Chapter 11 Technology, Productions, and Costs

1/65

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

66 Terms

Technology

The processes a firm uses to turn inputs outputs of good and services

Technological change

A change in the ability of a firm to produce a given level of outputs with a given quantity of inputs

Short Run

the period of time during which at least one of a firms inputs is fixed

Long run

the period of time in which a firm can vary all of its inputs, adapt new technology, and increase or decrease the size of its physical plant

total cost

the cost of all its inputs a firm uses in production

Variable cost

Costs that change as output changes

Fixed costs

Costs that remain constant as output changes

Opportunity cost

The highest valued alternative that must be given up to engage in an activity

Explicit Cost

A cost that involves spending money

Implicit Cost

A non monetary opportunity cost

Production Function

The relationship between the inputs employed by a firm and the maximum output it can produce with those inputs

Average total cost

Total Cost divided by the quantity of output produced

Marginal product of labor

The additional output a firm produces as result of hiring one more worker

Law of diminishing returns

The principle that, at some point, adding more of a variable output, such as labor, to the same amount of fixed input, such as capital, will causes the marginal product of the variable input to decline

Average product of labor

The total output produced by a firm divided by the quantity of workers

Marginal cost

The change in a firm's total cost from producing one or more unit of a good or service

Average fixed cost

Fixed Cost divided by the quantity of output produced

Average variable cost

Variable cost divided by the quantity of output produced

Long- run average cost curve

A curve that shows the lowest cost at which a firm is able to produce a given quantity of output in the long run, when no inputs are fixed

Economies of scale

The situation when a firms long run average costs fall as it increase the quantity of output it produces

Constant returns to scale

The situation in which a firms long run average costs remains unchanged as it increases output

Minimum efficient scale

The level of output at which all economies of scale are exhausted

Dis economies of scale

The situation in which a firms long run average costs rise as the firm increases its output

Isoquant

A cure that shows all the combinations of two inputs, such as capital and labor, that will produce the same level of output

Marginal rate of technical subsitutions

The rate at which a firm is able to substitute one input for another while keeping the level of output the same

Isocost line

All the combinations of two inputs, such as capital and labor, that have the same total cost

a. more output to be produced from the same inputs; less output to be produced from same inputs

Fill in the blanks. A positive technological change causes_______ , while a negative technological

change causes _______.

a. more output to be produced from the same inputs; less output to be produced from same inputs

b. less output to be produced from the same inputs; more output to be produced from same inputs

c. the same level of output to be produced from the same inputs more output to be produced from

same inputs

d. None of the above occurs.

b. where at least one input is fixed; where all inputs are variable

Fill in the blanks. The short run is a period of time _______, while the long run is s period of time

_______.

a. where at least one input is fixed; where all inputs are fixed

b. where at least one input is fixed; where all inputs are variable

c. where all inputs are variable; where at least one input is fixed

d. None of the above is true.

a. the relationship between the inputs used by the firm and the maximum output it can produce.

3. The production function shows

a. the relationship between the inputs used by the firm and the maximum output it can produce.

b. the relationship between the variable inputs and the cost of production.

c. the relationship between the fined inputs and the cost of production.

d. none of the above

c. stays the same regardless of the level of output.

4. Total fixed cost

a. increases as output increases.

b. decreases as output increases.

c. stays the same regardless of the level of output.

d. None of the above is true.

a. They are part of fixed cost.

If the number of people in a publishing company does not go up or down with the quantity of books itpublishes, then how should we categorize the salaries and benefits paid to these employees?

a. They are part of fixed cost.

b. They are part of variable cost.

c. They are an implicit cost.

d. They are not considered a part of the cost of production

a. opportunity cost

6. Which of the following is known as the highest-valued alternative that must be given up in order to engage in an activity?

a. opportunity cost

b. explicit cost

c. total cost

d. variable cost

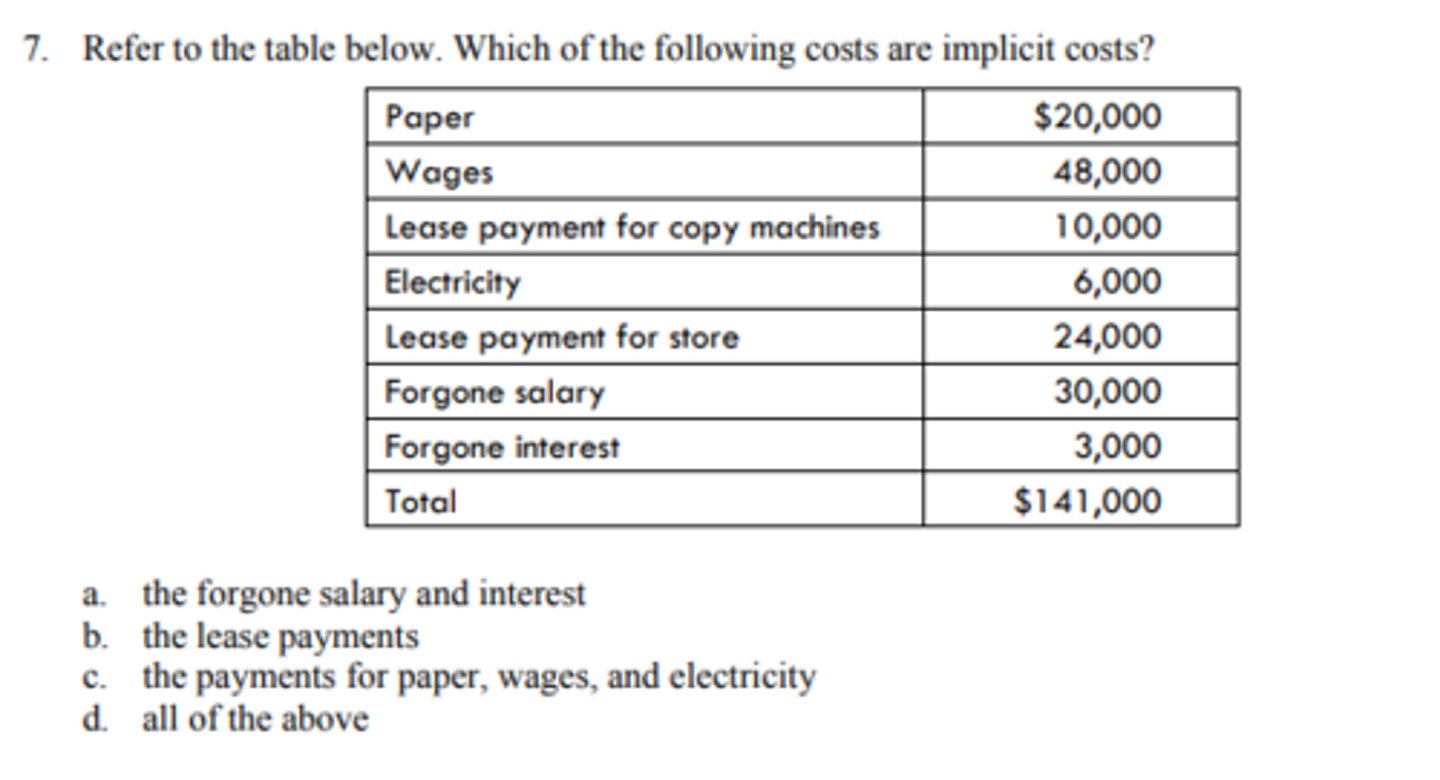

a. the forgone salary and interest

a. total variable cost divided by the level of output produced.

8. Average variable cost is

a. total variable cost divided by the level of output produced.

b. total cost divided by the level of output produced.

c. total fixed cost divided by the level of output produced.

d. None of the above.

b. in the short run.

9. The law of diminishing returns applies

a. in the long run.

b. in the short run.

c. either in the short run or the long run.

d. none of the above.

b. must be below the average variable cost curve.

10. When average variable cost curve is decreasing, marginal cost curve

a. must be above the average variable cost curve.

b. must be below the average variable cost curve.

c. can be above or below the average variable cost curve.

d. None of the above is true.

