ACCT 3110 Exam 4

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

36 Terms

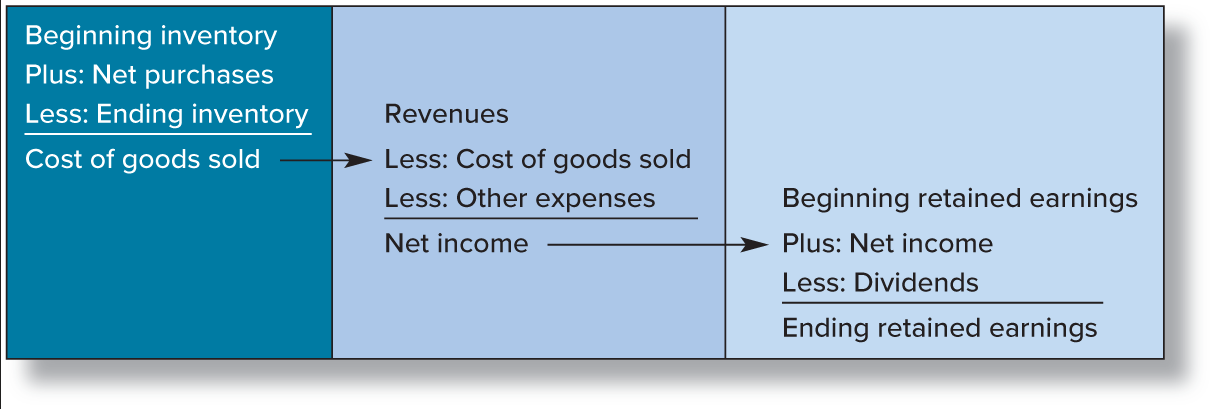

COGS equation

Beg. Inv. + Purchases + GAFS - End. Inv = COGS

Gross Profit Method

Beg. inv + net purchases = GAFS - Est. COGS = Est. End. Inv.

(Est. COGS = Net Sales * (1 - Gross Profit %))

Avg Retail Inventory Method

Cost of GAFS - Sales (retail) = End. Inv. (retail) * cost-to-retail % = End. Inv. (cost)

Cost of GAFS

Beg. Inv. + net purchases - net markdowns

Cost to retail % (avg)

GAFS (cost) / GAFS (retail)

Cost to retail % (conventional)

GAFS (cost) / GAFS (retail w/o markdown)

Conventional Retail Inventory Method

Cost of GAFS (w/ markdown) - Sales (retail) = End. Inv. (retail) * cost to retail % = Est. End. Inv. (cost)

