweight loss

Reduction of economic surplus. It’s the area that could’ve been economic surplus if we reached equilibrium. (Also occurs with shortages)

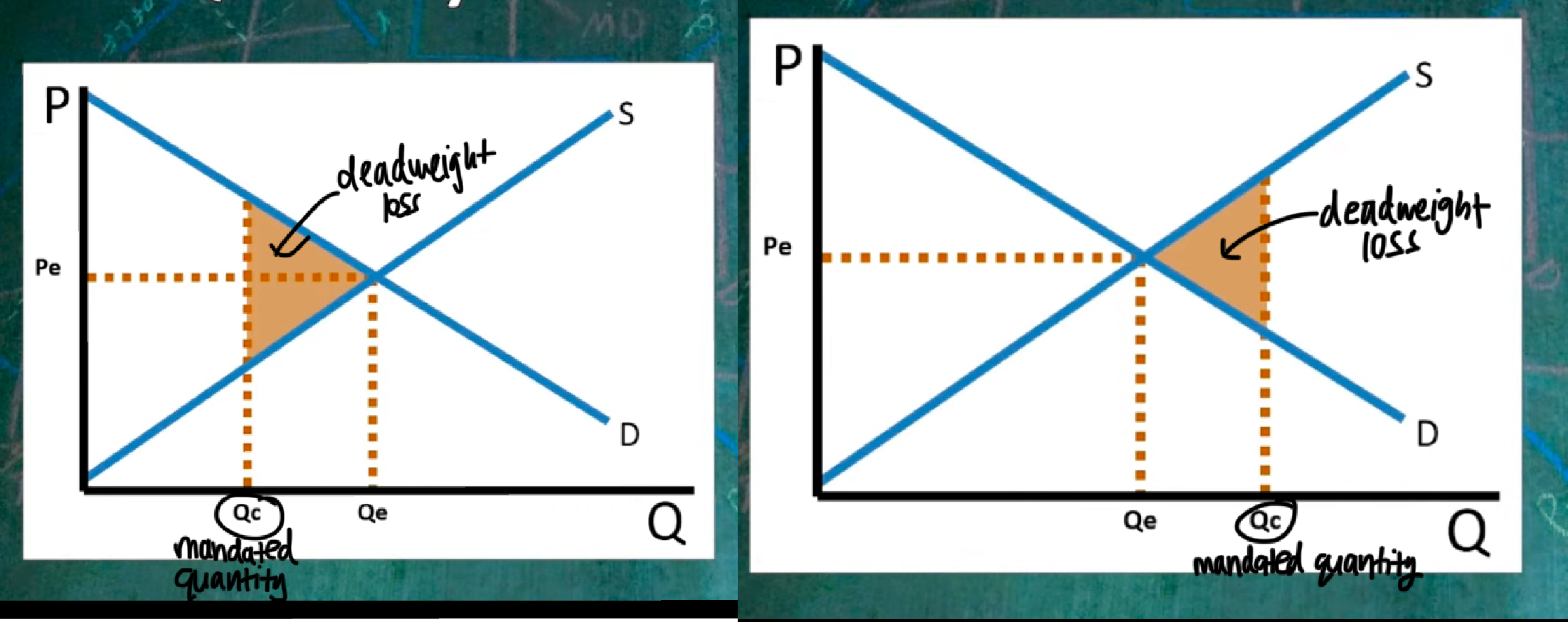

Quantity controls

The gov mandates a certain quantity to be produced. If it’s less than the equilibrium quantity, it leads to deadweight loss (same if it’s more than equilibrium)

