Introduction to Economics: Principles, Markets, and Elasticity

1/163

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

164 Terms

Economics

The study of how individuals and societies choose to use the scarce resources that nature and previous generations have provided.

Opportunity Cost

The best alternative that we forgo or give up when we make a choice or a decision.

Marginalism

The process of analyzing the additional or incremental costs or benefits arising from a choice or decision.

Efficient Market

A market in which profit opportunities are eliminated almost instantaneously.

Microeconomics

Examines the function of individual industries and the behavior of individual decision-making units, that is, firms and households.

Macroeconomics

Examines the economic behavior of aggregates such as income, employment, output, and so on - on a national scale.

Positive Economics

An approach to economics that seeks to understand behavior and the operation of systems without making judgements. It describes what exists and how it works.

Normative Economics

An approach to economics that analyzes outcomes of economic behavior, evaluates them as good or bad, and may prescribe courses of action.

Normative

Makes recommendations, not based on tested facts, tells you what should be/have been.

Positive

Connects cause and effects, based on tested facts, tells you what is/was.

Thinking Like an Economist

Economists try to address their subject with a scientist's objectivity, devising theories, collecting data, and analyzing these data to verify or refute their theories.

Scientific Method

A method of inquiry used in developing and testing theories about how the world works.

Observation, Theory, and More Observation

A process in economics where experiments are often difficult, and economists use whatever data the world provides.

Assumptions

Basic premises that economists use to build their theories and models.

Economic Models

Simplified representations of complex economic processes used to analyze and predict economic behavior.

Natural Experiments

Historical events that provide opportunities to study the effects of key natural resources on the world's economies.

Assumptions in Economics

Economists make assumptions to simplify the complex world and make it easier to understand.

Ceteris Paribus

Device used to analyze the relationship between two variables while the values of other variables are held unchanged.

Tradeoffs

To get one thing, you have to give up something else. Making decisions requires trading off one goal against another.

Cost of Something

Decision-makers have to consider both the obvious and implicit costs of their actions.

Marginal Benefit (MB)

The additional benefit received from consuming one more unit of a good or service.

Marginal Cost (MC)

The additional cost incurred from producing one more unit of a good or service.

Rational Decision-Maker

A rational decision-maker takes action if and only if the marginal benefit of the action exceeds the marginal cost.

Incentives

Behavior changes when costs or benefits change.

Trade

Trade allows each person to specialize in the activities he or she does best.

Invisible Hand

Households and firms that interact in market economies ********* they are guided by an 'invisible hand' that leads the market to allocate resources efficiently.

Government Intervention

When a market fails to allocate resources efficiently, the government can change the outcome through public policy.

Standard of Living

A country's standard of living depends on its ability to produce goods and services.

Money Printing

When a government creates large quantities of the nation's money, the value of the money falls, causing prices to increase.

Inflation and Unemployment Tradeoff

Reducing inflation often causes a temporary rise in unemployment.

Economic Activity Organization

The opposite of market organization is economic activity that is organized by a central planner within the government.

Productivity and Income

As a nation's productivity grows, so does its average income.

Market Failures

Examples of market failures include monopolies and pollution.

Time Horizons in Economics

Different assumptions are made when studying the effects of a policy change over different time horizons.

Economic Problems

Economics is concerned with the utilization of scarce resources for production, necessitating the development of an economic system that responds to the needs of its members.

What to Produce?

The economic society must determine consumers' demands through market study and consumer research, considering factors like physical environment, habits, culture, and customs.

How to Produce?

Choosing how to produce goods or services involves considering the availability and cost of resources, allocation of resources, value of output versus inputs, and available technology.

How Much to Produce?

Determination of how much of a product to produce depends on consumer demand and knowledge of people's tastes and desires, which are changeable.

For Whom to Produce?

Society must consider for whom to produce goods and services, weighing whether to prioritize poor consumers or rich individuals.

Market Economy (Capitalism)

Characterized by private property ownership, a pricing process, competition, and a profit motive.

Command Economy (Dictatorship)

The government owns most property resources and major factors of production, conducting and regulating economic activity through central planning.

Socialist Economy (Mixed)

Abandons profit motive for production for use, with central planning determining production goals and resource allocation.

The Role of the Government

Government involvement may improve efficiency and fairness in resource allocation, but poor functioning can lead to corruption and waste.

