ap microeconomics

1/80

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

81 Terms

scarcity

the inability of limited resources to satisfy unlimited wants

unlimited resources

land, labor, entrepreneurship, capital

what are the two main types of economies?

market economy and command economy

market economy

use prices to distribute resources, goods, and services

command economy

government controls allocation of resources, goods, and services

opportunity cost

value of the best alternative NOT chosen

production possibility curve

inside production possibilites curve

all resources are not being used

outside production possibilities curve

impossible

along the curve

closer to the top- more of good y than good x

closer to bottom- more of good x than good y

linear ppc

constant opportunity cost

curved ppc

increasing opportunity cost

determinants of ppc

changes in resources, technology, productivity, and trade

absolute advantage

a is better than b because a>b

comparative advantage

ability to produce at lower oppurtunity cost

output (goods produced) - other over

input (resources used) - it over

mutually beneficial terms of trade

between the two opportunity costs for a calculated comparative advantage

marginal analysis

analyzing how much benefit selling or buying a certain good provides compared to its cost

benefit maximizing behavior

where the marginal cost is less than or equal to the marginal benefit

calculating marginal utility

the marginal utility (in utils) divided by the cost = MU/$

diminishing marginal utility

as more units of a product are consumed, the satisfaction/utility it provides tends to decline

law of demand

consumers buy less at high prices and more at low prices

demand curve

downward

demand curve moves right

increase

demand curve moves left

decrease

demand shifters

taste and preference

market size

expectations

price of related goods

- substitutes - $ of good up, demand for sub up

- complements - $ of good up, demand for comp down

changes in income

- normal goods - $ up, demand up

- inferirior goods - $ up, demand down

law of supply

producers sell more at high prices and less at low prices

demand curve

upwards

supply shifters

resource costs

government - taxes, subsidies

# of sellers

technology

price of other goods

producer expectations

price elasticity of demand

inelastic - demand changes little with price changes (more vertical)

elastic - demand changes with price changes (more horizontal)

price elasticity of demand/ supply equation

demand - %∆Qd/%∆P

supply - %∆Qs/%∆P

elastic

goods affected by change in price, more horizontal

inelastic

goods not affected by change in price, more vertical

total revenue test

a method to determine the price elasticity of demand

total revenue increases when price falls, demand is elastic

total revenue decreases, demand is inelastic

characteristics of elastic supply

easy production, low cost, easy to switch to, low barriers to entry

characteristics of inelastic supply

difficult production, high costs, hard to change to alternative, high barriers to entry

characteristics of elastic demand

sensitive to price change, substitutes, luxury items, large portion of income, not needed immediately