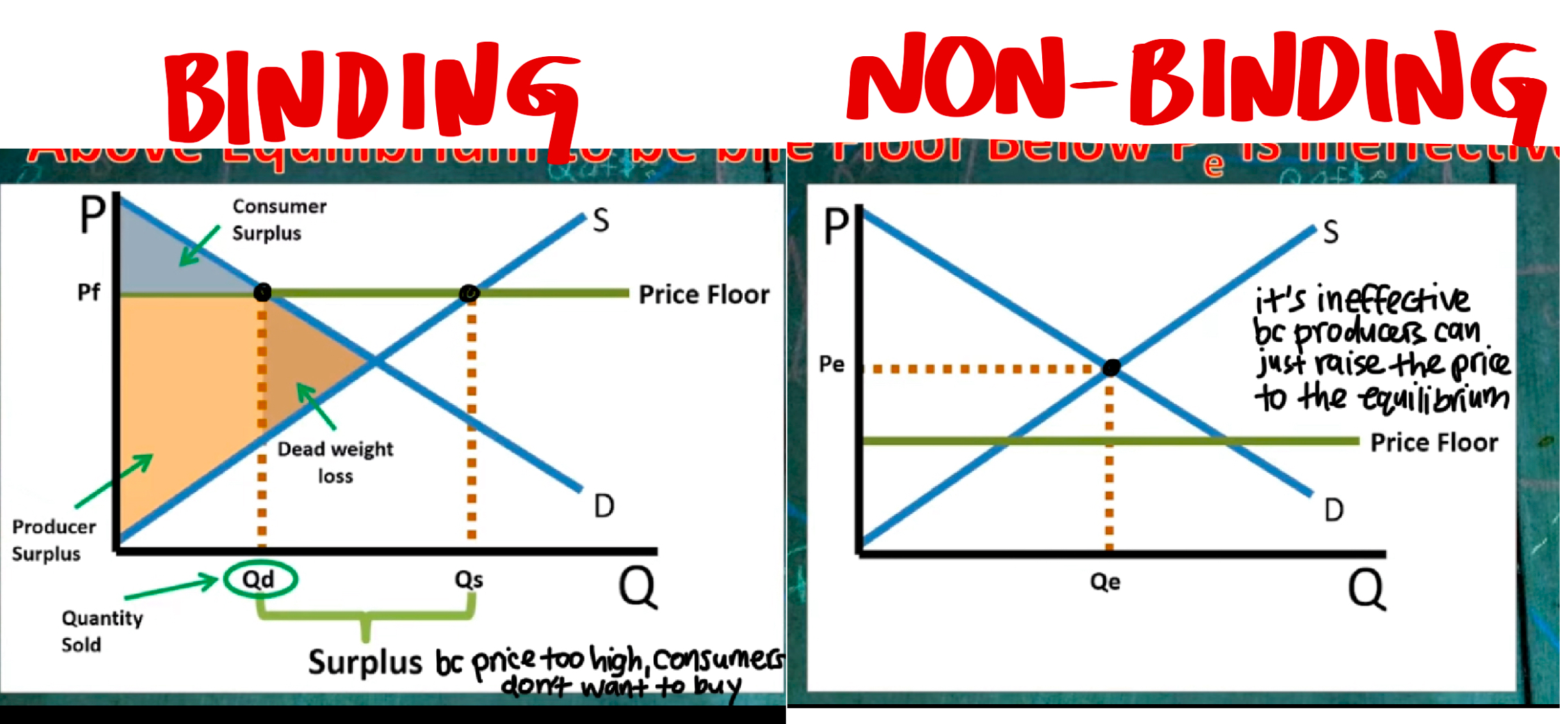

Price floor

Minimum price for a product, creates surplus. If the product is inelastic, the surplus will be smaller. A binding price floor is above equilibrium. A non-binding price floor is below, and it’s ineffective.

