Elasticity, Supply and Competition

1/38

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

39 Terms

Competition

The rivalry between firms or producers in a market.

Elasticity

Responsiveness of quantity demanded to price changes.

Shifts in Supply

Changes in supply caused by various factors except price.

increase = shift to right

decrease = shift to left

Movements Along Supply Curve

Changes in supply due to price changes

Cost of Production

Costs for a producer to produce a good / service.

PINTS WC (Factors impacting supply / causing shift)

Productivity

Indirect taxes

Number of Firms

Technology

Subsidies

Weather and disease

Cost of production

How does technology affect supply?

Advancements in technology means increase productivity and supply.

How do taxes affect supply?

Government levies that affect production costs, and therefore incentives to supply.

How do subsidies affect supply?

Government payments to lower production costs, therefore increase incentive to supply.

How does the weather affect supply?

Environmental conditions affecting agricultural supply.

How do Prices of Other Goods affect supply?

Influence of substitute goods on production decisions and supply incentives.

How do the number of firms affect supply?

More total firms in an industry increases supply levels.

Economies of Scale

Cost advantages from increased production levels.

Efficiency

The measure of how well scarce resources are used to produce final goods / services.

Increased supply means what to sales?

Increased supply may lead to higher sales volume.

Monopoly

Market dominance by a single firm.

