ACCT 5001 EXAM 2 - Rivers

1/137

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

138 Terms

Components of Inventory

1) Raw Materials - Inputs

2) Work in Process - Production begun but not completed

3) Finished Goods - completed, not yet sold

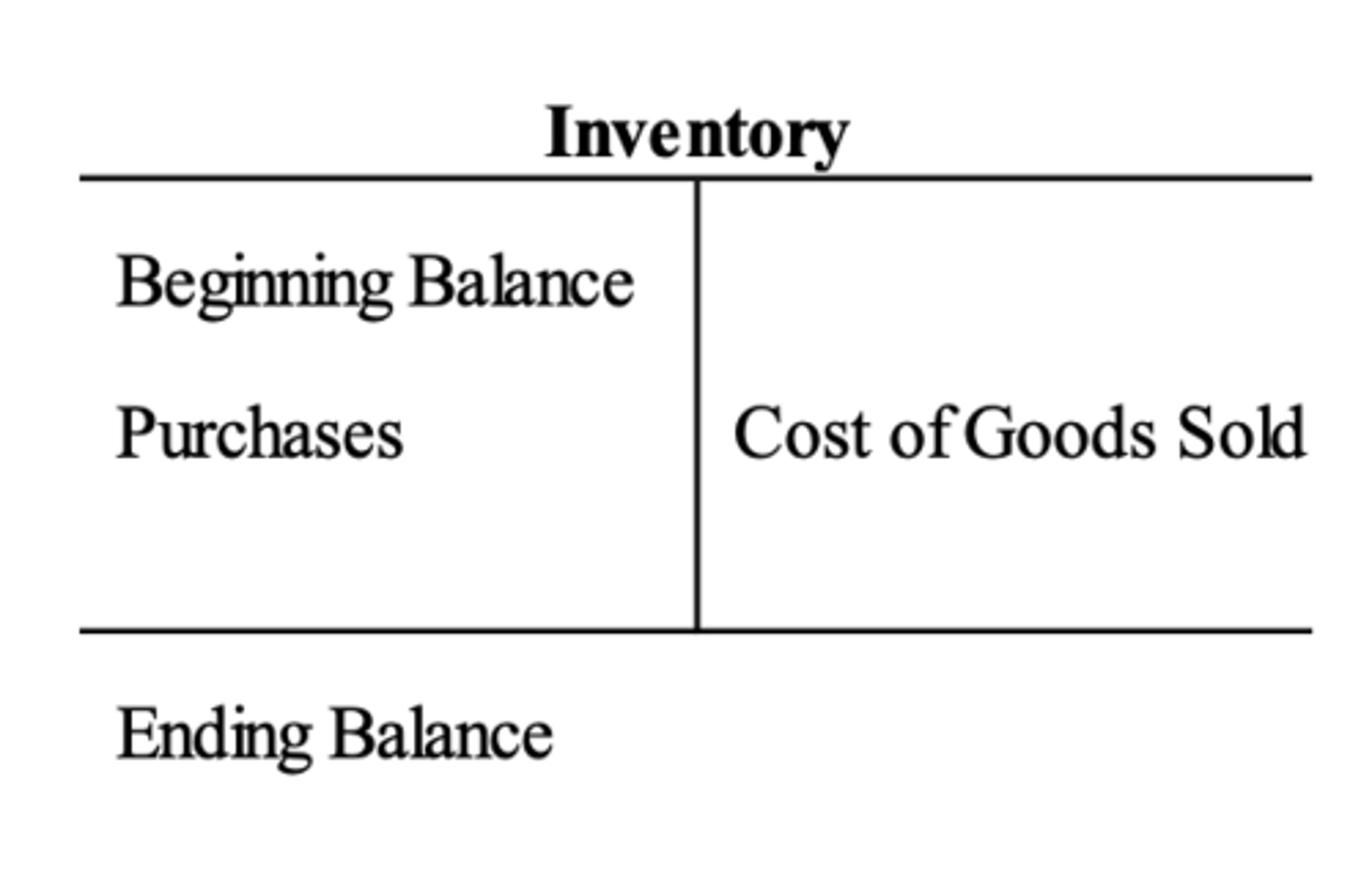

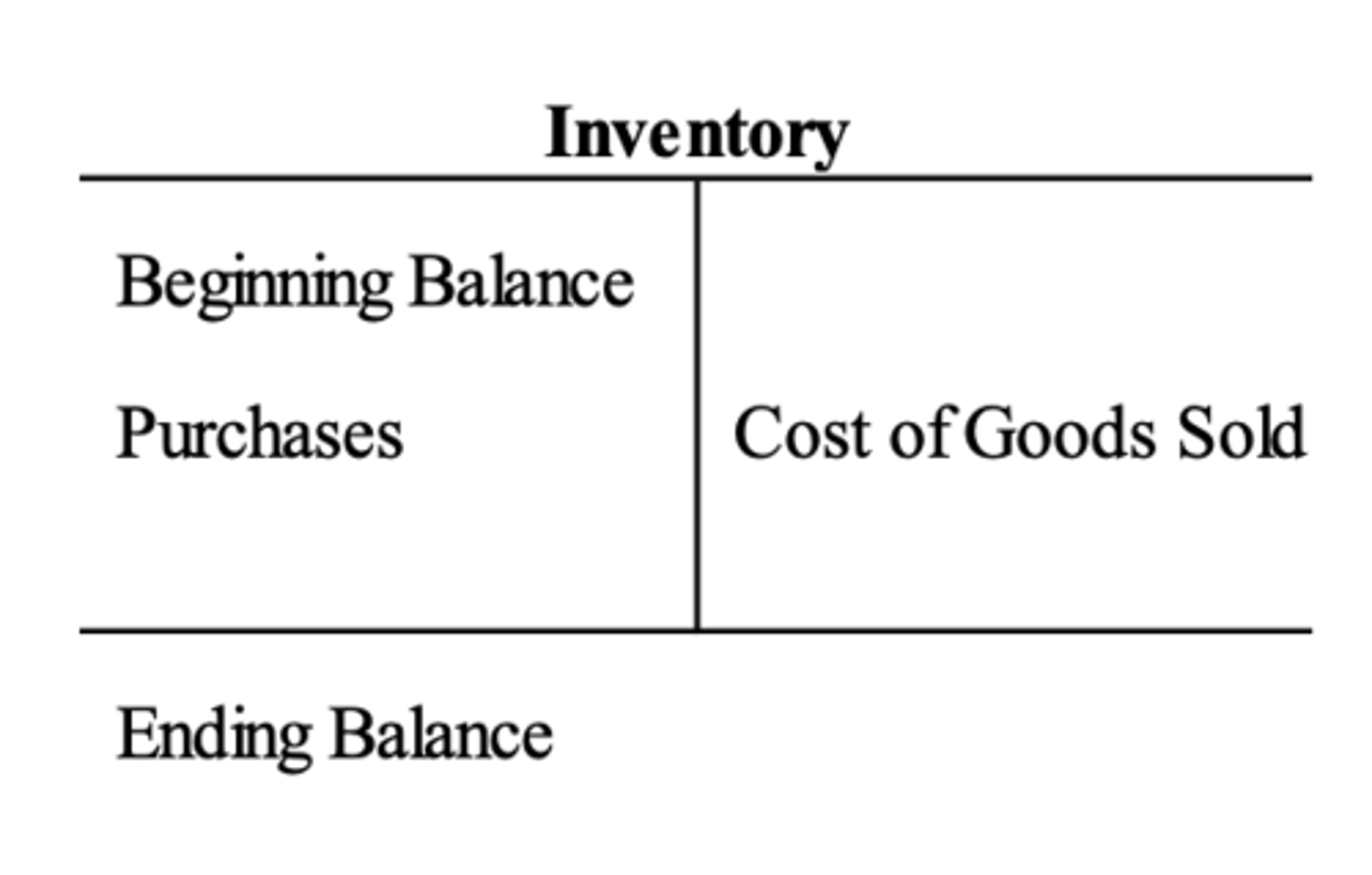

Inventory T-Account

Cost of Services (CGS)

- Cost of goods sold for service companies; includes labor, compensation, travel

- LIFO, FIFO, and WAC methods not applicable

Goods available for sale (GAFS)

Beginning inventory + Purchases

If inventory is sold, ...

The cost of the inventory goes to the income statement as cost of goods sold

If the inventory is not sold, ...

