Factor Markets microeconomics

1/18

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

19 Terms

Perfectly competitive labor market

-Many small firms are hiring workers

-Many workers with identical skills

-Wage is constant

-Workers are wage takers

profit maximization

MRP=MRC

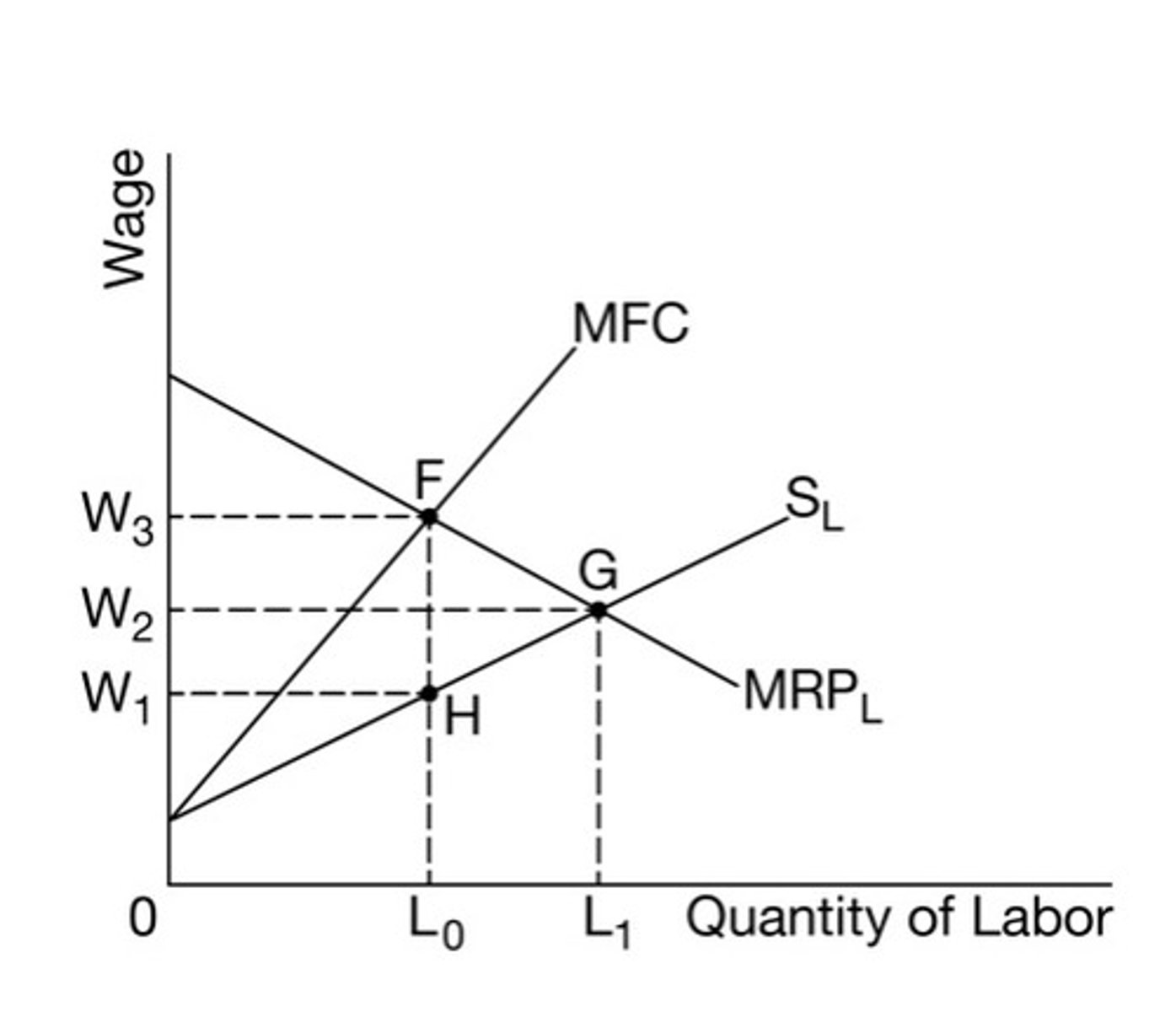

Monopsony

Market with only one buyer

factor markets vs product markets

Factor markets are where the factors of production are sold by households to businesses. Product markets are where goods/services ares old by businesses

four factors of production

land, labor, capital, entrepreneurship

why is the demand for labor downward sloping?

