Looks like no one added any tags here yet for you.

Cost To Buy (CTB)

PxQ

Cost To Make (CTM)

FC + (AVC xQ)

CPU

P - AVC

Total Contribution

TR - TVC or CPU x Q

Profit (from contibution)

Profit = Total Contribution - FC

Profit (from Revenue)

TR - TC

TR

TR = P x Q

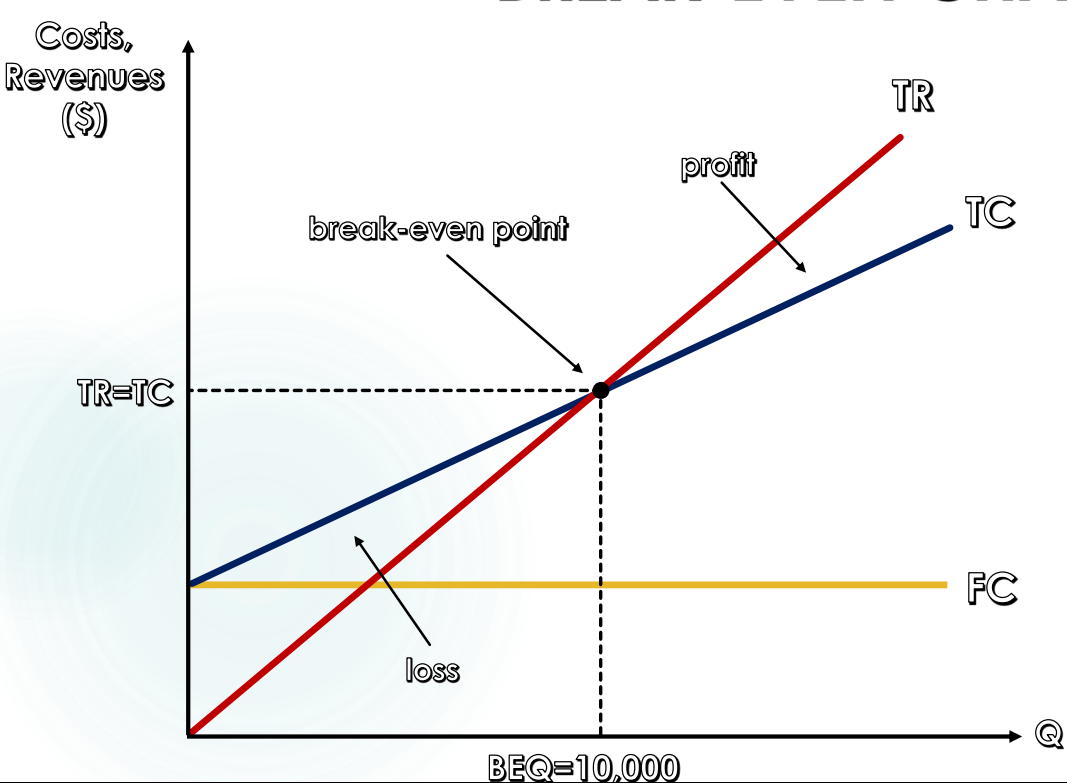

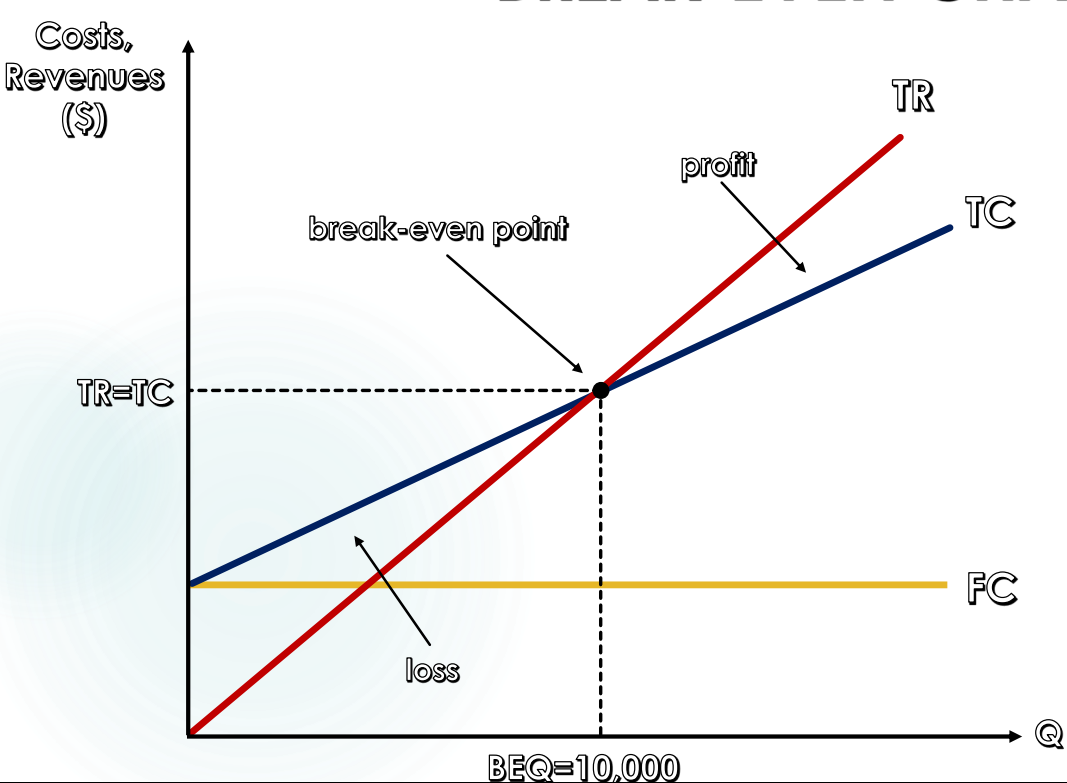

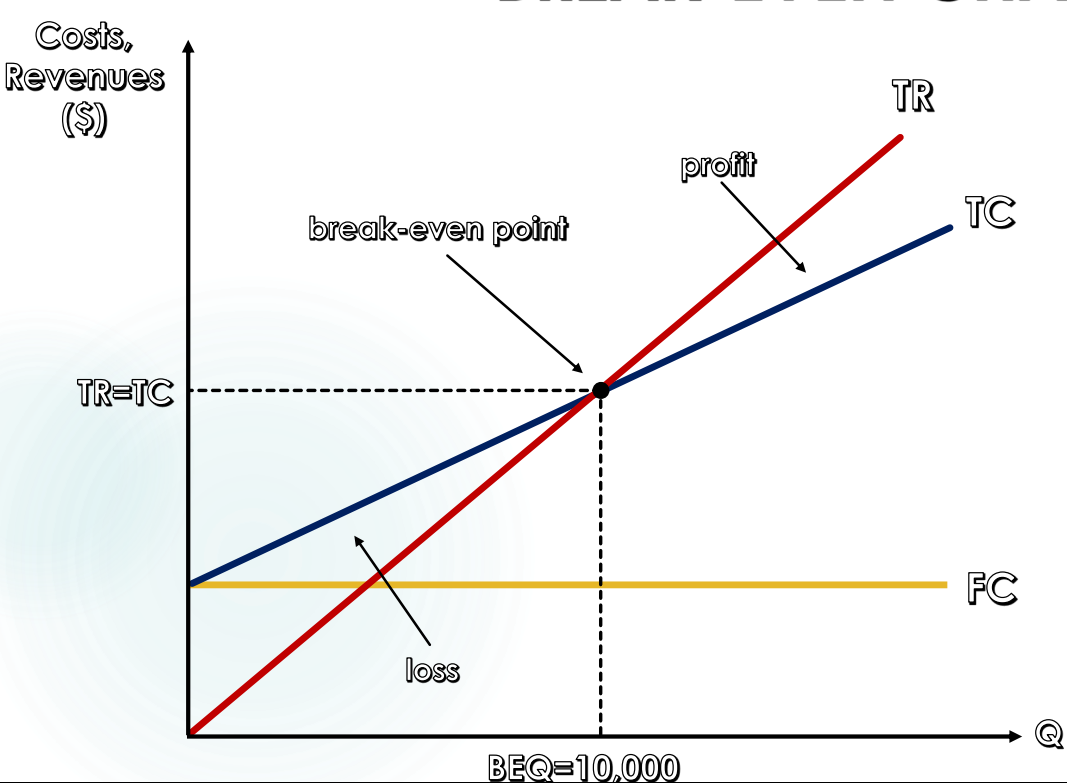

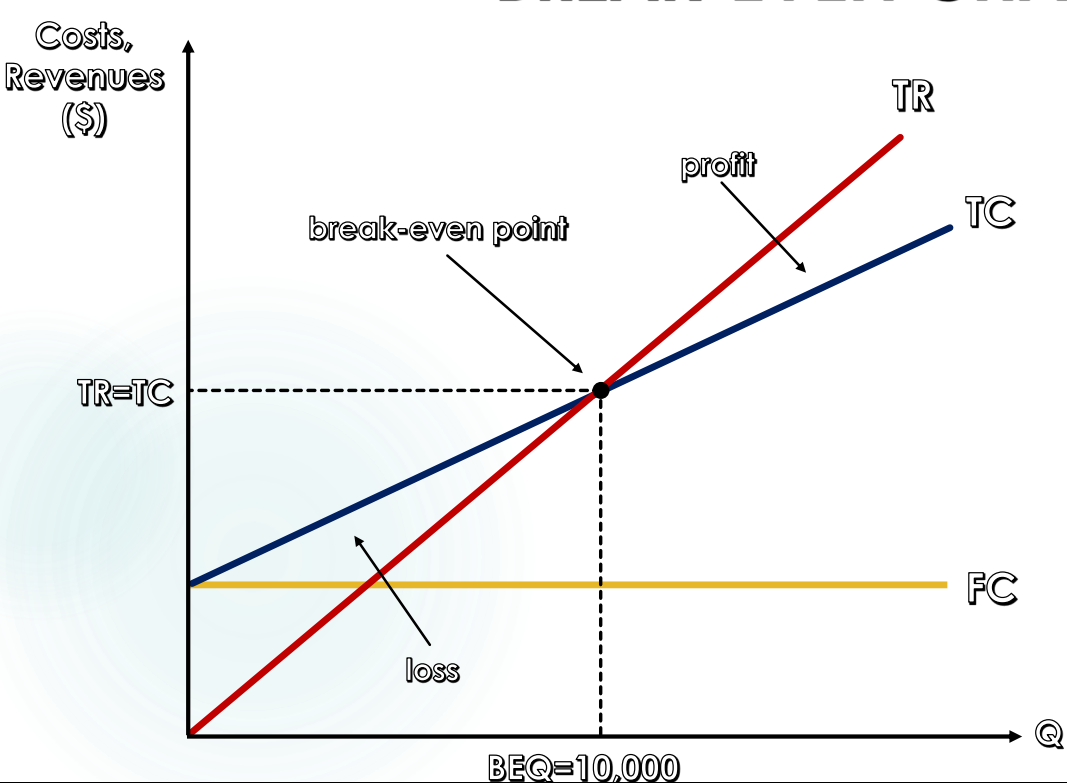

Break - even quantity

where TC = TR or FC/CPU

Target Profit Output

(FC + Target profit)/CPU

Break - even Revenue

FC / CPU x P

Break - even Price

FC / Q + Direct Cost per Unit

MAKE OR BUY (OUTSOURCING) DECISON

A judgment made by management whether to make a component internally or buy it from the market.

CONTRIBUTION

The sum of money that remains after all direct and variable costs have been taken away from the sales revenue.

CONTRIBUTION COSTING

A method of valuing costs by allocating direct costs to products or divisions (departments) of a business. Overheads are not accounted.

COST CENTRE

A section of business where costs are incurred and recorded (not involved in making profit).

ABSORPTION COSTING

A method of calculating taking in to consideration all types of costs. It involves making decisions about apportion a firm's indirect or fixed costs.

PROFIT CENTRE

A section of business where both costs and revenues are identified and recorded.

COSTS

The sum of money incurred by a business in the production process, e.g., the costs of raw materials, wages and salaries, insurance, advertising and rent.

Fixed costs (FC)

Costs that do not change with the amount of goods or services produced;

Variable costs (VC)

Costs that do change with the amount of goods or services produced.

DIRECT COSTS

Costs that can be identified with the production of specific product (cost centre), e.g., raw materials, direct labour

INDIRECT COSTS (OVERHEADS)

Costs that are not clearly identified with the production of specific product, e.g., advertising, interests on loans, legal expences, insurance

REVENUE

Income that a firm receives from selling its products.

REVENUE STREAMS

Income that an organisation gets from a particular activity.