The cost of the inventory stays on the balance sheet in ending inventory

FIFO

First in, First Out

- Assumes oldest items are sold first; newest items in EI

- Ex: Grocery Stores

LIFO

Last in, First Out

- Assumes newest items are sold first; oldest items in EI

- Only allowed in the US; not allowed under IFRS

Weighted Average Cost

Determines an average cost of all items using the formula:

Tot. $ Cost of Units (Beg+Purch) / Total # of Units

Specific ID

Specifically Identifying every unit of inventory; only practical for low volume/high cost items (i.e., jewelry)

T/F: Inventory cost flows have to follow physical flow of goods

False - They do not; they are heavily influenced by accounting assumptions

Effects of FIFO

1) Lower COGS b/c older items are generally less expensive

2) Higher Net Income

3) Higher Ending Inventory

4) Higher Taxes

Effects of LIFO

1) Higher COGS b/c newer items are generally more expensive

2) Lower Net Income

3) Lower Ending Inventory

4) Lower Taxes due to higher expenses/lower NI

Effects of Avg. Cost

Somewhere in the middle of FIFO & LIFO

Inflation and Inventory Costing

1) When using FIFO, the income statement reflects cheaper prices

2) Using LIFO creates layers of unsold inventory; the income statement reflects higher prices

Incentives w/ LIFO

1) Tax savings

2) Industry standard

Issues w/ LIFO

1) Maintenance of Inventory Layers

2) Increased Costs

3) LIFO Liquidation and creation of LIFO Reserve

LIFO Liquidation

The result of selling more units than are purchased during the period, which can have negative tax consequences if a company is using LIFO.

- Results in a reduction in COGS and an increase in NI ("Phantom Profits")

LIFO Layers

Over the years, companies build up "layers" of inventory valued on at different amounts due to inflation

LIFO Reserve

Difference between EI computed using FIFO (reflecting current replacement costs) and LIFO EI

T/F: Whether a company uses LIFO or FIFO affects the Statement of Cash Flows.

False: The choice of using one versus the other has no effect on the Statement of Cash Flows. It does however affect the balance sheet and the income statement.

Inventory Turnover

COGS/Avg. Inventory

- Signal of efficiency; Higher Inv. Turnover signals that the company is selling stock quickly; Lower Inv. Turnover signals that capital is being tied up in inventory or the company has weak sales

Days in Inventory

365/Inventory turnover

- FIFO numbers are usually lower for both ratios

Inventory Valuation: Lower of Cost or NRV

If NRV < Cost, the inventory is considered impaired; an "impairment loss" is recorded on the income statement

- This may occur due to obsolescence, price-level changes, or damage to the goods

Net Realizable Value

Selling price of the product in ordinary course of business (less) reasonably predicted costs of completion, disposal, and transportation

- The "net" amount a company expects to realize from the sale of inventory

Which valuation is used for LIFO, FIFO, & AC?

1) FIFO, Avg. Cost, and Specific ID are valued at Lower of Cost or NRV

2) LIFO inventories are valued at Lower of Cost or Market

Why invest in Short Term Investments (T-Bills, Commercial Paper, CDs)?

1) Generate short term gain

2) Financial Flexibility/Liquidity

Why invest in Debt Investments?

1) Fixed Income

2) Considered Safer

Investments in Other Companies

1) Influence their decisions (i.e., investing in a supplier)

2) Control their decisions

3) Quick Growth

4) Foothold in new market, industry, geographic location

5) Acquire particular expertise/skill/product

6) Eliminate competition

Debt Securities

Investments in the debt of others (another company or government)

- Classification of securities is driven by the intent of the owner

Debt - Trading Securities

1) Fair Value - Net Income

2) Unrealized holding gains/losses recognized in net income

3) Other income effects include interest when earned; gains/losses from sale

Debt - Available for Sale Securities

1) Fair Value - Other Comprehensive Income

2) Unrealized holding gains/losses recognized in OCI

3) Other income effects include interest when earned; gains/losses from sale

Debt - Held to Maturity Securities

1) Amortized Cost

2) Unrealized gains or losses not recognized

3) Other income effects include interest when earned; gains/losses if sold or redeemed early

Equity Securities

Investments in the equity of others (buying stock in another company)

- The way in which we account for equity investments depends on influence and intent

Equity - Fair Value Method

1) Insignificant Influence

2) Holdings <20% (No differentiation between Trading/AFS)

3) Unrealized gains/losses recognized in Net Income

4) Other Income Effects: Dividends declared, gains/losses from sale

5) Invest cash because they think the value of the security will increase, or to hedge risk

