Financial Statements of Limited Companies

1/5

Earn XP

Description and Tags

Financial Statements of Limited Companies

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

6 Terms

Entity Concept

Separate Business from owners to provide accurate position of the business: Taxation, Performance and Cashflows

IAS 1 states we must produce:

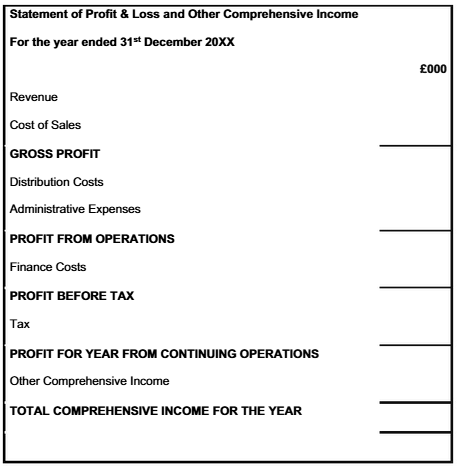

Statement of Profit or Loss and Other Comprehensive Income

Statement of Changes in Equity

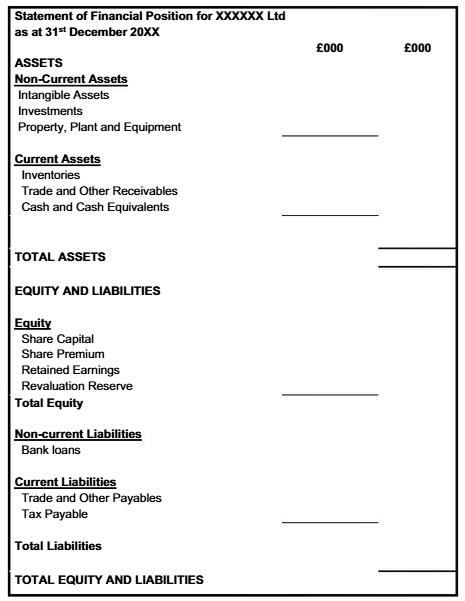

Statement of Financial Position

Statement of Cash Flows

Notes to the financial statements, including a statement of the company’s accounting policies

Companies Act requires:

A directors Report

An auditors Report (if applicable)

Typical Adjustments include:

Calculation of the depreciation expense for the year

Dealing with irrecoverable or doubtful debts/doubtful receivables

Dealing with closing inventories

Accrued and prepaid expenses and income

Corrections to errors in the way transactions have been accounted for

Inclusion of the tax charge for the year

Revaluation of non-current assets.

Changes in other reserves

Statement of Financial Position Standard layout

Statement of Profit & Loss and Other Comprehensive Income Standard Layout