characteristics of inelastic demand

few substitutes, required now, small portion of income

price elasticity of demand/ supply meaning

relatively elastic: >1

unit elastic: 1

relatively inelastic: <1

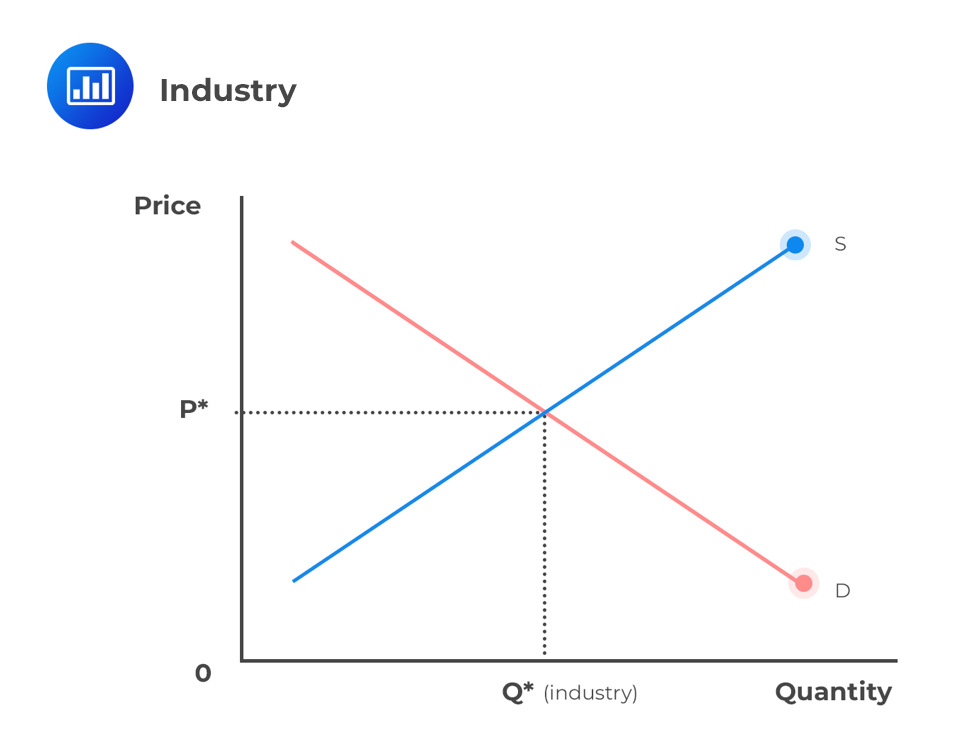

market equilibrium

Qs = Qd

price below the equilibrium is shortage

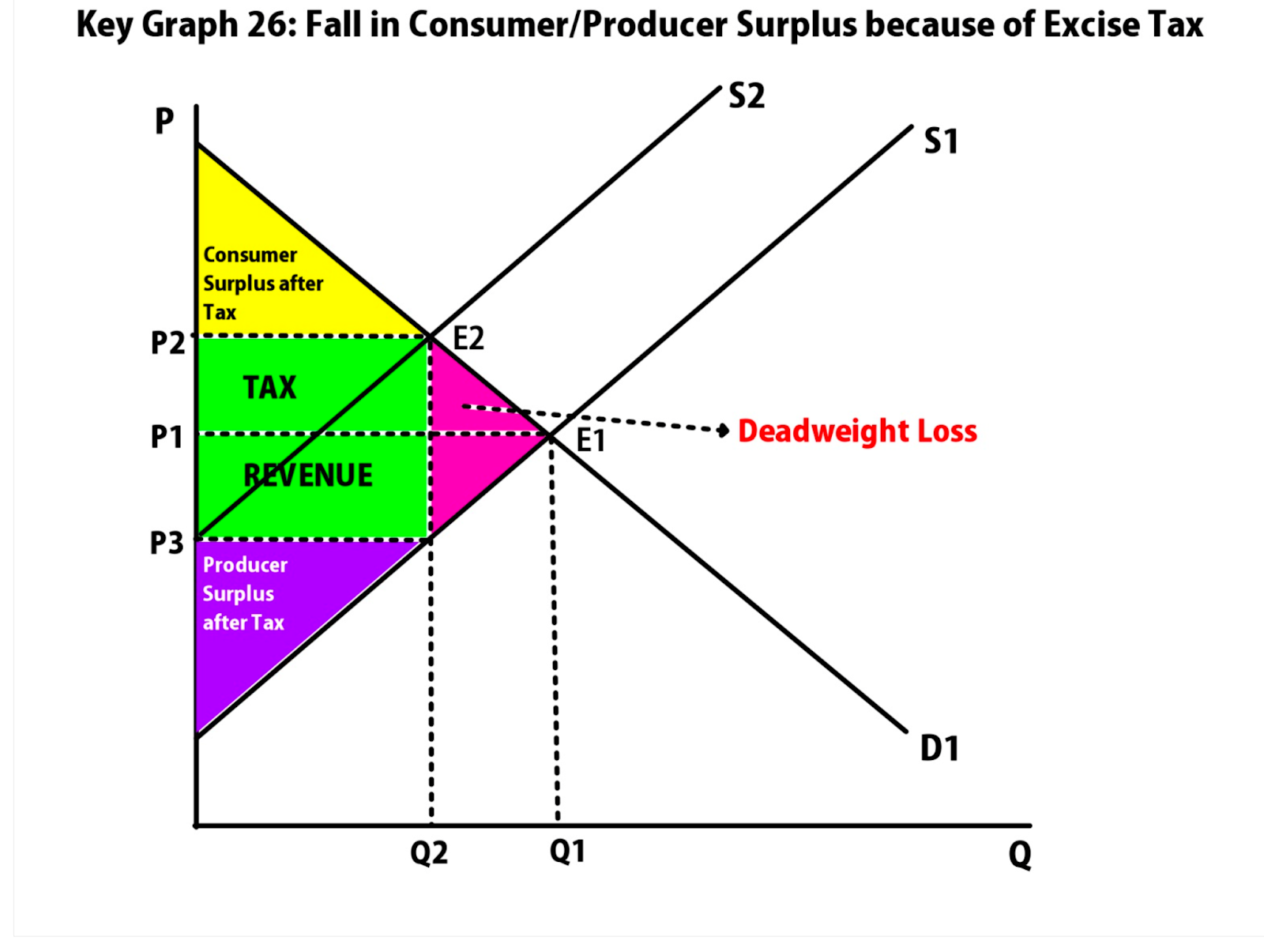

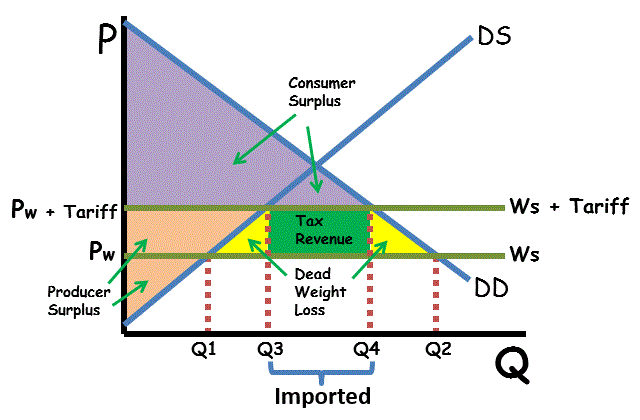

consumer surplus

price consumers are willing to pay - actual price

producer surplus