Equity - Equity Method

1) Significant Influence (Holdings between 20% - 50%)

2) Unrealized gains/losses not recognized

3) Other Income Effects: proportionate share of investee's net income, reduced by dividends declared

4) Influence the operations of another company

Equity - Consolidation

1) Controlling Influence (>50% Holdings)

2) Unrealized gains/losses not recognized

3) Income entirely consolidated

4) Gain control of another company

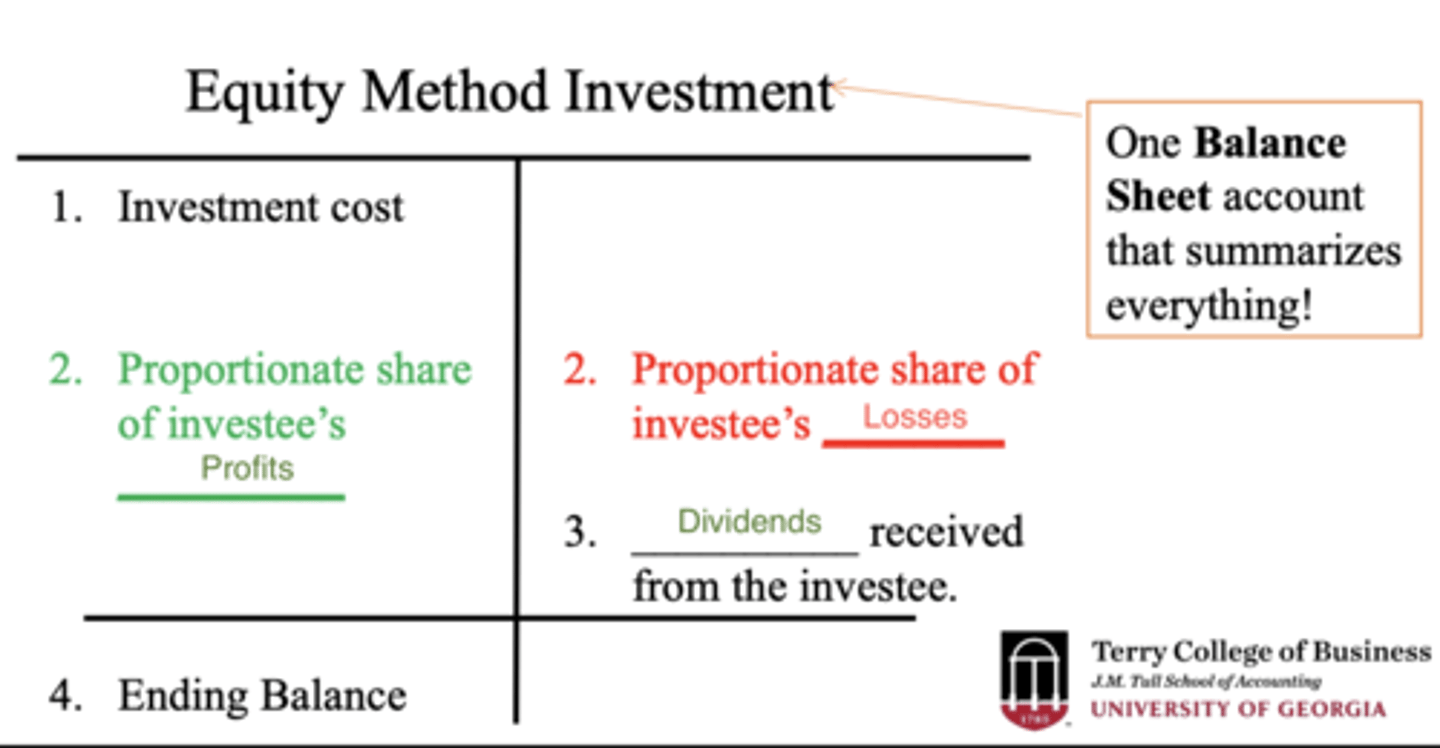

Equity Method Accounting

- Investor reports its initial investment in an account on the B/S called "Equity Method Investment"

- The investment is not marked to fair value on subsequent balance sheets

- Instead a proportionate share of investee's income and dividends recorded in financial statements