Price ceiling

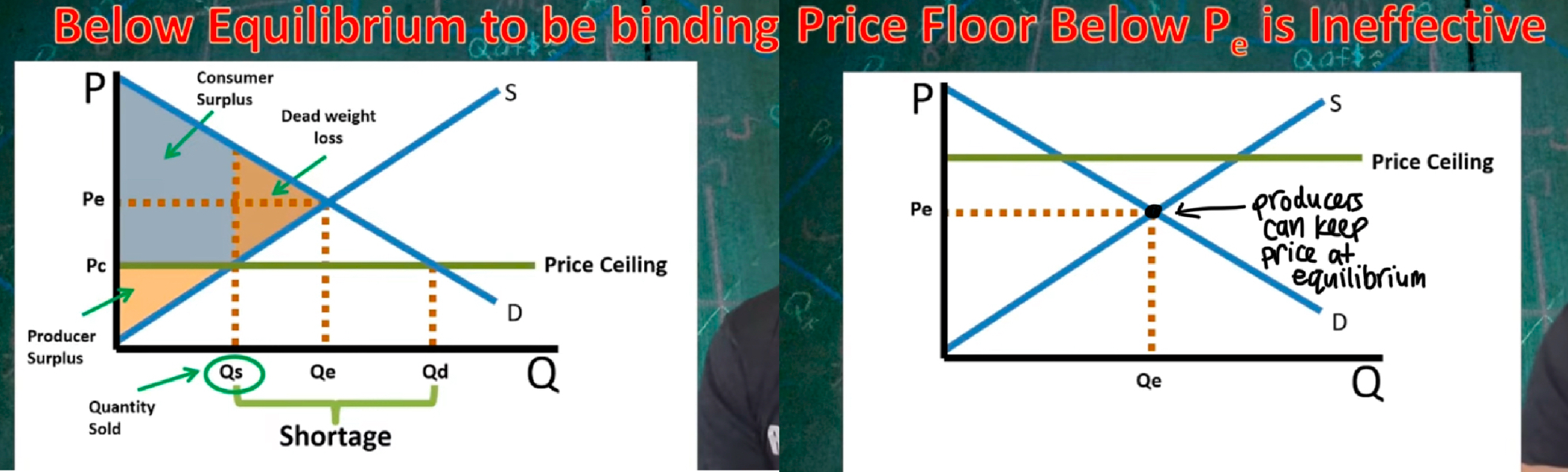

Maximum price for a product

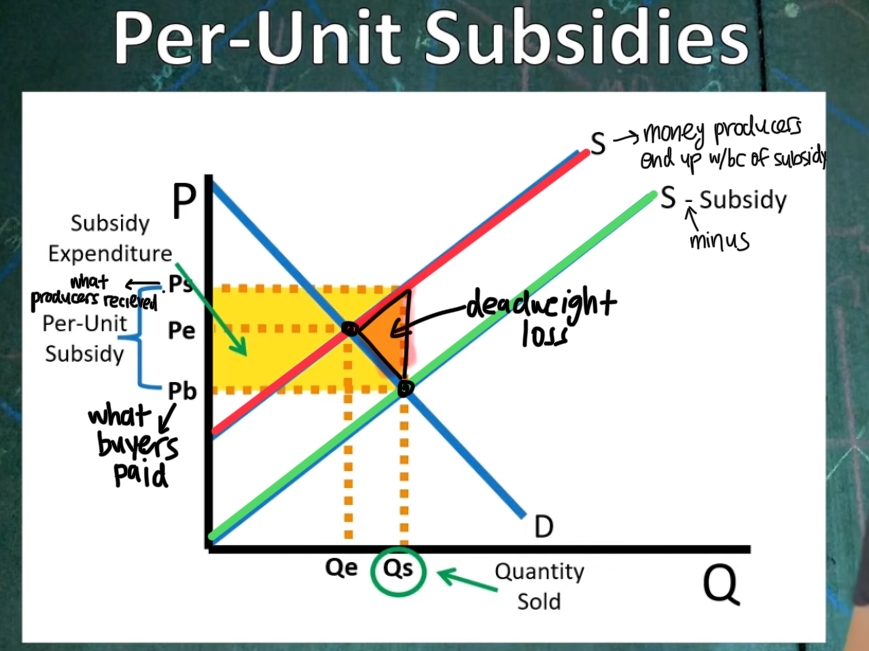

Per-unit subsidies

Gov pays producers per unit they make

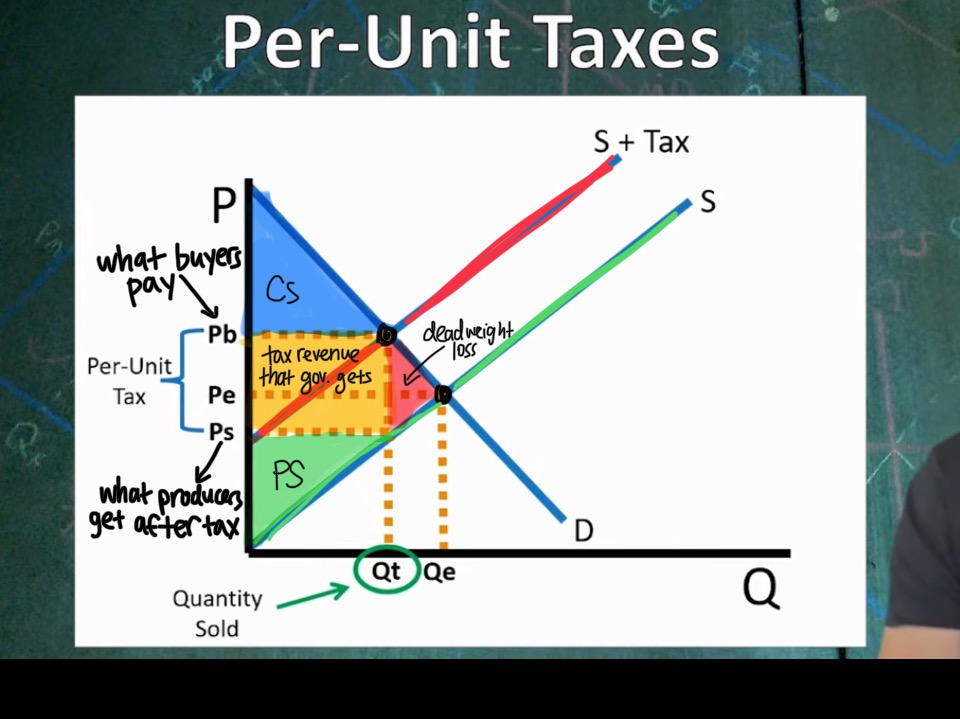

