Production, Costs, and Industry Structure in Microeconomics

1/56

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

57 Terms

Private enterprise

the ownership of businesses by private individuals

Production

the process of combining inputs to produce outputs

Firm

an organization that combines inputs of labor, capital, land, and raw or finished component materials to produce outputs.

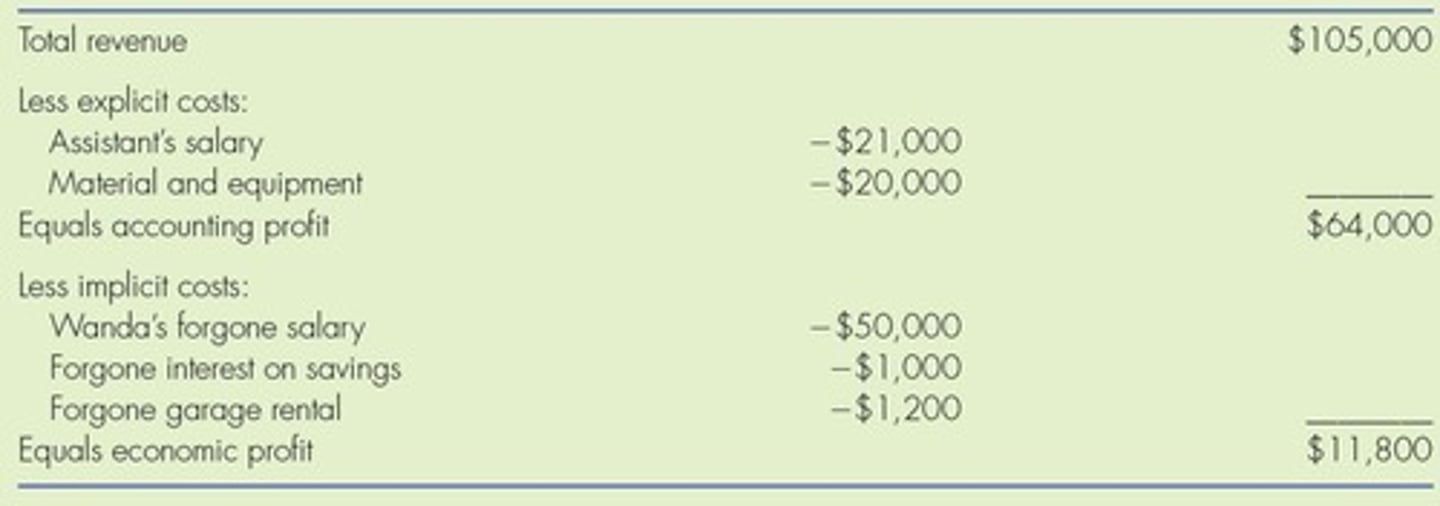

Revenue

the income a firm generates from selling its products.

Profit

the difference between total revenue and the opportunity costs of resources used in production

Total Cost

consists of Explicit and Implicit costs

Explicit costs

out-of-pocket costs; actual outgoing payments showing on the accounting statement.

Implicit costs

the opportunity cost of using resources that the firm already owns.

Accounting profit

the difference between dollars brought in and dollars paid out, does not account for implicit costs.

Economic profit

takes both explicit and implicit costs into account.

Production function

mathematical equation that tells how much output (Q) a firm can produce with given amounts of the inputs.

Fixed inputs

factors of production that can't be easily increased or decreased in a short period of time

Variable inputs

factors of production that a firm can easily increase or decrease in a short period of time

Short run

period of time during which at least some factors of production are fixed.

Long run

period of time during which all factors are variable.