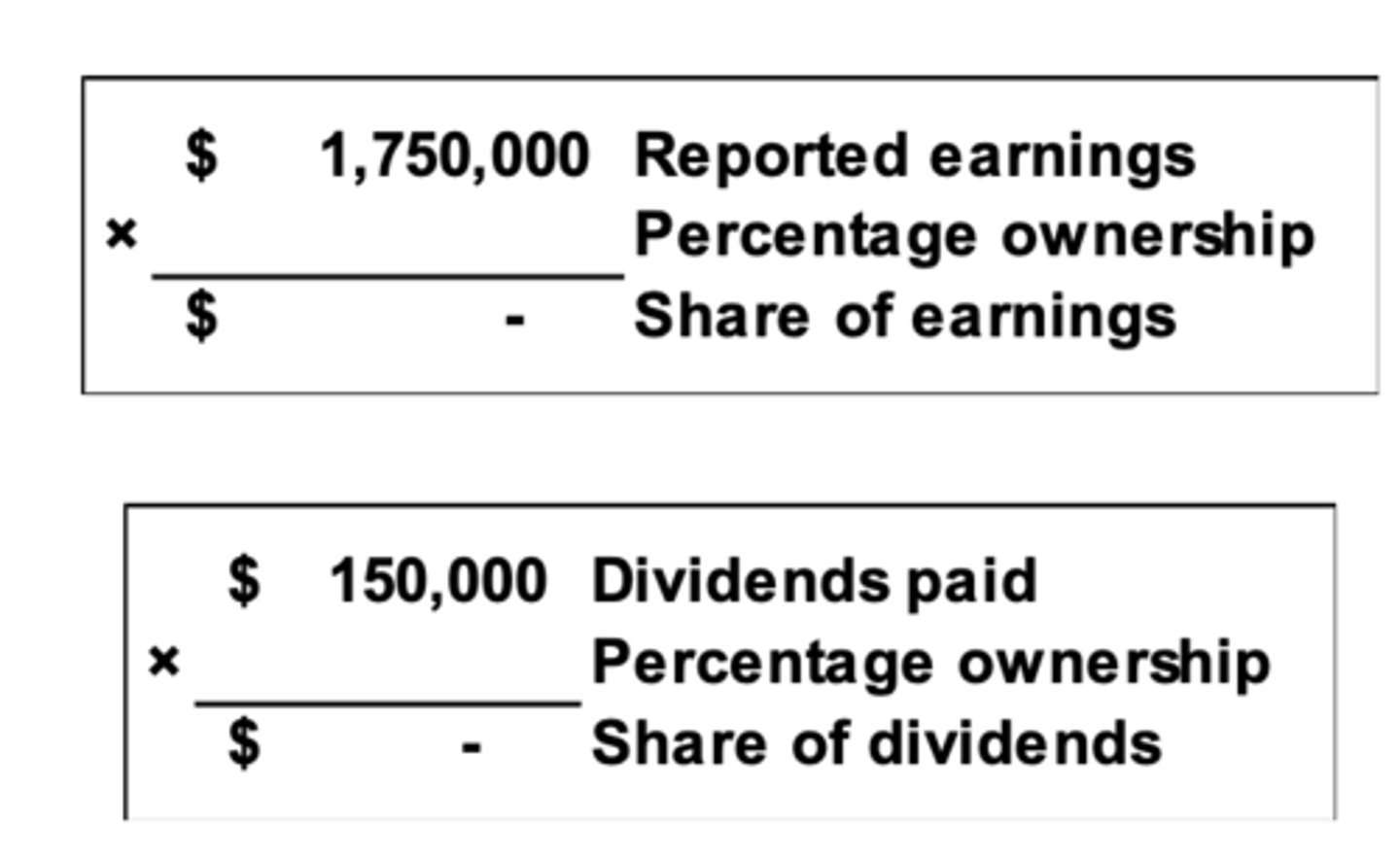

Calculating Share of Earnings for Equity Method

Consolidation Method

1) Financial statements of the investor company and investee are combined as if they are one single company

2) Portion not owned by the parent is reflected as non-controlling interest on the B/S

Consolidation - Balance Sheet

Report ALL assets and liabilities of subsidiaries owned more than 50%

- A non controlling interest EQUITY item represents the percentage of net assets and liabilities not owned by the parent company

Consolidation - Income Statement

Report ALL revenues and expenses of subsidiaries owned <50%

- A non controlling interest income item represents the percentage of subsidiary not owned by the parent company

Non-Depreciable Assets

Land; does not depreciate over time; no limited useful life

Depreciable Assets

PP&E; depreciates over time and has a limited life

- Allocate cost of the asset over its useful life

- Tangible Assets are capitalized (asset is created) and then expensed over time (benefit period) which is an example of an adjusting entry related to a deferral

Residual/Salvage Value

the amount the company expects to receive from selling the assets at the end of its service life.