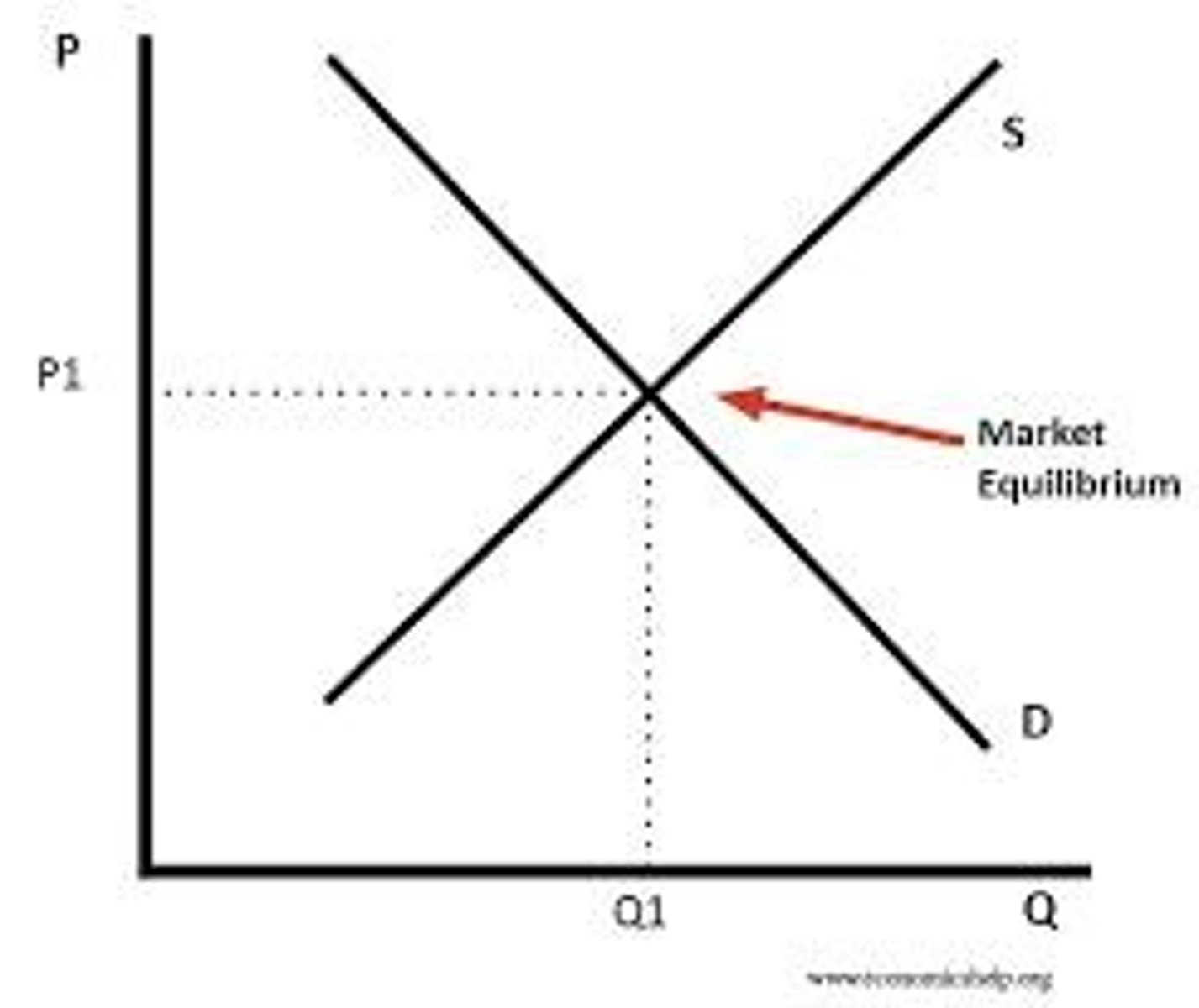

Equilibrium

State where quantity supplied equals quantity demanded.

Market Equilibrium

Planned demand equals planned supply in the market.