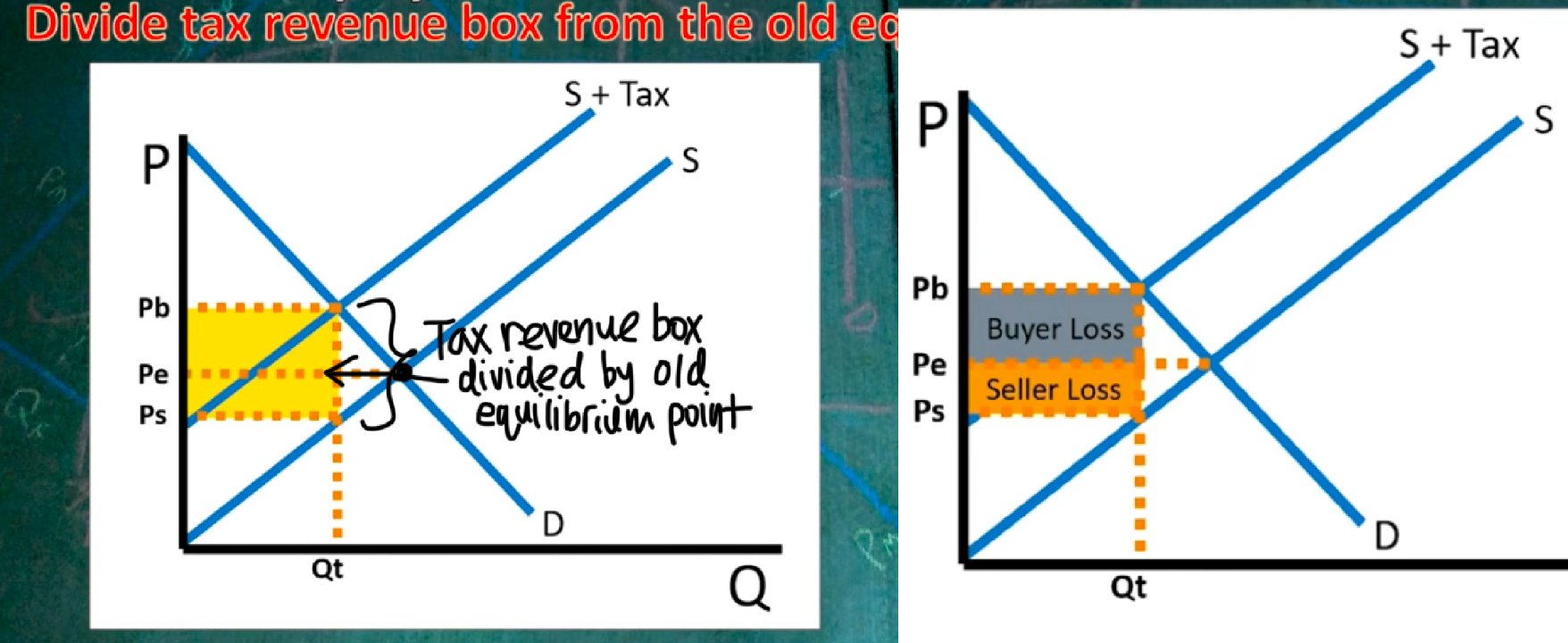

Per-unit taxes

Tax incidence/tax burden

How we find out who pays the tax (consumer or producer). If one of the curves (supply or demand) is less elastic, it pays more tax