Acquisition Costs of Fixed Assets

1) Land = Purchase Price + commissions, taxes + land prep. costs + title fees + legal fees - proceeds from salvage

2) Land Improvements = Costs of improving the land for use

3) Buildings = Construction costs + Financing costs (interest) + permits + closing costs + commissions + remodeling

4) Equipment = Purchase Price + freight-in + insurance in-transit + title fees + installation (training) + testing + sales tax

If the costs incurred achieve greater future benefits, ...

Capitalize

If the costs are incurred to maintain a given level of service, ...

Expense

Straight Line Depreciation

(Cost of Asset - Salvage Value) / # of Years of Useful Life

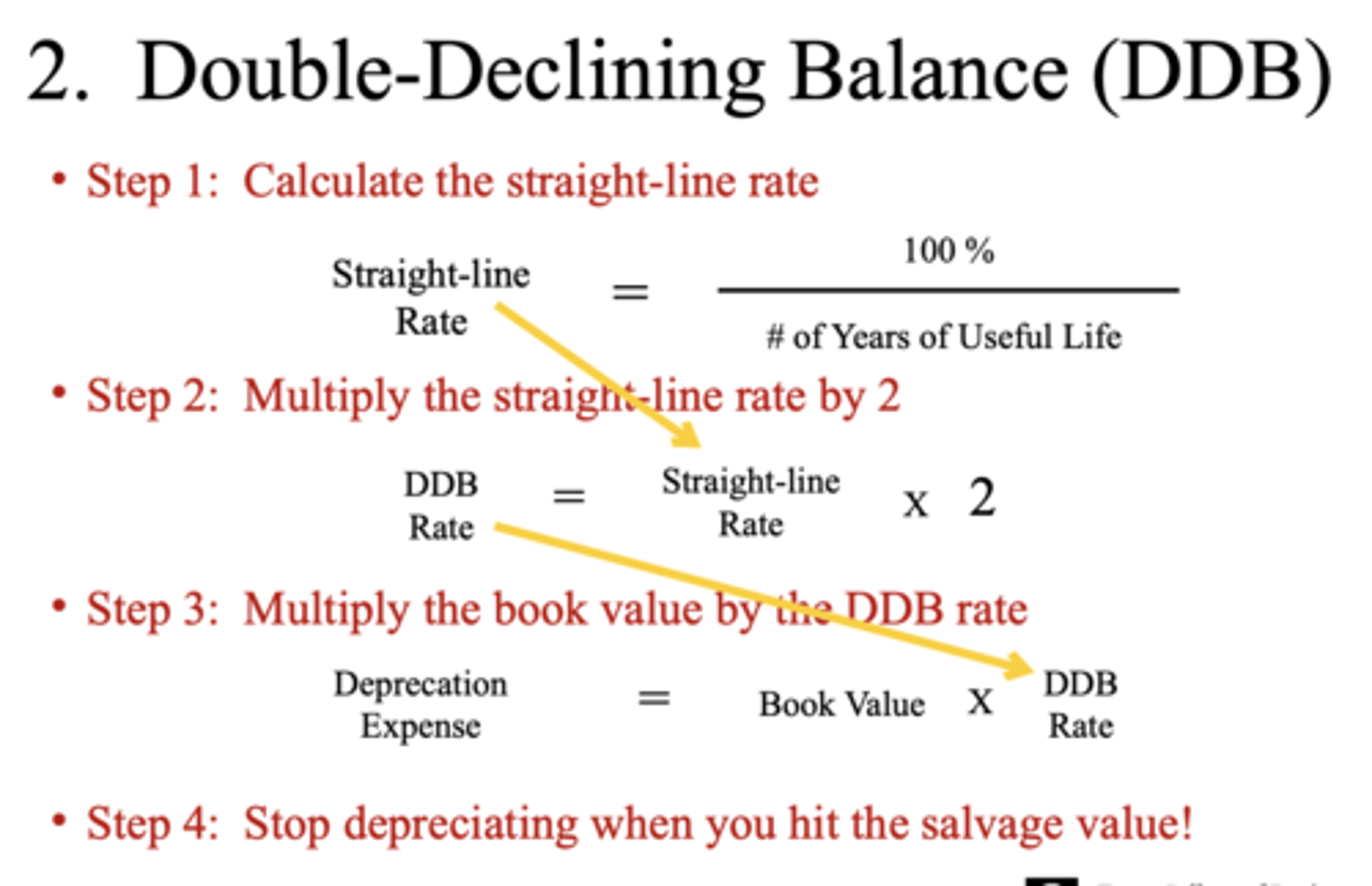

Double-Declining Balance

1. Calculate Straight-line rate

2. Multiply SL rate by 2

3. Multiply book value by the DDB rate

4. Stop depreciating when you hit the salvage value

Units of Production

[(Cost of Asset - Salvage Value) / Total # of Units in Asset Life] x # of Units Produced in the Year

Tangible Asset Impairment

1. Compute Book Value of the asset

2. Estimate un-discounted sum of future cash flows the asset is expected to generate

3. If sum of the cash flows > the BV, do nothing. The asset is not impaired

4. If sum of the cash flows < the BV, the asset is impaired and we must write down the asset to its Fair Value

Intangible Assets

Lack physical substance (but are not financial instruments); provide future economic benefit (generate revenue)

Examples of Intangibles

1) Rights

2) Information

3) Relationships

4) People

When to recognize intangibles?

Generally, internally-generated intangibles are off the balance sheet; purchased intangibles are on the balance sheet

Internally Developed Intangible Assets

- Expensed immediately [R&D expense, advertising expense, SG&A expense (employee training), wage expense (hiring knowledgable employees), stock based compensation (paying employee with options or restricted stock)]

Purchased Intangibles

- Capitalized as an asset

- Purchased patents, trademarks, customer lists, and goodwill

- Recorded at cost (include all costs necessary to make the intangible asset ready for its intended use)

- May be subject to amortization

Patent

Right to use, make, and sell a product (Legal life of 20 years)

Copyright

Right to reproduce and sell a published work (Legal Life equal to life of the creator + 70 years)

Franchise