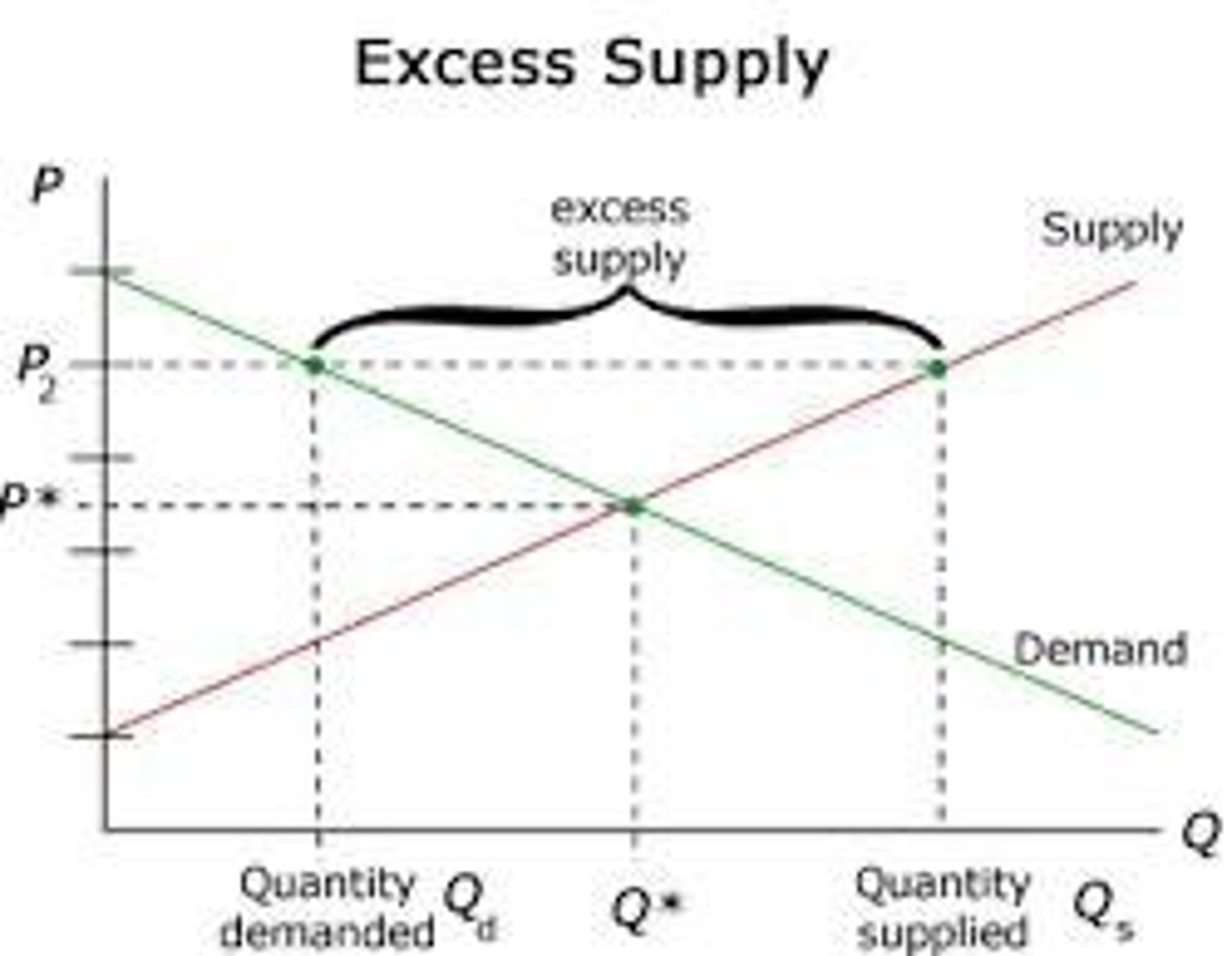

Excess Supply

When supply exceeds demand at a given price.

