SAPPECO quiz 1 (modules 1a, 2a, 2b)

1/81

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

82 Terms

Microeconomics

The study of the economic

behavior of individuals and

firms.

Macroeconomics

The study of the economy as a

whole, looking at economy-wide

factors such as interest rates,

inflation, growth, and

unemployment.

Applied Economics

Reduction of abstraction

a. Attaching labels to variables and

concepts in the core theory

b. Applying additional structure to

the theory

c. Providing numerical values for

key parameters

d. Interpret specific real events

Applied Economics

The reduction of abstraction:

formula for marginal rate of substitution

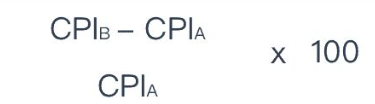

formula for inflation rate

consumer price index

CPI

Applied Economics

combination of macroeconomics and microeconomics

Laws of Demand and Supply

The Price Theory

Law of Diminishing Marginal Utility

Cournot Equilibrium

Nash Equilibrium

economic laws and theories

Formula to calculate the economic price

consumers

the people who buy goods and services

producers

create or provide a certain good (product) or

service. Producers can be individuals or

companies.

Demand

a schedule or curve that shows the various

amounts of a product that consumers are

willing and able to purchase at

each of a series of possible

prices during a specified

period of time.

Supply

a schedule or curve showing the various

amounts of a product that producers are willing and able to make available for sale at each of a series of possible prices during a specific period, other things equal.

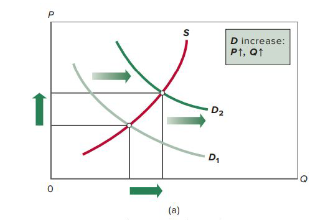

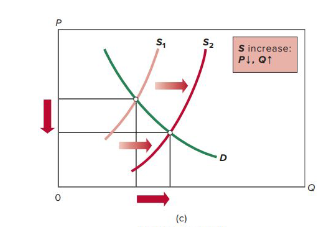

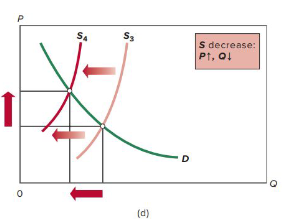

increase in demand

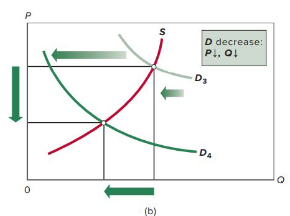

decrease in demand

increase in supply

decrease in supply

Commodity

A raw material, such as oil or copper, that is

usually traded in bulk. Changes in commodity

prices can have significant economic effects by, for example, feeding through into consumer prices.

Utility

In economics, utility is a term used to determine

the worth or value of a good or service. More

specifically, utility is the total satisfaction or

benefit derived from consuming a good or

service

1. What to produce?

2. How to produce?

3. For whom to produce?

4. What provisions (if any) are to be made for

economic growth?

4 Basic Economic Problems

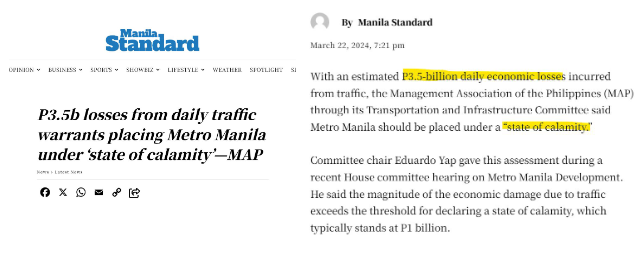

traffic congestion

cartel

Remittance Dependency

Natural Disaster Vulnerability

Environmental Sustainability

Socioeconomic Problems

Traffic Congestion

cartel

Agreement where a group of producers

collaborate to fix the price, or restrict the

supply, of a good or service. Cartels among

companies are often outlawed by government

antitrust regulations because they restrict

competition.

Remittance Dependency

play a crucial

role in supporting many Filipino

families, over-reliance on this

income source exposes the

economy to global economic

fluctuations and uncertainties in

foreign employment conditions.

Diversification strategies are

essential to mitigate risks

Natural Disaster Vulnerability

According to the Asian Development Bank,

the Philippines is among the world’s most

disaster-prone countries, experiencing an

average of 20 typhoons annually.

Environmental Sustainability

The Philippines placed 158th out of 180 countries in the 2022 edition of

the biennial Environmental Performance Index. Deforestation, pollution,

and habitat destruction are significant environmental challenges.

scarcity

Limited supply

shortage

temporary loss of supply

Self Actualization

Esteem

Love and Belonging

Safety needs

Physiological needs

Maslow’s Hiearchy of needs

Law of Demand

the claim that, other

things being equal, the

quantity demanded of a

good falls when the price

of the good rises

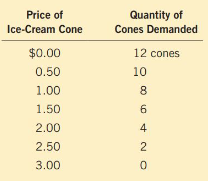

demand schedule

a table that shows the quantity demanded at each price. It illustrates the quantity demanded of the good changes as its price varies.

income

When this is lower, it means that you

have less to spend in total, so

you would have to spend less

on some—and probably

most—goods.