Right to do business in a certain geographic area (Legal Life as defined by the contract, may include renewals)

Trademark

Right to display a word, slogan symbol, or emblem that distinctively identifies a company, product, or service (Legal Life of 10 years, can easily be renewed for an indefinite number of 10 year periods)

Goodwill

Occurs when one company buys another company; difference between the purchase price and the FMV of net assets (No useful or legal life)

If the useful life of the intangible asset is determinable, ...

You amortize the cost over the lesser of the useful life or legal life

If the useful life is not determinable, ...

You do not amortize the cost, but monitor it for impairment

Intangible Asset Impairment

1. Compute BV of the intangible asset

2. Estimate the undercounted sum of future cash flows the asset is expected to generate

3. If sum of cash flows > book value, do nothing- the asset is not impaired

4. If sum of cash flows < book value, the asset is impaired and write down the asset to its fair value

Calculating Goodwill

Acquisition Price - Fair Market Value of Net Assets Acquired

Note: Net Assets = Assets - Liabilities

Financial Reporting Risk: Balance Sheet Undervalued

- Companies with high (greater) market cap compared to BS-BV

- Example: High growth tech

Financial Reporting Risk: Balance Sheet Overvalued

- Companies with market cap less than BS-BV

Financial Reporting Risk: Inflation Impact

- "Badwill" remains hidden

- Goodwill reported "masked" by inflation or other issues

Commercial Banks

May have better knowledge of a firm but are constrained in the amount of risk they can assume

Non-Bank Financial Institutions and Private Debt

Credit unions, insurance companies, etc supplement banks to provide specific needs. Also, investment bankers may broker private debt placement

Public Debt Markets

Requires that a firm have the size, financial strength, and credibility to bypass the banking sector. Firms issue either commercial paper or bonds

Sellers who provide financing

Suppliers typically extend very short-term financing to buyers but may occasionally grant a loan

Negative Covenants

1) Company receiving the $$ cannot do certain things

2) Prohibition on mergers, additional borrowing, sale of key assets

Positive Covenants

1) Company must do these things

2) Maintain certain financial ratios, provide audited financial statements, use assets as collateral, maintain insurance coverage