actual price -price the producer is willing to sell for

demand increase

price and quantity increase

demand decrease

price and quantity decrease

supply increase

price decreases, quantity increases

supply decrease

price increases, quantity decreases

deadweight loss

transactions that should occur, but don’t because of government intervention

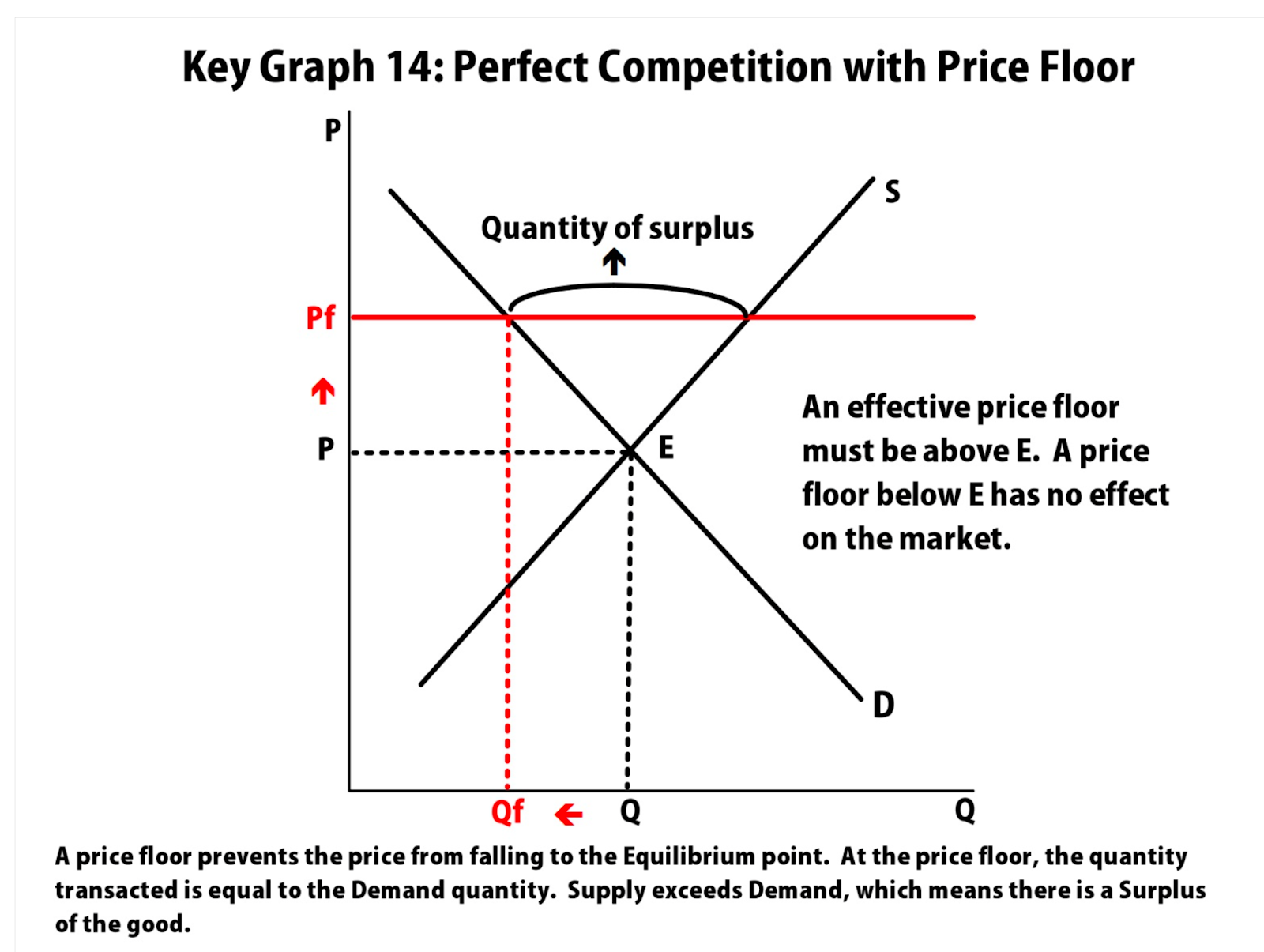

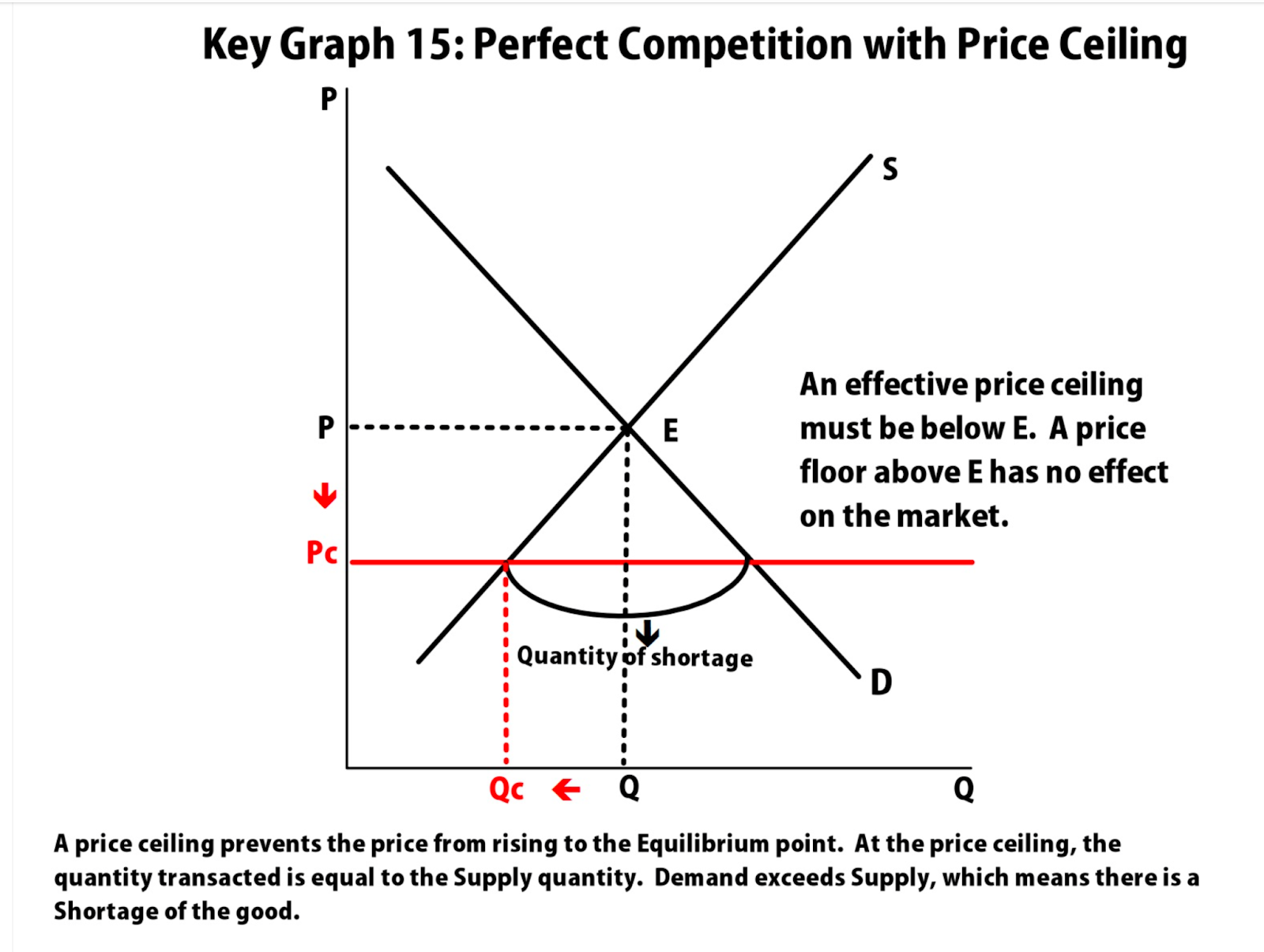

market disequilibrium

shortage : Qs < Qd, price is lower than equilibrium

surplus : Qs > Qd, price is above equilibrium

price floor

minimum price a supplier can charge

price is set above equilibrium (causes shortage)

price ceiling

maximum price a supplier can charge

price is set below equilibrium (causes surplus)

demand price

the price at which consumers will demand that quantity

supply price

the price at which producers will supply that quantity

quota rent

difference between demand price and supply price

tariffs

tax placed on a good that is imported or exported

production function

relation between the quantity of inputs a firm uses and the quantity of output it produces

fixed input

an input whose quantity doesn’t change

variable input

an input whose quantity can change

long run : time period in which all inputs can be variable

short run : time period in which at least 1 input is fixed

marginal product of labor

the extra output generated by employing one additional unit of labor, while keeping all other inputs constant