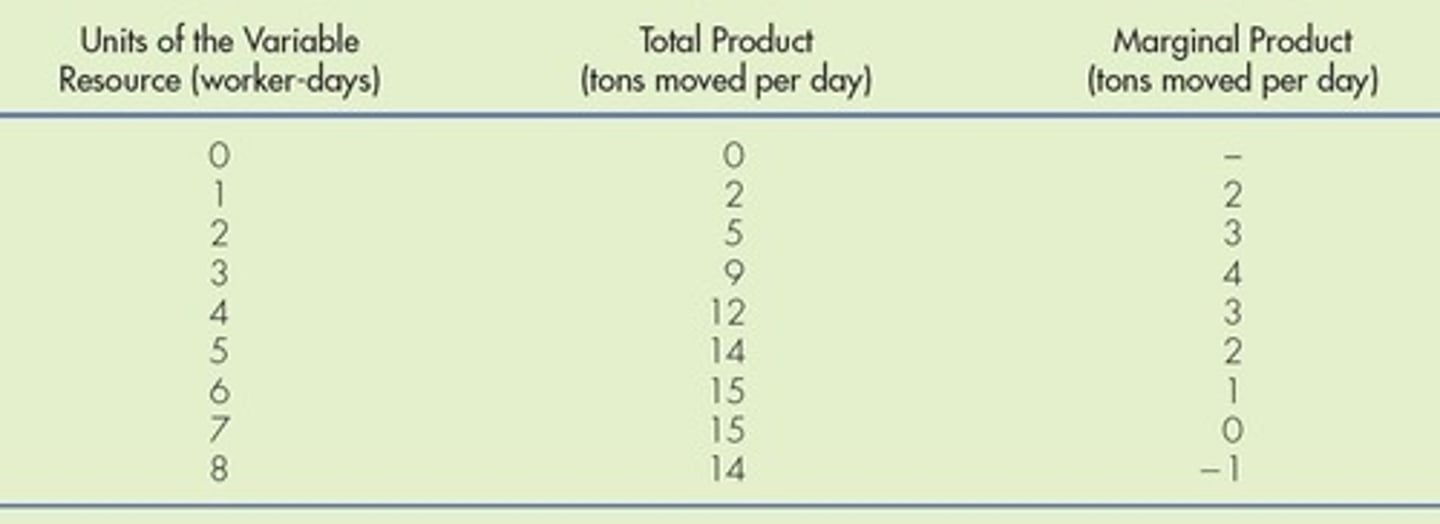

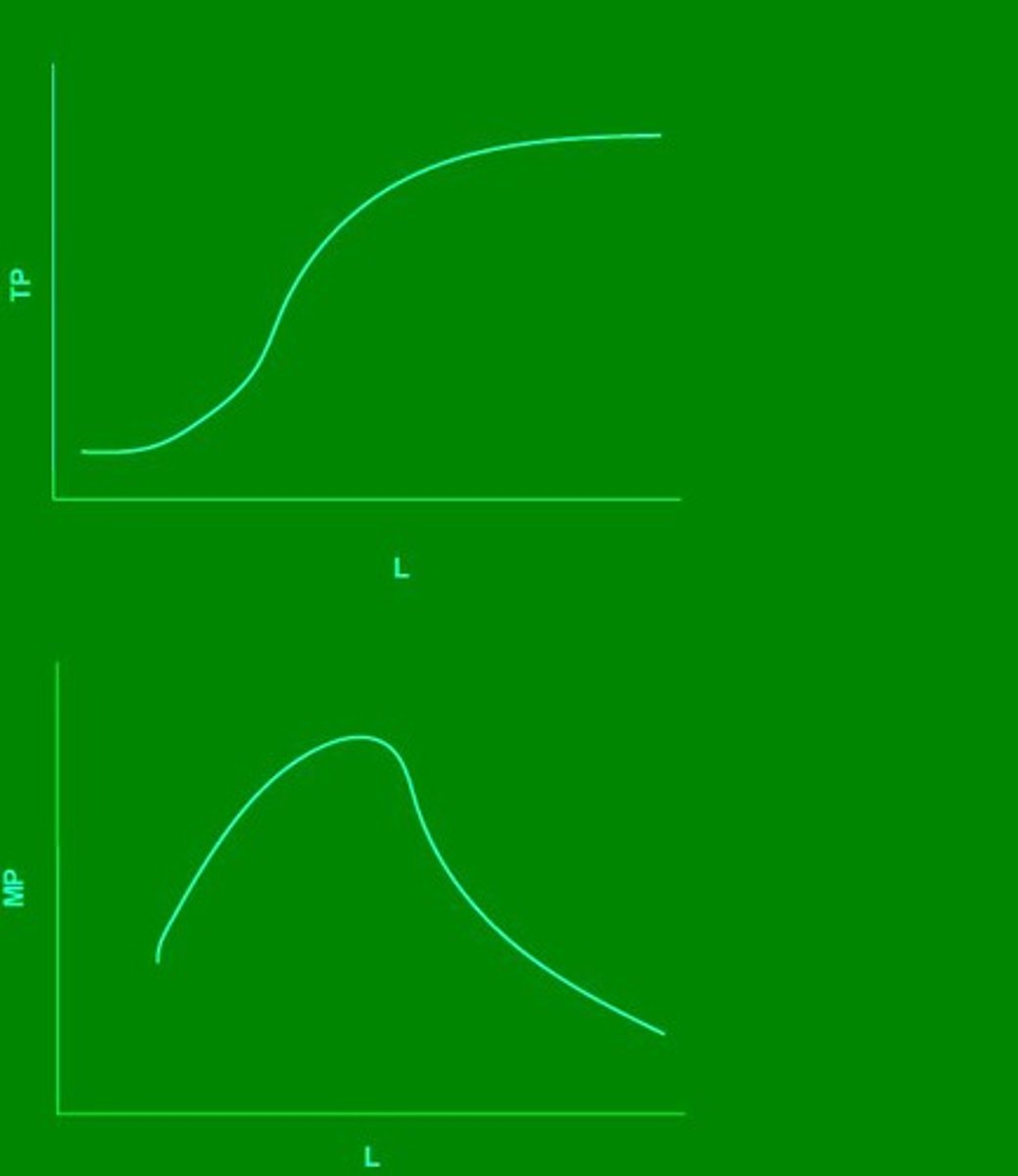

Total product (TP)

the firm's total output.

Marginal product (MP)

Change in total product from an additional unit of resource

Law of Diminishing Marginal Productivity

general rule that as a firm employs more of one variable input, eventually the amount of additional output produced as a result of adding one more unit of that input declines.

Marginal cost (MC)

Change in total cost resulting from a one-unit change in output

Variable costs (VC)

costs of the variable inputs, like labor.

Fixed costs (FC)

costs of the fixed inputs, like rent.

Total cost (TC)

the sum of fixed and variable costs of production

Total Cost Formula

TC = FC + VC

Marginal Cost Formula

MC = ∆TC/∆q

Increasing marginal returns

MC falls

Diminishing marginal returns

MC increases

Total product curve

general case of total product curve.

Marginal product curve

general case of marginal product curve.

Average Variable Cost (AVC)

Variable cost divided by quantity produced.

Average Fixed Cost (AFC)

Fixed cost divided by quantity produced.

Average Total Cost (ATC)

Total cost divided by output or sum of AVC and AFC.

Marginal Cost (MC)

Additional cost of producing one more unit.

U-shaped Cost Curves

Average costs decline, reach minimum, then rise.

Law of Diminishing Marginal Returns

Adding input yields progressively smaller increases in output.

Average Profit

Price minus average cost; indicates profitability.