Effects of a Debt Covenant to the Lender

- Lower risk

- Lower interest rate

- Protects themselves from borrower default

- Provides an early indication of challenges ahead

Desire for Credit - Borrowers

1) Operating: to cushion cyclical operating needs

2) Investing: to purchase new equipment and property

3) Financing: stock repurchases, debt maturity payments

Source of Debt

1) A/P - lender is seller of product/service

2) N/P - lender is bank/financial institution

3) B/P - lender is investors (Individual/corporation)

Benefits of Debt

- Interest tax shields

- Take advantage of opportunities

Downsides of Debt

- No payment flexibility

- Restrictive covenants

- Foregone investment opportunities

- Potential Default or even worse Bankruptcy

Current Debt

1) A/P, Accrued expenses

2) Notes/Bonds Pay. principal balance due within a year

3) Interest Payable

Long-Term Debt

Notes/Bonds payable principle balance due beyond a year from B/S date

Debt Effects on Cash Flow Statement

1) Cash paid for interest impacts operating activities

2) Cash received from borrowing and paid on principal impacts financing activities

Bond Issued at Par

Coupon interest rate equals market interest rate

Discount Bond

Coupon Interest Rate < Market Interest Rate

- Carrying Value of the bond increases over time

Premium Bond

Coupon Interest Rate > Market Interest Rate

- Carrying value of the bond decreases over time

Total Interest Over Life of Bond

Present Value of Bond - (Sum of Interest PMTS + Principal)

Public Debt Repurchases

Companies can go into the market and buy back their own public debt securities

- Like any investor, the company must repurchase the debt at the current market price

- A realized gain or loss is recognized for the difference between the carrying value of the debt and the cash paid to repurchase the debt (FMV)

- Effectively retires the debt

Debt/Equity Hybrid Securities

debt securities that include an equity option

- For companies: reduces interest costs; convertible securities offer a lower interest rate due to their option

- For investors: Upside potential with lower risk; fixed income now, growth potential later

Short Term Liquidity Risk

the near-term ability to generate cash to service working capital needs and debt service requirements, i.e., will the firm be able to fund operations and pay off suppliers and providers of short-term debt?

Long Term Solvency Risk

the longer-term ability to generate cash internally or from external sources to satisfy plant capacity (capital expenditures) and debt repayment needs

Tax Cuts and Jobs Act (TCJA)

Reduced US corporate rate from 35% to 21%

Goals:

- To prevent shifting of income to lower tax jurisdictions

- To incentivize spending that will boost productivity and lead to wage growth

Impacts:

- Significant savings noted for many companies in 2017 financials compared to prior years

- Lessened repatriation tax on previously deferred foreign income

- Minimum tax on certain foreign earnings

Effective Tax Rate

Total Tax Expense / Pre-Tax Income

- Average rate at which a corporations income is taxed

Note: Total Tax Expense is an Income Statement #

Financial Reporting

For a multinational, there may be a requirement to report to local authorities using IFRS and to report the same results of the same operations to the parent multinational under US GAAP

Goals: predictive value, comparability, faithful representation

- Uses full accrual method

Tax Reporting

Record must be kept of many different jurisdictions - cities, states, countries. Different types of taxes - income, sales, special taxes

Goals: revenue, social welfare, taxpayer behavior

- Uses modified cash basis

Book-Tax Differences: Permanent Differences

- Financial accounting number will never factor into taxes

- Increases or decreases the effective tax rate by decreasing or increasing pre-tax financial income subject to tax

Book-Tax Differences: Temporary Differences

- Timing difference between when the number hits the financial statement versus the tax return

- Creates deferred tax assets (future tax deductions) & deferred tax liabilities (future tax outlays)

Examples of Permanent Differences

1) Income that is never taxed - (Income from municipal bonds, life insurance proceeds on the death of a key executive, a portion of dividends received from other companies)

2) Expenses that are never deducted for tax purposes - (Expenses related to obtaining tax-exempt income, premiums paid for life insurance policies of key executives, payments and fines due to violations of the law, political contributions)

Examples of Temporary Differences

Arise when tax rules and accounting rules recognize income/expenses in different periods (timing differences between GAAP and IRC)

Deferred Tax Assets

- A deferred tax asset appears on the balance sheet.

- It arises when a company pays more in income taxes than what is reported as tax expense in the financial statements.

- This happens when taxable income is higher than accounting profit.

- As a result, income tax payable > tax expense.

- The company expects to recover this difference in the future, when tax expense will exceed what it actually pays.