Autarky

When countries are independent and don’t trade with other countries

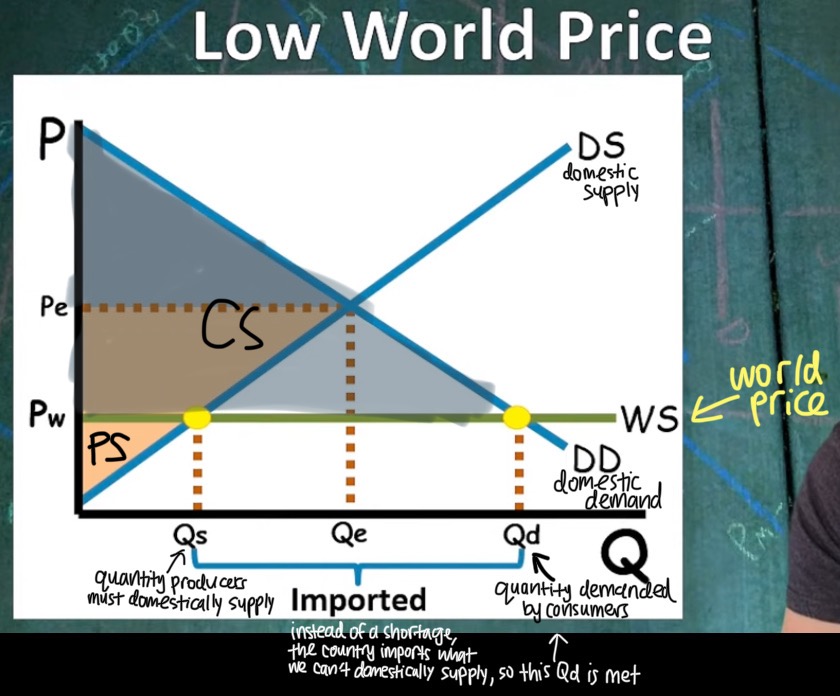

Low world price

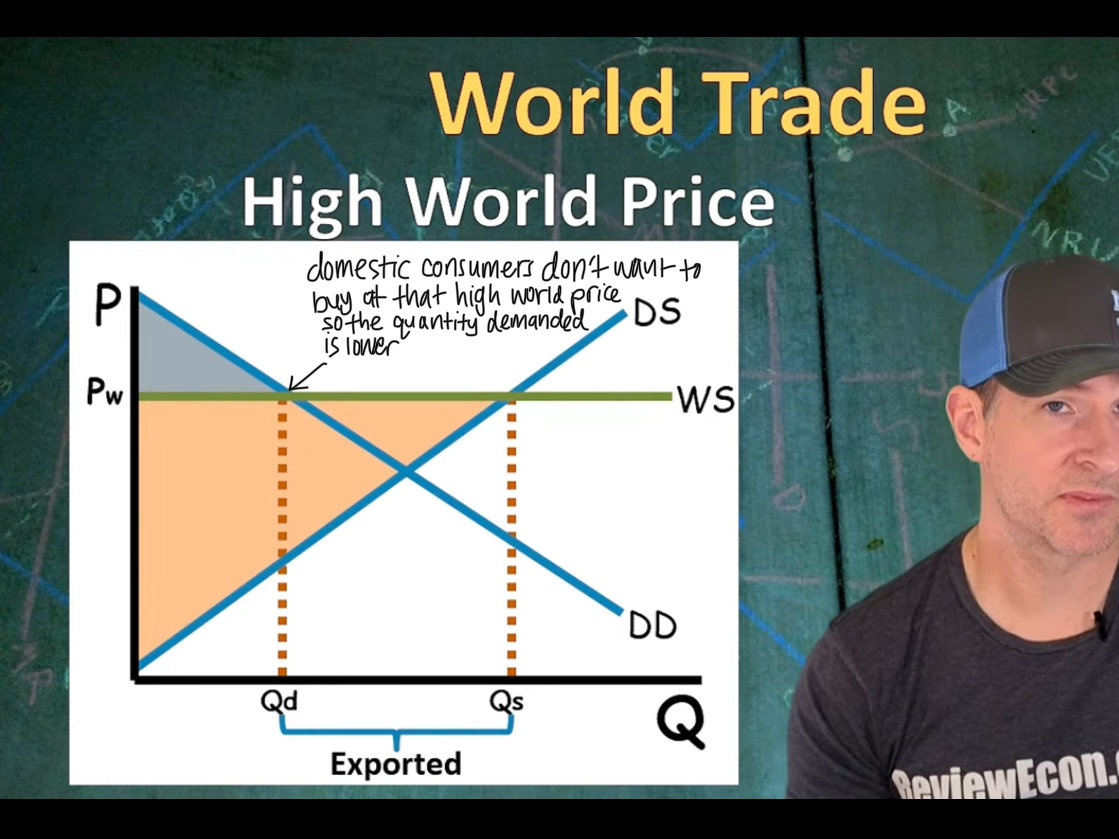

Note: World trade increases economic surplus

High world price

Quota

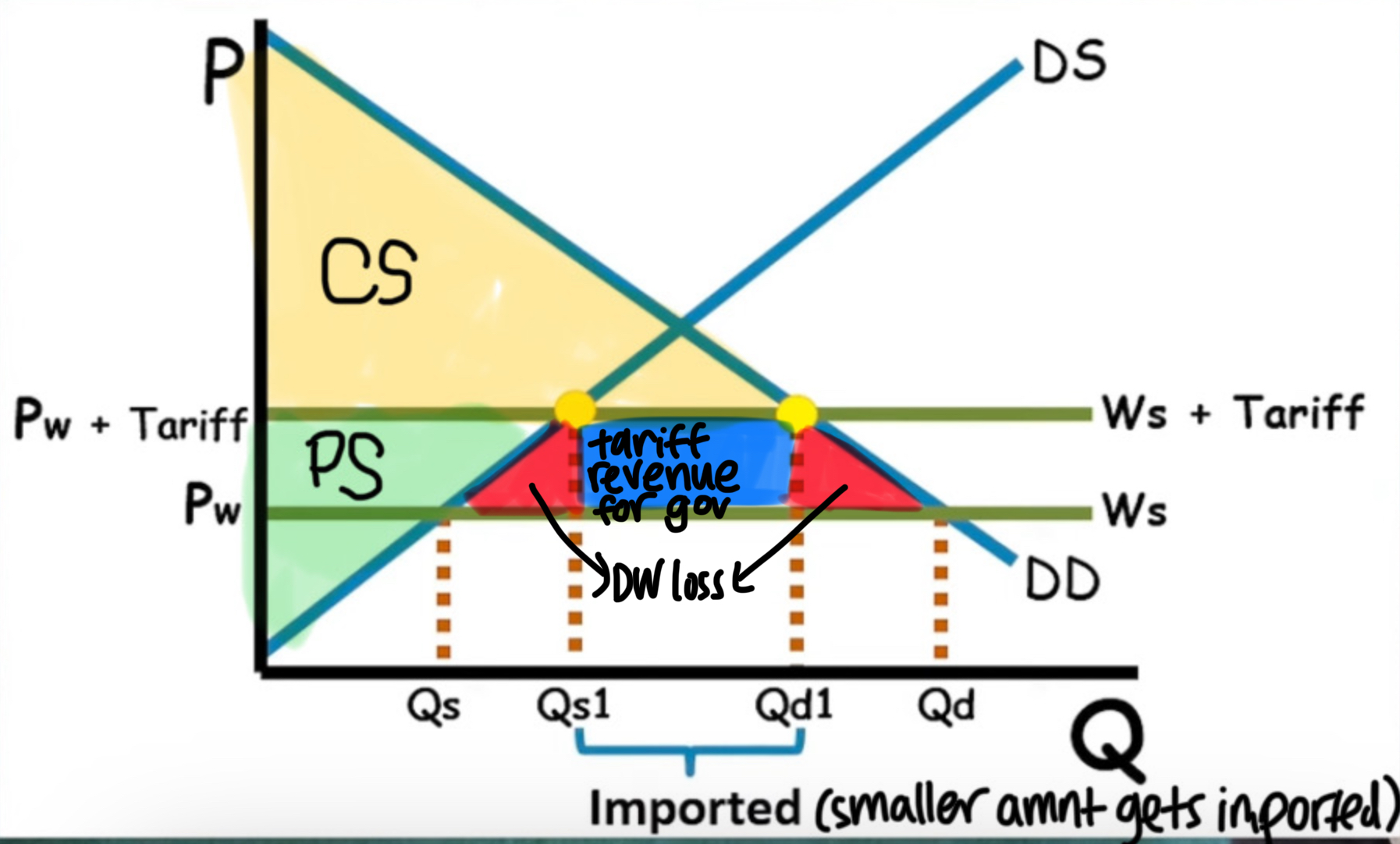

Places a limit on the amount of imported goods. It limits trade, decreases economic surplus, and creates deadweight loss

Tariff

A tax on imports. Results in higher world price. It limits trade, decreases economic surplus, and creates deadweight loss

Production function

Shows the relationship between the quantity of inputs and quantity of outputs (long-run and short-run)

Short-run production function

At least one input is fixed and u can change the quantity of labor, which will change the quantity of outputs and rate of production. We have fixed amounts of physical capital, but we can increase the #of workers

Long-run production function

All inputs are variable (subject to change). We can change the rate of production and the capacity of production. We can change the amount of physical capital and #of workers in a firm