Mixed Systems, Markets and Governments

All real systems are in some sense 'mixed'.

Scarcity

A fundamental economic problem of having seemingly unlimited human wants in a world of limited resources.

Choice

The act of selecting among alternatives in the face of scarcity.

Interdependence

The reliance of consumers and producers on each other in an economy.

Gains from Trade

The benefits that arise from trading goods and services, allowing for specialization and increased efficiency.

Consumer Research

The process of gathering information about consumer preferences and behaviors to inform production decisions.

Resource Allocation

The distribution of resources among competing uses.

Production Goals

Targets set by a central authority to determine the quantity and type of goods and services to be produced.

Central Planning Authority

An organization that makes decisions about the allocation of resources and production in a command economy.

Profit Motive

The incentive for individuals and businesses to improve their financial well-being through production and trade.

Economic Activity

The production, distribution, and consumption of goods and services in an economy.

Market economies

Economies in which the government plays a major role, involving regulation and income redistribution.

Reasons for Government Involvement

1. Market systems do not always produce what people want at the lowest cost - there are inefficiencies. 2. Rewards (income) may be unfairly distributed and some groups may be left out. 3. Periods of unemployment and inflation recur with some regularity.

Constrained choice

The limitation on choices due to scarcity of resources.

Investment

The process of using resources to produce new capital.

Capital

Resources that can be used to produce goods and services, which do not need to be tangible.