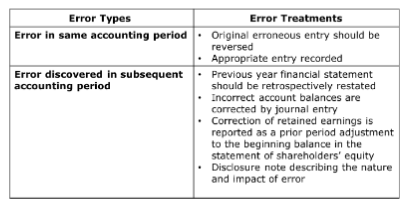

Inventory Errors

NRV from LCNRV

NRV = est. selling price - cost of completion, disposal, & transportation

Ceiling from LCM

Ceiling = NRV = selling price - est. selling cost

Floor from LCM

Floor = NRV - normal profit margin

Market from LCM

Market is the middle amount of floor, replacement cost, and ceiling

LCNRV

for companies that DON’T use LIFO or Retail Inventory Method

LCM

for companies that DO use LIFO or Retail Inventory Method

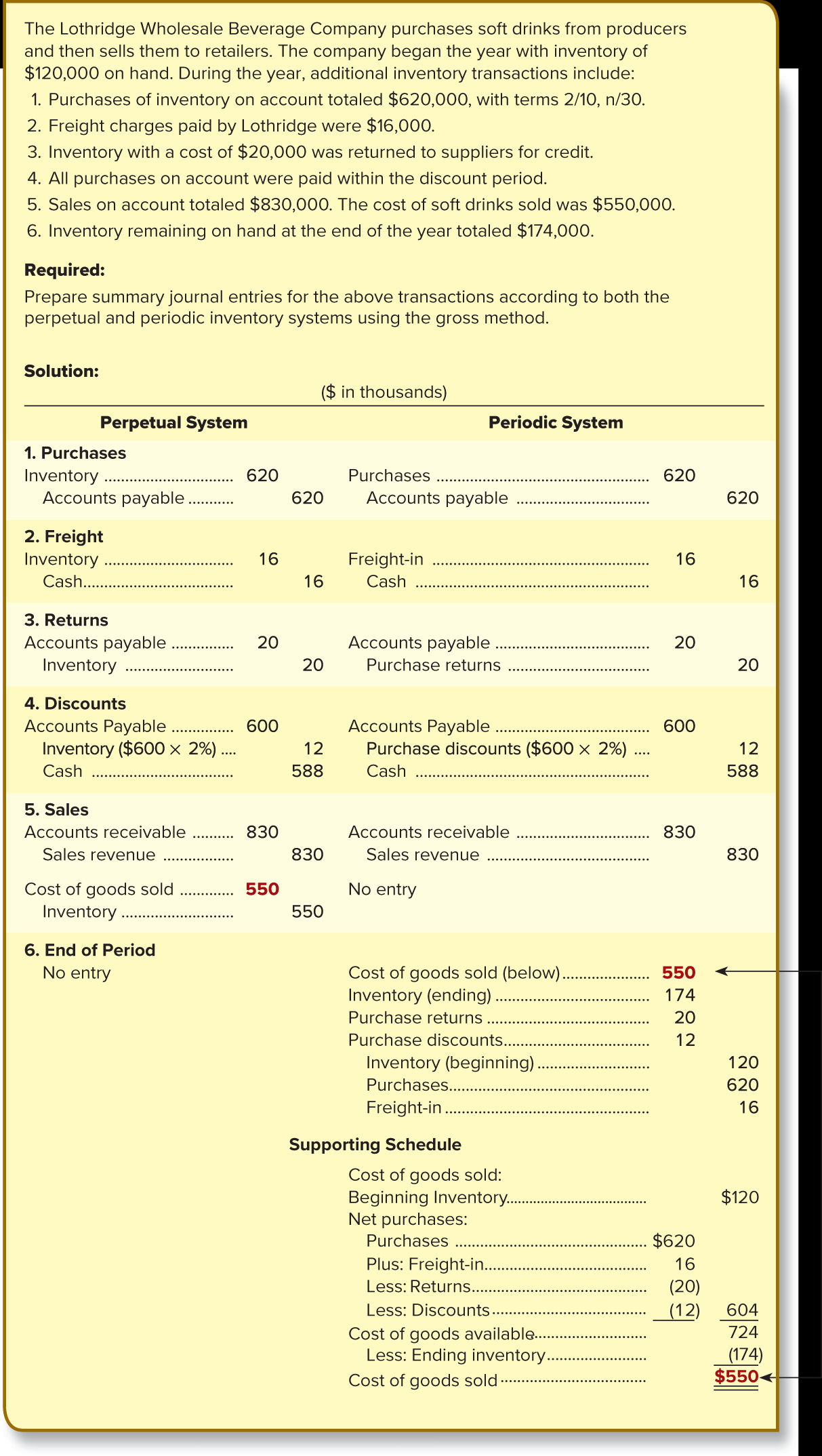

Perpetual Inventory System

continually adjust inventory acct for each change in inventory and COGS acct each time goods are sold or returned

Periodic Inventory System

adjusts inventory and records COGS only at the end of each reporting period. records inventory changes in temporary accts

FOB shipping point

legal title passes to buyer at a point of shipment

FOB destination

legal title passes to buyer when goods arrive at destination

Goods on consignment

A company (consignor) arranges for another company (consignee) to sell its product under consignment

Weighted avg unit cost

Cost of GAFS / quantity available for sale

Weighted avg - periodic

COGS = weighted avg per unit X units sold

only calculated at end of period

Weighted avg - perpetual

(cost of previous inventory + cost of new purchases) / # units on hand

FIFO

end inventory consists of most recently acquired units. Periodic amount = perpetual amount

LIFO - periodic

units sold are priced at most recent units purchased

LIFO - perpetual

each time inventory is purchased/ sold, LIFO layers adjust bc “most recent” items purchased changes as time passes

LIFO liquidation

removes entire current year year and some of beginning inventory / end inventory of previous year; some of “old” inventory is liquidated

LIFO inventory pools

groups inventory units into pools based on physical similarities of individual units and reduce the risk of LIFO liquidation

Dollar value LIFO

allows company to combine large variety of goods into one pool. inventory viewed as quantity of value than physical quantity

Cost index in base yr

1.00

Cost index in layer yr

cost in layer yr / cost in base yr

Error reporting

Periodic vs Perpetual

Change in Inventory methods - perpetual

dr inventory (new - old) cr retained earnings vice versa if old amount is larger than new amount

(Est.) loss on purchase commitment

Contract price - current market price at year-end

Year-End adjusting for purchase commitment

dr est. loss on purchase commitment cr est. liability on purchase commitment *for commitments in next period

Journal entry for purchase of purchase commitment

dr inventory dr loss on purchase commitment (difference) dr est. liability of commitment (from adj. entry) cr cash