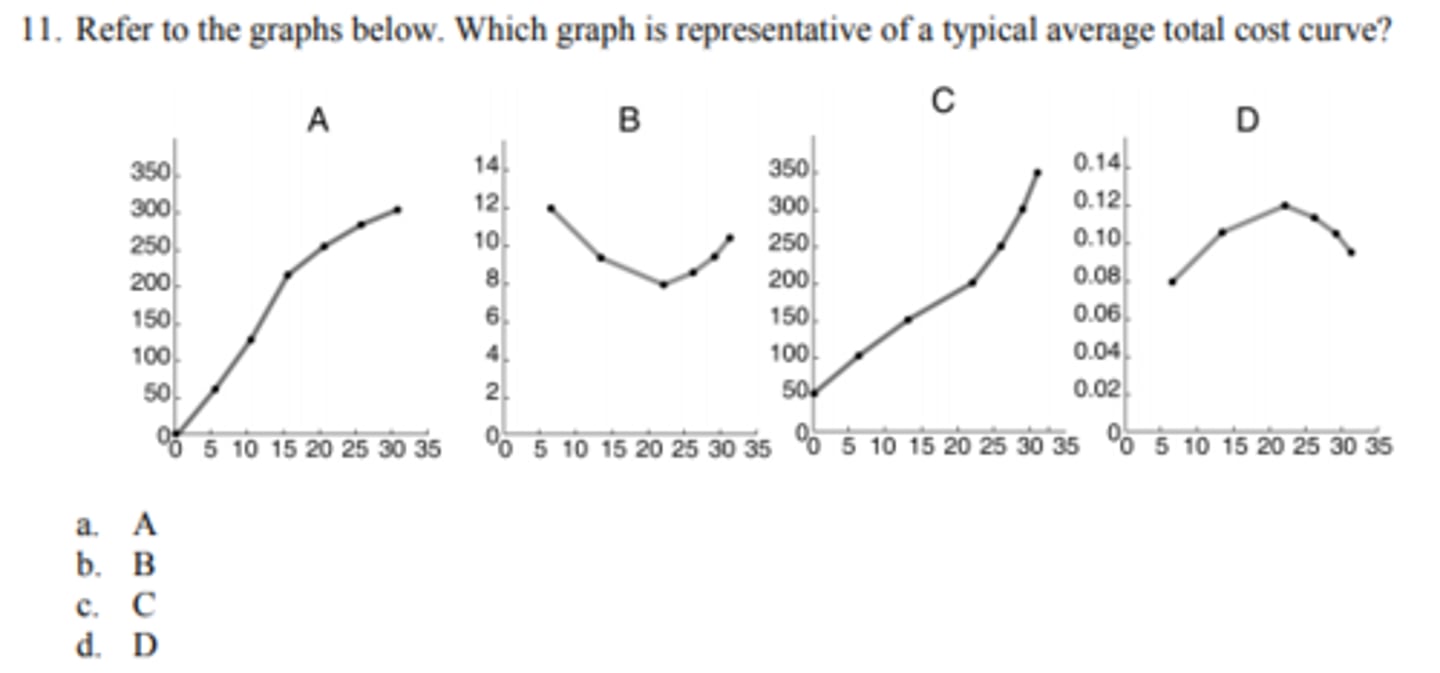

b. B

d. i, ii, and iii

12. Which of the following is true?

i. Total cost = fixed cost + variable cost

ii. Total cost = explicit costs + implicit costs

iii. Economic cost = accounting cost + implicit costs

a. i only

b. ii only

c. i and ii only

d. i, ii, and iii

a. the lowest cost of producing any level of output.

13. A long-run average cost curve has

a. the lowest cost of producing any level of output.

b. the highest cost of producing any level of output.

c. an inverted U-shape.

d. none of the above.