The number of workers that businesses are willing to hire increases as the wage falls.

Why is the supply for labor upward-sloping?

The number of workers that are willing and able to sell their labor increases as the wage increases

unemployment

caused by binding minimum wage

shifters of labor demand

1. Change in the demand for the product

2. Change in the productivity of the resource

3. Change in the price of related resources (substitute

and complementary resources)

Marginal Revenue Product (MRP)

The extra revenue generated when an additional worker is hired

Firms will hire workers up until MRP = wage

Marginal Resource Cost (MRC)

The additional money a worker adds to the total cost of production also known as marginal factor cost (MFC)

Least cost rule formula

MPx/Px = MPy/Py

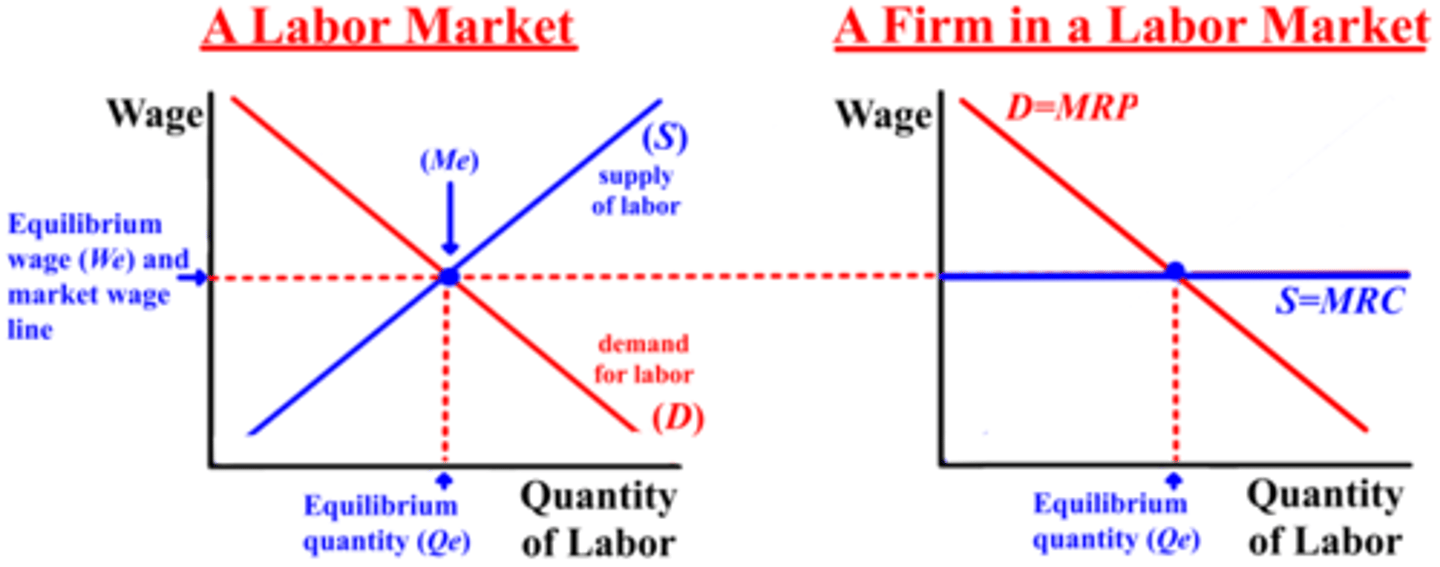

Competitive labor market and firm

Monopsonistic market graph

least cost rule

Always buy more what gives you more MP per dollar

other names for MP

MPP

MPL

MPPL

another name for MRP

Value marginal product (VMP)

MRC

wage

MRP>MRC

keep hiring