Sunk Cost

Costs that cannot be recovered once incurred.

Long Run

Period when all costs are variable.

Economies of Scale

Lower average costs as production scale increases.

Diseconomies of Scale

Higher average costs as production scale increases.

Long-Run Average Cost Curve

Lowest average cost at each output level.

Constant Returns to Scale

Average cost remains unchanged with proportional input changes.

Minimum Efficient Scale

Lowest output level for full economies of scale.

Short-Run Average Total Cost Curves

Curves representing average costs for different plant sizes.

Planning Curve

Long-run average cost curve; U-shaped.

Traffic Congestion

Increased costs due to overcrowding in operations.

Fixed Costs

Costs that do not change with output level.

Variable Costs

Costs that vary directly with output level.

Average Cost Intersection

Where MC intersects AVC or ATC indicates minimum point.

Output Level R

Point where low-cost firms operate efficiently.

Output Level A

Minimum efficient scale; lowest average cost achieved.

Output Level B

Point beyond which diseconomies of scale occur.

Short-Run Costs

Costs when at least one input is fixed.

Long-Run Planning

Firms adjust all inputs for optimal production.

Cost of Hiring Barbers

Variable cost incurred per barber employed.

Overhead

Common term for fixed costs in business.

Cost Curves Graph

Visual representation of MC, AVC, and ATC.

Barbershop Fixed Costs

Costs like space and equipment for operation.