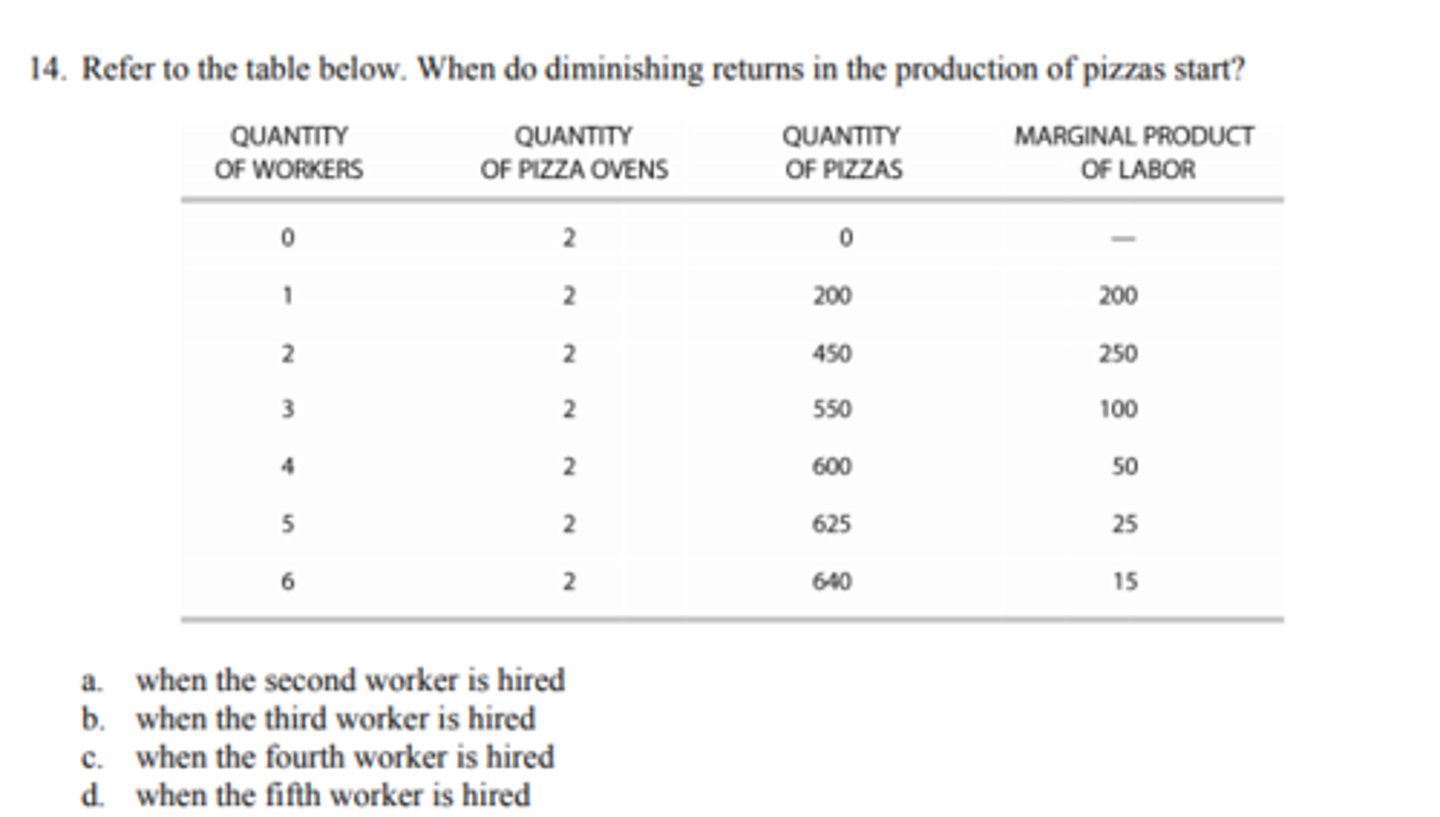

b. when the third worker is hired

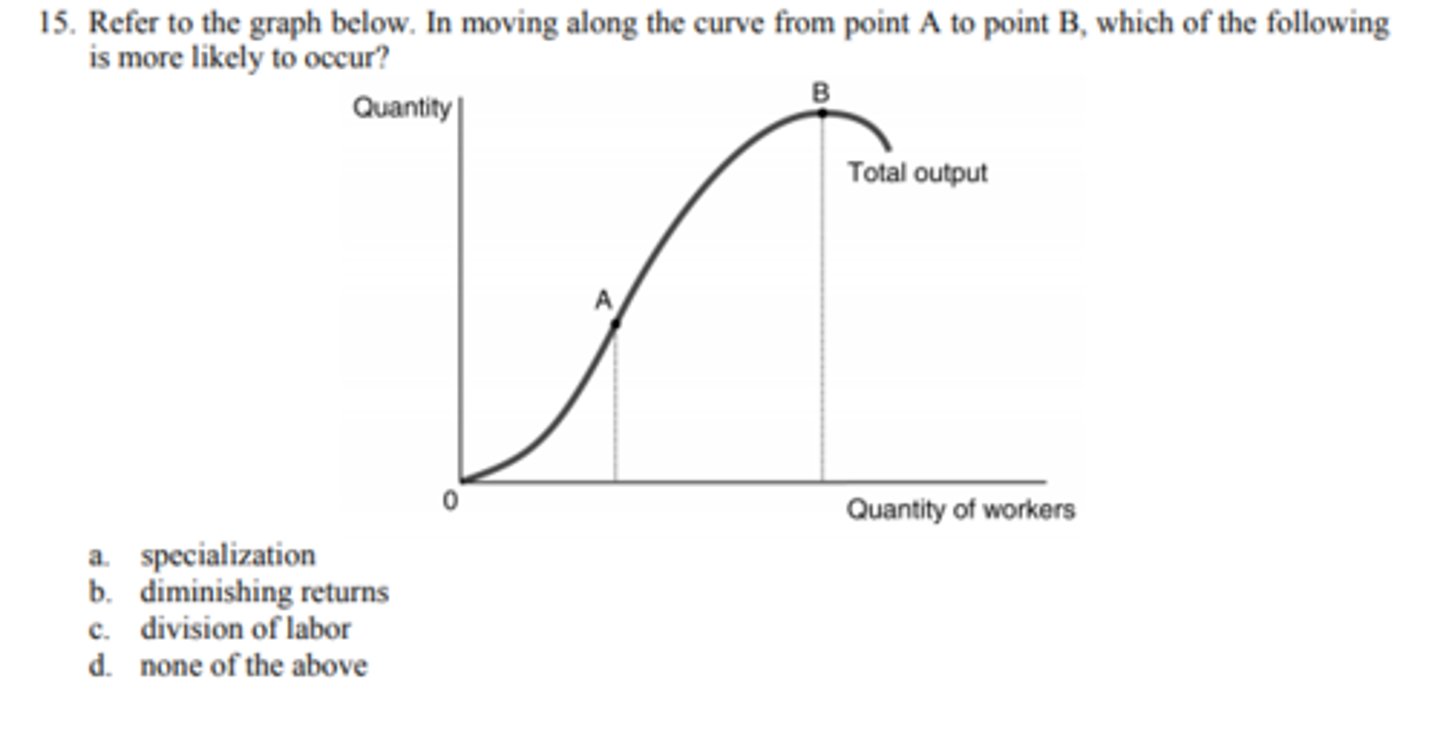

b. diminishing returns

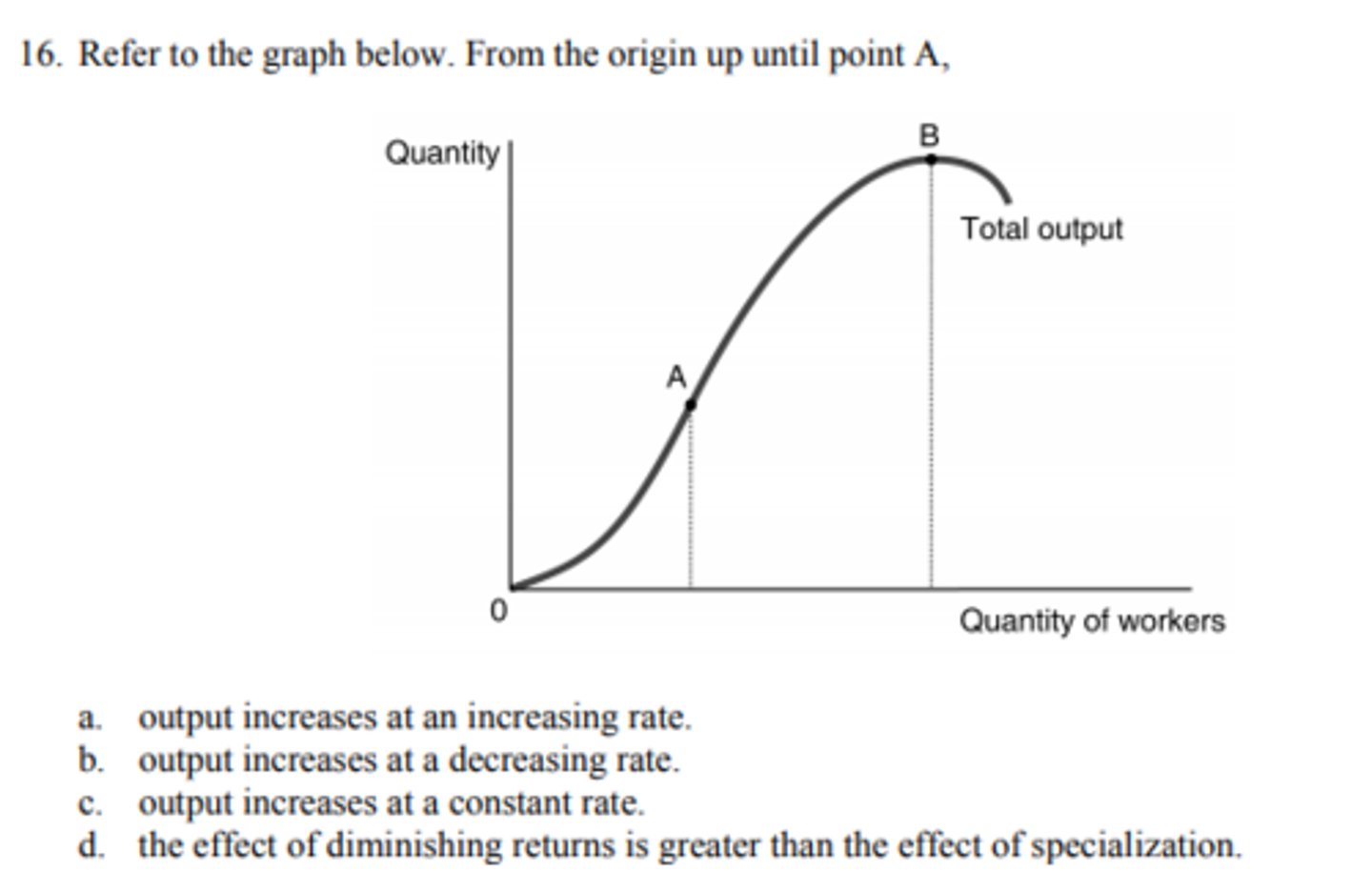

a. output increases at an increasing rate.

b. the downward sloping part of the long run average cost curve; the upward sloping part of the long run average cost curve

17. Fill in the blanks. Economies of scale are represented by_______, while diseconomies of scale are

represented by _______.

a. the upward sloping part of the long run average cost curve; the downward sloping part of the long

run average cost curve

b. the downward sloping part of the long run average cost curve; the upward sloping part of the long run average cost curve

c. the upward sloping part of the long run average cost curve; the upward sloping part of the long

run average cost curve

d. the downward sloping part of the long run average cost curve; the downward sloping part of the

long run average cost curve

c. constant; total fixed cost

18. Fill in the blanks. The vertical distance between the total cost and the total variable cost curves is

_______ and reflects _______.

a. variable; total fixed cost

b. constant; marginal cost

c. constant; total fixed cost

d. None of the above is true.