change in output/ change in labor

∆Q/∆L

production function

shows the relationship between the amount of labor and amount of output

law of diminishing marginal returns

increasing, decreasing, negatives

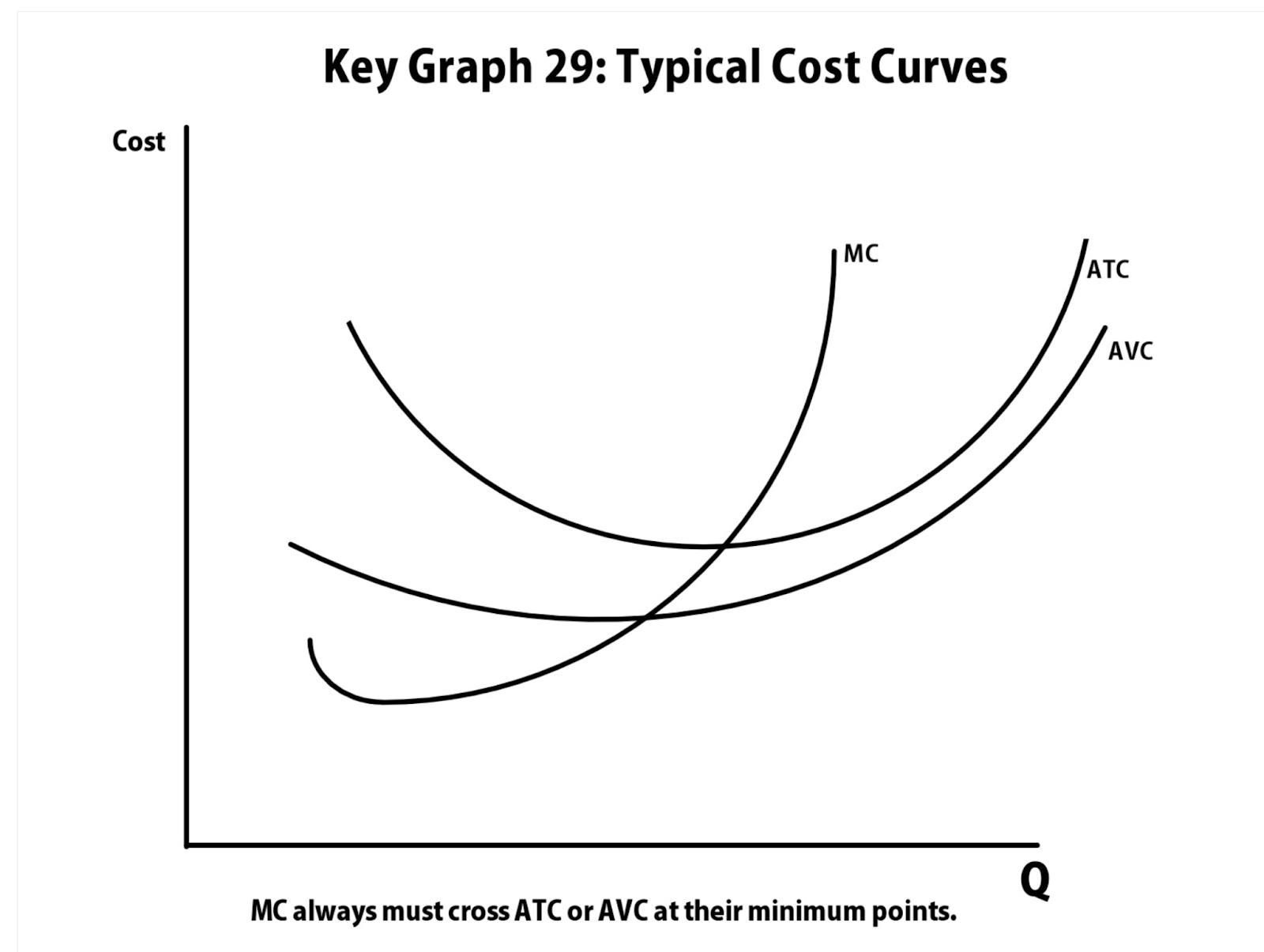

marginal cost of labor

wage / marginal production eq

W / (Q/L)

marginal cost vs marginal production

flipped graphs and inverse relationship

fixed cost

doesn’t change with out put (ex 1 muffin in an oven vs 20 muffins)

variable cost

cost that varies with output (ex labor)

total costs

variable + fixed

average fixed cost (AFC)

average variable cost (AVC)

average total cost (ATC)