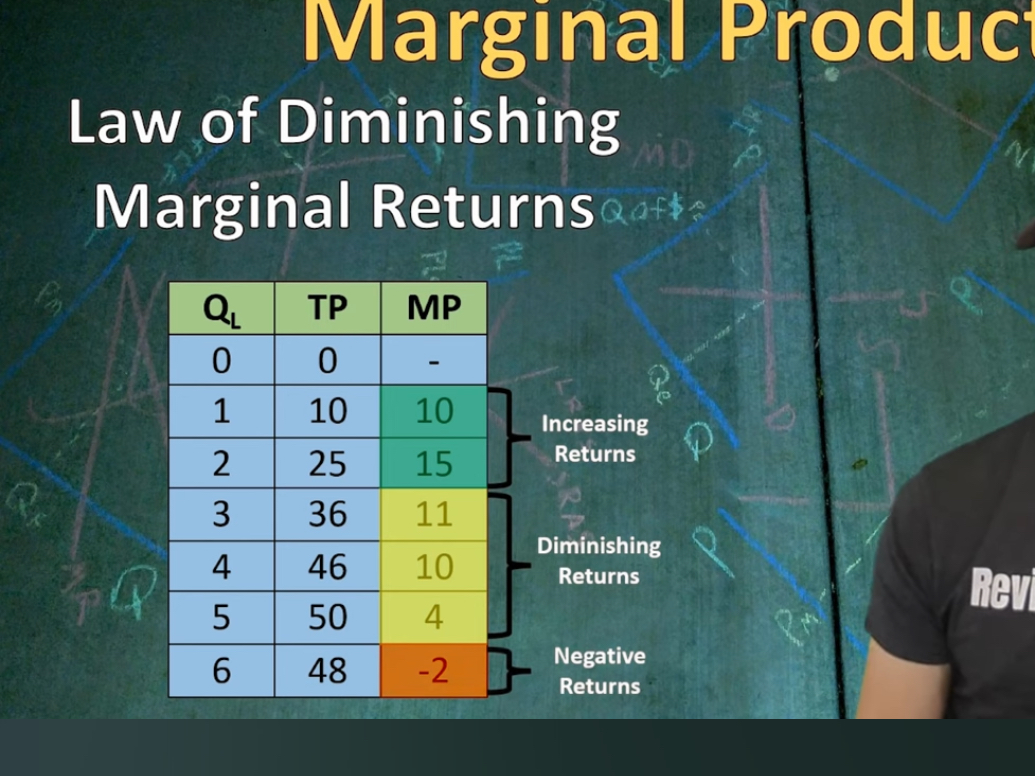

Marginal Product

Change in total product

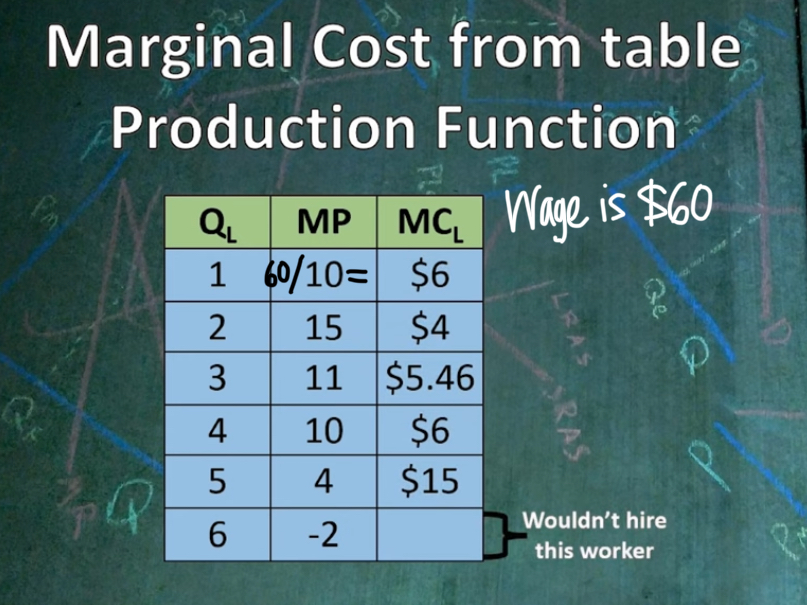

According to the Law of Diminishing Marginal Returns, at which quantity of workers does diminishing returns set in?

The 3rd worker bc that’s when the marginal product starts decreasing

Specialization