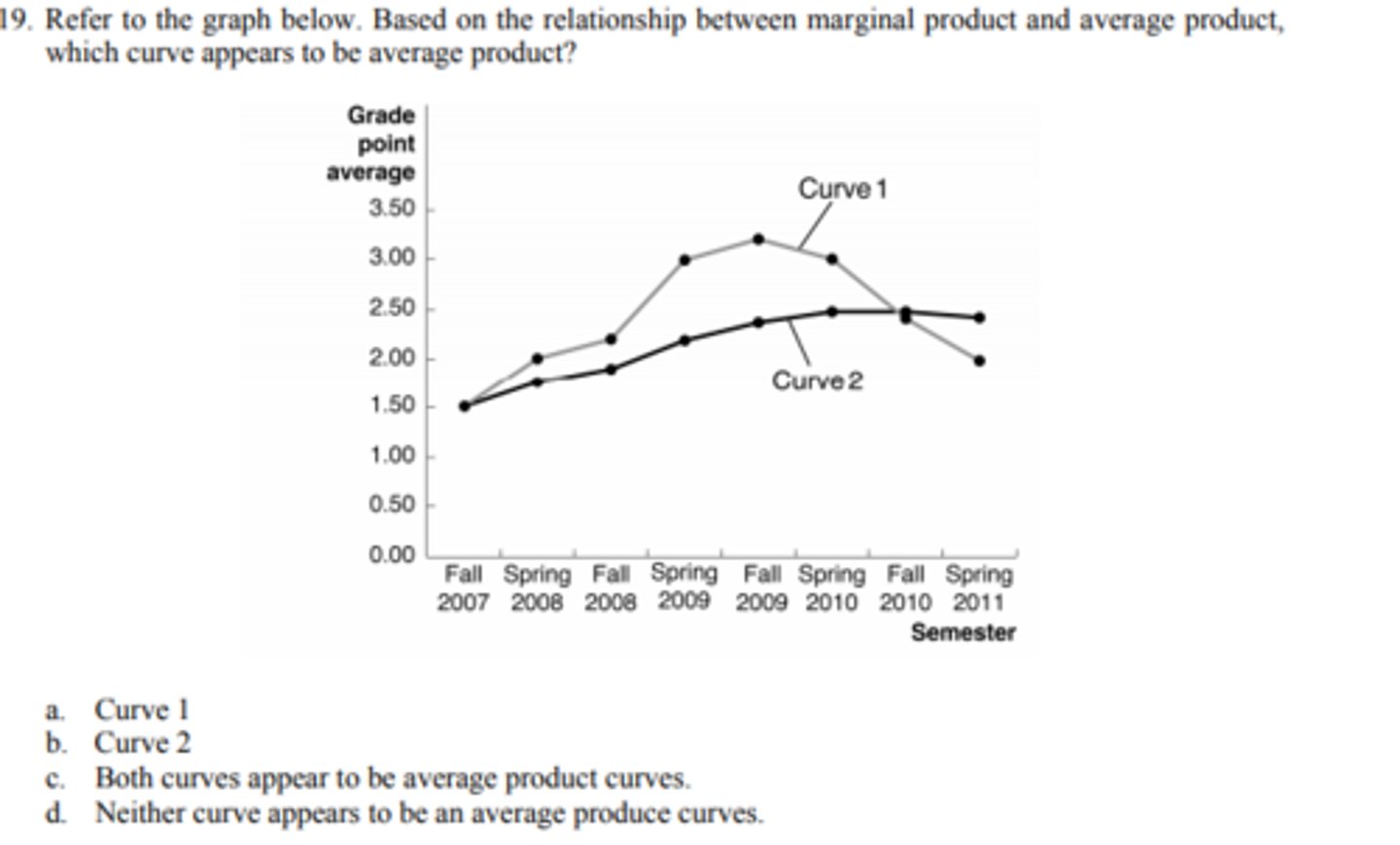

b. Curve 2

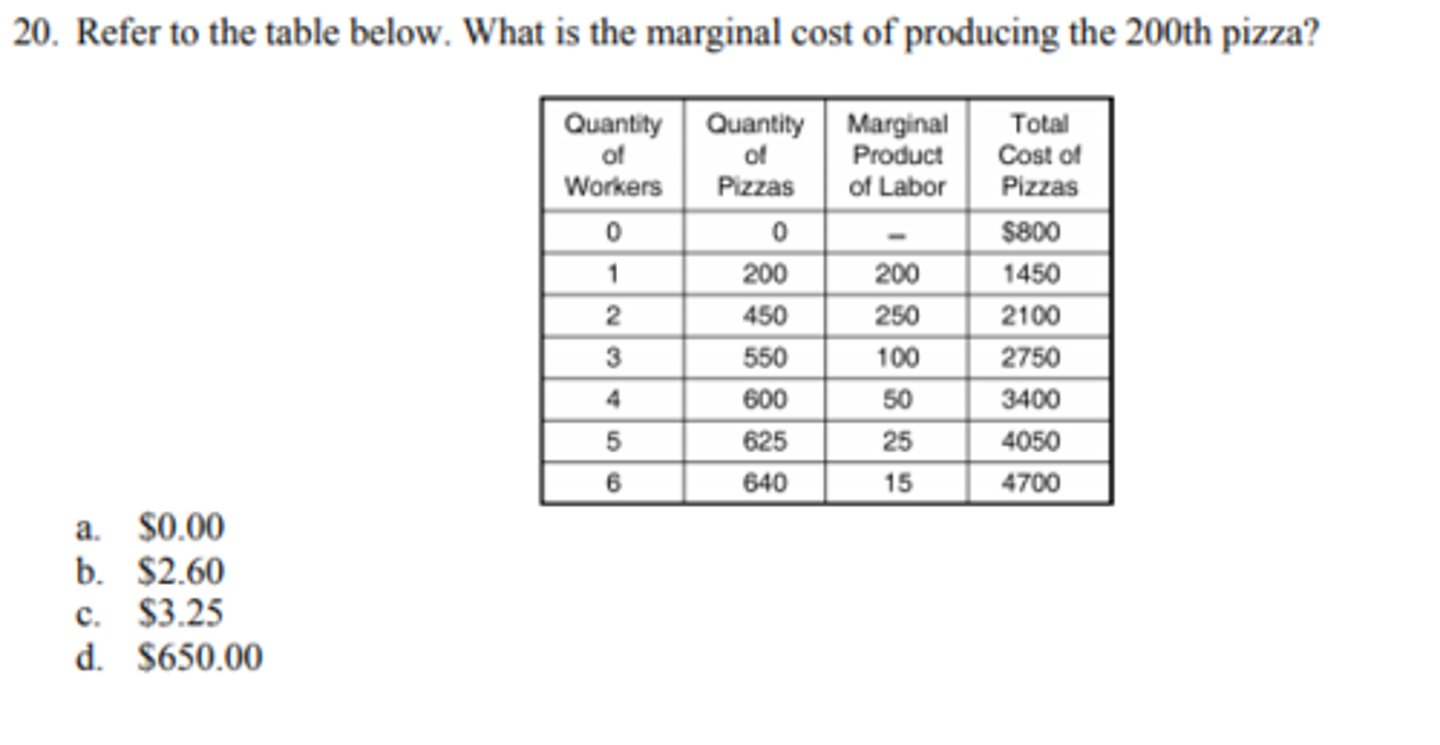

c. $3.25

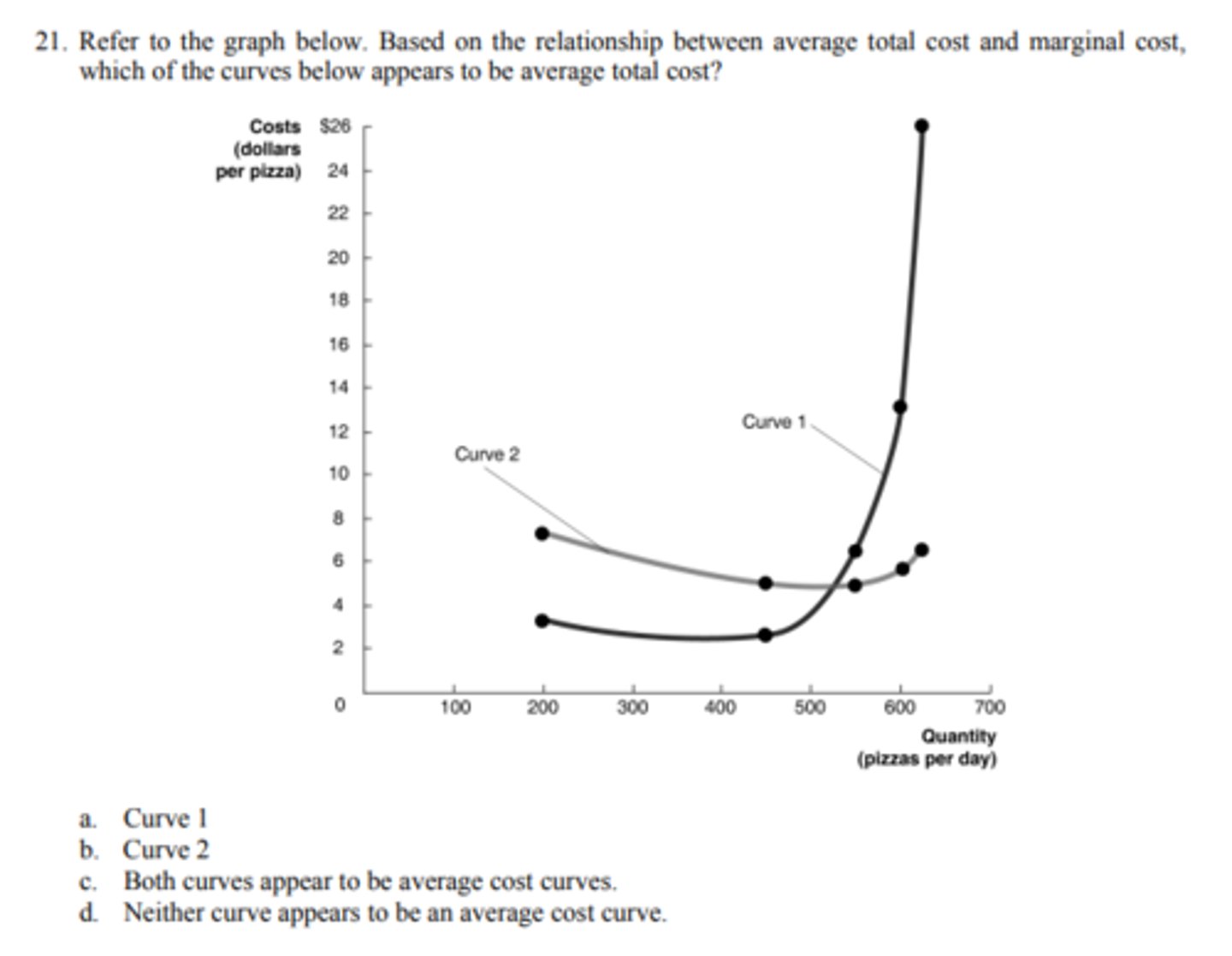

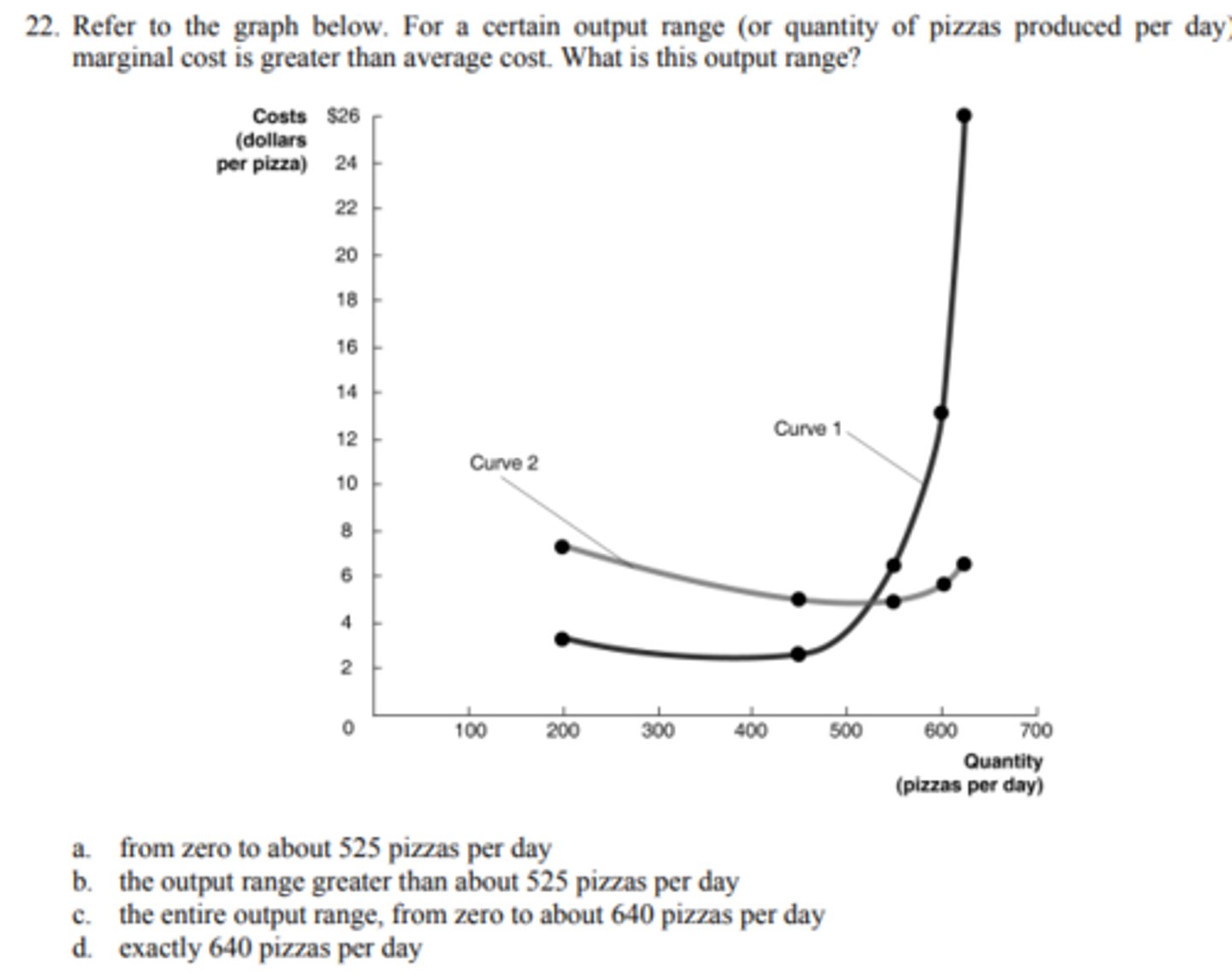

b. Curve 2

b. the output range greater than about 525 pizzas per day

b. decreasing.