FC / Q

VC / Q

AC / Q

change in fixed cost?

moves average variable cost curve only

change in variable cost?

moves all three curves

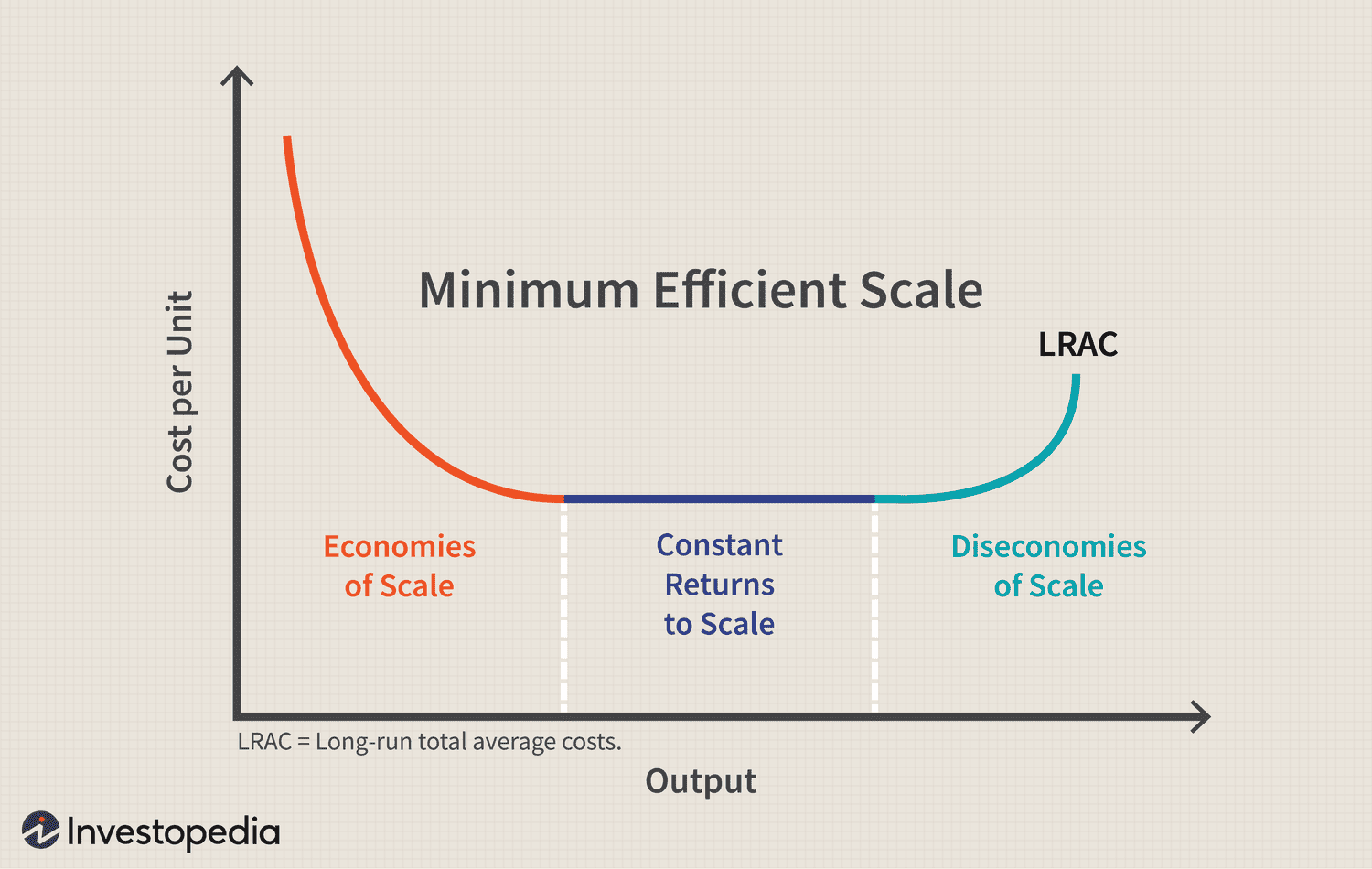

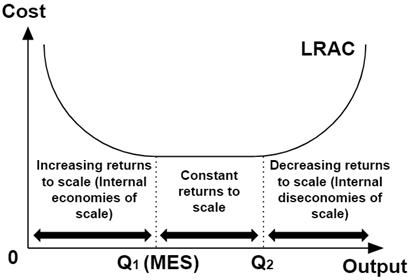

minimum effiency scale

the point at which a firm can produce its products for the lowest constant cost

accounting profit

revenue - explicit cost

long run average total cost