When each worker gets their own task, and they get highly skilled at their specific task. This increases the marginal product with each worker hired

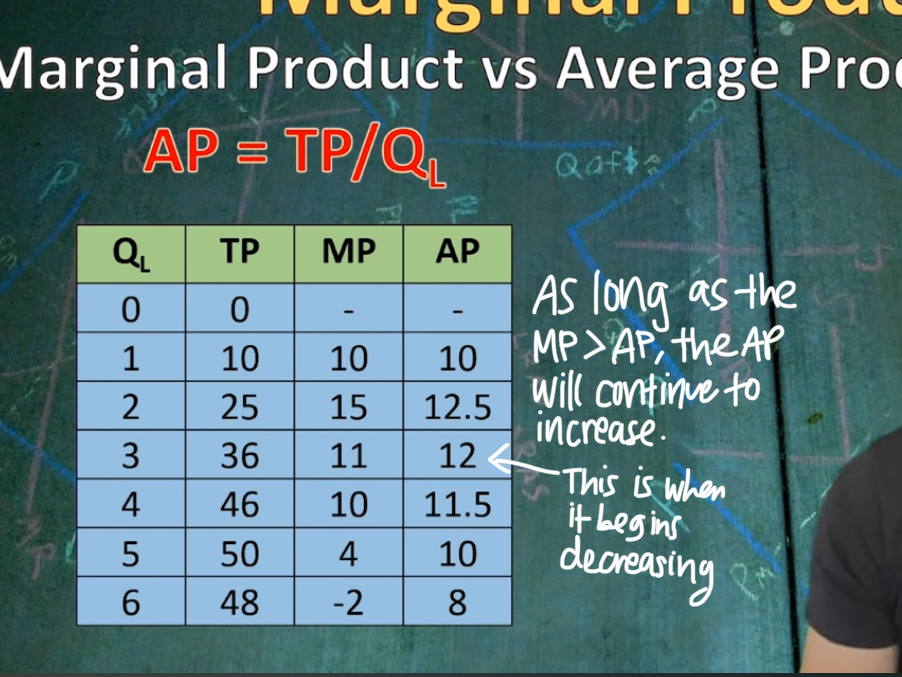

Average product

Total product / quantity of workers (aka finding average)

Marginal cost of labor

Wage that workers are paid/ marginal product of those workers