23. When marginal cost is less than average total cost, average total cost must be

a. increasing.

b. decreasing.

c. constant.

d. None of the above.

c. marginal product of labor is greater than average product of labor.

24. When average product of labor is increasing,

a. marginal product of labor equals average product of labor.

b. marginal product of labor is less than average product of labor.

c. marginal product of labor is greater than average product of labor.

d. None of the above is true.

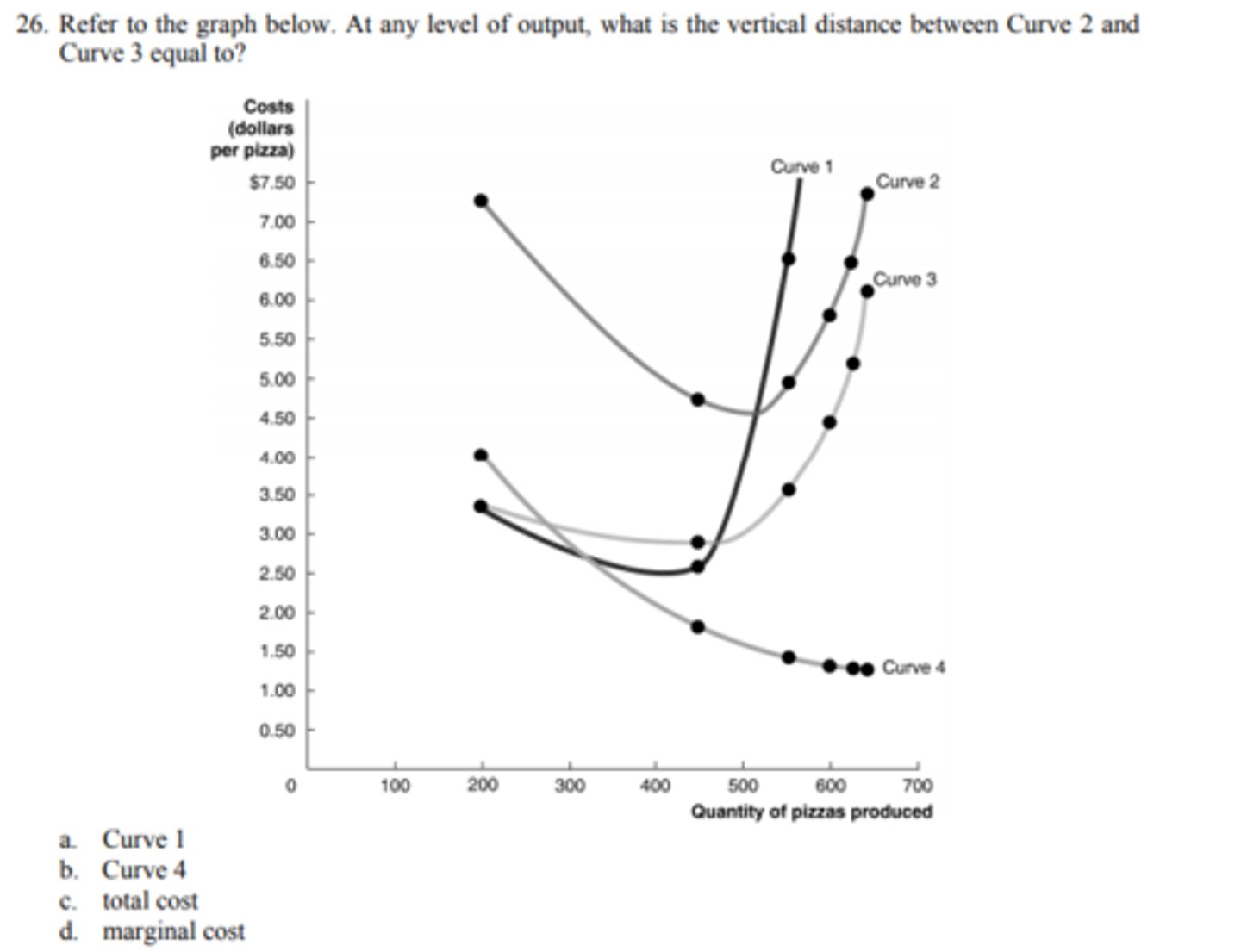

c. average fixed cost

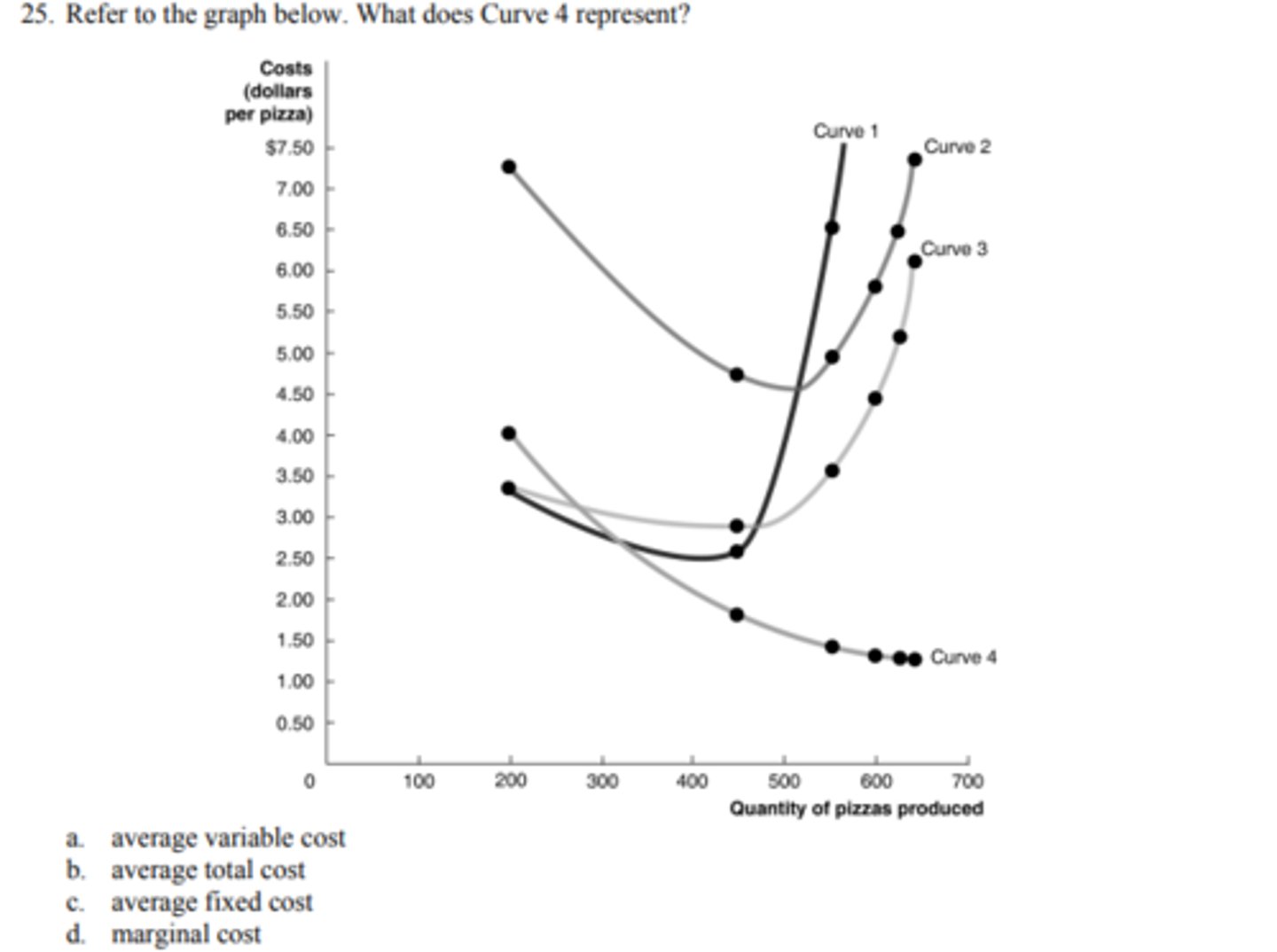

b. Curve 4

c. average fixed cost

27. The following cost measures reach their minimum points when they are equal to the value of marginal cost, except one. Which cost measure is the exception?

a. average variable cost

b. average total cost

c. average fixed cost

d. There is no exception; all three measures above reach their minimum values when they are equal

to the value of marginal cost.

a. the rate at which firms are able to substitute one input for another while keeping the level of output constant.