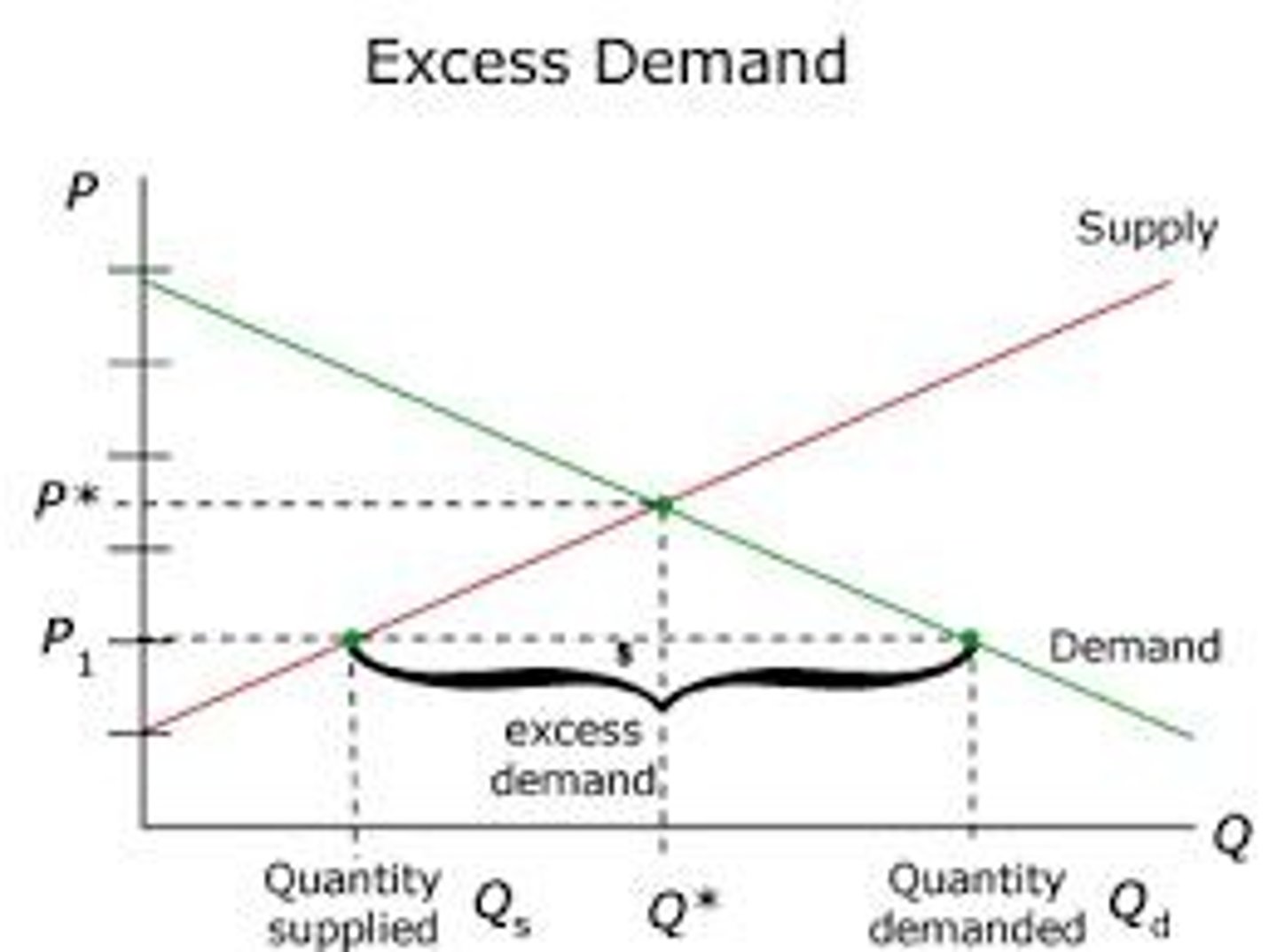

Excess Demand

When demand exceeds supply at a given price.

Firm Reaction to Excess Supply

Lower prices to sell unsold stock.

Firm Reaction to Excess Demand

Increase prices to balance supply and demand. (demand will lower)

Price Elasticity of Supply (PES)

Measure of how much supply changes with price.

What is perfect competition?

Market structure where a large number of firms sell homogeneous products and there are no obstacles to entry or exit of firms into the market.

Perfect Competition conditions:

- Large number of buyers and sellers

- Perfect market information

- Able to sell/buy as much as they wish at the ruling market price

- Unable to influence ruling market price

- Homogenous/identical products

- No barriers to entry or exit in the long run

What is monopolistic competition?

Market structure where large number of firms are competing in a market, each having enough product differentiation to achieve a degree of monopolistic power, and therefore have some power over the price they charge.

E.g. local restaurants, hair salons, local pubs.

What is an oligopoly?

Market structure where control over the supply of a product is in the hands of a small number of producers and each one can influence prices and affect competition.

E.g. O2, EE, Vodafone

What is a duopoly?

A market structure where there are only two firms in the market.

What is a monopoly?

Market structure in which there is only one producer / seller for a product, and the only business in an industry. A monopoly would have 100% market share.

What is a business monopoly?

When one business controls 25% or more of a particular market, whilst not being a complete monopoly and having other competitors.

What market structure is best for consumers and why?

Perfect competition

- lower prices

- more choice

What market structure is worse for consumers and why?

Monopolies

- high prices

- little choice

What are potential gains of competitive markets to consumers?

- prices will be lower

- lots of choice in market

- quality may be constantly improving

- incentive to innovate and produce new products as firms try to stay ahead of competition

What are the potential gains of competitive markets to firms?

- likely to be more efficient and have lower production costs

- may be easier to attract workers as there are lots of workers doing the same job

What are the potential losses of competitive markets to firms?

- prices likely to be driven much lower than in less competitive markets - may lead to reduced profit margins

- Lower profit margins may mean less funds available for re-investment

- a constant pressure to cut costs to be efficient

What are the potential gains in monopolistic markets to consumers?

- large firms may benefit from economics of scale, meaning firms may choose to pass on benefits of this to consumer in the form of lower prices

- product quality and range may be higher because (a): have profits to re-invest (b): they have incentive to do so as they want to keep their monopolistic power

What are potential gains of monopolistic markets to firms?

- prices are likely to be more price inelastic, meaning they can keep prices higher

- lack of competition means higher prices and therefore higher profit margins

- no pressure to constantly lower costs

What are potential losses of monopolistic markets to consumers?

- less competition is likely, so this means higher prices

- less choice in the market

- product quality and range/consumer service may decline - monopolies have a captured market

What are potential losses of monopolistic markets to firms?

- lack of competitive pressures may make this firm become stale and unresponsive to consumer demand