4.2.4.2 - Commercial banks & Investment banks

1/21

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

22 Terms

Functions of Commercial Banks

Primary Functions:

Accepting deposits

Lending

Providing efficient means of payment (facilitating transfer of funds)

Credit Creation - by using deposits to make new loans, commercial banks create credit and increase the money supply in the economy

Secondary Functions:

Providing financial advice

Providing foreign exchange

Functions of Investment Banks

Ensures the availability of capital for firms, governments & other entities

Prop Trading

Market Making

M&A

New Issues

UK Big Four Banks

HSBC

Barclays

Lloyds

NatWest

Balance Sheet =

Summary of assets & liabilites of a business

Asset =

What an individual/household/firm owns

Liability =

What an individual/household/firm owes

Commercial Bank’s Assets ranked by liquidity

Most Liquid

Cash

Balances at the Bank of England - cash reserves held at central bank - instantly accessible

Treasury Bills

Government Bonds

Investments

Advances - short-term lending (e.g. overdrafts) - repayable on demand, but can’t easily be sold on markets

Loans - long-term lending - repaid on fixed date, can’t easily be sold on markets

Fixed Assets

Least Liquid

Commercial Bank’s Liabilities

Customer Deposits (current accounts, savings accounts) - money owed back to customers

Borrowings from other banks

Share Capital - money raised by issuing shares

Capital Reserves (retained profit)

Bonds & debt securities Issued - owes interest & principal repayment

If a bank makes a new loan to a customer, what happens to the bank’s liabilities & assets?

Bank’s Liabilities INCREASE

Banks Assets INCREASE

Money Supply INCREASES

This is because transactions typically create both an asset & liability.

The loan acts as an asset because it is an agreement of repayment w/ interest by the borrower

Also a liability because the bank owes that money to the customer’s deposit account

Why is having more capital on a bank’s balance sheet safer?

Having more capital means the bank can absorb more losses on its assets

If the bank’s assets falls by more than its capital, it will be bankrupt.

Objectives of a Commercial Bank

Liquidity

Profitability

Security

Conflict between objectives of Profitability & Liquidity

Liquid assets generally yield a lower rate of return than more illiquid ones.

Banks therefore want to make profits by seeking investment opportunities & lending money out rather than holding cash that is not generating any returns.

However, banks have a need for liquidity as they must hold enough cash/liquid assets to meet the daily requirements of customers to make withdrawals.

Conflict between objectives of Profitability & Security

Banks may seek more risky investment opportunities & unsecured loans for higher returns, but this threatens the security & stability of the banks.

How do commercial banks make profit?

By charging higher interest rates on loans than what it pays on deposits

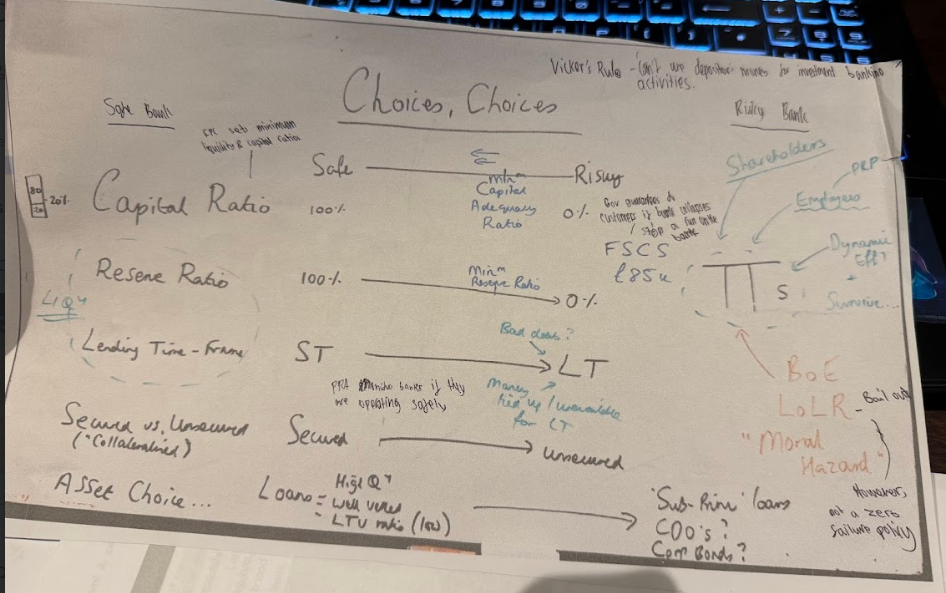

Vickers Rule

UK banks legally have to separate their retail deposit-taking businesses from investment banking operations.

i.e. can’t use depositors’ money for investment banking activities

Improves financial stability

‘Run on the Bank’ =

When a large number of customers simultaneously withdraw their deposits due to fears that the bank is, or is about to become, insolvent

Financial Services Compensation Scheme (FSCS)

Government guarantee to customers that if a bank fails, it covers up to £120,000 per person per firm.

Protects consumers’ deposits, maintaining confidence so reduces chance of a ‘run on the bank’

Bank of England ‘Lender of Last Resort’

BoE provides emergency liquidity to banks during crises, effectively bailing them out.

Prevents bank failures

However, moral hazard means banks may take advantage of this by taking risks knowing they will be bailed out if they fail.

Therefore, BoE employs a ‘not a zero failure’ policy, allowing some banks to fail if they do not affect the larger financial system.

Safe vs Risky Bank Summary Diagram

How banks create credit

*

Shadow Banking Sector =

= Financial intermediaries that provide credit (lend), but are not subject to regulatory oversight

Adds systemic risk as it is unregulated, so involves higher risk such as excessive leverage, inadequate liquidity.

Examples of Shadow Banking Entities

Hedge Funds

Private Equity Firms

Loan Sharks