28. Marginal rate of technical substitution is

a. the rate at which firms are able to substitute one input for another while keeping the level of output constant.

b. the rate at which firms are able to substitute one input for another while increasing the level of

output constant.

c. the rate at which firms are able to substitute one input for another while decreasing the level of

output constant.

d. none of the above

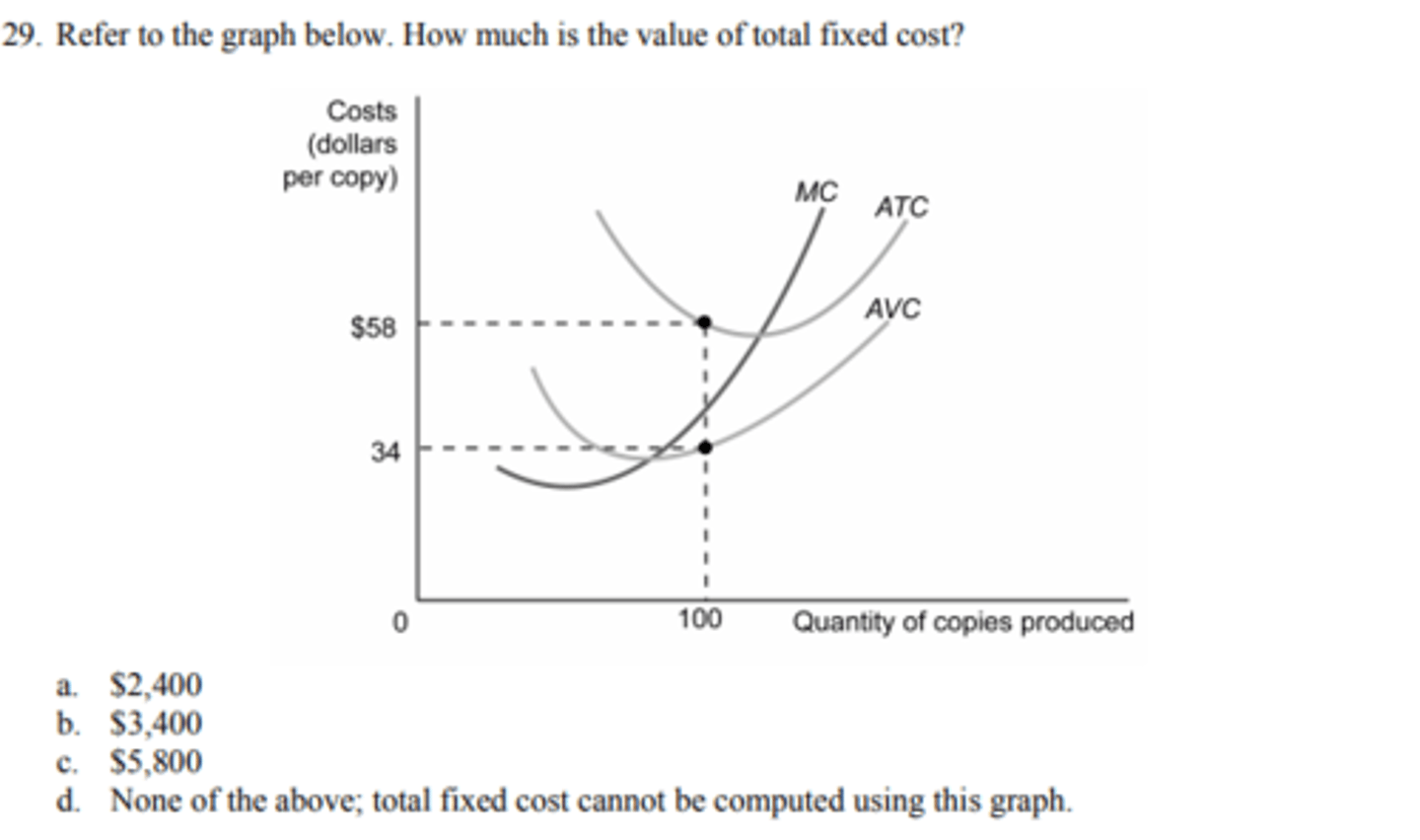

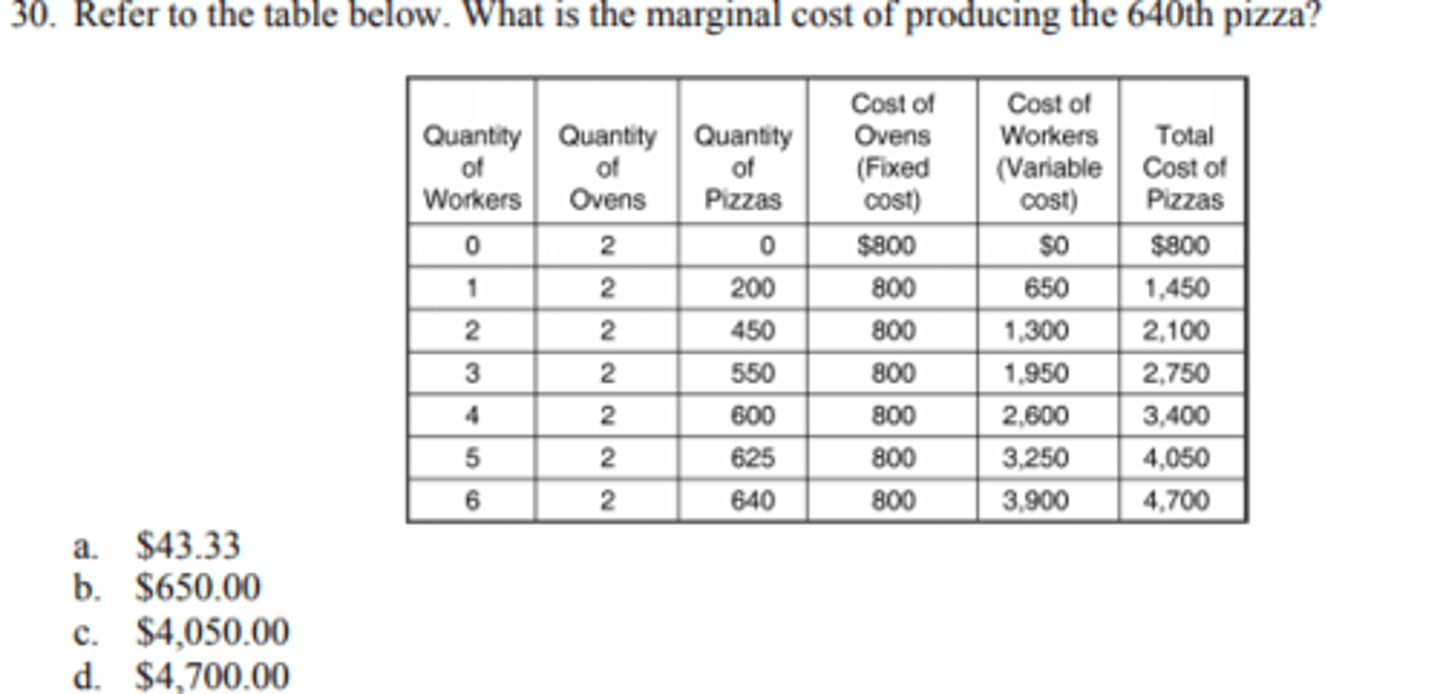

a. $2,400

a. $43.33

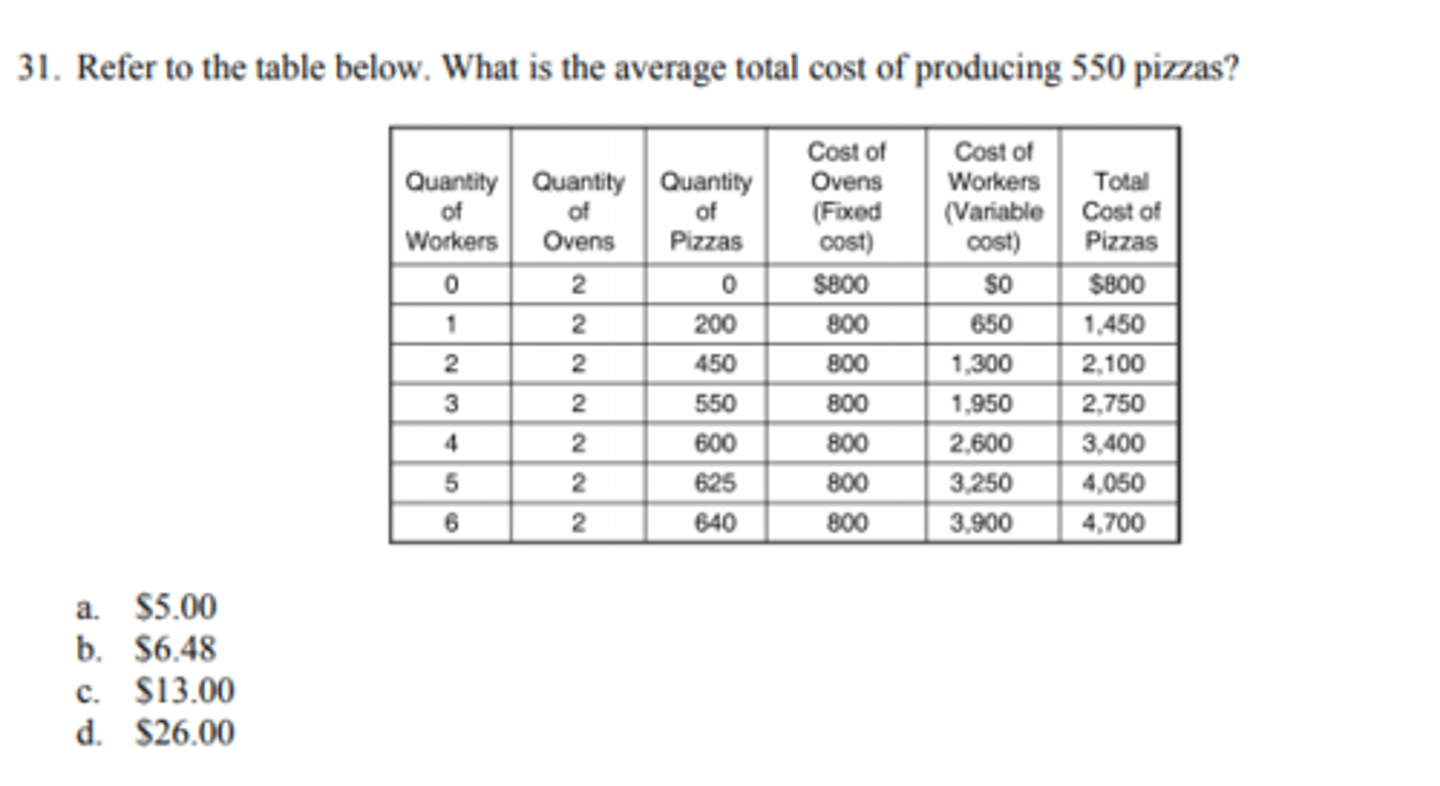

a. $5.00

b. The difference decreases.

32. What happens to the difference between average variable cost and average total cost as the level of

output increases?

a. The difference increases.

b. The difference decreases.

c. The difference remains the same.

d. The difference first increases then decreases.

c. smaller; average fixed cost

33. Fill in the blanks. As output increases, the vertical distance between average total cost and average

variable cost curves gets _______ and equals _______.

a. smaller; total fixed cost

b. larger; average fixed cost

c. smaller; average fixed cost

d. larger; marginal cost

b. the long-run average cost curve

34. Which of the following terms refers to the lowest cost at which a firm is able to produce a given level of output in the long run, when no inputs are fixed?

a. the long-run marginal cost curve

b. the long-run average cost curve

c. the variable inputs curve

d. economies of scale

c. Both (a) and (b) are correct.

35. Economies of scale

a. happens when the firm's long-run average total cost decreases as output increases.

b. is represented by the downward-sloping part of the long-run average cost curve.

c. Both (a) and (b) are correct.

d. None of the above is correct.