the average total cost of production when all inputs can be varied, allowing firms to achieve economies of scale

accounting profit

total revenue (price times quantity) - explicit costs

economic profit

total revenue (price times quantity) - explicit costs - implicit costs

normal profit

economic profit is zero

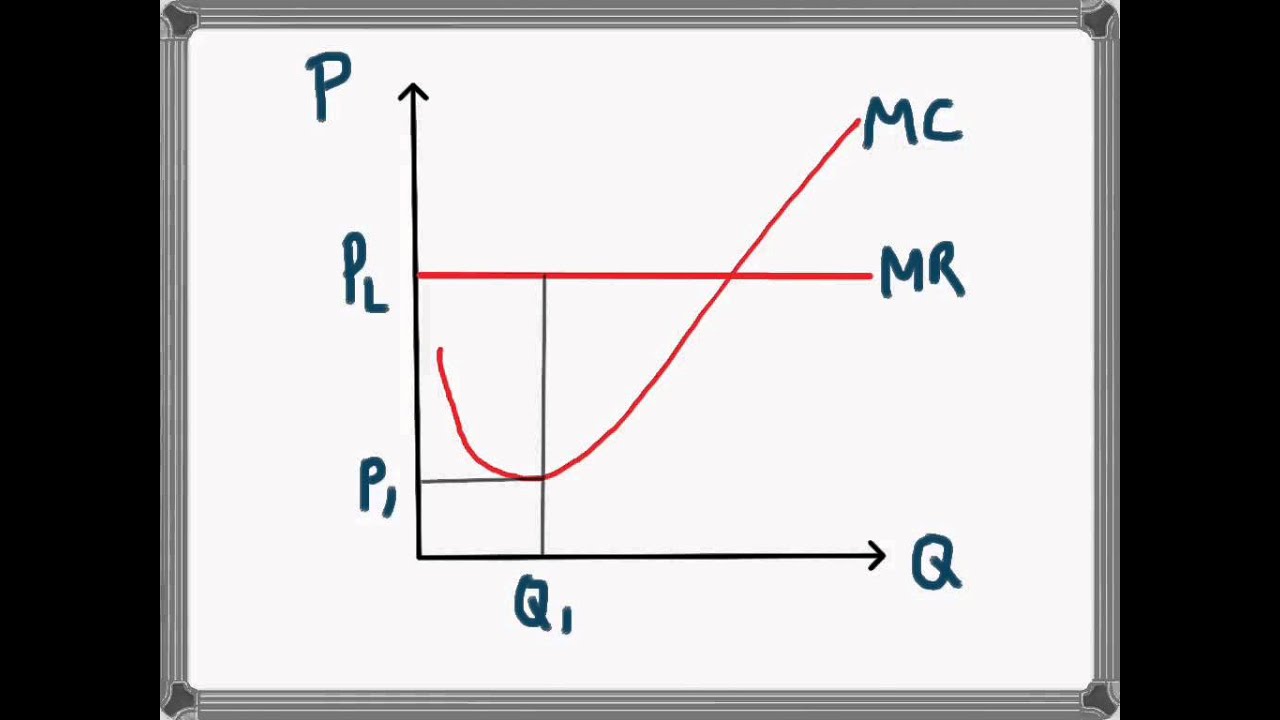

marginal revenue

TR/Q