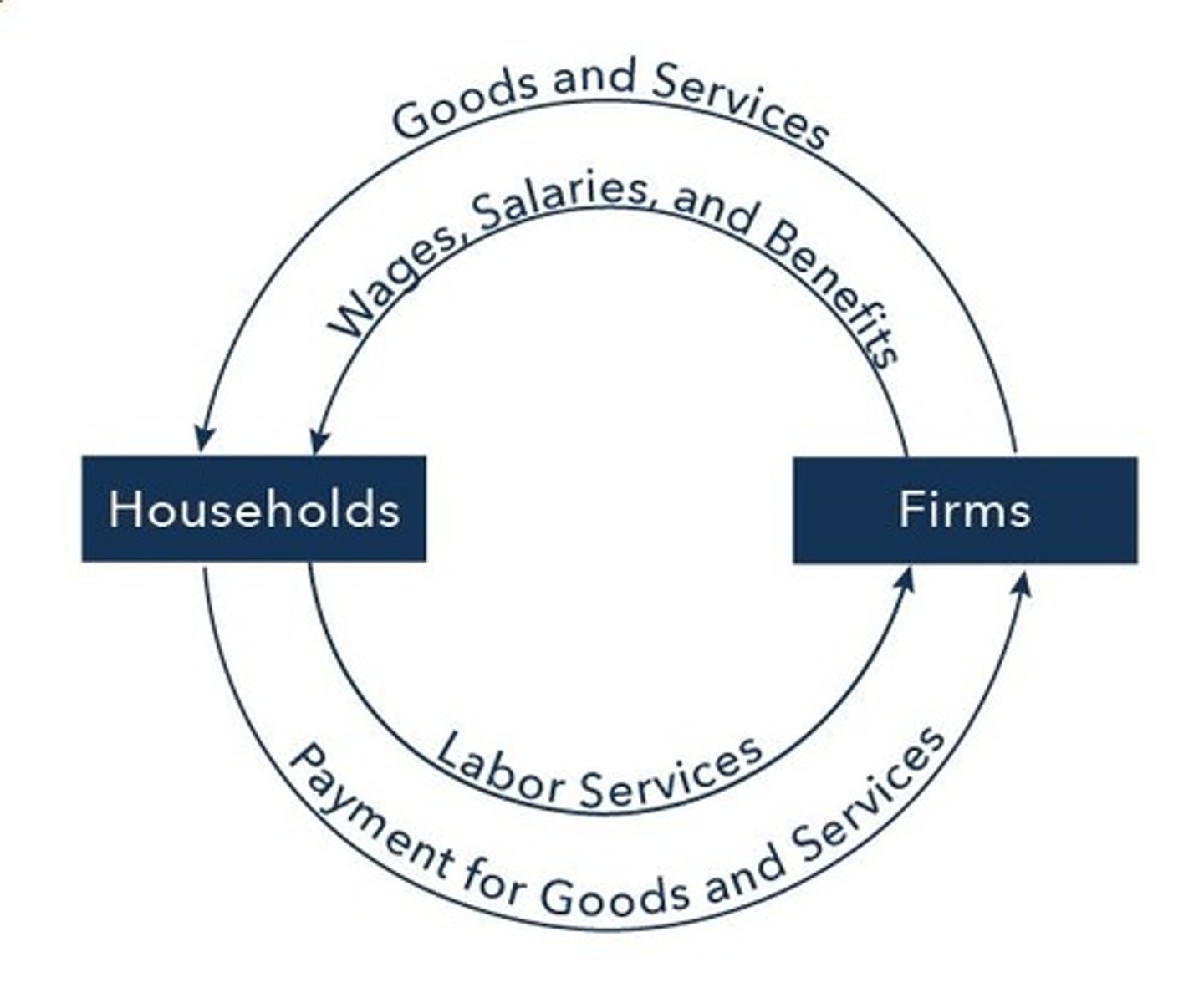

Circular Flow of Economic Activities

The model that illustrates the flow of goods, services, and money in an economy.

Households

The consuming units in an economy.

Entrepreneur

A person who organizes, manages, and assumes the risks of a firm.

Firm

An organization that transforms resources (inputs) into products (outputs).

Market for resources

The market where households supply resources to business firms in exchange for wages, salaries, rent, interest, and profit.

Market for consumer goods and services

The market where households are the buyers and business firms are the sellers of goods and services.

Input markets

Markets where firms demand inputs to produce outputs.

Output markets

Markets where households demand products produced by firms.

Consumption expenditures

The total spending by households on goods and services.

Wages

Payments made to labor for their work.

Rent

Payments made for the use of land or property.

Interest

Payments made for the use of borrowed money.

Profit

The financial gain obtained when revenue exceeds costs.

DEMAND

The amount of various quantities of goods and services which buyers are willing and able to purchase at a given price, time and place, ceteris paribus.

Demand Schedule

A listing of the different quantities of goods and services that buyers will purchase given the various alternative prices.

Market Demand

The total demand obtained by taking the horizontal summation of all individual demand of the consumers in the market.

Demand Curve

A plotted demand schedule.

Movement Along Demand Curve

The change in the quantity demanded due to the changes in the price of the product when all other factors are held constant.

Change in Demand

The shift in the entire demand schedule due to the changes in some factors that were held constant.

LAW OF DEMAND

States that as the price increases, the quantity demanded decreases; and as the price decreases, the quantity demanded increases, ceteris paribus.

SUPPLY

The amount of various quantities of goods and services which sellers are willing and able to sell at a given price, time and place, ceteris paribus.

Supply Schedule

The listing of the different quantities of goods and services that sellers will sell given the various alternative prices.

Market Supply

The horizontal summation of all individual supply of the consumers in the market.

Supply Curve

A plotted supply schedule.

Movement Along Supply Curve

The change in the quantity supplied due to the changes in the price of the product when all other factors are held constant.

Change in Supply

The shift in the entire supply schedule due to the changes in some factors that were held constant.

LAW OF SUPPLY

States that as the price increases, the quantity supplied also increases, and as the price decreases, the quantity supplied also decreases, ceteris paribus.

Income

The sum of all household's wages, salaries, profits, interest payments, rents and other forms of earnings in a given period of time.

Normal Good

A good for which an increase in income leads to an increase in demand, ceteris paribus.

Inferior Good

A good for which an increase in income leads to a decrease in demand, ceteris paribus.

Substitutes

Goods that can serve as replacements for one another.

Compliments

Goods that 'go together'; a decrease in the price of one results in an increase in demand for the other and vice versa.

Tastes and Preferences

Factors that determine the combinations of goods and services that a household is able to buy, influenced by individual choices.

Volatility of Tastes

The tendency of consumer preferences to change over time.

Idiosyncratic Tastes

The unique preferences of individuals that can vary widely among different people.

Expectations

Your expectations about the future may affect your demand for a good or service today.

Number of Buyers

Market demand is derived from individual demands, it depends on all those factors that determine the demand of individual buyers.

Cost of Production

For a firm to make a profit, its revenue must exceed its costs.

Price of inputs

The supply of a good is negatively related to the price of the inputs used to make the good.

Added Tax

As the added tax contributes to the price of the product, the firm decreases the supply of the product.

Technology

The invention of the machines used in production reduces the amount of labor necessary to make a product.