it becomes higher

When the peso rate is lower what happens to the dollar rate

normal good

good where the demand for a good falls when

income falls

inferior good

the good where the demand for a good rises when income falls

substitutes

complements

price of related goods

substitutes

When a fall in the price of one good

reduces the demand for another good

complements

When a fall in the price of one good

raises the demand for another good

tastes

Economists normally do not try

to explainthis because

they are based on

historical and psychological

forces that are beyond the realm

of economics. Economists do,

however, examine what

happens when tastes change.

number of buyers

In addition to the preceding

factors, which influence the

behavior of individual buyers,

market demand depends on this

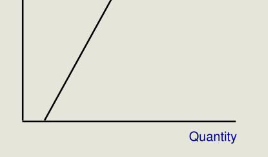

Law of Supply

the claim that, other things being equal,

the quantity supplied of a good rises when the

price of the good rises.

Input Prices

Technology

Expectations

Number of Sellers

Shifts in the Supply Curve

input prices

When the price of one or more

of the inputs rises, producing

the good is less profitable, and

firms supply less ice cream

Technology

Reduces the amount of labor

necessary to produce the good.

(e.g. Bibingka Oven)

Bibingka Oven

Traditional Bibingka Equipment

Expectations

The amount of product a firm

supplies today may depend on

its expectations about the

future

Number of Sellers

Market supply depends on the

number of sellers. Generally,

with more sellers, there is more

supply. With fewer sellers, there

is less supply.

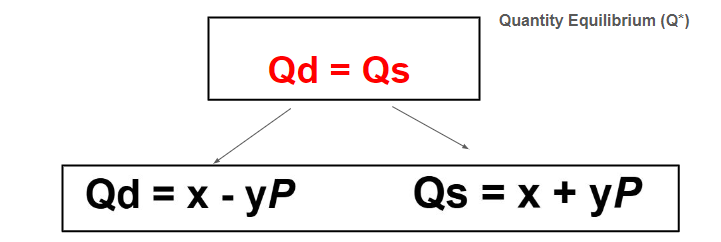

Equilibrium

a situation in which the market price has

reached the level at which quantity supplied equals quantity demanded.

Equilibrium Price

the price that balances quantity supplied and quantity demanded

Equilibrium Quantity

the quantity supplied and the quantity demanded at the equilibrium price

The Price Theory

an economic theory that states

that the price for a specific good

or service is determined by the

relationship between its supply

and demand at any given point.

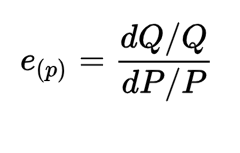

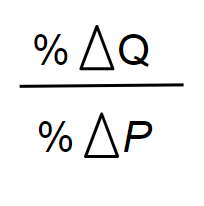

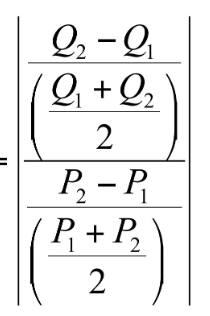

Price Elasticity of Demand

measures how much the quantity demanded

(Qd) responds to a change in price.

elastic

quantity demanded responds significantly to

changes in the price

Inelastic

quantity demanded responds only slightly to changes in the price.

elastic

close substitutes tend to

have more______ demand

inelastic

necessities

elastic

luxuries

basic formula of Economy price

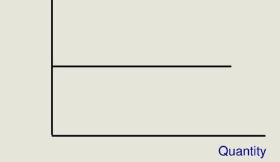

Infinity

calculated price elasticity of perfectly elastic

Perfectly Inelastic

result of change in price that declines to zero

greater than 1

calculated price elasticity of elastic

1

calculated price elasticity of unitary elasticity

Unitary Elasticity

result of change in price that is equivalent percentage change

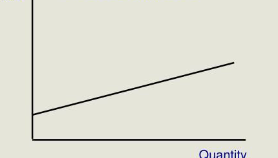

less than 1

calculated price elasticity of inelastic

inelastic

result of change in price with insignificant change

0

calculated price elasticity of Perfectly Inelastic

Perfectly inelastic

result of change in price with no change

Elastic

result of change in price that has a significant change in demand

Midpoint formula

Price Elasticity of Supply

measures how much the quantity supplied (Qs)

responds to a change in price.

This elasticity is usually positive because a

higher price gives producers an incentive to

increase output.

Firms operating close to full capacity.

Firms have low levels of stocks, therefore there

are no surplus goods to sell.

With agricultural products, supply is inelastic in

the short run

Supply could be inelastic for

the following reasons:

If there is spare capacity in the factory.

If there are stocks available.

If it is easy to employ more factors of

production.

If a product can be sold from the internet which

increases the scope of international competition

and increases options for supply

Supply could be elastic for

the following reasons:

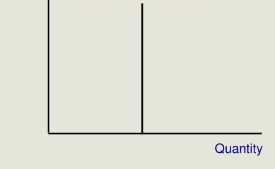

perfectly elastic

Elastic

Perfectly Inelastic

Inelastic

Equilibrium Formula

Equilibrium

balance between supply of and demand for a good at a market clearing price

All else being equal

What does Cetris Paribus mean

MPPa/MPPb

If MPPa and MPPb represents the marginal physical products of two inputs, then the marginal rate of substitution would be