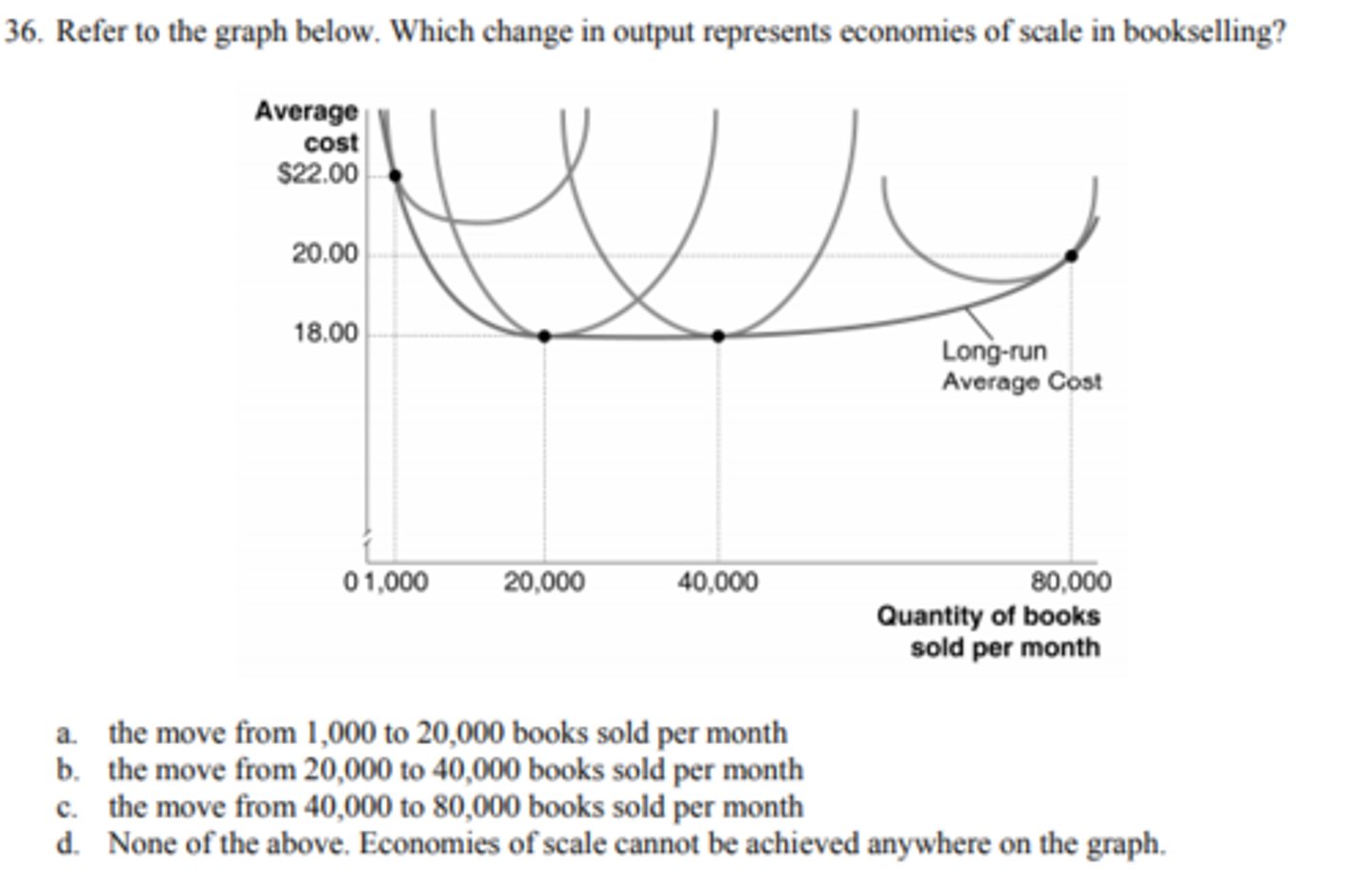

a. the move from 1,000 to 20,000 books sold per month

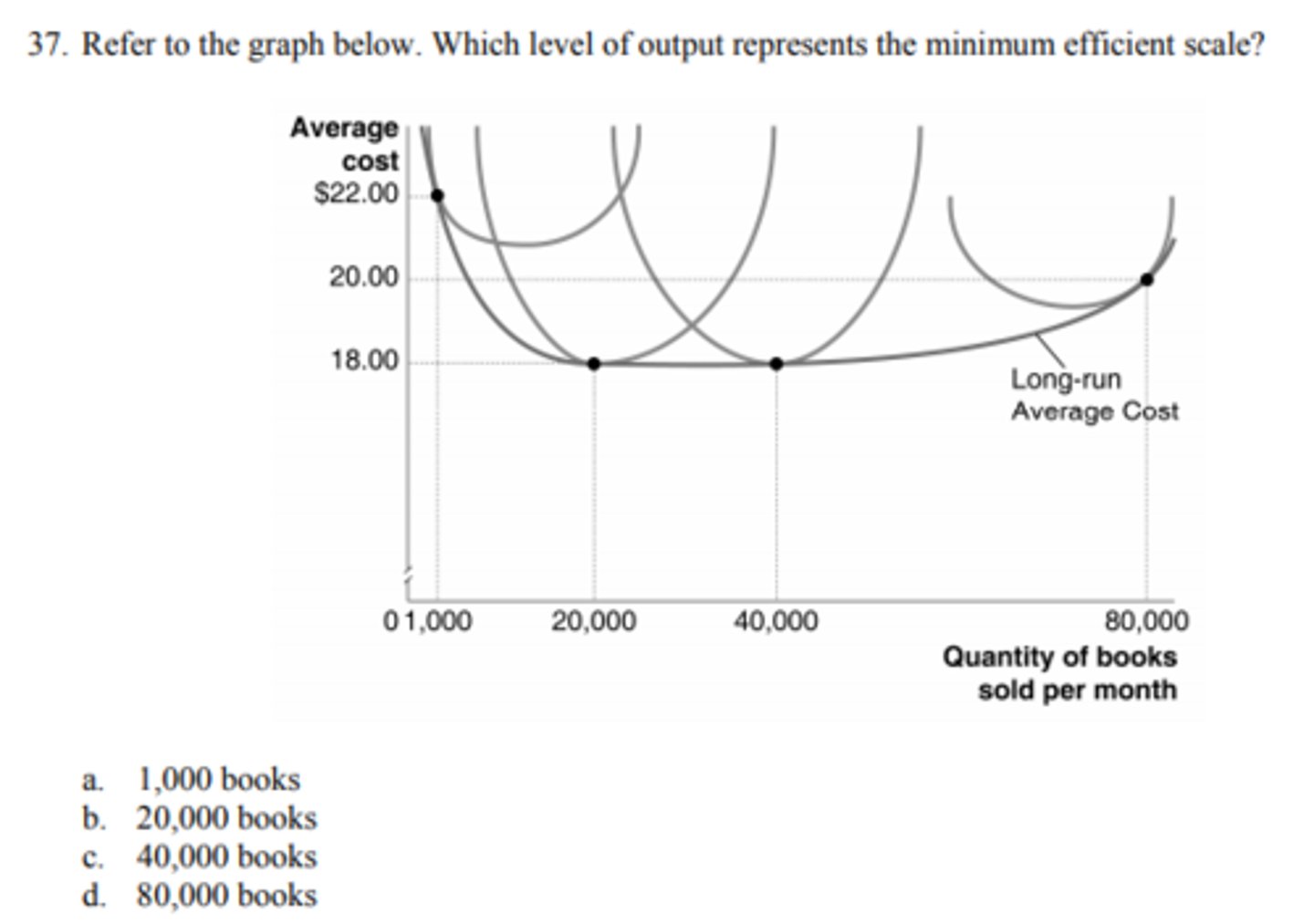

b. 20,000 books

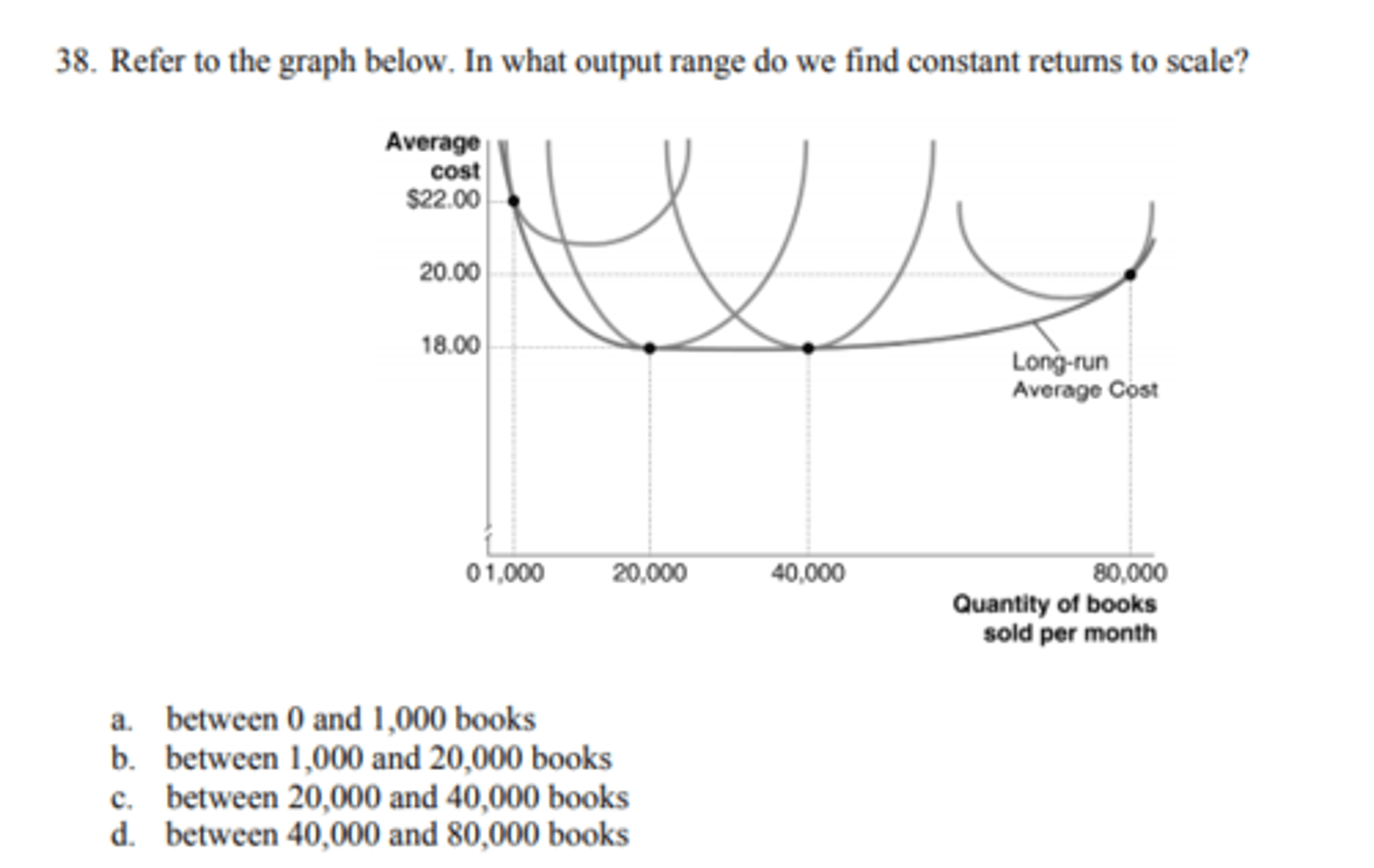

c. between 20,000 and 40,000 books

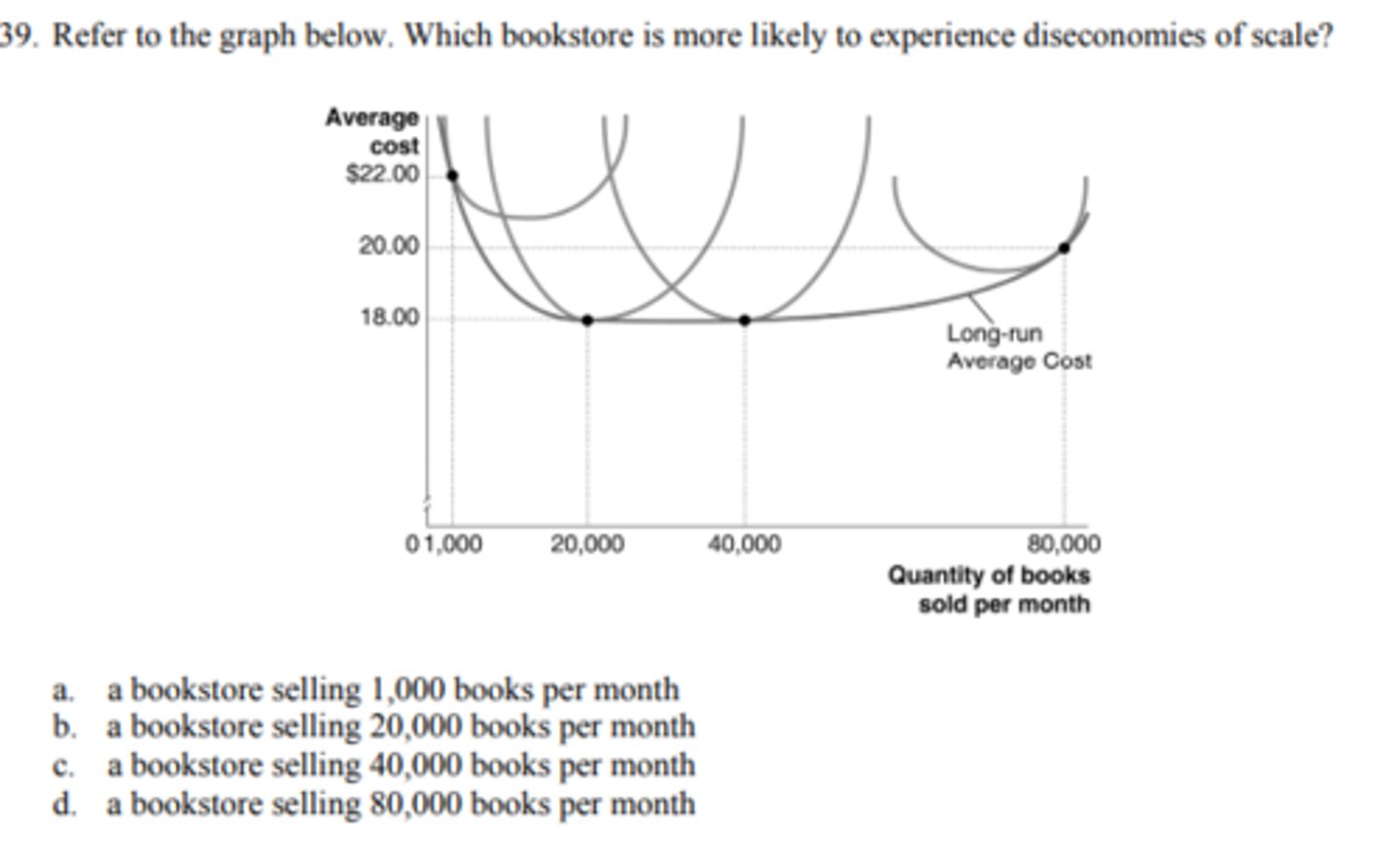

d. a bookstore selling 80,000 books per month

b. all economies of scale are exhausted.

40. Minimum efficient scale is the level of output at which

a. the firm has diseconomies of scale.

b. all economies of scale are exhausted.

c. the average cost is at its highest level.

d. None of the above is true.